Driving Modern Innovation: A Comprehensive Analysis of the Global Platinum Group Metals (PGM) Market

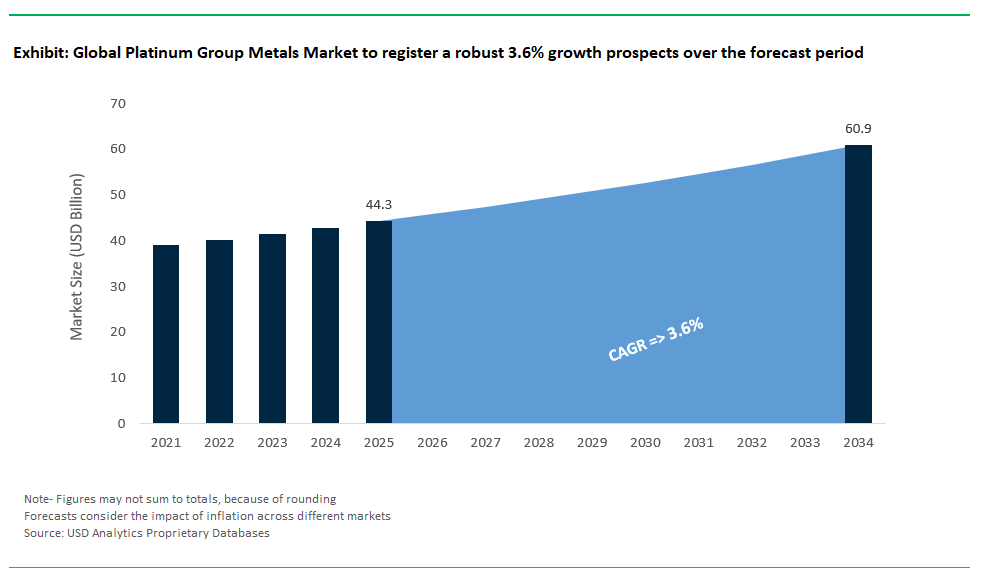

Valued at $44.3 billion in 2025 and forecast to reach $60.9 billion by 2034 at a CAGR of 3.6%, the Platinum Group Metals (PGM) market stands at the nexus of modern technological progress and environmental stewardship. Comprising six precious elements – platinum, palladium, rhodium, iridium, ruthenium, and osmium – PGMs are valued for their peerless catalytic prowess, corrosion resistance, and thermal stability. These special properties serve as the basis for a range of critical activities, from automotive emission control, through fuel cell technologies, to various sets of electronics, chemical processing, and even high-end jewelry.

"Electric motors and other devices that contain thin layers of rare earth could be the first products for turning the lab-scale material into mass-market goods, several companies and analysts say. On the other hand, the supply side is highly concentrated with sales from South Africa and Russia dominating global PGM output and, as such, the sector is susceptible to geopolitical events and threats to the supply chain. The rapid move towards PGM recycling, particularly from end-of-life catalytic converters, is reforming global supply dynamics and sits at the heart of circular economy and sustainability aspirations. While the PGM sphere looks set to continue being critical to global industry as well as the clean energy transition, the market is going to be increasingly important as end-user requirements become more varied and investment in clean energy increases.

Strategic Investments and Innovations Reshape the Global PGM Supply Chain

The last twelve months have been a year of transformation for the Platinum Group Metals sector, characterized by headline investment, increased resource definition and strategic entries into new geographies and applications. Progress continues at flagship South African Waterberg project In July 2025, Platinum Group Metals Ltd. PTM announced the continued advancement of its high-grade Waterberg project, located in South Africa, funded by a C$1 million private placement and a US$50 million at-themarket equity program. PTM also announced the signing of an MOU with Saudi partners together with the Ministry of Investment to contemplate the development of a new PGM smelter and refinery in Saudi Arabia (the same possibly being a significant development with respect to global PGM processing diversification.

There is an increasing amount of secondary recovery and joint venture work. Byblos investee business, Sylvania Platinum’s Thaba JV with ChromTech has commenced production in South Africa’s Bushveld Complex, targeting PGMs from historic tailings and run-of-mine ore, an initiative that advances secondary PGM production, while reducing environmental impact of disposals from historic mining activities. In research and development (R&D), Sibanye-Stillwater and Heraeus Precious Metals have established a collaboration to pioneer unique PGM applications within the hydrogen economy, centred on palladium-based fuel cell catalysts. Regional exploration is also picking up, such as Karelian Diamond Resources initiating PGM exploration in Northern Ireland – a potential indicator of additional supplies from beyond traditional producers.

