Photo Emulsion Market Size, Screen Printing Precision Demand, and Sustainable Formulation Shift

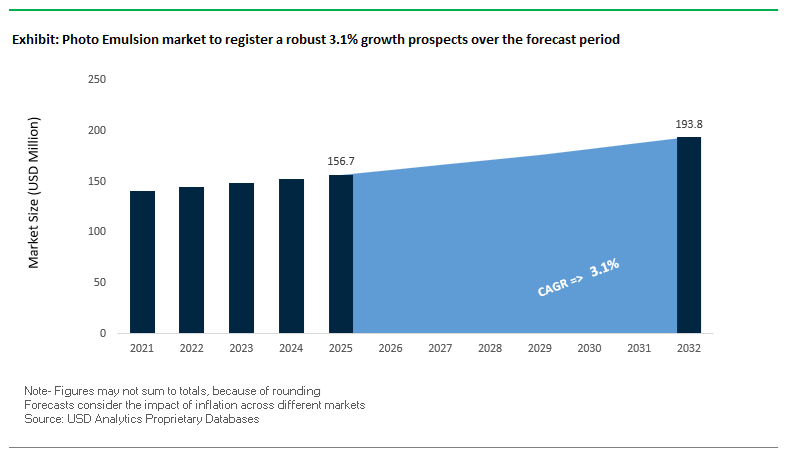

The global Photo Emulsion Market was valued at $156.7 million in 2025 and is projected to grow at a CAGR of 3.1% through 2032, reaching $194 million by 2032. This moderate growth reflects the market’s strong linkage to screen printing applications across textiles, electronics, automotive components, and industrial graphics, where photo emulsions are critical for image transfer precision, stencil durability, and process efficiency.

A key structural driver is the increasing demand for high-resolution printing and miniaturization, particularly in printed circuit boards (PCBs), flexible electronics, and haptic interfaces. Advanced photo emulsions, especially SBQ (pure photopolymer) systems, are gaining traction due to their ability to deliver faster exposure times, longer shelf life, and improved image definition compared to traditional diazo or dual-cure emulsions. These attributes are essential in high-precision manufacturing environments where consistency and throughput are critical.

In parallel, the textile and graphic arts sectors are evolving toward high-detail halftone printing, specialty inks, and automated production systems, increasing the need for emulsions that provide excellent mesh adhesion, chemical resistance, and easy reclaimability. The growing integration of AI-driven exposure systems and digital workflow optimization is further enhancing the performance expectations of emulsion technologies.

Sustainability is emerging as a major innovation axis, with manufacturers focusing on PFAS-free formulations, low-VOC chemistries, and water-efficient reclaiming processes. Regulatory pressure, particularly in Europe, is accelerating the transition toward eco-friendly emulsion systems and biodegradable cleaning solutions, reshaping product development strategies and competitive positioning across the market.

Market Analysis: SBQ Technology Expansion, PFAS-Free Innovation, and AI-Integrated Printing Systems Driving Market Evolution

Recent developments in the Photo Emulsion Market highlight a convergence of high-resolution technology advancement, sustainability-driven reformulation, and digital integration. In April 2026, Murakami Screen advanced its SBQ photopolymer technology, emphasizing ready-to-use emulsions such as Photocure SR and TXR, which eliminate diazo mixing and deliver faster exposure and extended shelf life. These systems are particularly suited for electronics and textile printing, where precision and process efficiency are paramount.

Innovation is also focused on integrating emulsion chemistry with advanced manufacturing systems. MacDermid Alpha’s February 2026 integration of Autotype emulsions with Tetrabond® stencil technology enhances consistency in miniaturized electronics assembly, ensuring precise solder paste deposition. Similarly, SAATI’s AI-driven LTS E70B system (September 2025) demonstrates the growing role of intelligent exposure control, optimizing emulsion performance in industrial textile printing environments.

Sustainability-driven product development is accelerating across the market. SAATI’s SAATItex PHU-HR, recognized with a Pinnacle Product Award, offers high-resolution performance with easy reclaimability and reduced chemical residue, while Kiwo’s eco-friendly reclaiming additives (June 2025) enable a one-step cleaning process, significantly reducing water usage and wastewater impact. Additionally, Chromaline’s PFAS-free stencil roadmap reflects the industry-wide transition away from fluorinated surfactants toward environmentally compliant alternatives.

