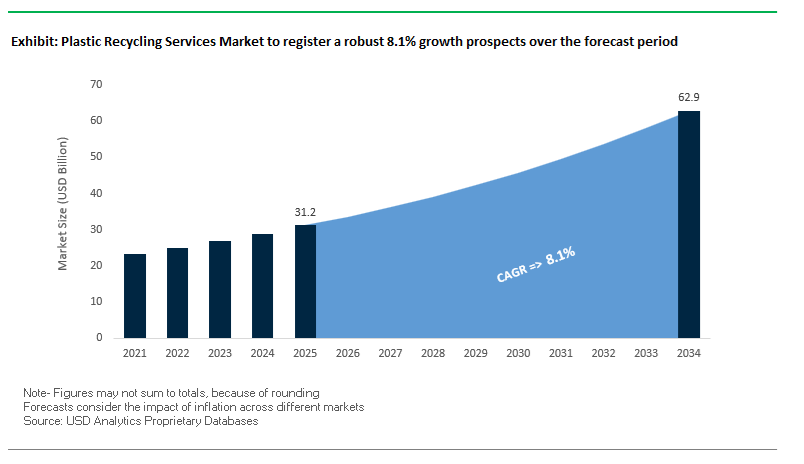

The Global Plastic Recycling Services Market is projected to grow from USD 31.2 billion in 2025 to USD 62.9 billion by 2034, expanding at a CAGR of 8.1%. This robust growth trajectory reflects the accelerating global shift toward circular economy models, heightened regulatory mandates on recycled content, and the scaling of advanced mechanical and chemical recycling technologies. The industry’s evolution is being driven by large-scale investment in collection infrastructure, material recovery efficiency, and feedstock traceability systems, as both developed and emerging economies align with sustainability objectives set under frameworks like the EU Packaging and Packaging Waste Regulation (PPWR) and UNEP’s Global Plastics Treaty.

Professionals in this sector face key operational challenges — balancing energy efficiency, feedstock purity, and output quality — while meeting rising demand from consumer goods, packaging, automotive, and construction end-users. With brands like Unilever, PepsiCo, and L’Oréal committing to integrate over 25% recycled content in plastic packaging by 2030, the market for certified post-consumer resins (PCR) such as rPET and rHDPE is experiencing unprecedented pressure on supply capacity and quality consistency.

Technology integration is transforming industry benchmarks: AI-powered sorting, robotic vision systems, and chemical depolymerization units are reducing contamination and enabling the recycling of once “non-recyclable” streams. Simultaneously, sustainability reporting and digital product passports are becoming mandatory tools for producers to validate recycled content and carbon savings across value chains.

Key Product Insights

- Rising Circularity Metrics: Leading recyclers achieve material recovery rates exceeding 80% for PET and HDPE streams, with AI-based sorting improving yield and purity.

- Energy Efficiency Benchmark: Advanced facilities target below 1,500 kWh per metric ton of PCR, optimizing both cost and carbon intensity.

- Regulatory Transformation: The EU PPWR (effective 2025) mandates all plastic packaging to be recyclable by 2030, reshaping compliance strategies.

- Recycled Content Targets: FMCG and packaging leaders are mandating 25–30% PCR integration in consumer packaging within the next decade.

- Chemical Recycling Expansion: Over 50,000 metric ton per annum facilities are being launched globally, bridging the quality gap between virgin and recycled polymers.

The Plastic Recycling Services Industry is therefore entering a technologically advanced and regulation-driven phase, where traceability, feedstock purity, and end-market demand alignment will determine long-term competitiveness and profitability.

The past year has marked a critical acceleration in global investments, technological upgrades, and regulatory enforcement in the plastic recycling ecosystem.

In October 2025, Borealis announced a major upgrade to its Integra Plastics AD facility in Bulgaria, deploying its proprietary Borcycle™ M mechanical recycling technology to enhance production capacity for premium recycled polypropylene (rPP) beyond 20,000 metric tons annually. The facility’s focus on food-grade and technical polymer grades positions it as a key asset for Europe’s high-specification packaging and automotive sectors.

