Physical Vapor Deposition (PVD) Faucet Finishes Market Size, Premiumization Trends, and Durable Surface Technologies

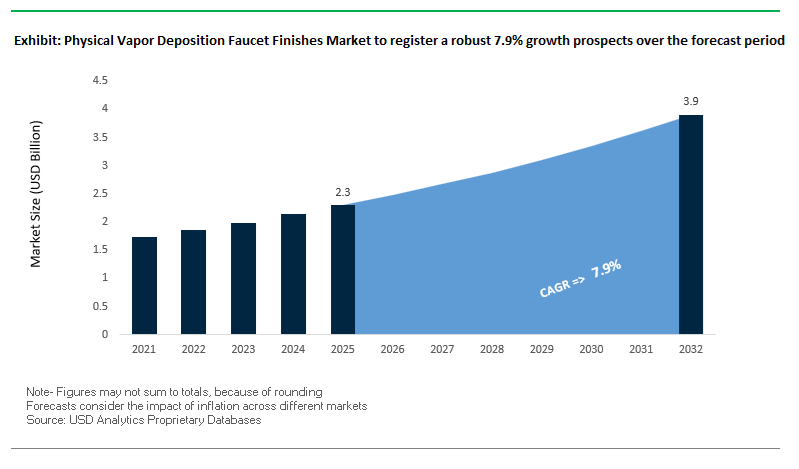

The global Physical Vapor Deposition (PVD) Faucet Finishes Market was valued at $2.3 billion in 2025 and is projected to grow at a CAGR of 7.9% through 2032, reaching $3.9 billion by 2032. This above-average growth reflects the increasing consumer and commercial demand for premium, long-lasting, and aesthetically differentiated faucet finishes across residential, hospitality, and commercial infrastructure segments.

A key structural driver is the shift toward high-end interior design and luxury bathroom/kitchen fittings, where PVD finishes provide superior scratch resistance, corrosion protection, color stability, and tarnish resistance compared to conventional electroplated or painted coatings. These finishes, including brushed brass, titanium, matte black, and gold tones, are increasingly positioned as both functional and design-centric elements in modern architecture.

Durability and hygiene are also emerging as critical decision factors. PVD coatings offer non-porous, chemically stable surfaces that resist degradation from cleaning agents and environmental exposure, making them particularly suitable for high-traffic commercial environments such as hotels, airports, and healthcare facilities. Additionally, growing awareness around product safety and compliance, especially in relation to heavy metal contamination in low-cost faucets, is driving demand toward certified, high-quality PVD-coated products from established brands.

Technological advancements in vacuum deposition processes and color engineering are enabling manufacturers to develop customized finishes, multi-tone effects, and textured surfaces, expanding design possibilities. The integration of touchless technologies and smart plumbing systems is further reinforcing the need for coatings that can withstand frequent use without compromising aesthetics or performance.

Market Analysis: Luxury Design Innovation, Matte Black Expansion, and Advanced PVD Color Engineering Driving Market Growth

Recent developments in the PVD faucet finishes market highlight a strong focus on premium design innovation, surface durability, and manufacturing scalability. In January 2026, Kohler launched its Billet Kitchen Faucet Collection, combining industrial aesthetics with advanced PVD processing to deliver textured, sand-blasted finishes that maintain long-term resistance to scratches and tarnishing. This reflects the growing demand for distinctive, high-end finishes in luxury kitchen design.

Product innovation is also targeting sustainability and everyday functionality. Hansgrohe’s Neovis faucet line (March 2026) integrates eco-efficient technologies with high-quality PVD coatings, ensuring long-term visual appeal in both residential and high-traffic commercial applications. Similarly, Delta Faucet’s 2026 collection expansion, unveiled at KBIS, introduces new product lines with enhanced PVD finish options and touchless features, aligning with evolving consumer preferences for hygiene and convenience.

Material innovation and finish diversification are key competitive differentiators. Delta’s planned expansion of Matte Black PVD technology (Spring 2026) addresses durability challenges associated with traditional painted finishes, offering chip-resistant, long-lasting alternatives. Meanwhile, Vapor Technologies’ “infinite” color system (2025) enables manufacturers to produce custom interference colors and multi-tone finishes, unlocking new possibilities in premium design customization.

