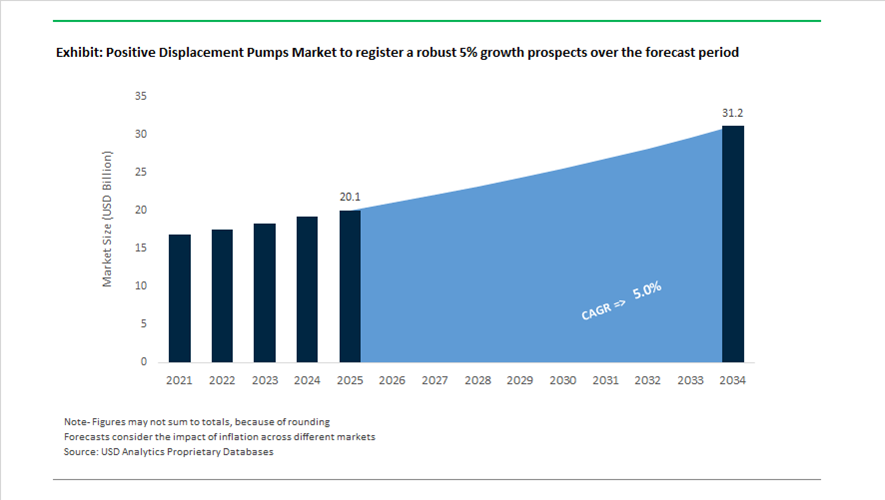

Positive Displacement Pumps Market Valued at $20.1 Billion in 2025, Projected to Reach $31.2 Billion by 2034 at 5% CAGR

The global positive displacement pumps market is valued at $20.1 billion in 2025 and is projected to reach $31.2 billion by 2034, expanding at a CAGR of 5%. Demand is rising across oil and gas, wastewater treatment, biopharmaceutical manufacturing, food and beverage processing, mining, specialty chemicals, and energy infrastructure where precise flow control, high-pressure capability, and viscous fluid handling are critical. Growth is closely tied to industrial automation, energy transition investments, Middle East EPC project expansion, and the increasing adoption of IIoT-enabled pump monitoring systems.

In April 2024, Flowserve secured over $150 million in original equipment pump contracts from international EPC firms supporting large-scale energy and infrastructure developments in the Middle East. These multi-year projects underscore renewed capital expenditure in upstream, downstream, and water infrastructure, directly supporting demand for high-pressure gear pumps, screw pumps, diaphragm pumps, and peristaltic pumps. In November 2024, DXP Enterprises strengthened its industrial pump distribution footprint through the acquisition of Burt Gurney & Associates and MaxVac Inc., enhancing its presence in vacuum and water-business pumping systems.

M&A momentum intensified in early 2025. In February 2025, DXP Enterprises acquired Arroyo Process Equipment, reinforcing its regional pump distribution network. In March 2025, Honeywell International announced the $2.16 billion acquisition of Sundyne, a producer of high-pressure pumps and compressors, expanding Honeywell’s capabilities in petrochemical, LNG, and hydrogen-related flow control applications. In the same month, Ingersoll Rand revealed plans to acquire ILC Dover, integrating liquid handling and positive displacement pump technologies with single-use systems for biopharma manufacturing. This alignment reflects rising demand for sanitary PD pumps, single-use bioprocessing pumps, and contamination-controlled fluid transfer systems in pharmaceutical production. Also in March 2025, PSG Biotech introduced a new SumoFlo® sensor delivering a 150:1 turndown ratio for precision control in bioprocessing pumps, following its 2024 CELE-8103-D display transmitter launch.

Product innovation continued across multiple end-use sectors in 2025. In February 2025, SPX FLOW launched the APV DW+ Series positive displacement pump line with 27 models engineered for high-viscosity applications in food, personal care, and industrial coatings, emphasizing pulsation-free flow to protect downstream equipment. In March 2025 at ISH, Grundfos introduced Alpha1 and 2 GO circulator pumps integrated with digital commissioning via the Grundfos GO app, reinforcing the push toward IIoT-enabled energy-efficient pumping systems in residential and commercial environments. In April 2025, NETZSCH installed eight PERIPRO peristaltic pumps at an energy self-sufficient wastewater treatment plant in Singapore, highlighting the role of PD pumps in circular-economy infrastructure. In May 2025, Roto Pumps introduced its P-Range for harsh mining, wastewater, and oil and gas environments, targeting abrasive and high-solids applications.