Similarly, SUEZ Group in August 2025 doubled the capacity of its Landemont, France site dedicated to plastic film recycling, addressing one of the most difficult segments in post-consumer waste processing. The move aligns with Europe’s commitment to resource regeneration and supports growing end-user demand for secondary raw materials (SRM). Meanwhile, Plastipak Packaging, Inc. reported that over 61% of its global energy consumption in 2024 originated from renewable sources, reflecting a sectoral emphasis on reducing carbon footprints in energy-intensive recycling operations.

Emerging economies are also fast becoming growth hotspots. In September 2025, India’s Council on Energy, Environment and Water (CEEW) identified a USD 200 million investment opportunity for establishing a 1,000-kilotonne-per-annum plastic recycling infrastructure in Odisha, signaling a major public-private expansion in Asia’s recycling capacity. Earlier, in February 2025, the Indian government reinforced its Extended Producer Responsibility (EPR) frameworks, incentivizing recyclers and formalizing the informal waste collection sector — an initiative expected to redefine regional feedstock availability and service scalability.

On the corporate innovation front, Borealis received FDA clearance (May 2025) for selected Borcycle™ M grades, allowing their use in food and cosmetics packaging, a milestone that expands the commercial reach of mechanically recycled content. In March 2025, Veolia launched its “GreenUp 2024–2027” strategy, aiming to scale regenerative solutions with over 30 operational plastic recycling plants worldwide. The company’s strategy complements Europe’s transition toward decarbonized resource management, emphasizing closed-loop production.

Globally, rising regulatory pressure — including the EU PPWR (effective February 2025) — and upcoming BPA bans in food-contact plastics (by 2025 end) are pushing recyclers to innovate around additive compatibility, deinking, and migration safety. However, raw material volatility — particularly fluctuations in tin and phosphorous prices — remains a key supply-side constraint. The sector’s long-term competitiveness will hinge on balancing cost efficiency with sustainability-driven innovation and data-verified transparency across supply networks.

Market Trend 1: Strategic Pivot to Advanced Sorting and Washing for Food-Grade rPET and rPP

A defining transformation within the plastic recycling services market is the widespread shift toward super-clean, food-grade recycling lines capable of producing high-purity rPET and rPP resins that comply with food-contact safety regulations. With the implementation of global recycled content mandates—including the EU’s requirement for at least 30% recycled plastic in PET bottles by 2030—recyclers are compelled to invest in capital-intensive, next-generation sorting and washing systems.

The scale of investment required is substantial. A typical food-grade rPET recycling line costs between $20 million and $50 million per production line, with commissioning cycles spanning 18 to 24 months, underscoring the high barriers to entry and the need for long-term strategic partnerships with brand owners. These super-clean recycling facilities integrate near-infrared (NIR) optical sorters, hot caustic washing, and decontamination modules to achieve regulatory compliance from agencies such as EFSA (Europe) and FDA (United States).

Energy efficiency is another focal point. Advanced PET washing systems with 3,000 kg/hour capacity operate at approximately 120 kWh per tonne of output, showcasing a 40% reduction in energy intensity compared to earlier generations. The optimization reflects the industry’s commitment to sustainability and operational cost control in high-volume PCR production. These next-gen facilities are also expanding their polymer range to include food-grade rPP, further diversifying the feedstock mix for packaging converters transitioning toward circular, monomaterial packaging structures.

Market Trend 2: Deployment of Chemical Recycling Technologies for Hard-to-Recycle Plastics

A parallel and equally transformative trend is the industrial-scale deployment of chemical (advanced) recycling technologies, including pyrolysis, solvolysis, and depolymerization, to process complex plastic waste streams—such as multilayer films, mixed polyolefins, and heavily contaminated residues that mechanical recycling cannot efficiently handle.

Leading energy and chemical companies are spearheading the expansion. For instance, ExxonMobil’s $200 million investment aims to process 500,000 tons of hard-to-recycle plastics annually by 2027, establishing one of the world’s largest advanced recycling networks. The commitment drives the strategic pivot toward molecular recycling as a critical enabler of the circular plastics economy.

