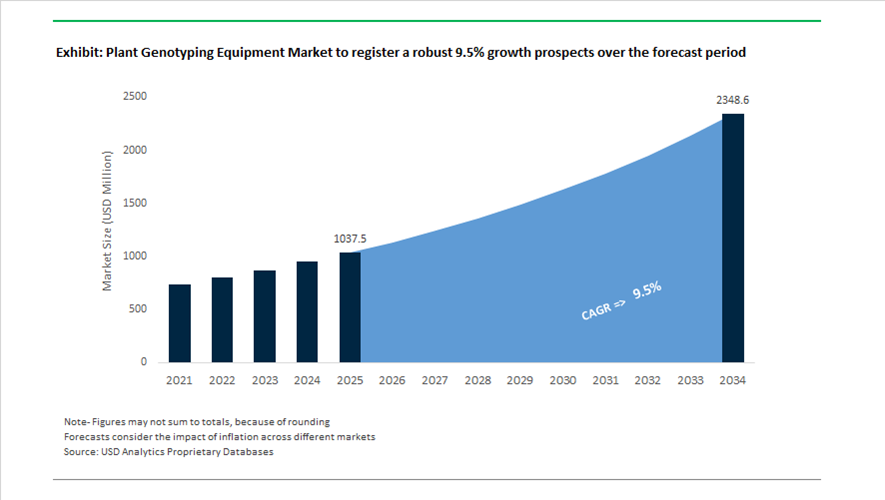

Plant Genotyping Equipment Market Size 2025–2034: $1,037.5 Million to $2,348.1 Million at 9.5% CAGR Driven by NGS Automation, CRISPR Breeding, and AI-Powered Genomics

The global plant genotyping equipment market is projected to grow from $1,037.5 million in 2025 to $2,348.1 million by 2034, registering a CAGR of 9.5%. Growth is being fueled by accelerating adoption of next-generation sequencing (NGS), high-throughput sample preparation platforms, automated extraction systems, CRISPR-enabled crop development, and AI-driven genomic analytics. As global seed companies and ag-biotech firms intensify efforts to develop climate-resilient, high-yield crop varieties, investment in plant DNA sequencing instruments, genotyping-by-sequencing (GBS) workflows, SNP detection systems, and automated laboratory platforms is expanding rapidly.

Strategic acquisitions and workflow integration initiatives in 2024–2025 strengthened market consolidation. In November 2024, Solis Agrosciences acquired the sequencing and bioinformatics platform of Ferris Genomics to integrate advanced genomic analysis directly into molecular breeding pipelines, reducing trait discovery timelines. In April 2025, Eurofins Genomics acquired LGC’s Sanger sequencing operations, reinforcing its foundational validation services even as the industry transitions toward NGS platforms. By August 2025, Eurofins centralized its NGS operations at a new Ebersberg hub in Germany to expand capacity and improve turnaround times for its AgriGenomics division serving global breeding companies.

Technological innovation in sequencing platforms is redefining cost structures and scalability. In June 2024, MGI Tech launched a large-scale low-pass whole genome sequencing workflow tailored for agricultural populations, offering a cost-effective alternative to traditional SNP arrays while capturing broader genetic variation. In 2025, Illumina introduced its 5-Base DNA Prep kits, enabling simultaneous detection of genomic variants and DNA methylation in a single sequencing run—an advancement particularly valuable for studying stress-induced epigenetic modifications in crops. These technologies allow breeders to integrate genomic selection and epigenomic insights into accelerated crop improvement programs.

Automation and high-throughput sample preparation are critical growth drivers. In April 2025, Qiagen initiated phased rollout of the QIAsymphony Connect, capable of processing 96 samples simultaneously, enhancing extraction efficiency for genomics laboratories. The company is preparing a full 2026 launch of QIAsprint Connect, marking its expansion into fully automated, high-throughput processing for plant, soil, and microbial samples. Similarly, in October 2024, LGC Biosearch launched Amp-Seq One, a streamlined one-step targeted GBS workflow reducing library preparation to approximately 120 minutes and eliminating the need for complex liquid handling systems, making high-volume commercial breeding more accessible.

Precision breeding partnerships are increasing equipment demand. In September 2024, Corteva Agriscience partnered with Pairwise to deploy CRISPR-based gene-editing tools aimed at improving crop resilience to extreme weather. Such gene-editing programs require intensive genotyping validation and phenotyping integration, significantly driving instrument utilization rates. Complementing genomic platforms, Agilent introduced the InfinityLab Pro iQ LC-MS series in 2025, enabling precise analysis of plant biomolecules in high-throughput research environments.