Application-specific innovation is expanding into new end-use segments. MacDermid Autotype’s SBQ emulsion expansion (January 2025) targets automotive interiors and touch-screen applications, where maintaining consistent emulsion thickness across complex surfaces is critical. Meanwhile, Ulano’s strategic focus on high-resolution graphic arts emulsions (March 2026) addresses demand in premium printing applications such as architectural glass and industrial graphics.

Support ecosystems are also evolving to enhance adoption. Easiway Systems’ digital initiatives (May 2025) provide educational tools for optimizing emulsion use and reclaiming processes, particularly for small and mid-scale printers transitioning to low-VOC and biodegradable solutions.

Market Trend: SBQ Photopolymer Emulsions Replacing Diazo Systems for High-Throughput Textile Screen Printing

The photo emulsion industry is undergoing a structural shift as textile screen printers transition from diazo-based dual-cure emulsions to pure photopolymer SBQ systems. This migration is driven by the need for higher production efficiency, reduced chemical handling, and compatibility with modern water-based and discharge ink systems used in apparel printing.

SBQ emulsions deliver a significant improvement in exposure speed, operating approximately 8x to 10x faster than traditional diazo systems. This acceleration reduces screen preparation time and alleviates production bottlenecks, enabling throughput improvements of up to 75% in high-volume garment printing environments. Faster exposure cycles also support lean manufacturing practices by minimizing idle time in screen-making workflows.

Material performance is also advancing. Modern SBQ emulsions feature solids content in the range of 42% to 50%, allowing for improved mesh bridging and efficient stencil build-up using simplified coating techniques. A one-plus-one coating approach can achieve equivalent stencil thickness to multiple passes of lower-solids diazo emulsions, reducing labor intensity and improving consistency in print quality.

Shelf-life stability further differentiates SBQ systems. Unlike diazo emulsions that degrade within 4 to 8 weeks after sensitization, SBQ emulsions are pre-sensitized and maintain stability for over 12 months. This reduces material waste and simplifies inventory management for printing facilities. These combined advantages are driving rapid adoption of SBQ photopolymer emulsions as the new standard in textile screen printing.

Market Trend: High-Resolution Photopolymer Emulsions Enabling Advanced PCB and Electronics Printing Applications

The electronics manufacturing sector is creating new demand for ultra-high-resolution photo emulsions capable of supporting increasingly complex circuit designs and miniaturized components. Applications such as printed circuit boards, membrane switches, and touch-sensitive interfaces require precise stencil definition to achieve fine conductive pathways and consistent functional performance.

Advanced photopolymer emulsions are now achieving resolution capabilities in the range of 30 to 50 microns, enabling the production of fine-line circuitry required for next-generation electronics, including 5G devices and IoT components. This level of precision is critical for maintaining signal integrity and ensuring reliable performance in high-density electronic assemblies.

Durability under aggressive processing conditions is equally important. Electronics-grade emulsions are engineered to withstand more than 5,000 print cycles without degradation when exposed to solvent-based or UV-curable inks. These formulations maintain edge definition and resist swelling, ensuring consistent print quality over extended production runs.

The combination of high resolution, chemical resistance, and mechanical durability is positioning advanced photopolymer emulsions as a key enabler of innovation in electronics manufacturing. As device complexity continues to increase, demand for precision screen printing materials is expected to grow significantly.

Market Opportunity: CARB VOC Regulations Driving Adoption of Low-Emission Photopolymer Emulsion Systems

Regulatory developments in the United States are creating a strong opportunity for low-VOC photo emulsion technologies. Enforcement of CARB Rule 1130.1 and related district-level regulations is tightening VOC limits for screen printing operations, affecting both inks and associated screen-room chemicals such as emulsions and cleaning agents.

Under current requirements, materials used in screen printing must comply with strict VOC concentration limits, often capped at 400 g/L for high-emission products. This is accelerating the transition toward water-reducible SBQ emulsions, which offer significantly lower volatile content compared to traditional diazo-based systems. These emulsions support compliance while maintaining high performance in exposure speed and stencil durability.

Operational benefits are also influencing adoption. Facilities that transition to ultra-low VOC systems can reduce hazardous waste disposal costs by approximately 20%, providing a direct economic incentive alongside regulatory compliance. This dual benefit is encouraging widespread reformulation across the screen printing supply chain.

As regulatory oversight continues to increase, manufacturers offering compliant, low-emission photopolymer emulsions are positioned to capture growing demand in both textile and industrial printing applications.