Technological advances have enabled single-train pyrolysis systems capable of processing 100,000 tonnes per year of mixed plastics, incorporating split-zone reactor configurations that separate melting and reaction phases. The innovation improves feedstock tolerance, allowing for continuous processing of heterogeneous inputs such as multi-layer packaging, agricultural films, and colored plastics.

By transforming waste plastics back into naphtha-like feedstocks, these facilities create virgin-equivalent resins with traceable recycled content, closing the loop for packaging, textiles, and automotive applications. As governments introduce mass balance certification frameworks and chemical recycling quotas, adoption is expected to surge, positioning chemical recyclers as indispensable players in achieving circularity targets.

Market Opportunity 1: Establishing Closed-Loop Recycling Services for Consumer Packaged Goods (CPG) Brands

The rapid expansion of brand-led circularity commitments from major consumer packaged goods (CPG) companies is driving a new service-based business model within the plastic recycling services industry—closed-loop recycling partnerships. These partnerships ensure guaranteed access to high-quality, food-grade PCR for packaging applications, strengthening brand compliance with regional and global recycling mandates.

A notable example is the Closed Loop Partners’ catalytic fund, initiated with $25 million from major chemical corporations including Dow and LyondellBasell, with plans to scale to $100 million. The fund specifically supports the expansion of polyethylene (PE) and polypropylene (PP) recycling infrastructure across North America, providing catalytic financing for localized, closed-loop recycling projects.

The initiative aims to recover and process over 500 million pounds of post-consumer plastic, significantly enhancing the availability of recycled resins for high-volume packaging converters. These vertically integrated recycling service models enable brands to trace material flows, validate recycled content, and ensure consistent resin quality, helping CPG firms meet commitments such as 30% PCR inclusion in primary packaging by 2025–2030.

The rise of such collaborative infrastructure investments marks a strategic shift in the market—from standalone recyclers to value chain-integrated recycling ecosystems, where brand owners, material science companies, and recyclers co-invest in asset development to secure long-term feedstock reliability.

Market Opportunity 2: Developing Specialized Recycling Streams for Automotive and Electronics Plastics

Another high-margin opportunity within the plastic recycling services market lies in the specialized recycling of high-value engineering plastics from End-of-Life Vehicles (ELVs) and Waste Electrical and Electronic Equipment (WEEE). Despite existing vehicle dismantling networks, approximately 800,000 metric tons of plastics from ELVs in Europe are still lost to landfill or incineration annually, representing a massive underutilized resource base for recyclers capable of handling ABS, PC, and PA-based materials.

Emerging EU proposals mandating 25% recycled plastic content in new vehicles by 2030, with a required portion derived from closed-loop automotive recycling, are set to redefine industry supply chains. The regulation creates a guaranteed market for specialized recyclers who can provide r-ABS, r-PC, and r-PA with consistent mechanical and thermal performance suitable for interior trims, dashboards, and under-hood applications.

Recycling companies investing in automated dismantling, polymer-specific sorting (NIR spectroscopy), and high-purity compounding lines are uniquely positioned to lead the niche. Additionally, similar recovery opportunities exist in electronic plastics, particularly housings and connectors made from PC/ABS blends and high-heat-resistant polymers, where recycling innovation is rapidly emerging as a differentiator in the global electronics circular economy.