PGM producers are also turning to the capital markets more and more in order to finance project development, e.g., $12m raised for Waterberg in PTM’s equity program. Collectively, these moves – alongside shared investments made in recycling technologies – are reinforcing supply chain resilience, as well as helping the sector adapt to changing global demand, particularly with PGMs playing an increasingly essential role in decarbonisation and clean energy technologies.

Decarbonization and Supply Security: Key Trends and Emerging Opportunities in the Platinum Group Metals Market

Rapid Expansion of the Hydrogen Economy and Fuel Cell Technologies

A major trend in the PGMs market is the soaring demand from the hydrogen economy and fuel cells usage. (1) Governments in North America, Europe and Asia are also jump-starting green-hydrogen production with ambitious incentives, tax credits (Canada’s 40% clean-hydrogen credit, America’s Inflation Reduction Act), and gigawatt-scale investments in deploying electrolyzers. This policy-driven momentum is quickly ramping up the required amounts of platinum and iridium essential catalysts for hydrogen-fuel-cells and PEM-electrolysers.

By the end of this decade, platinum demand in hydrogen could rise to as much as 11.2% of global platinum consumption, according to industry estimates. Iridium, which is a critical element for electrolyzer anodes, now looks set to be the fastest-growing PGM. That growth is not confined to policy alone: multi-gigawatt electrolyzer orders and programs like HySA in the Middle East, Australia and beyond, as well as research programs such as in Hydrogen South Africa, are deploying PGM-rich technology and enablng new boundaries of energy. It is these forces that are resulting in record levels of R&D dollars being spent on further refining PGM catalysts to improve efficiency, reduce PGM loading, resistance to durability challenges to create new strategic relationships between miners, refiners, and clean energy technology manufacturers. The upshot: a key diversification of PGM demand far beyond traditional auto catalysts.

Growing Importance of PGM Recycling for Supply Security and Sustainability

With risks to the geopolitical and operational environment of primary PGM mining only increasing – notably due to South Africa and Russia’s dominant position in mine supply – recycling is an increasingly important source of supply for security and circularity. PGMs recycling, particularly from ‘end-of-life’ autocatalysts, is a fast-growing business – returning raw material processing efficiencies of 95% at facilities such as Umicore’s and therefore a financial, as well as grammatical, imperative.

The major refiners are spending on hydrometallurgical and pyrometallurgical processes that can recover from automotive and industrial waste streams. The supply is increasing globally as older, higher load vehicles are scrapped and as electronics and industrial uses of lead have increased. Automakers and electronics companies are using recycled PGMs to meet carbon-neutral procurement goals, and industry leaders such as Johnson Matthey are expanding their recycling operations to mitigate supply chain risk. The industry is seeing new urban mining business models, whereby miners are partnering with recyclers to establish closed loop systems, which are making secondary PGM supplies more international.

Competitive Landscape: Industry Leaders and Strategic Innovators in the Platinum Group Metals Market

A handful of major mining and refining companies, supported by focused technology developers and recyclers, dominate the Platinum Group Metals industry. Their investments, partnerships, and R&D priorities set the pace for sectoral transformation.

Anglo American Platinum Limited: Global Leadership and Integrated PGM Operations

Anglo American Platinum is the world’s largest platinum producer, operating primarily in South Africa’s Bushveld Complex. With vast reserves and vertically integrated mining-to-refining operations, the company supplies a full suite of PGMs for autocatalysts, jewelry, electronics, and investment markets. Anglo American is at the forefront of responsible mining and operational efficiency, supporting the hydrogen economy and fuel cell adoption through the World Platinum Investment Council and direct market development initiatives. Their strategic focus is on cost optimization, high production levels, and advancing the role of PGMs in future clean technologies.

Impala Platinum Holdings Limited (Implats): Diversified Resources and Value Chain Integration

Implats is a leading integrated PGM producer, with mining, smelting, and refining operations spanning South Africa, Zimbabwe, and Canada. Its diversified portfolio spanning platinum, palladium, rhodium, and other PGMs serves automotive, jewelry, and chemical end-markets. Implats is strategically investing in downstream processing and exploration, maintaining a robust supply chain while broadening its geographic and product footprint. The company’s focus on operational efficiency and hydrogen economy applications positions it well for the evolving PGM landscape.

