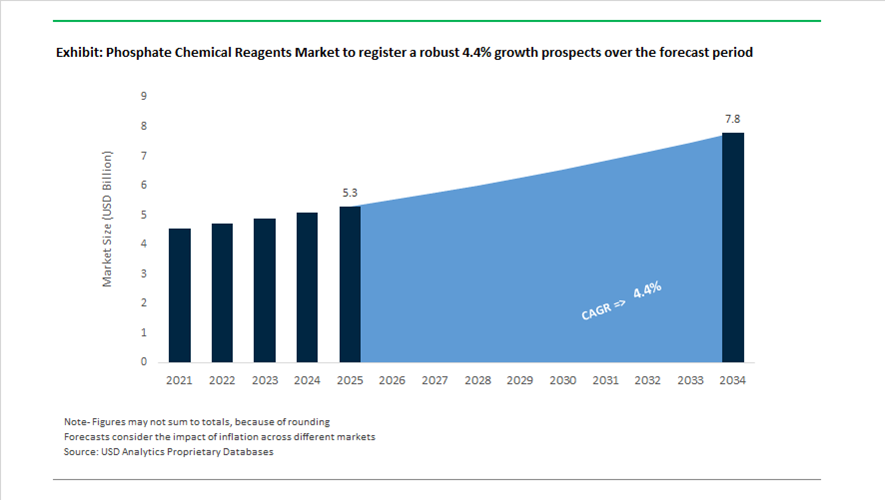

Phosphate Chemical Reagents Market Size 2025–2034: $5.3 Billion to $7.8 Billion at 4.4% CAGR Driven by Phosphoric Acid Integration, Circular Recovery Mandates, and High-Purity Reagent Innovation

The global phosphate chemical reagents market is projected to grow from $5.3 billion in 2025 to $7.8 billion by 2034, registering a CAGR of 4.4%. Market expansion is supported by rising demand for phosphoric acid derivatives, trisodium phosphate (TSP), phosphorus pentachloride, specialty precipitation reagents, and electronic-grade phosphate compounds used across agriculture, water treatment, pharmaceuticals, battery materials, and precision analytical chemistry. Structural integration of phosphate mining with downstream reagent production, regulatory mandates on phosphorus recovery, and growing adoption of high-purity nano-phosphate reagents are reshaping competitive positioning across global markets.

Vertical integration and geographic diversification intensified in 2024 and 2025. In December 2024, the Saudi Arabian Mining Company completed full acquisition of the Waad Al Shamal Phosphate Company stake, consolidating control over upstream phosphate rock extraction and downstream high-purity phosphate reagent manufacturing. This integration strengthens supply security for food-grade and industrial phosphate chemicals. In April 2025, Jordan Phosphate Mines Company signed a strategic agreement with Indonesia to establish a new phosphoric acid production facility in Surabaya, effectively doubling joint venture capacity and reinforcing Southeast Asia’s long-term supply of phosphate reagents for fertilizer blending, industrial processing, and chemical synthesis applications. In September 2025, China-based Wintrue acquired a 49% stake in a phosphate mine with reserves of approximately 30 million metric tons, ensuring raw material stability for its specialty phosphate reagent portfolio.

High-purity reagent demand in agrochemicals and pharmaceuticals is driving new capital investments. In August 2025, Albemarle announced construction of a new phosphorus pentachloride production facility aimed at supporting global demand for advanced synthesis reagents used in crop protection molecules and active pharmaceutical ingredients. In June 2024, Aditya Birla Chemicals inaugurated a $50 million manufacturing and R&D center in the United States focused on food-grade and industrial phosphate reagents, including trisodium phosphate, to address rising North American demand for precision cleaning and processing agents. Regulatory headwinds emerged in May 2025 when the U.S. Internal Revenue Service petitioned to classify TSP under the Superfund chemical tax framework, affecting pricing structures and encouraging industrial users to explore alternative phosphate blends.

Sustainability mandates and circular phosphorus recovery are redefining market dynamics in Europe. In February 2025, the European Commission introduced a directive requiring member states to increase phosphorus recovery from municipal wastewater by 20%. This policy triggered accelerated development of magnesium-based and calcium-based precipitation reagents designed to convert recovered phosphorus into reusable circular phosphate inputs. In July 2025, Solvay entered a partnership with an agricultural technology firm to develop green phosphorus reagents optimized for precision farming, targeting improved nutrient delivery efficiency while reducing environmental runoff and toxicity.