AI-enabled laboratory ecosystems are emerging as a structural differentiator. At SLAS2026, Agilent showcased integrated robotics and AI-powered workflow optimization tools developed with ABB and Biosero, demonstrating near-autonomous genotyping labs capable of reducing manual error and improving reproducibility.

Trends and Opportunities in the Global Plant Genotyping Equipment Market

Consolidation Toward End-to-End “Lab-to-Insight” Genotyping Platforms

The plant genotyping equipment market is undergoing a structural transition from fragmented, modular instrument stacks toward fully integrated “lab-to-insight” workflows. Breeding organizations, seed companies, and public research institutes are increasingly prioritizing platforms that unify nucleic acid extraction, library preparation, high-throughput sequencing, and bioinformatics interpretation within a single operational ecosystem. This shift is driven by the need to eliminate data handoff losses, reduce sample processing errors, and compress breeding decision timelines in large-scale genomic selection programs.

A defining inflection point occurred in October 2025 when Illumina unveiled its constellation mapped read technology, designed to resolve complex genic regions and structural variants in a single sequencing workflow. This innovation directly addresses long-standing limitations in short-read genotyping, particularly for polyploid crops and structurally complex genomes such as wheat and sugarcane. The platform is positioned to become a reference architecture for next-generation whole-genome plant analysis.

Vertical integration has further intensified following Illumina’s late-2024 integration of PIPseq™ V technology through the acquisition of Fluent BioSciences. By enabling single-cell transcriptomics and proteomics on the same NovaSeq™ X systems used for standard genotyping, breeding laboratories can now correlate allelic variation with functional expression patterns without migrating samples across platforms. This convergence of genotyping and functional genomics is redefining equipment purchasing decisions, favoring vendors that can deliver scalable, multi-omics compatibility.

Automation is reinforcing this trend. Industry benchmarking data from 2025 confirms that optimized Oxford Nanopore sequencing protocols now require less than half the pipetting steps of legacy workflows, cutting hands-on time by more than 40%. For national germplasm banks and high-volume breeding pipelines processing tens of thousands of samples annually, process intensification has become a decisive ROI driver.

Democratization of Genotyping via Portable and In-Field Sequencing Systems

A parallel trend is the decentralization of plant genotyping from centralized core facilities to greenhouses, quarantine stations, and field locations. Advances in miniaturized PCR and sequencing hardware are enabling real-time genetic diagnostics at the point of need, fundamentally changing how breeding programs respond to disease outbreaks and varietal integrity challenges.

In March 2025, Genome Prairie launched its Genome360 Initiative, deploying mobile laboratories across Canada equipped with Bento Lab portable PCR systems and Illumina iSeq100 sequencers. This model allows immediate pathogen detection such as clubroot in canola and real-time soil microbiome profiling, eliminating multi-week delays associated with centralized lab processing.

Cost compression has accelerated adoption. A 2025 peer-reviewed study demonstrated that Oxford Nanopore target amplicon sequencing can now achieve full-length gene analysis in crops like wheat and sunflower at approximately USD 3.4 per gene. This economics shift makes decentralized SNP and structural variant detection viable even for resource-constrained breeding programs in emerging markets.

Operationally, portable sequencing workflows are delivering actionable results in under 29 hours from DNA extraction to data output. This turnaround speed is becoming mission-critical for agricultural biosecurity, particularly in regions facing climate-driven pest migration and disease pressure where delayed genetic confirmation can translate directly into yield losses.

Genotype-to-Phenotype Integration for Climate-Resilient Crop Development

The most powerful growth opportunity in the plant genotyping equipment market lies in closing the long-standing genotype-to-phenotype gap. Equipment vendors are increasingly aligning genotyping platforms with automated phenotyping systems that use AI-driven imaging, robotics, and environmental sensors to link genetic markers directly to agronomic performance traits.

Evidence from AgriNext 2025 indicates that breeding programs combining AI-enabled genomic selection with CRISPR-Cas9 editing have increased wheat yields by approximately 10% while reducing conventional breeding cycles from 12 years to fewer than 6 years. These gains are contingent on equipment ecosystems capable of synchronizing high-throughput genotyping with continuous phenotypic data capture.

In August 2025, the Advanced Plant Phenotyping Laboratory at Oak Ridge National Laboratory demonstrated an AI-assisted phenotyping platform that automates physiological trait measurement and maps these traits to specific genetic loci at unprecedented scale. Such facilities are setting new benchmarks for equipment interoperability, favoring genotyping vendors that comply with open data standards.