Market dynamics are also being influenced by safety and regulatory awareness. Moen’s 2025 alert on off-brand faucet safety has reinforced consumer preference for trusted brands with compliant PVD-coated products, particularly in regions with strict drinking water standards. Additionally, LIXIL’s promotion of luxury PVD-based faucet collections through global design awards highlights the growing importance of architectural integration and aesthetic branding in the high-end segment.

From a manufacturing perspective, scalability and efficiency are becoming critical. IHI Hauzer’s focus on high-throughput PVD systems (March 2026) supports large-scale production of decorative finishes, particularly in Asia-Pacific, where urbanization and luxury housing demand are accelerating.

Market Trend: CrN and Stainless Steel PVD Finishes Replacing Electroplated Chrome in High-Traffic Faucet Applications

The physical vapor deposition faucet finishes market is undergoing a structural transition as manufacturers replace traditional electroplated chrome with chromium nitride PVD coatings and stainless steel-based finishes. This shift is driven by the need for high-durability, low-maintenance surfaces capable of withstanding aggressive cleaning protocols in hospitality, healthcare, and commercial infrastructure environments.

PVD chromium nitride coatings deliver significantly higher surface hardness, typically in the range of 2,000 to 2,500 HV on the Vickers scale, compared to 800 to 1,000 HV for conventional chrome plating. This increase translates into approximately 2.5 times higher abrasion resistance, effectively eliminating common surface defects such as swirl marks and micro-scratches caused by repeated mechanical cleaning.

Corrosion resistance is also substantially improved. In ASTM B117 salt spray testing, PVD-treated faucet finishes consistently exceed 1,200 hours without pitting or corrosion-related discoloration, whereas electroplated chrome surfaces typically degrade within 300 to 500 hours. This enhanced corrosion performance is critical in humid and chemically exposed environments such as hotels, airports, and public restrooms.

Lifecycle cost efficiency is a major adoption driver. PVD-coated faucets are increasingly specified to last across two full renovation cycles, typically spanning 8 to 15 years or more. In contrast, electroplated finishes often require replacement within 3 to 7 years in high-traffic settings. This durability advantage results in an estimated 40% reduction in long-term maintenance capital expenditure for large-scale hospitality and commercial assets, reinforcing the shift toward PVD-based surface engineering.

Market Trend: ZrN and TiN PVD Coatings Advancing Premium Metallic Finishes in Luxury Faucets

Luxury residential and hospitality segments are rapidly adopting zirconium nitride and titanium nitride PVD coatings as replacements for lacquered brass finishes. This transition is driven by the demand for premium aesthetics such as brushed gold and champagne bronze combined with long-term durability and resistance to environmental degradation.

ZrN and TiN coatings offer superior thermal and chemical stability compared to traditional lacquered brass. These coatings are inherently inert and resistant to ultraviolet exposure, preventing the discoloration and yellowing commonly associated with organic lacquer systems. They also withstand rapid temperature fluctuations, such as hot-to-cold water cycling, without cracking or delaminating.

A key technical advantage lies in the molecular-level bonding achieved through the PVD process. Unlike electroplated or lacquered finishes that form surface layers prone to peeling, PVD coatings are physically bonded to the substrate at the atomic level. This eliminates failure modes such as flaking or “peeling skin,” ensuring that the decorative finish maintains its integrity throughout the functional lifespan of the faucet.

These characteristics enable manufacturers to deliver high-end visual finishes with industrial-grade performance, aligning with the growing demand for durable luxury fixtures in premium residential developments and hospitality projects.

Market Opportunity: California Hexavalent Chromium Restrictions Driving Rapid Substitution Toward PVD Faucet Finishes

Regulatory developments in California are creating a strong substitution opportunity for PVD faucet finishes as scrutiny on hexavalent chromium intensifies. Under the Safer Consumer Products program, decorative chromium-plated products are increasingly being classified as priority categories, requiring manufacturers to conduct detailed alternatives assessments.

This regulatory framework is effectively discouraging the continued use of hexavalent chromium plating processes, which involve hazardous chemicals and generate toxic waste streams. PVD technology, as a vacuum-based and zero-discharge process, provides a compliant alternative that eliminates the need for chemical plating baths and associated emissions.

