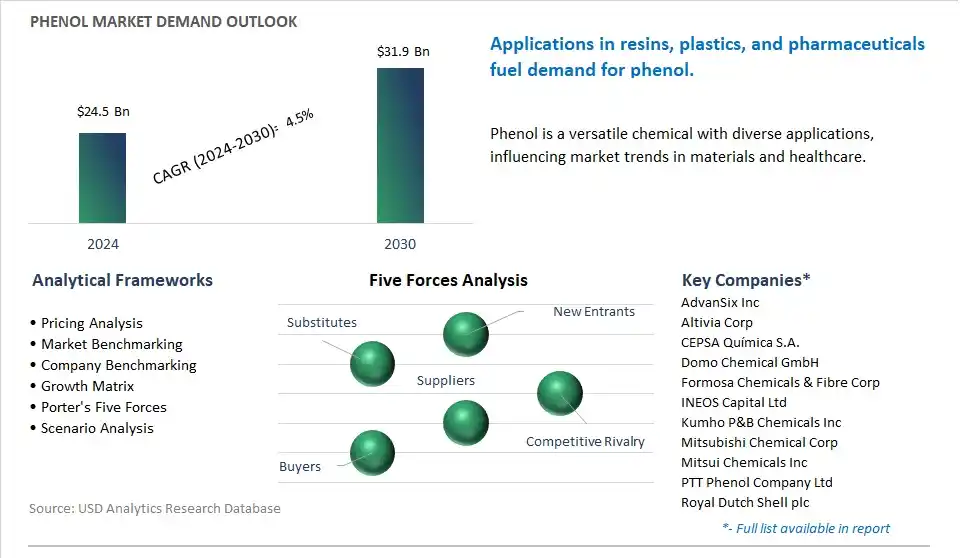

The global Phenol Market is poised to register a 4.5% CAGR from $24.5 Billion in 2024 to $31.9 Billion in 2030.

The global Phenol Market Study analyzes and forecasts the market size across 6 regions and 24 countries for diverse segments -By Product (Phenolic Resins Caprolactum Bisphenol-A Others), By Manufacturing Process (Cumene Process, Dow Process, Ranching–Hooker Process), By Classification (Monohydric, Dihydric, Trihydric), By Application (Epoxy Resins, Polycarbonates, Nylon, Bakelite, Detergents, Phenolic Resins, Pharmaceutical Drugs, Herbicides).

An Introduction to Global Phenol Market in 2024

The market for phenol is witnessing growth driven by its diverse applications in industries such as chemicals, plastics, pharmaceuticals, and electronics. One key trend shaping the future of the industry is the increasing demand for phenol derivatives such as bisphenol A (BPA), phenolic resins, and caprolactam in downstream applications such as polycarbonate plastics, epoxy resins, and nylon production. Phenol, produced primarily from petroleum-based feedstocks or by the cumene process, serves as a key building block for a wide range of chemicals and materials used in construction, automotive, electronics, and consumer goods. This trend is driving investments in phenol production capacities, process technologies, and feedstock diversification to ensure a stable and cost-effective supply chain for downstream industries while reducing environmental impact and dependency on fossil fuels. Moreover, the expanding market for specialty chemicals and advanced materials is driving innovation in phenol derivatives such as phenolic antioxidants, flame retardants, and heat-resistant polymers, enabling the development of high-performance products for demanding applications in aerospace, automotive, and electronic components. Additionally, the growing focus on sustainability and circular economy principles is driving the adoption of bio-based phenol production technologies such as lignin depolymerization, biocatalysis, and microbial fermentation, enabling the production of renewable phenol from biomass feedstocks such as wood, agricultural residues, and industrial waste streams. Furthermore, the integration of phenol derivatives into pharmaceuticals, disinfectants, and personal care products is driving market growth, driven by their antiseptic, antibacterial, and preservative properties, as well as their role in formulations for healthcare, hygiene, and infection control applications.

Phenol Market Competitive Landscape

The market report analyses the leading companies in the industry including AdvanSix Inc, Altivia Corp, CEPSA Química S.A., Domo Chemical GmbH, Formosa Chemicals & Fibre Corp, INEOS Capital Ltd, Kumho P&B Chemicals Inc, Mitsubishi Chemical Corp, Mitsui Chemicals Inc, PTT Phenol Company Ltd, Royal Dutch Shell plc, Solvay SA.

Phenol Market Dynamics

Phenol Market Trend: Increasing Demand for Bisphenol-A Alternatives

A prominent trend in the phenol market is the increasing demand for alternatives to bisphenol-A (BPA), driven by growing concerns over its potential health and environmental impacts. Bisphenol-A is a key derivative of phenol commonly used in the production of polycarbonate plastics and epoxy resins, but its use has come under scrutiny due to its endocrine-disrupting properties and potential adverse effects on human health. As a result, there is a rising demand for BPA-free alternatives in various applications, including food and beverage packaging, thermal paper coatings, and consumer products. Manufacturers are exploring and developing phenol-based compounds that offer similar performance characteristics to BPA but without the associated health risks, driving market growth and innovation in the phenol industry towards safer and more sustainable alternatives.