By 2025, the Breeding Application Programming Interface (BrAPI) had achieved near-universal adoption as the interoperability backbone for breeding data. This standardization ensures that genotyping instruments, phenotyping hardware, and decision-support software can operate within a unified predictive framework, enabling global collaboration on drought tolerance, heat resilience, and water-use efficiency traits.

Compliance-Driven Genotyping for Seed Traceability and Identity Preservation

Regulatory enforcement and consumer transparency demands are creating a structurally non-discretionary market for plant genotyping equipment. Seed certification agencies, exporters, and food processors are increasingly required to verify genetic identity to ensure varietal purity, IP protection, and labeling compliance.

A major catalyst emerged in November 2025 with the introduction of India’s Seeds Bill, 2025, which mandates a centralized seed traceability portal requiring QR-linked genetic identity for every seed container. This regulation is driving large-scale deployment of SNP genotyping and real-time PCR systems at seed processing and certification facilities across India, one of the world’s largest seed markets.

Beyond regulation, market forces are reinforcing adoption. Demand for non-GMO certification, varietal differentiation such as high-protein rice or gluten-free oats, and identity-preserved export chains has transformed genotyping into a core quality-control function. Equipment capable of rapid, high-confidence genetic fingerprinting is now essential infrastructure rather than optional R&D tooling.

Government enforcement agencies are also modernizing. Seed inspectors in the EU and Asia are increasingly equipped with portable DNA analyzers to identify spurious or counterfeit seeds directly in the market. In jurisdictions with strong IP enforcement, genetic verification has become the primary mechanism for protecting breeder rights, further expanding the installed base of plant genotyping equipment.

Plant Genotyping Equipment Market Share and Segmentation Insights

PCR and qPCR Systems Lead Plant Genotyping Equipment Adoption in Agricultural Biotechnology

PCR and qPCR systems accounted for 42.80% of the Plant Genotyping Equipment Market by equipment type in 2025, reflecting their central role in plant molecular breeding and genetic analysis workflows. These systems provide reliable DNA amplification and detection capabilities used in marker-assisted breeding, trait identification, and crop quality testing. PCR-based technologies remain widely adopted because they combine high analytical accuracy with relatively low operational cost and established laboratory protocols. In 2025, advancements in high-throughput PCR platforms incorporating automation, microfluidics, and multiplexing technologies are enabling plant breeding programs to process thousands of genetic samples per day while maintaining cost-efficient genotyping performance.

Genomic Selection Applications Drive Plant Genotyping Equipment Demand in Modern Crop Breeding

Genomic selection represented 34.80% of the Plant Genotyping Equipment Market by application in 2025, reflecting its growing role in accelerating crop improvement programs. This breeding approach uses genome-wide molecular marker data to predict the performance of breeding lines before field trials, significantly shortening breeding cycles and improving genetic gain. Agricultural biotechnology companies and research institutes increasingly rely on genomic selection for major crops including corn, wheat, and soybeans. In 2025, advances in genomic prediction models integrating machine learning and artificial intelligence algorithms are improving the accuracy of genomic selection strategies by capturing complex genotype-by-environment interactions and enabling breeders to target traits such as yield stability and stress tolerance.

Plant Genotyping Equipment Market Competitive Landscape

The global plant genotyping equipment market is evolving toward multi-omic, high-throughput systems integrating genomic, epigenomic, and phenomic data. Competition is defined by automation, cloud-enabled analytics, and scalable SNP and sequencing platforms supporting precision breeding and climate-resilient crop development.

Illumina Leads High-Throughput Genotyping with Dual-Omic Sequencing and AI-Driven Genomic Resolution

Illumina, Inc. dominates plant genotyping through advanced sequencing platforms and integrated multi-omics analytics. The 5-base solution launched in October 2025 enables simultaneous detection of genetic variants and DNA methylation, supporting epigenomic research in stress-resilient crops. TruPath™ Genome workflow introduced in February 2026 reduces library preparation time to 10 minutes and delivers up to 16 whole genomes per day for large-scale breeding programs. The Infinium PlantSNP-6 v2 array supports high-density SNP genotyping with optimized workflows for low-input plant samples. The Illumina Connected Multiomics platform integrates DRAGEN™ algorithms to resolve complex polyploid genomes. Strategy focuses on genomics-to-phenotype integration, high-throughput sequencing, and AI-enabled data analysis.