Market Opportunity: China VOC and Formaldehyde Standards Driving Shift Toward High-Purity Photopolymer Emulsions

China’s implementation of GB 38507-2025 is reshaping the competitive landscape for photo emulsions by introducing strict limits on VOC emissions and formaldehyde content in printing consumables. These regulations are particularly impactful in export-oriented textile and electronics manufacturing sectors, where compliance is mandatory for market access.

The standard imposes a formaldehyde threshold of 50 mg/kg, requiring manufacturers to adopt cleaner chemistries and eliminate residual contaminants associated with legacy diazo formulations. In addition, the inclusion of a prohibited solvent list has effectively banned numerous traditional additives, forcing a shift toward higher-purity SBQ and advanced photopolymer systems.

This regulatory environment is driving a large-scale reformulation cycle across the industry, with manufacturers investing in low-emission, high-performance emulsion technologies that meet both domestic and international compliance requirements. The transition is also supporting improved workplace safety and reduced environmental impact in printing operations.

Given China’s position as a global manufacturing hub for textiles and electronics, the enforcement of these standards is creating substantial demand for compliant photopolymer emulsions. Suppliers capable of delivering high-resolution, low-emission, and regulation-compliant products are well positioned to benefit from this market transformation.

Photo Emulsion Market Share and Segmentation Insights

Direct Liquid Emulsions Capture 52.7% Share Driven by Versatility and Cost Efficiency

The photo emulsion market by physical form is dominated by direct liquid emulsions, accounting for 52.7% of global market share in 2025, due to their unmatched versatility and cost-effectiveness in screen printing applications. These emulsions, typically based on diazonium or photopolymer chemistry, allow precise control over viscosity, coating thickness, and mesh compatibility, making them ideal for textile printing, graphic arts, industrial marking, and PCB fabrication. Their adaptability supports a wide range of printing requirements, from fine-detail graphics to heavy ink deposition. Additionally, automated screen coating machines enable rapid, high-throughput application of liquid emulsions, making them the preferred solution for large-scale production environments such as garment printing and electronics manufacturing. As demand for high-efficiency screen printing materials and customizable stencil systems grows, direct liquid emulsions continue to lead the global photo emulsion market.

General Purpose Segment Holds 45.4% Share Due to Balanced Performance and Ease of Use

In the photo emulsion market by functional grade, general purpose emulsions lead with a 45.4% market share in 2025, driven by their ability to meet the needs of the majority of screen printing applications across industries. These emulsions offer an optimal balance of resolution, exposure speed, durability, and resistance to water and solvents, making them suitable for approximately 80% of end-user requirements in textile, signage, and industrial printing. Their lower cost and forgiving processing characteristics—including tolerance to variations in exposure time and reclaiming—make them especially attractive for small-to-medium printing shops, commercial printers, and educational institutions. As the industry continues to prioritize cost-efficient, easy-to-use, and versatile screen printing solutions, general purpose emulsions remain the backbone of the photo emulsion and stencil materials market, ensuring consistent demand across both developed and emerging regions.

Competitive Landscape of the Photo Emulsion Market

Ulano Leads High-Precision Photo Emulsion Market with Advanced Photopolymer Technologies

Ulano Corporation is a global leader in the photo emulsion market, particularly in high-performance stencil-making chemicals for functional printing. In 2026, the company introduced QFX Blue, a solvent-resistant photopolymer emulsion designed for next-generation applications such as touch panels and membrane switches. With 35.5% solids content, Ulano’s emulsions excel in reproducing fine microstructures and smooth halftones, making them ideal for printed electronics and security printing. The company’s focus on CTS compatibility ensures high-speed exposure and durability in industrial environments. Its global R&D presence, including facilities in Texas and Singapore, supports expansion into Southeast Asia’s PCB manufacturing market.

Murakami Strengthens Screen Printing Leadership with Long-Life Photopolymer Emulsions

Murakami Screen USA Inc. is a major player in the screen printing photo emulsion market, known for its advanced PVA-SBQ photopolymer technologies. Its pre-sensitized emulsions offer extended shelf life of up to one year, reducing hazardous waste compared to traditional diazo systems. The company has expanded its Smartmesh series, integrating emulsions with proprietary mesh systems to provide a complete printing solution for electronics and ceramic industries. Murakami’s dual-cure emulsions deliver exceptional durability for long-run textile printing, while its Aquasol range ensures superior water resistance. These innovations reinforce its leadership in high-performance and industrial screen printing applications.