Plastic Recycling Services Market Share Insights, 2025-2034

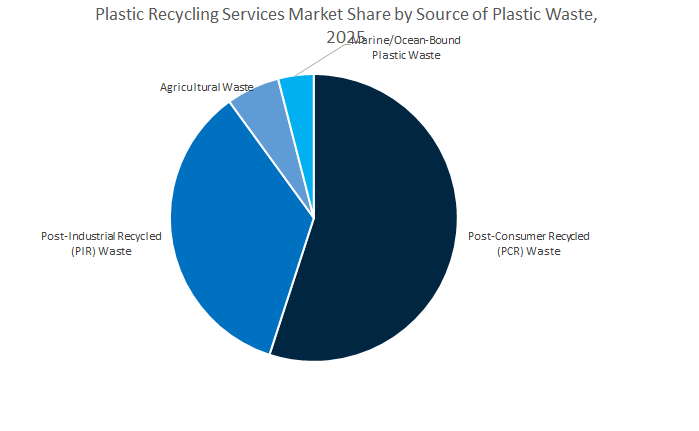

Market Share by Source of Plastic Waste

The Post-Consumer Recycled (PCR) Waste segment dominates the global plastic recycling services market, accounting for a projected 53.2% share in 2025. This dominance is driven by the massive volume of consumer packaging waste, including bottles, films, and containers, generated through retail, e-commerce, and food sectors. The expansion of municipal solid waste collection systems, coupled with Extended Producer Responsibility (EPR) frameworks across the EU, North America, and Asia-Pacific, has significantly boosted PCR supply and processing infrastructure. Brand owners are increasingly committing to recycled content targets—with global leaders pledging to integrate 25–50% PCR materials in packaging by 2030—further strengthening the market share of post-consumer recycling streams. Moreover, continuous advancements in mechanical and chemical recycling technologies have improved the quality of PCR resins, enabling their wider use in high-value applications such as rigid packaging and consumer goods.

Post-Industrial Recycled (PIR) Waste remains a substantial and strategically important segment, offering higher-quality feedstock derived from manufacturing scrap, defective products, and industrial offcuts. These materials are typically cleaner and more homogeneous, making them easier to process and suitable for closed-loop recycling systems used by automotive, electronics, and construction industries. The agricultural and marine waste segments, though smaller in market share, are gaining strategic importance due to the environmental urgency of plastic pollution mitigation. Ocean-bound and fishing net plastics are being increasingly targeted by corporate sustainability initiatives and global cleanup partnerships, particularly in Asia-Pacific and coastal regions of Africa. Recycling companies specializing in marine-grade polymers and reclaimed agricultural films are emerging as key players in the circular economy value chain, supported by incentives, consumer awareness campaigns, and traceability certification systems.

Market Share by End-Use Industry

The packaging sector holds the largest share of the global plastic recycling services market, accounting for approximately 41.6% of total demand in 2025. This segment’s leadership is fueled by the rapid expansion of circular packaging commitments from global brands such as Unilever, Coca-Cola, and Nestlé, which increasingly rely on recycled polyethylene (rPE), polypropylene (rPP), and polyethylene terephthalate (rPET) to meet regulatory mandates and sustainability goals. Recycled plastics are integral to the production of bottles, containers, films, and non-food packaging, where high purity, clarity, and mechanical performance are critical. In parallel, governments are tightening regulations—including the EU’s Single-Use Plastics Directive and California’s recycled content laws—forcing packaging manufacturers to invest heavily in advanced recycling technologies and closed-loop supply chains.

The building and construction sector represents a major downstream market, consuming recycled HDPE, PVC, and PP in durable applications such as plastic lumber, decking, pipes, insulation panels, and geosynthetics. These applications benefit from the lower performance sensitivity of recycled plastics, enabling the use of mixed and lower-grade feedstocks that might not meet food-contact requirements. Textiles and apparel form a rapidly expanding application area, primarily driven by the rPET fiber segment, which feeds into polyester fabrics for clothing, carpets, and upholstery. The rise of sustainable fashion initiatives and corporate commitments to circular textiles are significantly expanding this market segment.

The automotive and transportation industry utilizes recycled engineering plastics such as ABS, PA6, and PBT for interior trims, under-hood components, and structural parts, aligning with OEM sustainability targets and lightweighting trends. However, stringent safety and quality standards limit recycled content penetration compared to packaging or textiles. The electrical and electronics (E&E) sector, meanwhile, leverages recycled plastics in housings, connectors, and casings, though volumes remain moderate due to purity and insulation concerns. Agriculture and other industrial applications—including films, crates, and containers—continue to provide steady demand, particularly in emerging economies adopting recycled materials for low-cost, durable product manufacturing. Across applications, the rising integration of chemical recycling, digital waste traceability, and circular design principles is reshaping market dynamics, ensuring that recycled plastics play a central role in the transition to a low-carbon, resource-efficient global economy.