Thermo Fisher Expands Accessible SNP Genotyping with Benchtop NGS and Global Agrigenomics Partnerships

Thermo Fisher Scientific Inc. delivers comprehensive plant genotyping solutions through its Ion Torrent and Applied Biosystems platforms. The company reported $44.56 billion revenue in 2025, supported by growth in agrigenomics across Asia-Pacific and Latin America. The Ion AmpliSeq PlantSNP Genotyping Assay enables analysis of up to 1,000 SNPs per reaction, supporting mid-throughput breeding applications. Strategic collaborations with agricultural institutions, including ICAR, enable deployment of benchtop NGS systems for decentralized genotyping workflows. Axiom™ Plant Genotyping Arrays provide extensive pre-designed panels covering more than 80 plant species. Strategy emphasizes accessibility, scalability, and localized genotyping solutions.

QIAGEN Advances Automated Sample-to-Insight Workflows with High-Throughput Processing and Single-Cell Integration

QIAGEN N.V. is addressing throughput bottlenecks through automation and integrated sample processing technologies. The QIAsprint Connect system launched in February 2026 processes up to 192 samples per run with scalability to 600 samples per day, reducing manual handling. Collaboration with the Max Planck Institute validated QIAsymphony Connect for improved extraction efficiency from complex plant tissues. The acquisition of Parse Biosciences in December 2025 adds single-cell analysis capabilities, enabling cell-level gene expression profiling in plant systems. New consumables reduce plastic usage by up to 50%, aligning with sustainable laboratory standards. Strategy focuses on automation, high-throughput processing, and integrated genomic workflows.

LGC Biosearch Delivers High-Volume SNP Genotyping with Integrated Automation and Proprietary Chemistry Platforms

LGC Biosearch Technologies specializes in cost-effective, high-volume plant genotyping solutions for commercial breeding programs. The partnership with Dynamic Devices integrates robotic liquid handling with SNPline™ and sbeadex™ chemistry, enabling rapid sample-to-result workflows within minutes. The Amp-Seq One platform provides one-step targeted genotyping-by-sequencing with increased throughput for marker validation. The $100 million investment in an oligonucleotide synthesis center in Canada supports production of high-purity reagents for custom assays. KASP™ genotyping technology remains a global standard for SNP analysis in small and mid-scale laboratories. Strategy focuses on vertical integration, automation, and cost-efficient genotyping.

Eurofins Expands Genotyping-as-a-Service Model with Automated Labs and Low-Cost Whole Genome Sequencing

Eurofins Scientific (Eurofins Genomics) operates as a leading service provider influencing plant genotyping equipment demand through large-scale laboratory infrastructure. The company reported 24% EPS growth in 2025 driven by investments in automated genomics labs and digital reporting systems. Expansion of NGS operations in Ebersberg, Germany strengthens high-capacity sequencing capabilities. Acquisition of LGC’s Sanger sequencing business enhances validation and verification services. Partnership with Gencove introduces low-pass whole genome sequencing with imputation, reducing cost per sample for breeding programs. Strategy emphasizes service scalability, automation, and cost-efficient genomic data generation.

Agilent Advances Digital Lab Integration with Genotyping Panels and Accessible Analytical Infrastructure

Agilent Technologies, Inc. is integrating hardware and informatics to support reproducible plant genotyping workflows. The company generated $6.95 billion revenue in 2025 with growing focus on applied agricultural markets. The opening of a refurbishment center in India enhances accessibility of advanced analytical instruments for mid-tier research institutions. Collaboration with ICAR-National Research Centre for Grapes supports genomic traceability and food safety initiatives. SureSelect genotyping panels enable targeted enrichment and deep sequencing of plant genomes across diverse species. Strategy focuses on digital lab transformation, affordability, and high-sensitivity genotyping solutions.

United States – Federally Anchored Genomics with Industrial-Scale Automation

The United States plant genotyping equipment landscape is structurally anchored in federally funded research programs and industrial-scale breeding automation. The USDA Agricultural Research Service is executing its National Program 301 under the 2023–2027 strategic cycle, explicitly prioritizing advanced genotyping to unlock climate-resilient and high-yield crop traits. This policy backbone is translating into sustained demand for high-throughput sequencing platforms, robotic liquid handling systems, and integrated bioinformatics pipelines across public labs and commercial seed developers. Parallel to this, the Agricultural Genome to Phenome Initiative has funded large-scale genotyping projects during 2024–2025, including PacBio Revio-enabled HiFi sequencing of more than 5,000 wheat varieties, reinforcing demand for long-read sequencers and high-fidelity library preparation equipment.