KIWO Advances Photo Emulsion Technologies with Laser Imaging and Automated Coating Systems

KIWO Inc. is a technologically diverse leader in the photo emulsion market, offering integrated solutions combining chemicals and equipment. In 2026, the company launched the POLYCOL LIGHT-SCRIBE LX series, a high-end SBQ emulsion optimized for laser direct imaging (LDI), reflecting the shift toward digital workflows. KIWO is also investing in KIWOMAT automated coating systems, ensuring consistent emulsion thickness for high-spec industrial applications. Its Polycol Thick-Coat emulsions support specialized applications such as braille printing and gasket production. Additionally, its CLEANLINE range of eco-friendly cleaners supports ESG compliance, strengthening its position in sustainable and automated screen printing solutions.

SAATI Integrates Textile Engineering with Smart Emulsion Technologies for Industrial Applications

SAATI S.p.A. is a key innovator in the photo emulsion market, combining chemical expertise with advanced textile engineering. Its SAATItex Rotary DTR emulsion is widely used in high-speed textile printing, offering strong wet adhesion and reduced stencil failure rates. The company’s LTS E70B technology uses AI-driven optimization to improve coating and exposure efficiency in industrial production environments. SAATI is particularly strong in automotive glass and medical filtration applications, where precision apertures are critical. Its focus on R&D talent and smart materials innovation reinforces its leadership in high-performance and specialized emulsion applications.

Fujifilm Expands Hybrid Printing Solutions with Integrated Photo Emulsion Technologies

Fujifilm Holdings Corporation is a prominent player in the photo emulsion and imaging chemicals market, leveraging its expertise in digital and analog technologies. In 2026, the company focused on hybrid workflows that combine industrial inkjet and screen printing, optimizing emulsions for compatibility with digital primer systems. Fujifilm offers a comprehensive portfolio including film positives, emulsions, and UV curing systems, providing a one-stop solution for commercial printing operations. Its expansion in India supports the growing South Asian printing market. With multiple innovation awards, Fujifilm continues to lead in user-centric and high-performance printing solutions.

MacDermid Autotype Drives Advanced Emulsion Solutions for Automotive and Electronics Applications

MacDermid Autotype, part of MacDermid Alpha Electronics Solutions, is a specialist in high-performance photo emulsion coatings for demanding industrial applications. The company excels in producing stencil emulsions and hardcoated films for 3D-shaped components and smart surfaces, particularly in automotive interiors and EV dashboards. Its Capillex range of capillary films provides unmatched thickness uniformity, making it a preferred choice for precision printing applications. Integration with broader electronics solutions enables cross-functional innovation, including conductive materials for flexible circuits. MacDermid’s focus on advanced coatings positions it as a leader in high-reliability and next-generation emulsion technologies.

China’s Photo Emulsion Market: Scaling High-Sensitivity Systems for PCB and Textile Dominance

China continues to dominate the global photo emulsion market as the largest production hub, driven by its leadership in PCB manufacturing, textile screen printing, and industrial signage applications. The country is rapidly transitioning from commodity-grade emulsions to high-sensitivity dual-cure and SBQ-based photo emulsion systems, enabling superior edge definition and ultra-fine resolution required for advanced electronics. The surge in domestic 5G and IoT hardware production has accelerated the adoption of solvent-resistant SBQ emulsions, such as the SBQ-S300 series, capable of achieving sub-50 micron trace widths for next-generation circuit boards.

Environmental compliance is also reshaping the market landscape. The implementation of GB 30981.1-2025 VOC regulations has triggered a large-scale shift toward water-based photo emulsion formulations, boosting the use of HEUR rheology modifiers for improved stencil performance. Additionally, domestic manufacturers are expanding capacity, with companies like Sophah introducing ultra-high photosensitivity emulsions (DLS-3303 models) tailored for automotive dashboards and advertising signage. China’s stronghold in shipbuilding is further driving demand for industrial-grade diazo emulsions resistant to harsh cleaning agents. Meanwhile, the integration of Digital Mirror Device (DMD) UV exposure systems and the export growth of pre-coated screens highlight China’s move toward automation and digitalization in screen-making technologies.

Germany’s Sustainable Photo Emulsion Innovations: PFAS-Free Chemistry and Circular Manufacturing

Germany is at the forefront of sustainable photo emulsion technologies, aligning closely with the EU Green Deal and ECHA regulatory frameworks. The country is pioneering the transition to PFAS-free screen printing emulsions, with leading manufacturers developing alternative wetting agents and slip additives that maintain high surface performance without hazardous chemicals. This shift is setting new benchmarks for eco-friendly photo emulsion formulations across Europe.