The Global Plastic Recycling Services Market is defined by technological leadership, vertically integrated operations, and strategic collaborations across mechanical, chemical, and advanced recycling technologies. Key players such as Veolia, SUEZ, Borealis, Plastipak, Neste, and TOMRA Systems are pioneering scalable, circular models backed by digital intelligence, renewable energy, and certified traceability.

Veolia is a global front-runner in ecological transformation, with a robust focus on plastic waste regeneration, energy optimization, and depollution. Operating over 30 recycling plants worldwide, the company’s “GreenUp 2024–2027” strategy earmarks €2 billion in growth investments across its resource regeneration segment. Veolia has also launched one of the market’s first PFAS treatment systems, reinforcing its leadership in addressing contamination within plastic feedstocks. Its advanced recycling facilities play a pivotal role in supplying high-quality PCR resins for automotive, construction, and packaging applications.

SUEZ Group commands strong expertise in waste management, sorting, and resource recovery, processing nearly 32 million metric tons of waste annually across 479 facilities. Its Landemont (France) expansion in 2025 significantly enhanced capacity for recycling plastic films, a segment historically plagued by technical challenges. Producing nearly 2.5 million tonnes of SRM annually, SUEZ stands as one of Europe’s largest recyclate suppliers. The company’s circular integration strategy — including collaborations with CMA-CGM for waste-to-fuel initiatives — underscores its vision for a net-zero circular economy.

Plastipak remains one of the largest global suppliers of Bottle-to-Bottle recycling services, with a recycling capacity exceeding 500 million pounds (≈227,000 metric tons) per year. It specializes in food-grade PET and HDPE, serving major beverage and FMCG companies worldwide. With over 40 operational sites across the U.S., South America, and Europe, Plastipak integrates design innovation and circular manufacturing. Recognized with the PACK EXPO Technology Excellence Award for developing PET from waste carbon, the company continues to push technological frontiers in renewable feedstock and clean energy integration (over 61% renewable energy use as of 2024).

Borealis AG is a core innovator in polyolefin circularity, driving its Borcycle™ M and Borcycle™ C portfolios for mechanical and chemical recycling. Its Integra Plastics AD acquisition in Bulgaria added 20,000+ MT capacity, while new FDA-approved Borcycle™ grades enable food-contact applications. The company’s glass-fiber reinforced rPP compounds (65% PCR content) for automotive use illustrate successful upcycling at industrial scale. Borealis’ strategic integration of recycled and renewable feedstocks into its Porvoo (Finland) cracker highlights its leadership in closing the loop on virgin polymer production.

TOMRA Systems ASA underpins the global recycling infrastructure through sensor-based and AI-enabled sorting technologies. Its solutions are deployed in over 100 countries, supporting deposit return schemes (RVMs) and high-purity material recovery. TOMRA’s Deep Learning algorithms enable enhanced detection of mixed polymer streams, directly improving recovery rates and recyclate purity. Its long-term collaboration with Borealis ensures continuous supply of sorted feedstock for advanced polyolefin recycling, reinforcing its position as the technological backbone of circular material recovery.

Neste Corporation stands at the intersection of renewable fuels and chemical recycling, producing drop-in recycled feedstocks for polymer manufacturing. The company collaborates with Borealis and Covestro to chemically recycle end-of-life tires and mixed plastics into new automotive-grade materials. Through its mass-balance certified liquefied plastic waste feedstock, Neste supports large-scale integration of recycled inputs into refineries and polymer production plants. With strategic investment in scaling chemical recycling capacity, Neste is driving the transition to hard-to-recycle plastic valorization—bridging the gap between waste and virgin-quality materials.