Digitalization and advanced material innovation are emerging as competitive differentiators. In September 2025, BASF unveiled an AI-driven digital platform to optimize its phosphorus pentachloride and reagent supply chains, leveraging predictive analytics to reduce lead times and enhance inventory precision. In November 2025, Nippon Chemical Industrial Co. partnered with TDK Corporation to establish a joint venture for next-generation phosphorus-based materials, including high-performance reagents tailored for electronic components and advanced battery systems. By late 2025, Thermo Fisher Scientific and Merck introduced nano-sized phosphate reagents designed for ultra-high-precision analytical chemistry and heavy metal sequestration in water treatment applications, reflecting a shift toward micro-scale reactivity enhancement and specialized performance attributes.

Key Trends Reshaping Demand for Phosphate Chemical Reagents

Strategic Diversification into Ultra-High-Purity Phosphate Reagents for Advanced Semiconductor Nodes

The phosphate chemical reagents market is undergoing a decisive shift toward ultra-high-purity production as semiconductor manufacturing moves deeper into sub-7nm logic and advanced 3D NAND architectures. In these environments, phosphate-based reagents such as electronic-grade phosphoric acid are no longer treated as bulk wet chemicals but as yield-critical materials. Even trace metal contamination at parts-per-trillion levels can trigger wafer defects, forcing fabs to specify reagents compliant with SEMI C36 Grade 3 and above.

This shift is driving capital reallocation toward reshored and tightly controlled production capacity. In January 2025, Prayon commissioned a new electronic-grade phosphoric acid facility in Bex, Switzerland, explicitly designed to support European and North American semiconductor reshoring initiatives. The expansion effectively doubles the company’s capacity for high-purity phosphoric acid, addressing customer concerns around supply security, logistics risk, and compliance with increasingly stringent fab qualification protocols.

Product innovation is moving in parallel. In 2024, Alventa S.A. commercialized a SEMI C36 Grade 3 electronic-grade phosphoric acid tailored for integrated circuit fabrication, OLED display manufacturing, and photovoltaic cell processing. These applications require not only extreme purity but also consistent etching performance across high-volume manufacturing runs, reinforcing long-term supply contracts rather than spot purchasing.

The scale of this demand is structural rather than cyclical. With the global semiconductor market approaching a $600 billion valuation by late 2025 and more than 320 new fabs announced globally since 2022, phosphate reagent consumption is expanding rapidly. Each fab requires an average of approximately 0.42 million tonnes of high-purity phosphoric acid across wafer cleaning, etching, and surface treatment cycles, positioning ultra-high-purity phosphate reagents as a strategic bottleneck material in the global chip ecosystem.

Evolution of Specialized Phosphorylating and Activating Agents for Biopharma Applications

Beyond electronics, phosphate chemical reagents are gaining strategic relevance in biopharmaceutical synthesis, where they are evolving from passive buffering agents into active synthetic tools. The growth of mRNA vaccines, antisense oligonucleotides, and next-generation genetic therapies is increasing demand for highly specialized phosphate reagents that support precise phosphorylation and activation reactions.

Research published in Chemical Science in 2024 highlighted the critical role of phosphate donors such as those used by T4 polynucleotide kinase in phosphorylating 5′-hydroxyl groups during synthetic nucleic acid assembly. These phosphate-driven enzymatic systems are now central to the production of XNA and other engineered genetic materials used in targeted drug delivery and advanced therapeutics.

Commercial reagent suppliers are responding by moving up the value chain. In April 2025, Biologix Group introduced new ready-to-use phosphate reagent series, including PBS and DPBS buffers formulated to ultra-pure standards. These reagents are optimized for maintaining physiological pH during nucleoside-5′-triphosphate synthesis, which underpins all cell-free protein expression platforms. The shift toward pre-validated, application-specific phosphate formulations reflects the biopharma sector’s demand for reproducibility, regulatory readiness, and reduced process complexity.

cGMP Phosphate Buffers for Cell and Gene Therapy Manufacturing

Cell and gene therapy is emerging as one of the most attractive high-margin opportunities for phosphate reagent suppliers. Unlike conventional small-molecule drug production, CGT manufacturing relies on exceptionally large volumes of sterile, ultra-pure phosphate buffers used throughout cell washing, viral vector stabilization, and final formulation steps.

