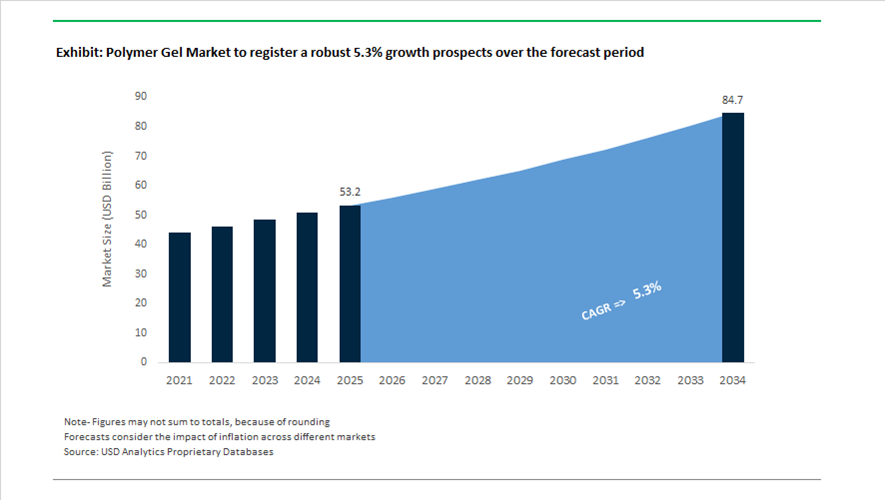

Polymer Gel Market Size Reaches $53.2 Billion in 2025, Projected to Hit $84.7 Billion by 2034 at 5.3% CAGR

The global polymer gel market is valued at $53.2 billion in 2025 and is projected to reach $84.7 billion by 2034, expanding at a CAGR of 5.3% during the forecast period. Growth is anchored in rising demand for hydrogels, super-absorbent polymers (SAP), smart gels, medical-grade polymer matrices, and high-performance gel materials across healthcare, hygiene, agriculture, electronics, and specialty packaging applications. The market is undergoing structural transformation driven by material science innovation, vertical integration among polymer manufacturers, and increasing regulatory focus on medical and sustainable polymer formulations.

In March 2024, Linxens and Clayens introduced a medical tracker embedded directly within polymer gel substrates, enabling real-time physiological monitoring through wearable hydrogel patches. This integration of conductive electronics with biocompatible polymer gels marked a pivotal convergence of medical devices and advanced materials engineering. In April 2024, IIT Mandi developed multifunctional smart microgels derived from natural polymers for controlled fertilizer release and soil moisture retention, accelerating adoption of hydrogel technology in precision agriculture and climate-resilient farming systems. In June 2024, researchers at North Carolina State University published findings on “glassy gels,” a new class of polymer gels containing over 50% liquid while demonstrating plastic-like rigidity and high fracture resistance. This breakthrough materially expands durability thresholds for next-generation gel materials used in structural, biomedical, and industrial environments.

Innovation momentum accelerated in 2025. In February 2025, researchers introduced double-network self-strengthening hydrogels capable of rapid structural hardening under mechanical stress, mimicking muscle adaptation. In June 2025, Sumitomo Seika expanded polymer hydrogel production capacity in Southeast Asia to address surging demand for hygiene and incontinence products, particularly in aging populations. In July 2025, Evonik launched a medical-grade super-absorbent polymer gel engineered for advanced wound care applications, integrating antimicrobial functionality and optimized moisture management for chronic wound treatment. In August 2025, Tokyo-based startup Gellycle commercialized its uniform-mesh “Tetra-Gel” hydrogel platform and initiated development of gel-based artificial tendons and ligaments for regenerative medicine, signaling commercial traction in tissue engineering and biomimetic polymer gels.

Corporate consolidation and application-focused polymer additive innovation are shaping 2026 developments. In October 2025, Daicel Corporation announced its acquisition of Polyplastics through an absorption-type split effective April 2026, consolidating engineering polymers and gel technology development under unified management to accelerate R&D synergies. In early 2026, Scott Bader entered a distribution partnership with Sandtech in France to strengthen European penetration of specialty resins and gelcoats, reinforcing the role of advanced gel chemistries in high-performance composite markets. In February 2026, Milliken unveiled a next-generation portfolio of polymer additives at PlastIndia, targeting medical and food packaging sectors to enhance polymer matrix clarity, stability, and performance in gel-based formulations.