Country Analysis: Regional Growth Dynamics and Strategic Developments in the Global Plastic Recycling Services Industry

United States: Accelerating Advanced Recycling Infrastructure and AI-Powered Waste Management

The United States plastic recycling services market is witnessing a profound transformation, characterized by massive infrastructure investments, advanced recycling technology integration, and corporate sustainability alignment. Major chemical and waste management companies are scaling up chemical recycling capacity through pyrolysis and solvolysis technologies—particularly concentrated in the Gulf Coast region—to process hard-to-recycle plastics, such as multi-layer films, flexible packaging, and mixed polyolefins. The initiatives are positioning the U.S. as a global hub for next-generation recycling solutions that convert plastic waste into high-quality feedstock for circular polymer production.

The rapid adoption of AI-driven sorting systems in Material Recovery Facilities (MRFs) is revolutionizing mechanical recycling efficiency. Platforms such as the AMP Neuron system enable machine learning-based sorting of HDPE, PP, and PET, substantially increasing purity levels and reducing contamination rates. Corporate sustainability mandates are further driving capital inflows into recycling, with major players such as LyondellBasell, Waste Management, and ExxonMobil partnering with Closed Loop Partners to secure consistent Post-Consumer Recycled (PCR) feedstock supply. Complementing The private efforts, federal and state grants have been directed toward upgrading local recycling infrastructure to enhance residential collection and processing efficiency. With its multi-billion-dollar investment in advanced recycling, AI-enabled operations, and policy-backed infrastructure, the U.S. is shaping the future of commercial-scale circular plastic systems.

China: Domestic Recycling Acceleration and Policy-Led Circular Economy Transformation

Following the National Sword Policy of 2018, China has pivoted from being the world’s largest plastic waste importer to becoming a self-sufficient recycling powerhouse focused on domestic waste management and advanced reprocessing technologies. The government’s intensified push for pollution control and sustainable material recovery has fueled large-scale investments in collection, sorting, and reprocessing infrastructure, establishing one of the world’s fastest-growing closed-loop recycling ecosystems.

China’s policy mandates are reshaping market behavior, enforcing a phase-out of single-use plastics and mandating recycled content integration in key industries such as packaging, logistics, and consumer goods. The nation’s PET recycling sector is particularly advanced, with high recovery rates for bottle-to-bottle systems, supported by leading domestic converters producing high-purity PET flakes for both food-grade and industrial use. Technological investments in AI sorting, infrared separation, and chemical depolymerization have enabled the country to process low-value, contaminated plastics that were previously landfilled or exported. Driven by regulatory ambition, industrial investment, and domestic innovation, China is emerging as a global model for circular economy implementation in plastic recycling services.

Germany: EPR Compliance and Chemical Recycling Leadership Underpinning the European Recycling Model

Germany remains the European benchmark for plastic recycling excellence, underpinned by its robust Extended Producer Responsibility (EPR) system, high recovery rates, and cutting-edge recycling infrastructure. The nation’s dual collection system for packaging waste ensures consistent, high-quality feedstock for mechanical recycling facilities, supporting strong circular economy performance across industries. With a recycling rate consistently above EU averages, Germany demonstrates how policy-backed systems and industrial cooperation can achieve large-scale material recovery efficiency.

Germany’s automotive sector is now driving the next phase of recycling innovation by incorporating recycled polypropylene (rPP) and recycled high-density polyethylene (rHDPE) into non-structural and interior vehicle components. Concurrently, leading chemical firms and consortiums are advancing chemical recycling pilot projects—such as pyrolysis and depolymerization—targeting complex multi-layer packaging materials. Furthermore, Germany’s leadership in standardization frameworks like EuCertPlast ensures quality, traceability, and certification of recycled polymers within the European supply chain. Supported by a sophisticated recycling infrastructure and strong environmental policy alignment, Germany continues to lead in technological, regulatory, and industrial dimensions of the plastic recycling services market.

India: EPR-Driven Market Formalization and Rapid Growth in Domestic Plastic Recovery Ecosystems

India is emerging as one of the fastest-growing markets for plastic recycling services, propelled by mandatory Extended Producer Responsibility (EPR) regulations, rising plastic waste generation, and an active informal recycling network transitioning into a formalized system. The Plastic Waste Management Rules and the ban on select single-use plastics (SUP) have created formal demand for Post-Consumer Recycled (PCR) materials, compelling producers and converters to invest in advanced collection, segregation, and reprocessing infrastructure.