Norilsk Nickel: Palladium Powerhouse and Arctic Mining Giant

Norilsk Nickel is the world’s largest palladium producer and a key supplier of platinum and rhodium, leveraging its immense Arctic mineral resources in Russia. With an integrated mining and metallurgical complex, Norilsk delivers cost advantages and production scale unmatched in the market. The company is modernizing its mining infrastructure and taking steps to address environmental concerns, with a clear strategic focus on maintaining palladium leadership and navigating geopolitical supply challenges.

Sibanye-Stillwater: Diversification and Technological Collaboration

Sibanye-Stillwater is a diversified precious metals group with deep PGM mining assets in South Africa and the United States. Its recent strategic moves such as collaborating with Heraeus Precious Metals to advance hydrogen economy applications underscore a focus on both geographic and commodity diversification. Sibanye-Stillwater is also expanding into battery metals and investing in future-facing commodities, strengthening its resilience and growth prospects.

Johnson Matthey plc: Global Leader in PGM Refining, Recycling, and Sustainable Technology

Johnson Matthey leads the global market in PGM refining, recycling, and advanced catalyst manufacturing. As the largest recycler of secondary PGMs, the company is vital to the circular economy. Johnson Matthey’s R&D investments are driving new advances in fuel cell and electrolyzer catalysts and in PGM recovery technologies. Their comprehensive PGM management spanning trading, refining, and catalyst manufacturing positions Johnson Matthey at the heart of the sector’s push toward clean energy, supply security, and environmental responsibility.

Platinum Group Metals (PGM) Market Share Analysis: Segment Insights for 2025

Platinum and Palladium Remain Dominant; Rhodium and Iridium Gain Strategic Importance

Platinum continues to be the dominant metal in the global PGM market, accounting for 35% of demand by 2025 due to strong demand for diesel automotive catalysts, high-end jewellery and emerging hydrogen fuel cell applications. Because of the metal’s catalytic performance and wide industrial applicability, its demand remains strong in the global bridal jewellery markets of China and India, and in worldwide hydrogen energy infrastructure. Palladium has a robust 30% share and maintains its leading position in the gasoline engine catalytic converters as emissions regulation is increasing around the world. But the auto industry is now taking a closer look at platinum as a possible stand-in, because of pesky price and supply issues. Rhodium is currently the costliest PGM and is crucial to efficient NOx removal in gasoline autocatalysts, in particular under Euro 7 and China VI regulations. Iridium and ruthenium are gaining momentum: iridium for PEM electrolyzers and high temperature aerospace components, and ruthenium from semiconductors and data storage. Osmium demand as a highly specialized metal group is small, but its role in medical implants or alloys with other precious metals continues to support the market prospects.

Automotive Catalysts Dominate, with Fuel Cells and Electronics Accelerating Future Growth

The automotive sector commands a commanding 45% share of global PGM demand in 2025, underscoring the metals’ irreplaceable function in catalytic converters to meet ever-stricter emissions regulations worldwide. Jewelry maintains a 20% share, driven by platinum’s cultural prestige in Asian bridal markets and palladium’s appeal as a white gold alternative. The fastest growth, however, is expected in fuel cells and green hydrogen technologies, where platinum and iridium are essential for PEM electrolyzers and electric vehicle stacks. Electrical and electronics applications are also rising, with ruthenium and iridium crucial for advanced semiconductors, hard drives, and OLED production. The chemical industry, glass and ceramics manufacturing, medical devices, and investment segments all contribute to the diversification and resilience of global PGM demand, especially as new energy and digital technologies scale up worldwide.

.png)

South Africa: World’s Primary PGM Producer and Hydrogen Innovation Hub

South Africa is the largest producer of platinum, palladium and rhodium in the world, and the Bushveld is the most prolific source of ore in the world. The continuing investment in mining infrastructure and processing centers within South Africa promises a continuous supply of primary PGMs, and initiatives such as Hydrogen South Africa (HySA) seek to leverage these materials to enable South Africa to become a global leader in green hydrogen solutions. Large mining companies are enhancing the recovery efficiency, processing tailings via secondary recovery and developing new green applications. Current partnerships like Sibanye-Stillwater with Heraeus Precious Metals and Tech JV of Sylvania Platinum’s Thaba underscore a shift towards added-value processing and innovation. Yet changing mining legislation and laborer dynamics continue to play a role, affecting investment and operational consistency.

South Africa’s PGMs are the primary material in global supply chains for automotive catalysts and nascent energy technologies. As demand for fuel cells and green hydrogen infrastructure grows, the country’s mining, refining and hydrogen innovation will be more important than ever. As even intermittent supply interruptions testify, South Africa continues to meet new challenges with strategic partnerships and technological advancement and thus its central position in the PGM ecosystem remains assured.