The regulatory trajectory indicates a de facto phase-out of new hexavalent chromium finishing installations, particularly in regions with strict environmental compliance requirements. Faucet manufacturers seeking to maintain market access in California are accelerating the transition to PVD coating solutions, including outsourcing to specialized toll-coating providers.

This shift is expected to drive sustained demand for PVD finishes across North America, particularly in segments where regulatory compliance and environmental certification are critical purchasing criteria.

Market Opportunity: China GB/T 23447-2025 Standard Driving Demand for Low-Leaching, High-Durability Faucet Coatings

China’s updated GB/T 23447-2025 standard is reshaping the faucet finishes market by introducing stricter requirements for material safety and corrosion resistance. The regulation imposes stringent limits on the leaching of heavy metals such as lead, cadmium, and chromium into potable water, significantly impacting the selection of surface finishing technologies.

PVD coatings provide a functional advantage by forming dense, non-porous barrier layers that significantly reduce metal ion migration. Compared to traditional electroplated coatings, PVD finishes can lower heavy metal leaching by approximately 95%, enabling manufacturers to meet the new safety thresholds required for certification in domestic and export markets.

The standard also introduces mandatory corrosion performance benchmarks. Faucets targeting high-quality certification must achieve top-tier ratings in accelerated corrosion testing, including Grade 10 performance in 24-hour copper-accelerated acetic acid salt spray tests. PVD-coated finishes are among the few solutions capable of consistently meeting these requirements without additional protective layers.

Given China’s position as the largest global manufacturing hub for sanitary fittings, the enforcement of these standards is creating a large-scale transition toward advanced PVD coating technologies. Suppliers offering high-performance, compliant, and scalable finishing solutions are well positioned to capture growth in this evolving regulatory environment.

Physical Vapor Deposition (PVD) Faucet Finishes Market Share and Segmentation Insights

Kitchen Faucets Capture 58.6% Share Driven by Wear Resistance and High-End Finishing Requirements

The physical vapor deposition (PVD) faucet finishes market by faucet type is dominated by kitchen faucets, accounting for 58.6% of global market share in 2025, due to their higher exposure to mechanical wear, cleaning chemicals, and frequent handling. PVD coatings such as stainless steel, matte black, and champagne bronze finishes provide superior scratch resistance, corrosion protection, and long-term aesthetic durability, making them essential for high-use kitchen environments. Additionally, kitchen faucets typically have larger surface areas and higher unit values compared to bathroom faucets, justifying the premium cost associated with PVD surface finishing technology. With growing consumer preference for luxury kitchen fixtures, designer finishes, and long-lasting coatings, kitchen faucets continue to drive revenue growth in the decorative PVD coatings market.

B2B (Wholesale/Trade) Segment Holds 65.1% Share Driven by Project-Based Procurement

In the PVD faucet finishes market by sales channel, the B2B (wholesale/trade) segment leads with a 65.1% market share in 2025, reflecting the dominance of contractor-driven procurement and large-scale construction projects. Builders, plumbers, and renovation contractors source PVD-finished faucets through plumbing wholesalers, distributors, and showroom networks, purchasing in bulk at competitive trade pricing. A key factor supporting this dominance is brand-controlled specification, where leading manufacturers such as Delta, Moen, Kohler, and Grohe manage distribution of premium PVD finishes primarily through professional channels to maintain quality standards and brand positioning. This structured supply chain ensures consistent availability for new construction and renovation projects, while limiting direct retail penetration of high-end product lines. As infrastructure development and residential remodeling grow globally, the B2B channel remains central to the global PVD faucet finishes market.

Competitive Landscape of the Physical Vapor Deposition (PVD) Faucet Finishes Market

Kohler Leads Premium PVD Faucet Finishes with Vibrant® Technology and Design Innovation

Kohler Co. dominates the PVD faucet finishes market in North America, leveraging its proprietary Vibrant® technology to deliver long-lasting, corrosion-resistant finishes. Its product portfolio includes high-demand finishes such as Brushed Moderne Brass, French Gold, and Vibrant Titanium, all molecularly bonded for lifetime durability. In 2026, Kohler introduced its “Colors of Nature” initiative, using PVD technology to replicate organic textures while maintaining sustainability standards. The launch of Vibrant® Brushed Bronze with fingerprint-resistant chemistry targets high-traffic hospitality environments. Additionally, Kohler’s expansion of global design centers in India and China enhances localized production and reduces lead times for premium faucet finish solutions.