Local enterprises such as Gravita India and ReCircle are expanding operations in polyethylene and PET recycling, while Indorama Ventures, a global PET leader, recycles over 1.9 billion bottles annually within India to meet international sustainability targets. Startups are leveraging digital traceability platforms and decentralized collection models to enhance efficiency in waste sourcing and processing. The country’s construction and FMCG sectors are increasingly adopting recycled content packaging and plastic composites, driving further demand for quality PCR feedstock. With strong policy backing, rapid urbanization, and growing investment from domestic and multinational firms, India’s recycling landscape is evolving into a structured, scalable circular economy model within the global plastic recycling services industry.

France: EU-Driven Circular Economy Policies and Global Leadership in High-Purity Recycling Systems

France is at the forefront of Europe’s circular plastic transition, fueled by EU Green Deal directives, domestic mandates on recycled content, and large-scale industrial partnerships. The country’s legislation requires increasing recycled polymer incorporation across packaging sectors, triggering a surge in demand for high-quality PCR materials. Leading waste management corporations such as Veolia and SUEZ, headquartered in France, are expanding their mechanical and advanced polyolefin recycling facilities, both domestically and internationally. The high-capacity plants form the backbone of Europe’s integrated recycling infrastructure, capable of processing diverse plastic streams into high-grade resins.

A defining feature of France’s leadership is its cross-industry collaboration—for instance, partnerships between Veolia and L’Oréal to produce cosmetic-grade PCR plastics from post-consumer packaging waste. The initiatives not only address brand sustainability goals but also create new revenue streams for recyclers focused on premium polymer applications. France’s early compliance with EU recycling targets, combined with its investment in mechanical and chemical recycling hybrid models, underscores its position as a trailblazer in circular packaging innovation and sustainable material management.

Netherlands: European Innovation Center for Chemical Recycling and Circular Waste Valorization

The Netherlands has established itself as a European hub for advanced plastic recycling innovation, driven by technology scale-ups, R&D excellence, and cross-border waste management efficiency. Dutch start-ups and engineering companies, such as BlueAlp, are pioneering chemical recycling systems capable of converting mixed and contaminated plastics into pyrolysis oil, providing feedstock for the production of virgin-equivalent polymers. With a commercial-scale capacity exceeding 17,000 tonnes per facility, The technologies mark a major step toward closing the plastic material loop within Europe’s industrial ecosystem.

The Netherlands’ strategic role extends beyond innovation—it also functions as a regional processing hub under the EU Circular Economy Action Plan, handling and valorizing waste from neighboring countries. Both government and private entities are channeling R&D investments into advanced separation, purification, and solvent-based recycling technologies to tackle complex waste streams like multi-layer films and contaminated flexibles. By integrating circular logistics, chemical recycling, and policy-driven innovation, the Netherlands exemplifies how small, high-tech economies can lead large-scale sustainable transformation in global plastic recycling services.

Plastic Recycling Services Market Report Scope

Plastic Recycling Services Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$31.2 Billion

|

|

Market Size (2034)

|

$62.9 Billion

|

|

Market Growth Rate

|

8.1%

|

|

Segments

|

By Technology (Mechanical, Chemical, Energy Recovery, Advanced/Dissolution, Organic), By Polymer Type (Polyethylene Terephthalate, High-Density Polyethylene, Low-Density Polyethylene, Polypropylene, Polystyrene, Polyvinyl Chloride, Acrylonitrile Butadiene Styrene, Others), By Source of Plastic Waste (Post-Consumer, Post-Industrial, Agricultural, Marine/Ocean-Bound), By Service Component (Collection & Sorting, Processing & Reprocessing, Consulting & Compliance, Equipment & Technology Supply), By End-User (Packaging, Automotive & Transportation, Building & Construction, Textiles & Apparel, Electrical & Electronics, Agriculture, Others), By Equipment & Machinery (Sorting, Washing & Drying, Shredders & Granulators, Extrusion & Pelletizing, Chemical Reactor Systems