Phenol Market Driver: Expansion of End-Use Industries and Chemical Manufacturing

A key driver propelling the phenol market is the expansion of end-use industries and chemical manufacturing sectors that rely on phenol and its derivatives for a wide range of applications. Phenol is a versatile chemical compound used as a precursor in the production of various downstream products, including phenolic resins, caprolactam, bisphenol-A, and alkylphenols, which find extensive use in automotive, construction, electronics, pharmaceuticals, and agriculture sectors. The steady growth in industrial activities, urbanization, infrastructure development, and consumer demand drives the demand for phenol-based products and fuels market expansion. Additionally, advancements in chemical synthesis technologies and process optimization contribute to increased production capacity and cost competitiveness, further stimulating market growth and driving investment in the phenol industry.

Phenol Market Opportunity: Focus on Sustainable Production Processes and Renewable Feedstocks

An opportunity for market differentiation and growth lies in the focus on sustainable production processes and renewable feedstocks for phenol manufacturing. With growing emphasis on environmental sustainability and regulatory compliance, there is a push towards reducing carbon emissions, minimizing waste generation, and optimizing resource utilization in chemical production processes. Manufacturers can capitalize on this opportunity by adopting greener manufacturing technologies such as biomass conversion, hydrogenation of benzene, and catalytic oxidation of cumene, which offer lower environmental impact and energy consumption compared to conventional phenol production methods. Additionally, the use of renewable feedstocks such as lignin, biomass, and agricultural residues as alternative sources of phenol precursor materials presents an opportunity to reduce reliance on fossil resources and promote circular economy principles. By investing in sustainable production practices and leveraging renewable feedstock options, companies can enhance their competitiveness, meet evolving market demands for eco-friendly products, and secure long-term growth opportunities in the phenol market.

Phenol Market Share Analysis: Phenolic Resins segment generated the highest revenue in the industry

The Phenolic Resins segment is the largest segment in the Phenol Market due to diverse key factors contributing to its dominance. Phenolic resins are versatile synthetic polymers derived from phenol and formaldehyde, widely used in various industries for their excellent mechanical, thermal, and electrical properties. One of the primary reasons for the dominance of phenolic resins is their extensive applications across multiple sectors, including automotive, construction, electronics, aerospace, and consumer goods. In the automotive industry, phenolic resins are used for manufacturing brake pads, clutch discs, and other friction materials due to their high heat resistance and frictional stability. In the construction sector, they find applications in manufacturing laminates, coatings, adhesives, and insulation materials, where their fire resistance and durability are valued. In addition, phenolic resins are indispensable in the electronics industry for producing printed circuit boards (PCBs) and electrical insulating materials due to their excellent electrical properties and dimensional stability. Additionally, phenolic resins are utilized in consumer goods such as kitchen countertops, household appliances, and furniture laminates, where their durability, moisture resistance, and aesthetic appeal are desirable. Further, the ongoing advancements in phenolic resin technology, including the development of low-emission formulations and sustainable bio-based alternatives, further drive their adoption across industries. With their diverse applications, superior performance characteristics, and ongoing innovations, phenolic resins maintain their position as the largest segment in the Phenol Market.

Phenol Market Share Analysis: Cumene Process Segment is poised to register the fastest growth rate (CAGR) over the forecast period to 2030

The Cumene Process segment is the fastest growing segment in the Phenol Market due to diverse key factors driving its rapid expansion. The Cumene Process is the most widely used method for commercial phenol production, accounting for a significant share of global phenol production capacity. This process involves the reaction of benzene with propylene to form cumene, followed by oxidation of cumene to produce phenol and acetone as co-products. One of the primary reasons for the dominance of the Cumene Process is its efficiency and cost-effectiveness compared to alternative manufacturing methods. The process offers high yields of phenol and acetone, making it economically attractive for large-scale production. In addition, advancements in process technology and catalyst development have improved the efficiency and environmental sustainability of the Cumene Process, reducing energy consumption, emissions, and waste generation. Additionally, the growing demand for phenol and its derivatives in various end-use industries, such as automotive, construction, electronics, and pharmaceuticals, further drives the adoption of the Cumene Process for phenol production. As industries continue to expand and innovate, particularly in emerging markets, the demand for phenol derived from the Cumene Process is expected to surge, making it the fastest growing segment in the Phenol Market.