Hansgrohe Expands Luxury PVD Finish Portfolio with Precision Engineering and Circular Solutions

Hansgrohe Group, including AXOR, is a European leader in high-end PVD faucet finishes, offering precision-engineered solutions for luxury architecture. Its FinishPlus service provides 15 distinct PVD finishes, supported by one of the world’s largest in-house PVD production facilities. In 2026, the company introduced new FinishSets for its iBox Universal 2 platform, ensuring consistent color matching across multiple product lines. Specialized finishes now account for nearly 25% of AXOR’s sales, reflecting strong demand for premium aesthetics. Hansgrohe is also pioneering circular economy initiatives by piloting PVD stripping and recoating services, enabling refurbishment instead of replacement, aligning with sustainability goals.

LIXIL Strengthens Mass-Premium Segment with Sustainable and Advanced PVD Finishing Technologies

LIXIL Corporation, through GROHE and American Standard, is a major player in the mass-premium PVD faucet finishes market. Its GROHE StarLight® technology delivers highly durable surfaces with enhanced hardness, making finishes like Hard Graphite a preferred choice for modern architectural designs. In 2026, LIXIL integrated PVD finishing into its 3D metal printing workflow, enabling complex geometries previously difficult to coat. The company is also positioning PVD as a sustainable alternative to traditional plating, eliminating harmful chromium waste. Its Aqua Sanctuary concept showcases the use of PVD finishes in wellness-focused bathroom designs, reinforcing its innovation leadership.

Delta Faucet Drives Consumer Innovation with Durable and Smart PVD Coating Solutions

Delta Faucet Company is a leader in consumer-focused PVD faucet finishes, combining durability with smart technology integration. Its Brilliance® PVD finishes are recognized for long-term reliability, maintaining performance for over a decade. In 2026, Delta introduced Lumicoat™ finishes that repel water and prevent mineral buildup, addressing key consumer challenges in hard-water regions. The company expanded its product range to include Matte Black PVD finishes, offering improved scratch resistance compared to traditional coatings. By integrating Touch2O® technology with PVD surfaces, Delta enhances hygiene and usability, positioning itself strongly in the smart and durable faucet coatings market.

Dornbracht Elevates Luxury Segment with Precious Metal PVD Finishes and Advanced Surface Technologies

Dornbracht AG & Co. KG is a premium brand in the luxury PVD faucet finishes market, specializing in high-end materials and design innovation. Its Brushed Dark Bronze finish utilizes advanced pre-deposition techniques to create unique visual depth, while its Durabrass series incorporates real gold for unmatched aesthetic appeal. The company has introduced Visible Light Activation technology, enabling self-cleaning surfaces that reduce residue buildup. Dornbracht’s focus on holistic design includes PVD-matched accessories, ensuring consistent aesthetics across bathroom environments. These innovations position Dornbracht as a leader in high-end, design-driven PVD coating solutions.

Moen Expands Smart Home Integration with High-Durability and Antimicrobial PVD Finishes

Moen Incorporated is a key player in the residential PVD faucet finishes market, focusing on durability, affordability, and smart home integration. Its Spot Resist™ PVD technology is widely adopted in retail and DIY segments for its ability to prevent fingerprints and water spots. The company has integrated Microban® antimicrobial protection into its PVD finishes, addressing growing consumer demand for hygiene-focused solutions. Moen’s LifeShine® finishes offer long-term resistance to tarnishing and corrosion, making them popular in multi-family housing projects. Its expansion into smart water systems further enhances its position in the connected and high-performance faucet finishes market.

United States PVD Faucet Finishes Market: Luxury Hospitality Growth and Smart Surface Innovation

The United States remains a premium market in the PVD faucet finishes market, driven by strong demand from luxury hospitality, residential remodeling, and smart home integration. Strategic collaborations between leading manufacturers and high-end hotel chains have accelerated the deployment of black, gold, and brushed PVD finishes across thousands of premium suites, reinforcing the role of PVD in upscale interior design.