The polymer gel market is transitioning from conventional absorbent materials toward functional, bio-integrated, and mechanically adaptive gel systems, supported by breakthroughs in crosslinking chemistry, nano-structured polymer networks, and sustainable feedstock development. Continuous advancements in hydrogel durability, antimicrobial performance, regenerative biomaterials, agricultural smart gels, and specialty packaging polymers are reshaping the competitive landscape and expanding high-margin application domains across global markets.

Market Trends and Strategic Opportunities in the Polymer Gel Market

Rapid Commercialization of Polymer Gels in Next-Generation Battery Electrolytes and Separators

Polymer gels are moving from laboratory validation into early-stage commercialization as battery manufacturers seek safer, higher-energy-density alternatives to conventional liquid electrolytes. The transition toward quasi-solid and gel-based electrolytes is being driven by the need to suppress dendrite growth in lithium-metal anodes while improving thermal stability in electric vehicles and stationary energy storage systems. Unlike liquid electrolytes, polymer gel systems combine mechanical integrity with ionic mobility, reducing leakage risks and improving interfacial contact between electrodes.

By early 2025, leading automotive OEMs such as Toyota and battery suppliers including Samsung SDI had publicly reaffirmed their solid-state and hybrid electrolyte roadmaps. Samsung SDI, which holds approximately 19.5% share in advanced electrolyte innovation, is scaling polymer gel matrices to lower interfacial resistance, one of the most persistent bottlenecks in fast-charging battery architectures. These gels are increasingly used as compliant interlayers that maintain electrode contact during volume expansion and contraction over extended cycling.

Investment is also accelerating in hybrid polymer gel systems that integrate ceramic fillers to enhance ionic conductivity without sacrificing flexibility. By mid-2025, companies such as Wildcat Discovery Technologies had shifted toward polymer-ceramic hybrid gels designed to withstand more than 3,000 charge-discharge cycles required for grid-scale energy storage. This approach balances the brittleness of pure ceramic electrolytes with the mechanical resilience of polymers.

Regulatory pressure is reinforcing this shift. Safety-focused mandates across the European Union and North America are favoring non-flammable electrolyte solutions. Industry assessments from late 2024 indicate that PVDF- and PEO-based gel electrolytes can eliminate liquid leakage risks and reduce the complexity of thermal management systems, lowering total battery pack costs by up to 15% for OEMs.

Precision Agriculture Adoption of Polymer Gels as Functional Soil Conditioners

In agriculture, polymer gels are transitioning from niche soil additives to essential tools for water and nutrient management in water-stressed regions. This trend is driven by chronic water scarcity, rising irrigation costs, and stricter environmental controls on fertilizer runoff. Cross-linked superabsorbent polymer gels are being engineered to act as underground water reservoirs, improving soil structure and crop resilience.

A widely cited April 2025 study confirmed that targeted application of superabsorbent polymer gels can increase soil water holding capacity by as much as 34.9%. In sandy soils, these gels reduce deep percolation losses and enable irrigation frequency reductions of up to 30% while maintaining stable crop yields. This performance has positioned polymer gels as a core input in precision irrigation programs.

Regulatory scrutiny on microplastics is also reshaping product design. According to March 2025 industry disclosures, manufacturers are rapidly shifting from synthetic polyacrylamide gels to biodegradable, natural polymer-based systems derived from cellulose and starch. These bio-based gels are increasingly co-formulated as controlled-release carriers for nitrogen and phosphorus, addressing the fact that 40 to 70% of applied nitrogen is typically lost through leaching and volatilization.

Large-scale adoption is emerging in arid regions. Under the 2025 Qatar Research, Development and Innovation grant programs, field trials demonstrated that polymer gels can improve crop tolerance to saline soils by acting as osmotic buffers. This capability is opening new demand channels across the Middle East and North Africa, where soil degradation and salinity are structural agricultural challenges.

Medical-Grade Bio-Adhesive Polymer Gels for Advanced Wound Management

Healthcare represents one of the fastest-growing opportunity areas for polymer gels as wound care shifts toward bioactive and patient-adaptive solutions. Modern hydrogel dressings are no longer passive coverings but multifunctional platforms that regulate moisture, deliver therapeutics, and respond dynamically to wound conditions.