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Veolia, SUEZ, Waste Management, Inc. (WM), Plastipak Holdings, Inc., Indorama Ventures Public Company Limited, KW Plastics, LyondellBasell Industries N.V., Biffa plc, Republic Services, Inc., Custom Polymers, Inc., MBA Polymers Inc., Teijin Limited, Berry Global Inc., TerraCycle, AMP Robotics

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

By Recycling Process/Technology

- Mechanical

- Chemical

- Energy Recovery

- Advanced/Dissolution

- Organic

By Polymer Type

- Polyethylene Terephthalate

- High-Density Polyethylene

- Low-Density Polyethylene

- Polypropylene

- Polystyrene

- Polyvinyl Chloride

- Acrylonitrile Butadiene Styrene

- Others

By Source of Plastic Waste

- Post-Consumer

- Post-Industrial

- Agricultural

- Marine/Ocean-Bound

By Service Component

- Collection & Sorting

- Processing & Reprocessing

- Consulting & Compliance

- Equipment & Technology Supply

By End-Use Industry

- Packaging

- Automotive & Transportation

- Building & Construction

- Textiles & Apparel

- Electrical & Electronics

- Agriculture

- Others

By Equipment & Machinery

- Sorting

- Washing & Drying

- Shredders & Granulators

- Extrusion & Pelletizing

- Chemical Reactor Systems

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Plastic Recycling Services Market

- Veolia

- SUEZ

- Waste Management, Inc. (WM)

- Plastipak Holdings, Inc.

- Indorama Ventures Public Company Limited

- KW Plastics

- LyondellBasell Industries N.V.

- Biffa plc

- Republic Services, Inc.

- Custom Polymers, Inc.

- MBA Polymers Inc.

- Teijin Limited

- Berry Global Inc.

- TerraCycle

- AMP Robotics

*- List not Exhaustive

Research Coverage

This report investigates the Global Plastic Recycling Services Market, delivering analysis reviews on demand, pricing, and capacity outlooks while it highlights regulatory inflection points (PPWR, EPR), scale-up economics for mechanical vs. chemical routes, and bankable KPIs across yield, purity, and energy intensity; it maps technology breakthroughs—from AI-enabled sorting to food-grade decontamination and mass-balance certified chemical recycling—and translates them into procurement, investment, and partnership playbooks. Built by USDAnalytics, the study benchmarks feedstock quality risk, end-market pull (packaging, automotive, construction, textiles), and traceability readiness (digital product passports), compares operator cost curves and carbon intensity, and stress-tests scenarios under policy enforcement and resin-price volatility—making this report an essential resource for executives, investors, and operations leaders tasked with de-risking supply, locking PCR quality, and scaling circularity through 2034.

Scope Highlights

Segmentation:

- By Recycling Process/Technology: Mechanical; Chemical; Energy Recovery; Advanced/Dissolution; Organic.

- By Polymer Type: Polyethylene Terephthalate; High-Density Polyethylene; Low-Density Polyethylene; Polypropylene; Polystyrene; Polyvinyl Chloride; Acrylonitrile Butadiene Styrene; Others.

- By Source of Plastic Waste: Post-Consumer; Post-Industrial; Agricultural; Marine/Ocean-Bound.

- By Service Component: Collection & Sorting; Processing & Reprocessing; Consulting & Compliance; Equipment & Technology Supply.

- By End-Use Industry: Packaging; Automotive & Transportation; Building & Construction; Textiles & Apparel; Electrical & Electronics; Agriculture; Others.

- By Equipment & Machinery: Sorting; Washing & Drying; Shredders & Granulators; Extrusion & Pelletizing; Chemical Reactor Systems.

- By Region: North America (United States, Canada, Mexico); Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe); Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC); South & Central America (Brazil, Argentina, Rest of SCA); Middle East & Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa).

Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

Timeframe: Historic data from 2021–2024 and forecast data from 2025–2034.

Companies: Analysis/profiles of 15+ companies.

Deliverables

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.