Further consolidation occurred in August 2025 when CIRCOR acquired Flowserve’s herringbone gear pump product line, strengthening its aerospace and industrial flow control portfolio. In October 2025, Atlas Copco Group completed the acquisition of CRI-MAN S.p.A., integrating slurry-handling chopper pump technology into its Industrial Flow division to support biogas and wastewater sectors.

The positive displacement pumps market is increasingly shaped by high-pressure process pumps for energy projects, sanitary PD pumps for biopharma, slurry and chopper pumps for wastewater, peristaltic pumps for sustainable treatment plants, IIoT-integrated circulator pumps, and precision gear pumps for aerospace and chemical processing. Strategic acquisitions, regional EPC-driven capital cycles, and digital monitoring integration are redefining competitive dynamics across global industrial pumping systems.

Trends and Opportunities in the Positive Displacement (PD) Pumps Market

Strategic Pivot to Digital-Enabled Positive Displacement Pumps for Predictive Maintenance

The Positive Displacement pumps market is undergoing a decisive transition from equipment-centric sales to digitally enabled lifecycle solutions. End users in oil and gas, chemicals, power generation, and mining are increasingly prioritizing uptime economics, where a single unplanned outage can exceed USD 1 million per day in lost production. In response, PD pump manufacturers are embedding vibration, temperature, pressure, and flow sensors directly into pump housings, enabling continuous condition monitoring and real-time performance analytics.

This shift toward data-driven pumping systems is enabling predictive maintenance strategies that materially alter cost structures for asset-intensive industries. Industrial Internet of Things (IIoT) platforms such as Flowserve’s RedRaven ecosystem have demonstrated maintenance cost reductions of up to 40% while extending asset life by approximately 20%. In one widely cited industrial deployment, early detection of cavitation-induced hydraulic instability allowed operators to avert a catastrophic failure event valued at nearly USD 16 million, underscoring the economic rationale behind sensor-enabled PD pumps.

Adoption momentum is accelerating. By mid-2025, industry assessments indicate that smart, connected PD pumps are moving rapidly from pilot deployments into standard procurement specifications, with connected units in the field expected to rise by roughly 40% by 2027. Artificial intelligence-based diagnostics are now capable of identifying bearing wear, seal degradation, and viscosity deviations well before performance degradation becomes visible at the process level. For operators, this transition from reactive maintenance to condition-based intervention is redefining PD pumps as digital assets rather than mechanical commodities, strengthening long-term service contracts and aftermarket revenue streams for OEMs.

Material Science Innovations for Ultra-Pure and Highly Corrosive Media

Parallel to digitalization, materials innovation is emerging as a core competitive axis in the PD pumps market. The rapid expansion of semiconductor fabrication, lithium-ion battery chemical processing, and high-purity pharmaceutical manufacturing is driving demand for pumps capable of handling aggressive, high-purity fluids without metallic ion contamination. Traditional stainless steel designs are increasingly inadequate in these environments, particularly where hydrofluoric acid, ultra-pure water, or abrasive chemical slurries are involved.

In early 2025, PSG, a Dover Company, launched the Malema M-2300 series targeting semiconductor chemical mechanical planarization applications, utilizing high-purity fluoropolymers and ceramic components to ensure contamination-free operation at advanced 2 nm and 3 nm chip nodes. These designs reflect a broader market trend toward straight-tube flow paths, minimized dead zones, and inert wetted materials that comply with the ultra-stringent purity requirements of next-generation fabs.

The same material-driven trend is evident in hygienic and sanitary pumping. In June 2025, Dover Corporation strengthened its position in hygienic PD pumps through the acquisition of ipp Pump Products GmbH, expanding its portfolio of rotary lobe and progressive cavity pumps for food, beverage, and pharmaceutical applications. Clean-label food production and biologics manufacturing increasingly demand pumps that combine gentle handling, corrosion resistance, and full regulatory compliance, elevating material selection from a design consideration to a primary purchasing criterion.