By November 2025, publications indexed in PubMed Central indicated a fourfold increase in hydrogel wound-healing patents since 2020. The most commercially attractive designs incorporate pH-sensitive and temperature-responsive mechanisms that release antimicrobial agents or growth factors only when infection markers are detected. This selective response reduces antibiotic overuse and improves healing outcomes.

The rising incidence of chronic wounds is reinforcing demand. Clinical data from 2025 shows that advanced hydrogel dressings reduce tissue maceration by maintaining optimal moisture balance and accelerate re-epithelialization by 25 to 40% compared with conventional foam-based dressings. Shear-thinning polymer gels are particularly valuable in diabetic foot ulcers and venous leg ulcers, where conformability to irregular wound geometries is essential for patient comfort and clinical efficacy.

Soft Robotics and Wearable Sensors Enabled by Self-Healing Conductive Gels

The convergence of materials science and electronics is creating a premium niche for conductive polymer gels in soft robotics and wearable sensing. Ionic hydrogels and organogels allow devices to flex, stretch, and self-repair while preserving electrical conductivity, a combination that rigid materials cannot achieve.

In November 2025, researchers at RIKEN announced a gold-bonded, self-healing polymer gel capable of restoring both mechanical integrity and electrical pathways after damage. This thioether-functionalized system is designed for wearable electronics exposed to repeated bending, offering a pathway to longer device lifetimes and reduced electronic waste.

Energy-harvesting applications are further expanding the opportunity set. A September 2025 MDPI report identified polymer gel-based triboelectric nanogenerators as a critical enabler for self-powered wearable sensors. These gels function simultaneously as flexible electrodes and triboelectric layers, allowing devices to harvest energy from body motion and skin deformation. This positions polymer gels at the core of the emerging Internet of Bodies ecosystem, where continuous sensing and autonomy are key value drivers.

Polymer Gel Market Share and Segmentation Insights

Synthetic Polymer Gels Dominate Due to Controlled Performance and Industrial Scalability

Synthetic gels accounted for 52.80% of the Polymer Gel Market by material type in 2025, driven by their precisely controlled chemical structure, consistent performance, and large-scale manufacturing capability across multiple industries. Synthetic polymer gels such as polyacrylates, polyacrylamides, polyvinyl alcohol, and silicone-based gels are widely used in personal care, healthcare, and industrial applications where controlled absorption capacity, mechanical stability, and durability are critical. Superabsorbent polyacrylate gels remain the dominant material used in hygiene products and water management applications. In 2025, research and development in biodegradable synthetic polymer gels has intensified, focusing on modified polyvinyl alcohol systems and aliphatic polyester-based gels that maintain high absorption performance while enabling environmentally responsible degradation.

Personal Care and Hygiene Segment Drives Global Demand for Superabsorbent Polymer Gels

Personal care and hygiene represented 42.80% of the Polymer Gel Market by application in 2025, reflecting the massive consumption of superabsorbent polymer gels used in disposable hygiene products such as baby diapers, adult incontinence products, and feminine hygiene items. Polyacrylate-based superabsorbent polymers provide high fluid absorption capacity, fluid retention, and leak prevention, making them essential materials in modern hygiene product design. Global population growth, aging demographics, and increasing hygiene awareness continue to drive consumption of these products worldwide. In 2025, sustainable hygiene product development has become a major innovation focus, with manufacturers exploring biodegradable superabsorbent polymers and thinner absorbent core technologies that reduce material usage while maintaining high absorption performance in next-generation hygiene products.

Polymer Gel Market Competitive Landscape

The global polymer gel market is evolving toward stimuli-responsive hydrogels, bio-based SAPs, and aerogel-based thermal barriers. Competition is shaped by EV battery safety, wearable healthcare diagnostics, and sustainable polymer gel technologies enabling high-performance, multifunctional applications.