Technological innovation is centered on performance-enhanced finishes, such as Lumicoat™ PVD coatings, which resist mineral buildup and water spotting—critical for regions with hard water conditions. The integration of silver-ion antimicrobial PVD coatings in healthcare and commercial environments is further expanding application scope. With rising home improvement spending, PVD finishes are increasingly preferred in master bathroom renovations, outperforming traditional chrome due to durability and aesthetics. Additionally, the U.S. EPA’s recognition of PVD as a sustainable manufacturing process is accelerating the shift away from hexavalent chrome, while brands like Kohler are embedding PVD-coated touchless sensors into smart faucet systems.

China PVD Faucet Finishes Market: High-Volume Production and Dual-Carbon Transition

China dominates the global PVD faucet finishes industry as the largest manufacturing base, rapidly evolving from mass production to premium, export-oriented solutions. Government mandates promoting PVD-coated fixtures in Grade-A residential developments are fueling domestic demand, particularly in Tier-1 cities.

Sustainability initiatives under the Dual-Carbon policy have led to the closure of traditional electroplating lines and the widespread adoption of closed-loop PVD coating systems, significantly reducing environmental impact. Chinese manufacturers are also advancing multi-target vacuum-arc deposition technologies, enabling gradient and customizable finishes for global markets. Investments in digital logistics and smart warehousing have drastically reduced delivery times for custom PVD faucets, strengthening China’s competitiveness. With a dominant share in global exports, particularly in affordable luxury segments, China continues to expand its influence across Southeast Asia and the Middle East.

Germany PVD Faucet Finishes Market: Precision Engineering and Sustainable Water Efficiency

Germany leads Europe’s PVD faucet finishes market through its focus on engineering precision, sustainability, and water efficiency. Leading brands such as Hansgrohe and Grohe are optimizing ultra-thin PVD layers (0.3–0.5 microns), ensuring sharp design aesthetics while maintaining durability and corrosion resistance.

The market is also driven by exports of premium finishes like Rose Champagne and Brushed Nickel, reflecting strong demand across European luxury housing segments. Over 42% of new product launches integrate water-saving technologies, aligning with strict EU regulations. Germany’s push toward circular economy practices includes digital product passports for traceability of rare metals used in PVD processes. Additionally, innovations such as AR-enabled showroom visualization tools are enhancing customer experience by allowing architects and designers to simulate finish textures and lighting effects before installation.

India PVD Faucet Finishes Market: Urban Premiumization and Smart Cities Expansion

India is emerging as the fastest-growing market for PVD-coated faucet finishes, driven by rapid urbanization, luxury real estate growth, and government initiatives like the Smart Cities Mission. Metropolitan regions such as Mumbai, Delhi, and Bengaluru are witnessing strong demand for premium finishes including gold and matte black PVD coatings, particularly in high-end residential projects.

Strategic developments such as the JSW Paints–Akzo Nobel India consolidation are improving access to high-performance PVD precursors, reducing production costs for domestic brands. Government policies, including the extension of PLI schemes to coating machinery, are accelerating the installation of PVD chambers across industrial hubs. Public infrastructure projects are standardizing PVD-coated fixtures for durability and corrosion resistance in high-traffic environments. Additionally, growth in hospitality and destination weddings is driving demand for bespoke finishes in heritage and luxury properties, further expanding India’s premium PVD segment.

Italy PVD Faucet Finishes Market: Design Leadership and Bespoke Luxury Finishes

Italy defines global trends in the PVD faucet finishes market, with a strong emphasis on design innovation, artisanal craftsmanship, and bespoke luxury production. Boutique brands are creating hybrid PVD finishes combining stone, glass, and metal, offering unique textures that cannot be replicated through traditional plating methods.

The country is also driving the “Integrated Bath” concept, where PVD finishes are harmonized across fixtures, hardware, and architectural elements for cohesive interior design. Compliance with EU regulations has accelerated the adoption of lead-free brass PVD coatings, ensuring safety while maintaining premium aesthetics. Italy is at the forefront of fashion-driven PVD colors, including gunmetal and chocolate finishes, which are gaining popularity in luxury real estate markets. Investments in small-scale PVD systems enable the production of limited-edition finishes, positioning Italy as a global hub for high-end, customized PVD solutions.