Phenol Market Share Analysis: Trihydric Segment is poised to register the fastest growth rate (CAGR) over the forecast period to 2030

The Trihydric segment is the fastest growing segment in the Phenol Market due to diverse key factors driving its rapid expansion. Trihydric phenols, also known as polyphenols, are compounds containing three hydroxyl (OH) groups attached to a phenolic ring. These compounds exhibit unique antioxidant, antimicrobial, and anti-inflammatory properties, making them increasingly sought after for various applications in industries such as pharmaceuticals, food and beverages, personal care, and cosmetics. In the pharmaceutical industry, trihydric phenols are utilized for their potential therapeutic benefits, including cardiovascular protection, anti-aging effects, and anticancer properties. In addition, trihydric phenols are used as natural antioxidants and preservatives in food and beverage formulations to extend shelf life and maintain product quality. In the personal care and cosmetics industry, these compounds are incorporated into skincare, haircare, and cosmetic products for their skin-rejuvenating, moisturizing, and UV-protective properties. Additionally, the growing consumer awareness of the health and wellness benefits associated with natural ingredients drives the demand for trihydric phenols derived from botanical sources such as green tea, grapes, and berries. As consumers increasingly seek natural and sustainable alternatives in their products, the demand for trihydric phenols is expected to continue rising, making it the fastest growing segment in the Phenol Market.

Phenol Market Report Segmentation

By Product

Phenolic Resins

Caprolactum

Bisphenol-A

Others

By Manufacturing Process

Cumene Process

Dow Process

Ranching–Hooker Process

By Classification

Monohydric

Dihydric

Trihydric

By Application

Epoxy Resins

Polycarbonates

Nylon

Bakelite

Detergents

Phenolic Resins

Pharmaceutical Drugs

Herbicides

Regions Included

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Phenol Companies Profiled in the Market Study

AdvanSix Inc

Altivia Corp

CEPSA Química S.A.