LG Chem Drives EV Battery Safety with Aerogel-Based Nexula® Thermal Barrier Systems

LG Chem is advancing polymer gel innovation through aerogel-integrated thermal barrier materials for EV battery safety. The Nexula® platform, launched in March 2026, delivers high-performance thermal insulation to delay thermal runaway in battery packs. Its dual-layer safety system combines engineering plastics with aerogel gels to prevent heat propagation in high-density modules. A strategic MoU with EL Electric supports development of flame-retardant EV cables using ultra-high molecular weight polymers with 30% higher flexibility. Vertical integration into precursor-free cathode materials strengthens synergy with gel electrolyte systems. Strategy focuses on EV safety, thermal management gels, and integrated battery material ecosystems.

Evonik Expands High-Purity SAP and Smart Gel Portfolio for Medical and Additive Manufacturing Applications

Evonik Industries AG leads in specialty superabsorbent polymers and advanced polymer gels for healthcare and industrial applications. The launch of antimicrobial SAP gels in July 2025 enhances wound care through superior moisture management and healing efficiency. Strong 2025 performance in Smart Materials and Specialty Additives supports continued growth in high-margin gel applications. The use of ISCC PLUS-certified ammonia BMBcert™ feedstock strengthens its sustainable polymer gel supply chain. Collaboration with Desktop Metal enables qualification of INFINAM® ST 6100L photopolymer gels for industrial 3D printing. Strategy emphasizes medical-grade gels, circular feedstocks, and high-performance additive manufacturing materials.

Sumitomo Chemical Accelerates Smart Gel Development with AI-Driven Molecular Design and SAP Expansion

Sumitomo Chemical is scaling polymer gel capabilities under its “Leap Beyond” strategy, targeting healthcare and ICT sectors. Expansion of hydrogel production in Southeast Asia supports rising demand for SAPs in hygiene and incontinence products. The company has developed biomass-derived super engineering plastics, including LCPs, for high-strength gel matrices in electronics. Recognition as a Clarivate Top 100 Global Innovator in 2026 highlights its advanced R&D capabilities. Its AI Native Company structure enables digital molecular design of smart gels for targeted drug delivery systems. Strategy focuses on AI-driven innovation, high-performance hydrogels, and regional capacity expansion.

Arkema Strengthens Specialty Polymer Gel Portfolio with Fast-Curing Systems and Battery Material Integration

Arkema is positioning itself as a specialty materials leader through advanced polymer gel intermediates and curing technologies. The Luperox® NeatCure system enables rapid, dust-free curing of elastomers, improving process safety and efficiency. A €650 million capital expenditure plan supports expansion in high-performance sealants and bio-based coatings utilizing polymer gel technologies. Strategic pricing adjustments in 2026 ensure continued investment in next-generation materials amid supply chain volatility. Arkema’s presence at InterBattery 2026 highlights its focus on solid-state and semi-solid gel battery materials. Strategy centers on specialty polymers, curing innovation, and energy storage applications.

Nippon Shokubai Dominates SAP Value Chain with Biomass-Based Gels and Advanced Thermal Storage Materials

Nippon Shokubai leads the acrylic acid and SAP market with a strong focus on sustainability and innovation. ISCC PLUS certification enables supply of biomass-balanced polymer gels for hygiene and coating applications. Collaboration with Hokkaido University and Toyo Aluminium supports development of latent heat storage microcapsules using polymer gel cores. Expansion into Halal-certified SAP production in Indonesia targets high-growth markets in Southeast Asia and the Middle East. The Open Innovation Center accelerates commercialization of regenerative gels for drug delivery and 3D cell culture systems. Strategy emphasizes sustainable SAP production, thermal energy storage, and biomedical gel applications.

Cosmo Speciality Chemicals Expands Functional Polymer Gels with PFAS-Free Processing Aids and High-Performance Masterbatches

Cosmo Speciality Chemicals is emerging as a key player in functional polymer gels and specialty masterbatches. The expansion of CosmoWhite and CosmoAdd portfolios includes PFAS-free polymer processing aids that enhance gel rheology and extrusion performance. Integration with its films business supports development of UV-stable and thermally stable polymer matrices for packaging and non-wovens. The company focuses on application-specific masterbatches that improve durability and moisture retention in polymer-based products. Strong FY2025 growth in specialty segments supports further global expansion plans. Strategy centers on value-added polymer gels, sustainable additives, and packaging innovation.