Russia: Palladium Powerhouse Amid Geopolitical Complexity

Russia is the world’s largest source of palladium and a leading producer of platinum and rhodium. The nation’s large, vertically integrated mining, metallurgical industries serve worldwide automobile, industrial and jewelry markets with much needed PGMs. Geopolitical and international political situations can greatly impact global PGM trade flow, pricing, and the stability of the market with Russia as a key, if unpredictable, player in the supply chain.

Russia’s strategic aim still is to maximize its dominant palladium supply, to create more integrated production and, to cope with outside challengers. Industrial consumers around the world, particularly for gasoline auto catalysts, are keenly watching Russian supply trends. Canadian technological know-how means efficient extraction and refining but regulatory and political developments continue, injecting uncertainty and potentially some volatility into global PGM pricing and trading.

United States: Innovation and Clean Energy Driving Demand and Domestic Supply

The US is both a major consumer and innovator in the PGM sector (through extensive R&D investments in catalytic, fuel cells, electronic applications). Federal policies, like the Inflation Reduction Act, are driving cleantech hydrogen development, thereby increasing demand for platinum in PEM electrolyzers and fuel cell vehicles. The Stillwater Complex in Montana is home to the nation’s primary domestic PGM production and is important for the supply chain security of key industries.

American industry is the global leader in automotive catalyst technology and recycling, investing heavily in advanced pollution control and green energy. Strategic objectives are directed towards enhancing diversity of supply for PGM, fostering local mining and scaling up recycling to reduce import dependency. The fact that entities such as Platinum Group Metals Ltd. (PTM) trade on US capital markets is another indication of US dominance or control in the global dynamic of PGM finance and project development – even where the production asset is offshore. The presence of companies like Platinum Group Metals Ltd. (PTM) on US capital markets further reflects American influence in global PGM finance and project development, even when production assets are located abroad.

Japan: Technology Leader and Clean Energy Pioneer

Japan plays a pivotal role in global PGM demand, fueled by leading-edge R&D in hydrogen fuel cells, automotive catalysts, and high-tech electronics. The government actively promotes hydrogen adoption and FCEV rollout, directly boosting platinum and palladium requirements. Japanese manufacturers are global pioneers in developing more efficient and lower-loading PGM catalyst formulations for emission control and fuel cell technologies.

Japan’s robust electronics sector relies on ruthenium and iridium for semiconductors, hard drives, and display technologies. Strategic investments in recycling and overseas PGM assets, such as the Waterberg Project in South Africa, highlight Japan’s commitment to resource security and innovation. Ongoing collaboration between government agencies and private industry ensures that Japan remains at the forefront of PGM technology and application development.

China: World’s Largest Consumer and Emission Standards Driver

China’s rapid growth in automotive manufacturing, including gasoline, hybrid, and electric vehicles, is the primary engine of PGM demand globally. The country is implementing ever-stricter vehicle and industrial emission standards, requiring increased PGM loadings in catalytic converters and industrial processes. China is also ramping up investments in hydrogen energy and fuel cells, further expanding platinum and iridium consumption.

Chinese companies are focused on securing long-term PGM supply, investing in recycling, and scaling up local processing. Demand is also buoyed by the jewelry market and significant use of ruthenium in electronics manufacturing. Recent data show a surge in physical PGM buying, both for industrial use and investment, confirming China’s pivotal role as a global demand center and price setter in the PGM industry.

Zimbabwe: Rising Producer with Strategic Growth Potential

Zimbabwe is home to the Great Dyke, a major PGM-bearing geological structure, making it an important and growing supplier of platinum, palladium, and rhodium to global markets. Efforts to attract foreign investment and upgrade mining infrastructure are central to the government’s strategy for economic development. Zimbabwe’s regulatory landscape and political environment present challenges, but ongoing improvements are positioning the country as a more attractive destination for international mining capital.

The country’s ability to increase its global PGM share will depend on stable policy frameworks and continued investment in extraction and processing technology. Zimbabwe’s reserves and output are vital for the diversification and security of global PGM supply chains, especially as demand rises for green hydrogen, automotive, and electronics applications.

Canada: Responsible Extraction and Clean Energy Applications

Canada is emerging as a notable PGM supplier, with significant deposits in regions such as the Sudbury Basin and robust mining expertise. Government incentives for clean hydrogen and green energy projects including a 40% tax credit are driving new demand for platinum and iridium. Canadian miners are investing in advanced extraction technologies and responsible production methods to improve recovery and environmental performance.