Private-sector consolidation and automation are reinforcing this trajectory. The November 2024 acquisition of Ferris Genomics’ sequencing and bioinformatics assets by Solis Agrosciences created an integrated service pipeline spanning sample prep, sequencing, and data analytics, increasing pull-through demand for end-to-end genotyping workflows. On the technology front, Illumina’s October 2025 launch of its 5-base sequencing chemistry has expanded the functional scope of genotyping equipment to include epigenetic insights, particularly relevant for complex traits in corn and soybean. At the lab level, leading seed companies such as Bayer and Corteva have embedded Agilent Bravo LS and Hamilton STARlet robotic platforms into CRISPR-enabled breeding labs, driving reported productivity gains of up to 80% and accelerating the shift toward fully automated genotyping laboratories.

China – Cost-Optimized Scale and Regulatory Incentivization

China’s plant genotyping equipment market is expanding through regulatory incentives, cost-reduction strategies, and large-scale infrastructure deployment. The revised Regulations on the Protection of New Varieties of Plants, effective June 1, 2025, extend protection periods to 25 years for woody plants and 20 years for others, materially improving the return profile for private investment in genotyping platforms. This regulatory shift is stimulating procurement of high-throughput sequencers and multiplex assay systems by domestic breeding companies seeking to protect and monetize proprietary germplasm.

Technology localization is a central theme. In June 2024, MGI Tech launched its whole-workflow solution for agricultural low-pass whole genome sequencing, specifically engineered to reduce per-sample costs in population-scale studies. This has expanded adoption among provincial breeding programs handling diverse crops from rice and maize to horticultural species. Concurrently, under the 2025–2026 Work Plan for Stabilizing Growth, the government has prioritized domestic production of G5-grade reagents essential for sequencers, directly strengthening upstream supply security for genotyping equipment vendors. The Ministry of Industry and Information Technology digitalization blueprint further accelerates integration of AI and machine learning into genotyping data analysis, increasing demand for compute-integrated sequencing and analysis platforms.

India – Public Infrastructure Meets Precision Breeding

India’s plant genotyping equipment ecosystem is transitioning from fragmented academic use toward coordinated national infrastructure. In December 2025, the Department of Biotechnology launched the National Biofoundry Network, comprising six hubs focused on high-performance biomanufacturing and indigenous genomics. These hubs are expected to drive standardized procurement of sequencers, PCR systems, genotyping arrays, and automation tools tailored to local crop priorities. Complementing this, the launch of the Indian Biological Data Centre portals has made 10,000 whole genome datasets openly accessible, increasing utilization rates of genotyping equipment by reducing duplication and accelerating trait discovery.

Regulatory clarity is reinforcing equipment demand. The 2025 notification of guidelines for genetically engineered plants containing stacked events provides a defined biosafety pathway for multi-trait gene-edited crops, encouraging breeders to invest in precise genotyping and validation tools. Demonstrated outcomes, such as the mid-2025 release of ADT 39-Sub1 rice developed through marker-assisted selection, highlight the practical impact of genotyping platforms in climate-resilient breeding. Across Bengaluru and Hyderabad, CRISPR-Cas9-based SDN1 research programs are further expanding demand for compact, high-accuracy genotyping instruments capable of rapid variant confirmation while maintaining transgene-free status.

European Union (Germany & Switzerland) – Regulatory Enablement and Phenomics Integration

The European Union’s plant genotyping equipment market is being reshaped by regulatory reform and advanced phenomics-genomics integration. The March 14, 2025 endorsement of a new regulation on New Genomic Techniques by the EU Council establishes a Category 1 pathway for NGT plants equivalent to conventional breeding, effectively lowering regulatory friction for genotyping-intensive breeding programs. This policy clarity is particularly significant for Germany and Switzerland, where public-private breeding consortia are scaling investments in high-resolution genotyping platforms.

Technology innovation is centered on efficiency and data integration. In October 2025, Thermo Fisher Scientific introduced the SwiftArrayStudio Microarray Analyser across European labs, reducing hands-on time by 40% and delivering results within 30 hours. The concurrent launch of arrays such as Axiom PangenomePro supports population-scale genotyping aligned with EU breeding initiatives. Germany-based LemnaTec has expanded its Scanalyzer HTS platforms, enabling direct linkage of non-destructive phenotyping with genotypic data and shortening trait validation cycles by roughly 40%, a critical advantage for commercial breeders.