China – Functional Gels Moving from Academic Proof to Industrial Platforms

China’s polymer gel ecosystem is rapidly transitioning from laboratory validation to application-driven industrialization, supported by national manufacturing and sustainability priorities. In early 2026, researchers at the Chinese Academy of Sciences demonstrated the commercial potential of bio-functional gels by integrating garlic-derived nitrogen-doped carbon dots into whey protein–starch emulsion gels. This breakthrough enabled real-time microbial spoilage detection in food logistics, signaling strong downstream demand for smart packaging polymer gels in cold-chain and e-commerce distribution. Parallel to this, Nanjing’s designation as host city for the Polymers 2026 International Conference reinforces its role as a national hub for biomedical gels, self-healing polymers, and next-generation functional gel architectures.

Industrial pull is equally strong in advanced manufacturing and energy storage. Redirected funding under Made in China 2025 has accelerated the scale-up of conductive hydrogel “electronic skins” for soft robotics and precision automation. In agriculture, the large-scale deployment of bio-based superabsorbent polymer gels across Northern China in 2025 reflects policy-backed adoption to combat water scarcity and stabilize crop yields. Meanwhile, battery manufacturers are expanding gel polymer electrolyte production for semi-solid-state batteries, positioning polymer gels as a critical enabler for higher energy density EV platforms targeted for 2026 launches.

India – Agriculture-Led Demand and Domestic Gel Manufacturing Protection

India’s polymer gel market is being shaped by agricultural productivity goals, petrochemical integration, and trade protection measures. In March 2025, Gulbrandsen announced a new specialty polymer facility in Dahej, scheduled for mid-2026 completion, aimed at functional polymer gels and waxes for personal care and industrial coatings. This investment strengthens domestic supply chains at a time when the government has imposed anti-dumping duties on selected polymer precursors from China and Japan to shield local gel and resin producers from price erosion.

Agricultural applications remain a primary growth vector. The Indian Council of Agricultural Research reported in late 2025 that SPG1118 hydrogel application at low dosages significantly improved chickpea seed yields by stabilizing root-zone hydration. Complementing this, Department of Science & Technology-backed startups commercialized biodegradable starch-graft-polyacrylate gels as seed coatings to improve germination in high-value horticulture. Beyond agriculture, petrochemical majors including Reliance Industries and GAIL are advancing polyacrylamide-based gel R&D for enhanced oil recovery, reinforcing polymer gels as a strategic material across energy and food security priorities.

Germany – Decarbonized SAPs and High-Value Technical Gel Innovation

Germany continues to position itself as the global benchmark for sustainable and high-performance polymer gel technologies. In February 2025, BASF introduced HySorb® B 6610 ZeroPCF, the first polyacrylate superabsorbent polymer gel certified with a zero product carbon footprint, manufactured within the Antwerp Verbund ecosystem. This launch underscores Germany’s leadership in biomass-balance and carbon-neutral gel production for hygiene and medical applications. German manufacturers are also accelerating the transition to renewable energy-driven gel production to reduce Scope 3 emissions in feminine hygiene and adult incontinence products.

Beyond absorbents, Germany’s innovation focus extends into mobility and healthcare. Evonik Industries launched thermally conductive polymer gels in late 2025, engineered for heat dissipation in high-power EV charging modules. Concurrently, research clusters around Ludwigshafen are piloting 3D-printable, resorbable hydrogel systems for bone and tissue regeneration, with clinical validation expected in late 2026. These developments position Germany at the intersection of sustainability, electrification, and advanced medical polymer gel applications.

Japan – Scaling SAP Innovation and AI-Centric Thermal Gels

Japan’s polymer gel industry is characterized by precision scaling, global certification, and electronics-driven applications. In May 2025, Sumitomo Seika Chemicals completed a dedicated SAP pilot plant at its Himeji Works, creating a bridge between laboratory innovation and mass production. This facility enables faster commercialization cycles for next-generation absorbent gels. Sustainability credentials were further reinforced when Nippon Shokubai obtained ISCC PLUS certification in the U.S. for acrylic acid and SAP production, enabling global supply of net-zero carbon polymer gels.

Thermal management represents another strategic pillar. Shin-Etsu Chemical commercialized pump-out-resistant thermal gels in 2025, specifically designed for high-density AI computing clusters and data centers. These gels address reliability challenges under repeated thermal cycling, reinforcing Japan’s role in high-value electronic and AI infrastructure polymer gel markets.