Powering the Green Hydrogen and Carbon Capture Value Chain

Decarbonization initiatives are creating one of the most structurally significant growth opportunities for the Positive Displacement pumps market in decades. Green hydrogen production, transport, and refueling rely heavily on high-pressure reciprocating and diaphragm pumps capable of handling hydrogen and associated process fluids with absolute sealing integrity. According to the International Energy Agency, global electrolyzer capacity must reach approximately 560 GW to align with climate targets, translating into substantial demand for PD pumps across compression, storage, and dispensing stages.

National programs are reinforcing this trajectory. India’s National Green Hydrogen Mission, backed by an outlay of ₹19,744 crore, targets annual production of 5 million metric tons by 2030. This scale of deployment requires robust, low-leakage PD pumps for electrolyzers, hydrogen compression stations, and downstream chemical synthesis units, positioning pump manufacturers at the center of hydrogen infrastructure build-outs.

Carbon capture, utilization, and storage (CCUS) presents a parallel opportunity. In June 2025, Sulzer published technical guidance outlining optimized pump-around systems for amine-based carbon capture units, where PD pumps must operate reliably at temperatures approaching 240°C while maintaining low pressure drops. As CCUS projects move from demonstration to commercial scale, demand is shifting toward highly specialized PD pumps designed for solvent stability, energy efficiency, and continuous operation in harsh chemical environments.

Scaling Biopharmaceutical Manufacturing Through Single-Use Pump Integration

The biopharmaceutical sector’s rapid shift toward Single-Use Technologies (SUT) is reshaping fluid handling requirements and creating a premium niche for PD pump manufacturers. Single-use pump heads and tubing assemblies eliminate the need for Clean-in-Place and Steam-in-Place validation, significantly reducing downtime and contamination risk in multiproduct biologics facilities.

At the 2025 ISPE Annual Meeting, Watson-Marlow Fluid Technology Solutions showcased its WMArchitect single-use assemblies, highlighting dosing accuracies of ±0.5% for shear-sensitive biologics. Such precision is critical in fill-finish operations for vaccines, monoclonal antibodies, and gene therapies, where even minor dosing errors can result in substantial product losses.

Integration capabilities are becoming a differentiator. Modern PD pumps are increasingly equipped with digital communication protocols that allow seamless interaction with single-use bioreactors, mixers, and downstream processing equipment. Plug-and-play integration reduces commissioning time, simplifies regulatory compliance, and accelerates time-to-market for new therapies. As global biopharma capacity continues to expand, particularly in Asia-Pacific and North America, single-use compatible PD pumps are transitioning from niche solutions to core components of next-generation drug manufacturing infrastructure.

Positive Displacement Pumps Market Share and Segmentation Insights

Rotary Pumps Lead Industrial Fluid Handling Applications with Continuous Flow Performance

Rotary pumps accounted for 58.60% of the Positive Displacement Pumps Market by pump type in 2025, reflecting their widespread use across industrial fluid transfer applications requiring continuous, pulsation-free flow. Gear pumps, lobe pumps, screw pumps, vane pumps, and progressive cavity pumps are widely used to handle viscous fluids, chemicals, oils, slurries, and food ingredients across multiple industries. Their ability to maintain consistent flow rates and operate efficiently with high-viscosity materials supports their adoption in chemical processing, oil and gas operations, and wastewater treatment systems. In 2025, hygienic rotary pump designs are gaining prominence in regulated industries, with manufacturers developing CIP-compatible pumps with polished surfaces and sanitary construction to meet stringent 3-A and EHEDG standards for food and pharmaceutical processing environments.

Chemical Processing Industry Drives Positive Displacement Pump Demand for Precise Fluid Control

Chemical processing accounted for 24.80% of the Positive Displacement Pumps Market by end-use industry in 2025, supported by the need for reliable pumping solutions capable of handling corrosive, viscous, shear-sensitive, and hazardous fluids used in chemical manufacturing operations. Positive displacement pumps provide precise metering, controlled fluid transfer, and stable flow characteristics required in chemical reactors, blending systems, and transfer operations. The scale and diversity of global chemical production continue to sustain strong demand for high-performance pump technologies. In 2025, growing adoption of sealless positive displacement pumps is reshaping equipment selection, with magnetically coupled gear pumps and diaphragm pumps eliminating shaft seal leakage and reducing fugitive emissions in applications involving toxic or volatile chemical fluids.