By 2024, global biopharmaceutical facilities consumed more than 2.1 billion liters of buffer solutions annually. CAR-T cell therapy alone accounted for approximately 70 million liters of specialized phosphate buffers in 2023, reflecting the intensity of reagent usage per patient dose. As more therapies progress from clinical trials to commercial-scale production, buffer demand is rising in direct proportion to patient volumes rather than batch size efficiencies.

Strategic acquisitions underscore the importance of supply chain control in this segment. In August 2024, Merck KGaA acquired Mirus Bio for roughly $600 million to strengthen its viral vector and cell therapy manufacturing capabilities. This move reflects a broader industry trend toward vertical integration, where control over phosphate buffer quality, sterility, and regulatory documentation is treated as a competitive advantage rather than a procurement function.

The growth of personalized medicine further reinforces this opportunity. By the end of 2025, personalized and advanced therapies are expected to reach more than 1.4 million patients globally. Each therapy often requires custom-formulated, cGMP-compliant phosphate buffers tailored to specific cell lines or vectors, creating sustained demand for flexible, high-purity phosphate reagent platforms with rapid customization capabilities.

Non-Halogenated Phosphate Flame Retardants for Electric Vehicles and Energy Storage

A second major opportunity lies in the expansion of non-halogenated phosphate flame retardants as regulatory pressure accelerates the phase-out of brominated and chlorinated additives. Updated restrictions under EU REACH and U.S. EPA frameworks are pushing manufacturers toward phosphorus-based flame retardant systems that deliver thermal stability with lower smoke toxicity and reduced human health risks.

In September 2025, the National Institute of Environmental Health Sciences reported an accelerating global withdrawal of halogenated flame retardants such as PBDEs, creating a regulatory vacuum now being filled by phosphate esters and inorganic phosphates. These materials are particularly well suited for enclosed environments such as electric vehicles, where fire safety and toxicity during thermal events are critical considerations.

EV battery systems are a primary demand driver. Compliance with safety standards such as UL 2580 and IEC 62619 is pushing OEMs toward halogen-free flame-retardant polypropylene and engineering plastics that rely on phosphate additives. These formulations play a key role in preventing thermal runaway and limiting fire propagation within battery compartments and high-voltage cable assemblies.

Investment activity confirms the strategic convergence of phosphate reagents and energy storage. In 2024, Mosaic began construction of a 100,000-tonne-per-year purification facility in Louisiana to upgrade agricultural-grade phosphoric acid into technical-grade material suitable for Lithium Iron Phosphate battery production. This project illustrates how phosphate chemical reagents are becoming foundational inputs across both the semiconductor and electric mobility value chains.

Phosphate Chemical Reagents Market Share and Segmentation Insights

Phosphoric Acid Leads Phosphate Chemical Reagent Demand Across Multi-Industry Processing Applications

Phosphoric acid accounted for 38.60% of the Phosphate Chemical Reagents Market by reagent type in 2025, reflecting its versatility as the foundational phosphorus compound used across multiple industrial sectors. This reagent serves both as a precursor for manufacturing other phosphate chemicals and as a direct process reagent in semiconductor fabrication, water treatment systems, food processing, and pharmaceutical manufacturing. Its widespread industrial use continues to sustain strong global demand for phosphoric acid based chemical reagents. In 2025, growing demand for ultra-high purity phosphoric acid in semiconductor wet etching and wafer cleaning processes is shaping market dynamics, with chemical producers investing in advanced purification technologies capable of achieving parts-per-billion impurity levels required for next-generation semiconductor manufacturing.

Water Treatment Sector Drives Phosphate Reagent Consumption in Municipal and Industrial Infrastructure

Water treatment represented 28.40% of the Phosphate Chemical Reagents Market by application in 2025, making it the largest consumption segment across municipal and industrial water management systems. Phosphate reagents are widely used for corrosion control in drinking water distribution networks, scale inhibition in industrial cooling systems, and nutrient management in wastewater treatment plants. The scale of global water infrastructure continues to support consistent demand for phosphate treatment chemicals. In 2025, increasing focus on phosphorus recovery technologies in wastewater treatment facilities is influencing chemical usage patterns, with treatment plants deploying phosphate precipitation and recovery systems that capture phosphorus as struvite for reuse in agricultural fertilizer production.