Turkey PVD Faucet Finishes Market: Strategic Manufacturing Hub for EMEA

Turkey is rapidly emerging as a key PVD faucet finishes production and export hub, bridging European design expertise with Middle Eastern and African demand. Significant investments by major conglomerates in advanced PVD lines are strengthening the country’s manufacturing capabilities, particularly for large-scale construction projects in the Gulf region.

The growth of e-commerce channels is expanding access to premium PVD-coated fixtures, supported by a digitally connected consumer base. Turkey’s strategic role as a gateway for Vision 2030 projects in Saudi Arabia is boosting exports of corrosion-resistant PVD hardware designed for extreme climates. Efforts to localize the production of titanium and zirconium PVD targets are enhancing supply chain resilience, while innovations such as triple-layer PVD coatings are delivering superior salt spray resistance for coastal applications.

Japan PVD Faucet Finishes Market: Precision Sputtering and Hygiene-Driven Innovation

Japan’s PVD faucet finishes market is characterized by precision engineering, advanced sputtering technologies, and hygiene-focused innovations. The use of Digital Mirror Device (DMD) modulated PVD enables highly detailed textures that replicate natural materials such as silk and leather, elevating the tactile experience of premium fixtures.

Functional innovation is a key differentiator, with companies like TOTO integrating photocatalytic PVD coatings that actively decompose bacteria and organic residues using ambient light. Advances in low-energy HiPIMS-based PVD processes are improving coating density while reducing energy consumption. Japan is also pioneering smart faucet technologies, embedding sensors within PVD-coated surfaces for seamless communication with home automation systems. Anti-fogging hydrophilic PVD coatings further enhance durability and aesthetics, while updated JIS standards ensure global leadership in the “healthy home” and smart bathroom segments.

Physical Vapor Deposition Faucet Finishes Market Report Scope

Physical Vapor Deposition Faucet Finishes Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$2.3 Billion

|

|

Market Size (2032)

|

$3.9 Billion

|

|

Market Growth Rate

|

7.9%

|

|

Segments

|

By Finish Color and Aesthetic (Chrome, Nickel, Gold, Black, Bronze, Custom), By Surface Texture (Polished, Brushed, Matte, Textured), By Substrate Material (Brass, Stainless Steel, Zinc, Plastics), By Faucet Type (Bathroom Faucets, Kitchen Faucets), By Technology (Sputter Deposition, Cathodic Arc Evaporation, Thermal Evaporation, Ion Plating), By End-Use Sector (Residential, Commercial, Institutional), By Project Category (New Install, Aftermarket), By Sales Channel (B2B, B2C, Online)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Kohler Co., Hansgrohe SE, Masco Corporation, Grohe AG, Fortune Brands Innovations, Inc., Oerlikon Balzers, IHI Ionbond AG, Hauzer Techno Coating B.V., Vapor Technologies, Inc., Fantini Rubinetti, Dornbracht AG and Co. KG, Bühler Group, PLATIT AG, KCC Corporation, Mustang Vacuum Systems Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Physical Vapor Deposition Faucet Finishes Market Segmentation

By Finish Color and Aesthetic

- Chrome

- Nickel

- Gold

- Black

- Bronze

- Custom

By Surface Texture

- Polished

- Brushed

- Matte

- Textured

By Substrate Material

- Brass

- Stainless Steel

- Zinc

- Plastics

By Faucet Type

- Bathroom Faucets

- Kitchen Faucets

By Technology

- Sputter Deposition

- Cathodic Arc Evaporation

- Thermal Evaporation

- Ion Plating

By End-Use Sector

- Residential

- Commercial

- Institutional

By Project Category

By Sales Channel

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Physical Vapor Deposition Faucet Finishes Industry

- Kohler Co.

- Hansgrohe SE

- Masco Corporation

- Grohe AG

- Fortune Brands Innovations, Inc.

- Oerlikon Balzers

- IHI Ionbond AG

- Hauzer Techno Coating B.V.

- Vapor Technologies, Inc.

- Fantini Rubinetti

- Dornbracht AG & Co. KG

- Bühler Group

- PLATIT AG

- KCC Corporation

- Mustang Vacuum Systems Inc.

*- List not Exhaustive