Positive Displacement Pumps Market Competitive Landscape

The global positive displacement pumps market in 2026 is defined by high-viscosity fluid handling, IoT-enabled monitoring, and PFAS-compliant systems. Demand is accelerating across semiconductor, hydrogen, and pharmaceutical sectors, while Water-as-a-Service (WaaS) models and lifecycle optimization strategies reshape competitive dynamics.

Flowserve Strengthens Nuclear and Energy Transition Portfolio with Strategic Valve Acquisition

Flowserve is reinforcing its position in the positive displacement pumps market through strategic expansion into mission-critical flow control systems. The $490 million acquisition of Trillium Flow Technologies’ valve division enhances its high-pressure PD pump and valve integration capabilities for nuclear and conventional power sectors. Its 2025 Cash Improvement Plan strengthened liquidity, enabling margin-accretive investments expected to deliver operating income growth by late 2026. Flowserve’s Business System (FBS) is central to driving EBITDA margin expansion into the low twenties via lean manufacturing and digital service integration. The company remains a global leader in nuclear safety pumps and high-pressure fluid handling systems essential for energy transition infrastructure. Its turnkey solutions, combining pumps, valves, and automation, position it strongly in EV cooling and hydrogen applications.

IDEX Expands High-Margin Niche Leadership with Precision Metering and Harsh Fluid Handling Solutions

IDEX Corporation continues to dominate high-specification PD pump segments through its decentralized "premier compounder" model. The company reported record 2025 sales of $3.5 billion, supported by strong demand for precision metering pumps and industrial fluid handling systems. Its Fluid & Metering Technologies segment recorded $979 million in Q4 orders, reflecting growth in sanitary, chemical, and abrasive applications. IDEX achieved a 103% free cash flow conversion rate, generating $617 million to fund acquisitions and shareholder returns. Through brands like Viking Pump and Abel Pumps, it specializes in diaphragm and piston pumps for harsh environments, including mining and marine sectors. The company is also advancing microfluidic and syringe pump technologies to support personalized medicine and DNA sequencing applications.

Ingersoll Rand Accelerates Precision Dosing and Localized Manufacturing for Semiconductor and Pharma Growth

Ingersoll Rand is scaling its presence in the positive displacement pumps industry through its Precision and Science Technologies (PST) segment. The company reported 19% year-on-year revenue growth in India, driven by demand for oil-free compressors and high-precision PD pumps in semiconductors and renewable energy. Its new Sanand manufacturing facility enhances localized production of reciprocating pumps and engineered gas compressors, targeting over 90% localization by 2026. With 76 acquisitions completed over six years, Ingersoll Rand continues to pursue inorganic growth to optimize margins toward a 25%+ EBITDA target. The PST segment is a leader in precision dosing pumps for pharmaceutical manufacturing, where zero leakage and process accuracy are critical. Its portfolio supports high-purity fluid transfer systems required in advanced industrial and healthcare applications.

Xylem Transforms into Digital Water Leader with AI-Driven Pumping and PFAS Remediation Solutions

Xylem is redefining the positive displacement pump market through digitalization and water infrastructure modernization. The company achieved $9.0 billion in 2025 revenue, supported by the successful integration of Evoqua and expanded EBITDA margins of 22.2%. Its Xylem Vue platform leverages AI for predictive maintenance and energy optimization in pumping systems, while the MitiGATOR™ system addresses PFAS contamination challenges. Strategic manufacturing expansions in India and Vietnam enhance supply chain resilience and support growth in industrial sectors. Xylem is actively transitioning toward Water-as-a-Service (WaaS) models, generating recurring revenue streams in North America and the Middle East. Its digital-first strategy positions it as a leader in smart water management and energy-efficient PD pumping systems.