Innovation in Germany is also focused on renewable raw materials, including lignin-derived and starch-based binders, aimed at reducing the carbon footprint of stencil production and reclamation. The rise of printed electronics and flexible circuits is further driving demand for nanomaterial-compatible emulsions capable of handling conductive inks with silver nanowires and graphene. Additionally, the adoption of Laser-to-Screen (LTS) technology is accelerating the use of fast-curing one-component SBQ emulsions, eliminating secondary exposure steps and improving production efficiency. Investments in closed-loop water-based manufacturing systems and compliance with BS EN 13501 fire safety standards are reinforcing Germany’s leadership in high-performance, sustainable photo emulsion solutions.

Japan’s Ultra-High Purity Photo Emulsion Market for Semiconductor and Advanced Optics

Japan remains a global leader in ultra-high-purity (UHP) photo emulsions, particularly in applications intersecting with semiconductor manufacturing, advanced optics, and precision electronics. The country is developing emulsions with sub-ppb trace metal specifications, essential for supporting 2nm semiconductor nodes and highly sensitive fabrication environments. These advanced materials are critical for applications such as FOUP systems and chemical distribution infrastructure in next-generation chip manufacturing.

Beyond semiconductors, Japan is innovating in EV thermal management, using functional photo emulsions to print heat-reflective coatings that reduce battery cooling energy loads. Breakthroughs such as plasma-enhanced photocatalytic emulsions (e.g., ARITERAS KPC) are enabling dual-functionality in cleanroom environments by decomposing organic pollutants. The country is also advancing 6G infrastructure development, leveraging photo emulsion technologies for precise optical fiber patterning. Enhanced shelf-life innovations—extending SBQ emulsions beyond 24 months—are reducing waste and improving operational efficiency, while smart construction applications integrate seismic-reinforcement additives into architectural emulsions.

United States Photo Emulsion Market: High-Tech Manufacturing and Regulatory Transformation

The U.S. photo emulsion market is undergoing a transformation driven by regulatory changes, nearshoring trends, and high-tech manufacturing growth. The implementation of Maine Chapter 90 regulations is accelerating the shift away from PFAS-based formulations toward bio-wax and silicone-based dispersions, reshaping product development strategies across the industry.

Simultaneously, the rise of medical device manufacturing, including biosensors and diagnostic test strips, is increasing demand for high-resolution, biocompatible photo emulsions capable of achieving up to 2500 dpi precision. Infrastructure investments under the Infrastructure Investment and Jobs Act (IIJA) are fueling demand for durable, UV-resistant emulsions used in road signage and outdoor advertising. The widespread adoption of Computer-to-Screen (CTS) technology is further boosting demand for UV-blocking additives and advanced pre-exposure solutions. Additionally, innovations in nanocoating-compatible emulsions are enabling hydrophobic smart textiles, while aerospace applications are driving the development of PACVD-compatible fire-retardant emulsions for aircraft interiors.

South Korea’s Precision Photo Emulsion Market for OLED and Semiconductor Applications

South Korea’s photo emulsion industry is heavily influenced by its leadership in OLED displays, 3D NAND memory, and advanced electronics manufacturing. The country is focusing on chemically resistant, high-performance emulsions essential for Thin-Film Encapsulation (TFE) processes in foldable display production.

Technological advancements include low-voltage curing photo emulsions (<160V), enabling patterning on heat-sensitive flexible substrates—a key requirement for next-generation electronics. South Korea is also innovating in marine and industrial sustainability, integrating biocide-free anti-fouling additives into emulsions for shipbuilding applications. In packaging, the country leads in retort pouch coatings, utilizing photo-emulsion stencils for high-barrier adhesion under extreme sterilization conditions. Additionally, demand from the K-beauty sector is driving the adoption of soft-touch emulsions for premium packaging, while smart city projects are increasing the use of decorative and protective coatings in public infrastructure.

India’s Rapidly Expanding Photo Emulsion Market: Textile Growth and PLI-Driven Manufacturing

India is emerging as a high-growth market in the global photo emulsion industry, fueled by textile manufacturing expansion, government incentives, and infrastructure development. The consolidation of industrial coatings supply chains, highlighted by JSW Paints’ acquisition of Akzo Nobel India, is strengthening domestic access to high-performance photo emulsions for packaging and industrial applications.