Phosphate Chemical Reagents Market Competitive Landscape

The global phosphate chemical reagents market is consolidated among vertically integrated producers controlling phosphate rock mining, purified phosphoric acid (PPA), and specialty reagent synthesis. Competitive intensity is shaped by downstream chemical expansion, high-purity phosphate innovation, ESG-aligned production, and regional manufacturing strategies to stabilize supply chains.

ICL Group Integrates Specialty Phosphate Reagents with Localized Production Expansion in India

ICL Group (Israel Chemicals Ltd.) operates a fully integrated mine-to-market model spanning phosphate rock extraction, purified phosphoric acid (PPA), and specialty phosphate salts. The March 2026 Maharashtra facility replicates its Israeli production system, reducing exposure to Strait of Hormuz shipping disruptions. HALOX® and FLASH-X® brands target phosphate-based corrosion inhibitors and flash-rust prevention in coatings. POLYRON® and CALGON® product lines serve condensed phosphate demand for dispersants and sequestrants in paints, coatings, and construction chemicals. The company reported over $7.15 billion revenue in 2025 with 5% year-on-year growth, supported by the Bartek Ingredients acquisition. Portfolio expansion focuses on high-performance specialty phosphate reagents and downstream chemical integration.

OCP Group Expands High-Purity Phosphate Chemical Capacity with Green Manufacturing Infrastructure

OCP Group controls the world’s largest phosphate reserves and is expanding into high-value phosphate chemical reagents and derivatives. The $12 billion investment program (2025–2026) targets downstream expansion, including high-purity phosphoric acid production at Jorf Lasfar and Safi. Green phosphate manufacturing integrates solar, wind energy, and desalinated water to meet ESG standards in Europe and North America. The company recorded MAD 114 billion ($11.4 billion) revenue in 2025, reflecting 17% growth driven by technical-grade phosphate demand in India and Europe. Production systems allow switching between fertilizer-grade and reagent-grade phosphates based on market pricing. Industrial scale and process flexibility support both bulk and specialty phosphate chemical supply.

Mosaic Advances Phosphate Chemical Reagents Through Rare Earth Recovery and Nutrient Efficiency Technologies

The Mosaic Company focuses on nutrient-use efficiency (NUE) and phosphate reagent innovation linked to critical mineral recovery. Following phosphate inclusion in the U.S. Critical Minerals List (November 2025), the company accelerated Rare Earth Element (REE) extraction from phosphogypsum (PG). Mosaic Biosciences integrates biological solutions with phosphate reagents to improve nutrient uptake and chemical stability. Fusion technology, supported by 50+ patents, enables uniform nutrient distribution, reducing runoff and improving application efficiency. The planned divestment of Carlsbad potash operations (H1 2026) reallocates capital toward high-margin phosphate and specialty chemical segments. R&D intensity remains centered on sustainable phosphate processing and advanced reagent performance.

PhosAgro Strengthens High-Purity Phosphate Reagent Output with Low-Impurity Apatite Feedstock

PhosAgro utilizes high-purity apatite concentrate with low cadmium and lead content for reagent-grade phosphate chemical production. Q1 2025 output reached 2.37 million tonnes of phosphate-based products, with wet-process phosphoric acid production increasing 3.8% to 929,000 tonnes. Sodium Tripolyphosphate (STPP) and feed-grade phosphates exceeded 1 million tonnes monthly production in January 2025. Export volumes to India increased 12-fold in Q3 2025, supported by shifting global trade flows and Chinese export constraints. The RUB 75 billion modernization program targets energy-efficient chemical synthesis across Vologda and Saratov facilities. Production scale and feedstock purity support industrial, food-grade, and specialty phosphate reagent applications.

EuroChem Expands Integrated Phosphate Chemical Production Across Brazil and Emerging Markets

EuroChem Group is developing integrated phosphate mining and chemical production assets in high-growth regions. The Serra do Salitre complex in Brazil combines phosphate extraction with downstream reagent manufacturing and is expected to reach full capacity by 2026. The ProTech Lab drives R&D in water-soluble fertilizers and specialty phosphate reagents for precision agriculture and industrial use. The December 2024 exit from EuroChem Migao Limited aligns with a strategy focused on South America and Central Asia. New NPS (Nitrogen-Phosphorus-Sulphur) product lines address soil stability and industrial chemical intermediate demand. Expansion strategy emphasizes integrated production, regional market access, and specialty phosphate chemical development.