Brazil – Climate-Focused Genomics and Field-Integrated Trials

Brazil’s plant genotyping equipment demand is being driven by climate resilience priorities and strong intellectual property activity. The nationwide Genomics for Climate-Resilient Crops initiative announced in October 2025, with implementation scheduled for Q1 2026, is creating coordinated demand across research hubs for sequencing systems, genotyping arrays, and bioinformatics infrastructure. This initiative aligns with Brazil’s strong patent footprint, with 89,925 agrifood-related patent applications recorded by March 2025, many centered on crop adaptation and genetic improvement.

Institutional capability is anchored by the Embrapa network, which is deploying integrated platforms combining CRISPR-Cas gene editing and proprietary bioinformatics. Equipment demand is increasingly hybrid in nature, linking laboratory genotyping with field-based validation. The surge in mapping and imagery patents during spring 2025 reflects this convergence, as breeders integrate spatial data with genotypic insights, driving adoption of portable and high-throughput genotyping tools optimized for decentralized trials.

Comparative Snapshot – Plant Genotyping Equipment by Region

Plant Genotyping Equipment Market County Level Snapshot

|

Region

|

Primary Demand Driver

|

Dominant Technology Focus

|

Structural Role

|

|

United States

|

Federal programs and seed industry automation

|

Long-read sequencing, robotics, multi-omics

|

Global innovation and scale leader

|

|

China

|

Cost reduction and regulatory incentives

|

Low-pass WGS, multiplex assays, AI analytics

|

High-volume, cost-optimized adopter

|

|

India

|

National infrastructure and precision breeding

|

Marker-assisted genotyping, CRISPR validation

|

Emerging coordinated growth hub

|

|

European Union

|

NGT regulatory reform and phenomics

|

Microarrays, phenomics-genomics integration

|

Standards and integration leader

|

|

Brazil

|

Climate resilience and IP generation

|

Field-linked genotyping, CRISPR platforms

|

Climate-driven application leader

|

Plant Genotyping Equipment Market Report Scope

Plant Genotyping Equipment Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1037.5 Million

|

|

Market Size (2034)

|

$2348.1 Million

|

|

Market Growth Rate

|

9.5%

|

|

Segments

|

By Equipment Type (PCR & qPCR Systems, DNA Sequencing Systems, Microarray Equipment, Mass Spectrometry Systems, Capillary Electrophoresis Systems, Automated Liquid Handling Systems), By Genotyping Methodology (SNP Genotyping, Genotyping-by-Sequencing, SSR Genotyping, Whole Genome Sequencing), By Application (Marker-Assisted Selection, Marker-Assisted Backcrossing, Genomic Selection, Trait Mapping & Discovery, Seed Quality Control), By End-User (Agricultural Biotechnology Companies, Academic & Research Institutes, Contract Research Organizations)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Thermo Fisher Scientific Inc., Illumina Inc., Agilent Technologies Inc., Danaher Corporation, PerkinElmer Inc., MGI Tech Co. Ltd., Pacific Biosciences of California Inc., Bio-Rad Laboratories Inc., QIAGEN NV, Eurofins Scientific SE, BGI Genomics Co. Ltd., Oxford Nanopore Technologies plc, LGC Limited, LemnaTec GmbH, SGS SA

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Plant Genotyping Equipment Market Segmentation

By Equipment Type

- PCR & qPCR Systems

- DNA Sequencing Systems

- Microarray Equipment

- Mass Spectrometry Systems

- Capillary Electrophoresis Systems

- Automated Liquid Handling Systems

By Genotyping Methodology

- SNP Genotyping

- Genotyping-by-Sequencing

- SSR Genotyping

- Whole Genome Sequencing

By Application

- Marker-Assisted Selection

- Marker-Assisted Backcrossing

- Genomic Selection

- Trait Mapping & Discovery

- Seed Quality Control

By End-User

- Agricultural Biotechnology Companies

- Academic & Research Institutes

- Contract Research Organizations

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Plant Genotyping Equipment Industry

- Thermo Fisher Scientific Inc.

- Illumina Inc.

- Agilent Technologies Inc.

- Danaher Corporation

- PerkinElmer Inc.

- MGI Tech Co. Ltd.

- Pacific Biosciences of California Inc.

- Bio-Rad Laboratories Inc.

- QIAGEN NV

- Eurofins Scientific SE

- BGI Genomics Co. Ltd.

- Oxford Nanopore Technologies plc

- LGC Limited

- LemnaTec GmbH

- SGS SA

*- List not Exhaustive