Government initiatives such as PMAY-U 2.0 (Housing for All) are driving demand for cost-effective, water-based diazo emulsions used in architectural printing. At the same time, leading textile hubs like Tirupur and Ludhiana are rapidly adopting CTS-compatible photo emulsions, reducing production turnaround times and supporting fast-fashion exports to global markets. Innovations such as self-cleaning “lotus-effect” emulsions, developed by major paint companies, are gaining traction in urban construction projects. Additionally, growth in agritech and refining sectors is creating niche demand for chemically resistant and corrosion-resistant emulsions used in sensors and industrial signage applications.

Brazil’s Photo Emulsion Market: Agribusiness-Driven Industrial Applications and Green Chemistry

Brazil’s photo emulsion market is closely tied to its position as a global leader in agribusiness, industrial manufacturing, and bio-based chemicals. The expansion of agricultural machinery production is increasing demand for powder-coating-compatible emulsions used in tractors and harvesters, supported by investments such as PPG’s Sumaré plant expansion.

The country is also a pioneer in bio-sourced solvents derived from sugarcane, which are being integrated into environmentally friendly photo emulsion formulations and reclaiming processes. In aerospace, Brazil’s growing aircraft manufacturing sector is driving demand for lightweight, high-performance emulsions for cockpit control patterning. Given high solar exposure, local R&D is focusing on UV-resistant emulsions with HALS stabilizers to enhance durability in outdoor signage. Furthermore, investments in industrial coatings and retail distribution are accelerating the adoption of premium architectural and industrial photo emulsions, supported by initiatives like WEG’s expansion in liquid paint production.

Photo Emulsion Market Report Scope

Photo Emulsion market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$156.7 Million

|

|

Market Size (2032)

|

$194 Million

|

|

Market Growth Rate

|

3.1%

|

|

Segments

|

By Product (Diazo-Based Emulsions, SBQ-Based, Dual-Cure Emulsions, Dichromate Emulsions), By Physical Form (Direct Liquid Emulsions, Capillary Films, Indirect Films, Dry Film Photoresists, Silver Halide Suspensions), By Solvent (Water-Resistant Emulsions, Solvent-Resistant Emulsions, Universal), By End-Use Industry (Textiles and Apparel, Electronics and Semiconductors, Packaging and Commercial Graphics, Glass and Ceramics, Medical Devices, Photography and Fine Arts), By Substrate Compatibility (Polyester and Nylon Mesh, Metallic Mesh, Silicon Wafers and Copper-Clad Laminates, Glass and Polyimide), By Functional Grade (General Purpose, High-Resolution, Extreme Durability, Rapid-Exposure)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Ulano Corporation, KIWO, MacDermid Alpha Electronics Solutions, Saati S.p.A., Murakami Screen USA Inc., Fujifilm Sericol, Chromaline, ProdEcran, Kopimask S.A., Amex srl, Taiyo Ink Mfg. Co., Ltd., Screen Print Direct, Feteks Kimya Sanayi, UES, GRAFITEX GmbH

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Photo Emulsion Market Segmentation

By Product

- Diazo-Based Emulsions

- SBQ-Based

- Dual-Cure Emulsions

- Dichromate Emulsions

By Physical Form

- Direct Liquid Emulsions

- Capillary Films

- Indirect Films

- Dry Film Photoresists

- Silver Halide Suspensions

By Solvent

- Water-Resistant Emulsions

- Solvent-Resistant Emulsions

- Universal

By End-Use Industry

- Textiles and Apparel

- Electronics and Semiconductors

- Packaging and Commercial Graphics

- Glass and Ceramics

- Medical Devices

- Photography and Fine Arts

By Substrate Compatibility

- Polyester and Nylon Mesh

- Metallic Mesh

- Silicon Wafers and Copper-Clad Laminates

- Glass and Polyimide

By Functional Grade

- General Purpose

- High-Resolution

- Extreme Durability

- Rapid-Exposure

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Photo Emulsion Industry

- Ulano Corporation

- KIWO

- MacDermid Alpha Electronics Solutions

- Saati S.p.A.

- Murakami Screen USA Inc.

- Fujifilm Sericol

- Chromaline

- ProdEcran

- Kopimask S.A.

- Amex srl

- Taiyo Ink Mfg. Co., Ltd.

- Screen Print Direct

- Feteks Kimya Sanayi

- UES

- GRAFITEX GmbH

*- List not Exhaustive