PGMs produced in Canada serve domestic and export markets, particularly for automotive catalysts, fuel cells, and industrial uses. The country’s strategic focus on supply chain diversification, clean energy, and sustainable resource development is positioning it as a key player in North American and global PGM markets.

Platinum Group Metals Market Report Scope

Platinum Group Metals Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$44.3 Billion

|

|

Market Size (2034)

|

$60.9 Billion

|

|

Market Growth Rate

|

3.6%

|

|

Segments

|

By Metal Type (Platinum, Palladium, Rhodium, Iridium, Ruthenium, Osmium)

By Source (Primary (Mined), Secondary (Recycled))

By Application (Automotive Catalysts (Gasoline, Diesel, Hybrid, Heavy-Duty Vehicles), Jewelry, Chemical Industry (Catalysts, Pigments), Electrical & Electronics (Hard Disks, Sensors, Capacitors, Connectors), Fuel Cells (PEM Electrolyzers, Fuel Cell Electric Vehicles - FCEVs), Glass, Ceramics, and Pigments, Medical & Dental, Investment (Bars, Coins, ETFs), Other Industrial Applications (Turbine Blades, Laboratory Equipment)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Anglo American Platinum Limited, Impala Platinum Holdings Limited, Norilsk Nickel, Sibanye-Stillwater, Johnson Matthey plc, Platinum Group Metals Ltd., Northam Platinum Holdings Limited, African Rainbow Minerals Limited, Glencore plc, Heraeus Holding, Umicore, Metal Concentrators (Pty) Ltd., Tanaka Kikinzoku Kogyo K.K., Chimet S.p.A., JX Nippon Mining & Metals Corporation

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Platinum Group Metals Market Segmentation

By Metal Type

- Platinum

- Palladium

- Rhodium

- Iridium

- Ruthenium

- Osmium

By Source

- Primary (Mined)

- Secondary (Recycled)

By Application

- Automotive Catalysts (Gasoline, Diesel, Hybrid, Heavy-Duty Vehicles)

- Jewelry

- Chemical Industry (Catalysts, Pigments)

- Electrical & Electronics (Hard Disks, Sensors, Capacitors, Connectors)

- Fuel Cells (PEM Electrolyzers, Fuel Cell Electric Vehicles - FCEVs)

- Glass, Ceramics, and Pigments

- Medical & Dental

- Investment (Bars, Coins, ETFs)

- Other Industrial Applications (Turbine Blades, Laboratory Equipment)

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Platinum Group Metals Market

- Anglo American Platinum Limited

- Impala Platinum Holdings Limited

- Norilsk Nickel

- Sibanye-Stillwater

- Johnson Matthey plc

- Platinum Group Metals Ltd.

- Northam Platinum Holdings Limited

- African Rainbow Minerals Limited

- Glencore plc

- Heraeus Holding

- Umicore

- Metal Concentrators (Pty) Ltd.

- Tanaka Kikinzoku Kogyo K.K.

- Chimet S.p.A.

- JX Nippon Mining & Metals Corporation

* List Not Exhaustive

Research Coverage

This report from USDAnalytics provides an in-depth, fact-driven investigation of the global Platinum Group Metals (PGM) Market, offering comprehensive analysis reviews and industry breakthroughs across the entire value chain. It examines market segmentation by metal type, source, and application, highlights the regulatory, technological, and geopolitical forces shaping global supply and demand, and assesses opportunities from the hydrogen economy, electronics, and medical technologies. Covering historic data (2021–2024) and forecast trends (2025–2034), this report is an essential resource for mining companies, manufacturers, investors, and policymakers navigating a rapidly evolving PGM landscape.

By Metal Type: Platinum, Palladium, Rhodium, Iridium, Ruthenium, Osmium

By Source: Primary (Mined), Secondary (Recycled)

By Application: Automotive Catalysts (Gasoline, Diesel, Hybrid, Heavy-Duty), Jewelry, Chemical Industry, Electrical & Electronics, Fuel Cells, Glass/Ceramics/Pigments, Medical & Dental, Investment, Other Industrial

Geographic Scope: 25+ countries across North America, Europe, Asia Pacific, South America, Middle East & Africa

Companies Covered: Anglo American Platinum, Impala Platinum, Norilsk Nickel, Sibanye-Stillwater, Johnson Matthey, Platinum Group Metals Ltd., Northam Platinum, African Rainbow Minerals, Glencore, Heraeus, Umicore, Metal Concentrators, Tanaka, Chimet, JX Nippon Mining & Metals

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.