Domo Chemical GmbH

Formosa Chemicals & Fibre Corp

INEOS Capital Ltd

Kumho P&B Chemicals Inc

Mitsubishi Chemical Corp

Mitsui Chemicals Inc

PTT Phenol Company Ltd

Royal Dutch Shell plc

Solvay SA

*- List Not Exhaustive

TABLE OF CONTENTS

1 Introduction to 2024 Phenol Market

1.1 Market Overview

1.2 Quick Facts

1.3 Scope/Objective of the Study

1.4 Market Definition

1.5 Countries and Regions Covered

1.6 Units, Currency, and Conversions

1.7 Industry Value Chain

2 Research Methodology

2.1 Market Size Estimation

2.2 Sources and Research Methodology

2.3 Data Triangulation

2.4 Assumptions and Limitations

3 Executive Summary

3.1 Global Phenol Market Size Outlook, $ Million, 2021 to 2030

3.2 Phenol Market Outlook by Type, $ Million, 2021 to 2030

3.3 Phenol Market Outlook by Product, $ Million, 2021 to 2030

3.4 Phenol Market Outlook by Application, $ Million, 2021 to 2030

3.5 Phenol Market Outlook by Key Countries, $ Million, 2021 to 2030

4 Market Dynamics

4.1 Key Driving Forces of Phenol Industry

4.2 Key Market Trends in Phenol Industry

4.3 Potential Opportunities in Phenol Industry

4.4 Key Challenges in Phenol Industry

5 Market Factor Analysis

5.1 Value Chain Analysis

5.2 Competitive Landscape

5.2.1 Global Phenol Market Share by Company (%), 2023

5.2.2 Product Offerings by Company

5.3 Porter’s Five Forces Analysis

5.4 Pricing Analysis and Outlook

6 Growth Outlook Across Scenarios

6.1 Growth Analysis-Case Scenario Definitions

6.2 Low Growth Scenario Forecasts

6.3 Reference Growth Scenario Forecasts

6.4 High Growth Scenario Forecasts

7 Global Phenol Market Outlook by Segments

7.1 Phenol Market Outlook by Segments, $ Million, 2021- 2030

By Product

Phenolic Resins

Caprolactum

Bisphenol-A

Others

By Manufacturing Process

Cumene Process

Dow Process

Ranching–Hooker Process

By Classification

Monohydric

Dihydric

Trihydric

By Application

Epoxy Resins

Polycarbonates

Nylon

Bakelite

Detergents

Phenolic Resins

Pharmaceutical Drugs

Herbicides

8 North America Phenol Market Analysis and Outlook To 2030

8.1 Introduction to North America Phenol Markets in 2024

8.2 North America Phenol Market Size Outlook by Country, 2021-2030

8.2.1 United States

8.2.2 Canada

8.2.3 Mexico

8.3 North America Phenol Market size Outlook by Segments, 2021-2030

By Product

Phenolic Resins

Caprolactum

Bisphenol-A

Others

By Manufacturing Process

Cumene Process

Dow Process

Ranching–Hooker Process

By Classification

Monohydric

Dihydric

Trihydric

By Application

Epoxy Resins

Polycarbonates

Nylon

Bakelite

Detergents

Phenolic Resins

Pharmaceutical Drugs

Herbicides

9 Europe Phenol Market Analysis and Outlook To 2030

9.1 Introduction to Europe Phenol Markets in 2024

9.2 Europe Phenol Market Size Outlook by Country, 2021-2030

9.2.1 Germany

9.2.2 France

9.2.3 Spain

9.2.4 United Kingdom

9.2.4 Italy

9.2.5 Russia

9.2.6 Norway

9.2.7 Rest of Europe

9.3 Europe Phenol Market Size Outlook by Segments, 2021-2030

By Product

Phenolic Resins

Caprolactum

Bisphenol-A

Others

By Manufacturing Process

Cumene Process

Dow Process

Ranching–Hooker Process

By Classification

Monohydric

Dihydric

Trihydric

By Application

Epoxy Resins

Polycarbonates

Nylon

Bakelite

Detergents

Phenolic Resins

Pharmaceutical Drugs

Herbicides

10 Asia Pacific Phenol Market Analysis and Outlook To 2030

10.1 Introduction to Asia Pacific Phenol Markets in 2024

10.2 Asia Pacific Phenol Market Size Outlook by Country, 2021-2030

10.2.1 China

10.2.2 India

10.2.3 Japan

10.2.4 South Korea

10.2.5 Indonesia

10.2.6 Malaysia

10.2.7 Australia

10.2.8 Rest of Asia Pacific

10.3 Asia Pacific Phenol Market size Outlook by Segments, 2021-2030

By Product

Phenolic Resins

Caprolactum

Bisphenol-A

Others

By Manufacturing Process

Cumene Process

Dow Process

Ranching–Hooker Process

By Classification

Monohydric

Dihydric

Trihydric

By Application

Epoxy Resins

Polycarbonates

Nylon

Bakelite

Detergents

Phenolic Resins

Pharmaceutical Drugs

Herbicides

11 South America Phenol Market Analysis and Outlook To 2030

11.1 Introduction to South America Phenol Markets in 2024

11.2 South America Phenol Market Size Outlook by Country, 2021-2030

11.2.1 Brazil

11.2.2 Argentina

11.2.3 Rest of South America

11.3 South America Phenol Market size Outlook by Segments, 2021-2030

By Product

Phenolic Resins

Caprolactum

Bisphenol-A

Others

By Manufacturing Process

Cumene Process

Dow Process

Ranching–Hooker Process

By Classification

Monohydric

Dihydric

Trihydric

By Application

Epoxy Resins

Polycarbonates

Nylon

Bakelite

Detergents

Phenolic Resins

Pharmaceutical Drugs

Herbicides

12 Middle East and Africa Phenol Market Analysis and Outlook To 2030

12.1 Introduction to Middle East and Africa Phenol Markets in 2024

12.2 Middle East and Africa Phenol Market Size Outlook by Country, 2021-2030

12.2.1 Saudi Arabia

12.2.2 UAE

12.2.3 Oman

12.2.4 Rest of Middle East

12.2.5 Egypt

12.2.6 Nigeria

12.2.7 South Africa

12.2.8 Rest of Africa

12.3 Middle East and Africa Phenol Market size Outlook by Segments, 2021-2030

By Product

Phenolic Resins

Caprolactum

Bisphenol-A

Others

By Manufacturing Process

Cumene Process

Dow Process

Ranching–Hooker Process

By Classification

Monohydric

Dihydric

Trihydric

By Application

Epoxy Resins

Polycarbonates

Nylon

Bakelite

Detergents

Phenolic Resins

Pharmaceutical Drugs

Herbicides

13 Company Profiles

13.1 Company Snapshot

13.2 SWOT Profiles

13.3 Products and Services

13.4 Recent Developments

13.5 Financial Profile

AdvanSix Inc

Altivia Corp

CEPSA Química S.A.

Domo Chemical GmbH

Formosa Chemicals & Fibre Corp

INEOS Capital Ltd

Kumho P&B Chemicals Inc

Mitsubishi Chemical Corp

Mitsui Chemicals Inc

PTT Phenol Company Ltd

Royal Dutch Shell plc

Solvay SA

14 Appendix

14.1 Customization Offerings

14.2 Subscription Services

14.3 Related Reports

14.4 Publisher Expertise

By Product

Phenolic Resins

Caprolactum

Bisphenol-A

Others

By Manufacturing Process

Cumene Process

Dow Process

Ranching–Hooker Process

By Classification

Monohydric

Dihydric

Trihydric

By Application

Epoxy Resins

Polycarbonates

Nylon

Bakelite

Detergents

Phenolic Resins

Pharmaceutical Drugs

Herbicides

Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)