China – Semiconductor-Grade Autonomy Backed by Environmental Discipline

China’s phosphate chemical reagents industry is being reshaped by a dual mandate of strategic autonomy and regulatory tightening. Under the MIIT Work Plan for Stabilizing Chemical Growth (2025–2026), the country is prioritizing electronic-grade phosphoric acid and phosphorus precursors to push domestic self-sufficiency beyond 90% for semiconductor fabrication. This policy focus has accelerated investments in high-purity processing, particularly as fabs demand ultra-low metal and particle specifications. Capacity expansion is already visible. By late 2025, Fujian ZhanHua Chemical and Yuntianhua Group successfully scaled high-purity ammonium phosphate lines, aligning reagent output with surging domestic demand from LFP battery cathode producers.

Environmental enforcement is acting as both a constraint and a catalyst. The 2025 Draft Environmental Code mandates closed-loop phosphorus recovery, forcing new reagent plants in provinces such as Yunnan to integrate phosphogypsum repurposing technologies from inception. Simultaneously, export controls introduced by MOFCOM in October 2025 on dual-use phosphorus compounds have tightened global supply of key precursors used in flame retardants and precision reagents. At the operational level, the Jiangbei New Material Technology Park in Nanjing has been designated a Smart Hub, where AI-driven process optimization pilots in 2026 are expected to materially reduce the energy intensity of electrolytic phosphorus production, reinforcing China’s cost and scale advantage.

India – Fertilizer-Led Scale Converging with Specialty Reagents

India’s phosphate chemical reagents landscape is expanding from its traditional fertilizer base toward higher-value formulations. In August 2025, Paradeep Phosphates Limited announced a ₹1,500 crore investment to lift granulated and phosphoric acid capacity by 40% by end-2026, targeting a total output of 3.7 million tonnes. This scale-up directly supports the government’s Nutrient-based Subsidy scheme update in 2025, which introduced higher incentives for unique NPK formulations such as 19-19-19 grades, strengthening domestic manufacturing depth.

Policy ambition extends beyond fertilizers. The NITI Aayog Chemical Industry Report 2025 outlines the creation of integrated, port-connected chemical hubs to lift India’s share of the global specialty chemical value chain to 6% by 2030. Within this framework, nano-phosphate reagents are emerging as a growth vector, with India targeting 20–25% annual growth through 2026 by leveraging liquid phosphorus formulations for higher nutrient-use efficiency. Consolidation is reinforcing this trajectory. The Q3 2025 amalgamation of Mangalore Chemicals and Fertilizers into the PPL fold added 700,000 tonnes of west coast capacity, improving feedstock security and export readiness.

United States – High-Purity Pivot Anchored in Energy Storage and Semiconductors

The U.S. phosphate chemical reagents market is being recalibrated around domestic supply security and advanced manufacturing. In 2025, the Department of Commerce reaffirmed trade protection measures, including anti-dumping duties on phosphate imports, to safeguard domestic producers such as Innophos and Avantor. These protections are enabling reinvestment into higher-purity and application-specific reagent lines.

Demand-side momentum is increasingly linked to energy storage. High-purity phosphoric acid streams are being redirected toward LFP battery cathode manufacturing, supported by Inflation Reduction Act incentives that favor localized battery material supply chains through 2026. Regulatory oversight is also intensifying. The EPA has set June 2026 as the final deadline for reporting releases of 131 phosphorus-related compounds under the National Pollutant Release Inventory, raising compliance thresholds for producers. In parallel, Avantor expanded its high-purity phosphate offerings in 2025 to meet 6N and 7N purity requirements for next-generation 2 nm semiconductor fabrication, underscoring the shift toward ultra-clean laboratory and fab reagents.

Saudi Arabia – Integrated Mining-to-Reagent Platform

Saudi Arabia is consolidating its position as a globally integrated phosphate reagent supplier by leveraging mining dominance and energy transition strategies. During 2024–2025, Maaden finalized the acquisition of The Mosaic Company’s stake in the Waad Al Shamal Phosphate Company, centralizing control over one of the world’s largest phosphate value chains. This vertical integration is enabling tighter coordination between raw material extraction and reagent-grade processing.