United States – Defense, Medical Training, and Industrial Gel Distribution

The U.S. polymer gel landscape is increasingly shaped by defense funding, industrial distribution strategies, and advanced medical simulation. In February 2025, Univar Solutions secured exclusive rights to distribute BASF LuquaSorb® superabsorbent polymer gels for industrial applications across North America, targeting CASE sectors that require controlled rheology and absorption performance. This distribution move strengthens the availability of high-specification gels for coatings and sealants.

Public-sector funding is catalyzing next-generation applications. The U.S. Army Corps of Engineers issued a 2026 challenge focused on stimuli-responsive polymer gels integrated into smart textiles for soldier protection and adaptive camouflage. In parallel, Gelastomerics LLC, working with Colorado State University, unveiled a hydrogel-elastomer composite in late 2025 that closely mimics human soft tissue. This innovation is gaining traction in surgical training and biomechanical simulation, highlighting the U.S. emphasis on defense and healthcare-driven polymer gel development.

Comparative Snapshot – Polymer Gel Industry by Country

Polymer Gel Market County Level Snapshot

|

Country

|

Primary Demand Driver

|

Key Polymer Gel Focus

|

Strategic Positioning

|

|

China

|

Smart packaging, EVs, water efficiency

|

Biosensor gels, SAPs, gel electrolytes

|

Scale-driven industrialization

|

|

India

|

Agriculture and domestic manufacturing

|

Hydrogels, seed-coating gels, EOR gels

|

Food security and localization

|

|

Germany

|

Decarbonization and EV transition

|

Zero-PCF SAPs, thermal gels, medical hydrogels

|

Sustainability and high-value tech

|

|

Japan

|

Electronics and global certification

|

SAPs, AI-server cooling gels

|

Precision scaling and electronics

|

|

United States

|

Defense, healthcare, industrial CASE

|

Smart textile gels, training hydrogels

|

Application-led innovation

|

Polymer Gel Market Report Scope

Polymer Gel Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$53.2 Billion

|

|

Market Size (2034)

|

$84.7 Billion

|

|

Market Growth Rate

|

5.3%

|

|

Segments

|

By Material Type (Synthetic Gels, Natural Gels, Hybrid & Composite Gels), By Form (Amorphous Gels, Semi-Crystalline Gels, Crystalline Gels, Aerogels & Xerogels), By Stimuli Responsiveness (pH-Responsive Gels, Temperature-Responsive Gels, Electro & Magneto-Responsive Gels, Photo-Responsive Gels), By Application (Healthcare & Medical, Agriculture & Water Management, Personal Care & Hygiene, Energy & Electronics, Industrial Applications)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF SE, Nippon Shokubai Co. Ltd., Sumitomo Seika Chemicals Co. Ltd., Evonik Industries AG, LG Chem Ltd., Dow Inc., SABIC, Formosa Plastics Corporation, Songwon Industrial Co. Ltd., Reliance Industries Limited, Kao Corporation, Sanyo Chemical Industries Ltd., Chemtall, Covestro AG, Huntsman International LLC

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Polymer Gel Market Segmentation

By Material Type

- Synthetic Gels

- Natural Gels

- Hybrid & Composite Gels

By Form

- Amorphous Gels

- Semi-Crystalline Gels

- Crystalline Gels

- Aerogels & Xerogels

By Stimuli Responsiveness

- pH-Responsive Gels

- Temperature-Responsive Gels

- Electro & Magneto-Responsive Gels

- Photo-Responsive Gels

By Application

- Healthcare & Medical

- Agriculture & Water Management

- Personal Care & Hygiene

- Energy & Electronics

- Industrial Applications

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Polymer Gel Industry

- BASF SE

- Nippon Shokubai Co. Ltd.

- Sumitomo Seika Chemicals Co. Ltd.

- Evonik Industries AG

- LG Chem Ltd.

- Dow Inc.

- SABIC

- Formosa Plastics Corporation

- Songwon Industrial Co. Ltd.

- Reliance Industries Limited

- Kao Corporation

- Sanyo Chemical Industries Ltd.

- Chemtall

- Covestro AG

- Huntsman International LLC

*- List not Exhaustive