Infrastructure expansion is reinforcing export orientation. The Waad Al Shamal industrial city is being expanded in 2026 with new units dedicated to food-grade and tech-grade sodium hexametaphosphate, targeting Europe and Africa. Concurrently, Maaden is piloting Green Phosphate projects using solar-powered electrolysis to supply hydrogen for ammonia synthesis in phosphate reagents. This initiative positions Saudi output as both cost-competitive and aligned with low-carbon procurement standards in international markets.

Germany – Regulatory Tightening and Circular Phosphorus Leadership

Germany’s phosphate chemical reagents industry is navigating stricter regulatory scrutiny while advancing circular recovery models. The European Commission’s Chemicals Industry Package in Q4 2025 introduced targeted revisions to REACH, imposing higher transparency and data requirements on phosphorus-based flame retardants and additives. These measures are reshaping product qualification timelines and increasing compliance costs across the value chain.

Despite regulatory headwinds, Germany remains critical to semiconductor reagent supply and circular innovation. Nagase Europe launched a dedicated supply chain in November 2025 for phosphorus oxychloride in 6N and 7N grades, stored in specialized high-purity quartz bubblers for EU chip manufacturers. On the sustainability front, Germany is leading initiatives under the European Sustainable Phosphorus Platform, with 2026 set to mark the first commercial-scale deployment of struvite precipitation from municipal wastewater. This positions Germany as a reference market for circular phosphorus recovery technologies.

Comparative Snapshot – Phosphate Chemical Reagents by Country

Phosphate Chemical Reagents Market County Level Snapshot

|

Country

|

Strategic Focus

|

Primary Demand Driver

|

Structural Position

|

|

China

|

Self-sufficiency and export control

|

Semiconductors, LFP batteries

|

Scale-led with regulatory intensity

|

|

India

|

Fertilizer scale to specialty shift

|

NPK, nano-phosphates

|

Expansion-driven, policy-backed

|

|

United States

|

High-purity domestic security

|

Batteries, 2 nm fabs

|

Compliance-heavy, innovation-led

|

|

Saudi Arabia

|

Vertical integration

|

Export-grade reagents

|

Resource-integrated, low-cost

|

|

Germany

|

Regulation and circular recovery

|

Semiconductors, recycling

|

Innovation-centric, compliance-led

|

Phosphate Chemical Reagents Market Report Scope

Phosphate Chemical Reagents Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$5.3 Billion

|

|

Market Size (2034)

|

$7.8 Billion

|

|

Market Growth Rate

|

4.4%

|

|

Segments

|

By Reagent Type (Phosphoric Acid, Ammonium Phosphates, Sodium Phosphates, Potassium Phosphates, Calcium Phosphates, Specialty Phosphorus Precursors), By Purity Grade (Ultra-High Purity, Analytical Grade, Food & Pharma Grade, Technical Grade), By Application (Semiconductor Doping & Etching, Energy Storage, Precision Agriculture, Water Treatment, Food & Beverage, Pharmaceuticals)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

The Mosaic Company, OCP Group, Nutrien Ltd., Yara International ASA, Saudi Arabian Mining Company, Sinopec, Innophos Holdings Inc., Avantor Inc., Paradeep Phosphates Limited, EuroChem Group AG, Israel Chemicals Ltd., Nagase & Co. Ltd., PhosAgro, Solvay SA, Hubei Xingfa Chemicals Group

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Phosphate Chemical Reagents Market Segmentation

By Reagent Type

- Phosphoric Acid

- Ammonium Phosphates

- Sodium Phosphates

- Potassium Phosphates

- Calcium Phosphates

- Specialty Phosphorus Precursors

By Purity Grade

- Ultra-High Purity

- Analytical Grade

- Food & Pharma Grade

- Technical Grade

By Application

- Semiconductor Doping & Etching

- Energy Storage

- Precision Agriculture

- Water Treatment

- Food & Beverage

- Pharmaceuticals

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Phosphate Chemical Reagents Industry

- The Mosaic Company

- OCP Group

- Nutrien Ltd.

- Yara International ASA

- Saudi Arabian Mining Company

- Sinopec

- Innophos Holdings Inc.

- Avantor Inc.

- Paradeep Phosphates Limited

- EuroChem Group AG

- Israel Chemicals Ltd.

- Nagase & Co. Ltd.

- PhosAgro

- Solvay SA

- Hubei Xingfa Chemicals Group

*- List not Exhaustive