Sulzer Enhances Water and Energy Efficiency with High-Performance Pumping Systems and Global Project Wins

Sulzer is achieving record profitability by focusing on energy-efficient pumping technologies and integrated water treatment solutions. The company reported CHF 556 million EBITDA with a 15.6% margin, driven by strong demand in water and renewable energy sectors. Its Flow Division achieved double-digit order growth, supported by large-scale projects such as the Inpasa ethanol facility in Brazil. The launch of its Water Treatment Center of Excellence consolidates key brands to deliver lifecycle-optimized solutions for municipal and industrial clients. Sulzer’s R&D focuses on reducing global energy consumption from pumping systems, including innovations in progressing cavity pumps and smart controllers like BlueLinQ Pro. Its strategy emphasizes efficiency, digital monitoring, and sustainable infrastructure development.

Grundfos Leads Intelligent and Energy-Efficient Pumping with Digital Platforms and Net-Zero Manufacturing

Grundfos is setting the benchmark for sustainable and intelligent pumping solutions in the global PD pumps market. The company reported €4.7 billion in 2025 sales, driven by demand for energy-efficient and digitally enabled pump systems. Its ALPHA GO circulator pump introduces real-time optimization and automated commissioning, enhancing efficiency in HVAC and industrial cooling applications. Grundfos Connect, showcased at IFAT 2026, enables cloud-based monitoring and predictive maintenance for utilities. The company’s LEED Zero Water-certified Chennai facility highlights its leadership in circular water management and sustainable manufacturing. Grundfos is leveraging its Net Zero strategy to commercialize advanced water-saving technologies and intelligent dosing systems globally.

United States: Infrastructure-Led Demand and Technology-Driven Consolidation

The United States positive displacement pumps industry in 2025 is being reshaped by federal infrastructure funding, municipal modernization, and consolidation among leading pump manufacturers. Under the Bipartisan Infrastructure Law, the Environmental Protection Agency has released targeted grant funding for public drinking water resilience, accelerating procurement of high-precision positive displacement pumps for water reuse, desalination, and advanced treatment applications. These projects are favoring pumps capable of accurate metering, chemical resistance, and consistent performance under variable flow conditions. At the manufacturing level, Grundfos announced plans in August 2025 for a new manufacturing facility in Texas, designed to localize production of smart water solutions and support long-term revenue expansion in the U.S. market.

Municipal and industrial upgrades are reinforcing this momentum. Pennsylvania American Water’s investment in upgrading the Kane Borough wastewater treatment plant in October 2025 integrated advanced sludge-handling positive displacement pumps to improve operational reliability and solids management. Strategic consolidation is also redefining competitive dynamics. In December 2025, ITT Inc. entered a definitive agreement to acquire SPX FLOW, significantly strengthening its North American portfolio in twin-screw, sanitary, and process-critical pump technologies. Innovation remains a differentiator, as Flowserve’s INNOMAG TB-MAG Dual Drive sealless magnetic-drive pump received the 2025 Vaaler Award, underscoring rising demand for leak-free, safety-critical pump solutions. Public utilities continue to be a growth anchor, with Xylem reporting record revenues in 2025, largely driven by increased adoption of intelligent pumping systems across U.S. municipalities.

India: Regulatory Enforcement and Localized Manufacturing Expansion

India has emerged as one of the most dynamic markets for positive displacement pumps, driven by regulatory enforcement in water reuse, industrial expansion, and domestic manufacturing under Make in India initiatives. Government mandates introduced in mid-2025 now require large industrial water users to significantly increase wastewater recycling over the coming decade. This policy shift is accelerating adoption of precision metering, dosing, and high-viscosity sludge-handling positive displacement pumps across chemicals, textiles, and mining. Domestic manufacturers are responding with localized product development. In May 2025, Roto Pumps launched its P-Range of positive displacement pumps, engineered specifically for high-viscosity and abrasive media in mining and wastewater applications.

Industrial corridor development is also influencing pump specifications. Under Make in India 2.0, food and beverage processing investments are driving demand for 3A- and EHEDG-certified hygienic rotary lobe pumps, reflecting stricter hygiene and export compliance requirements. Agriculture remains a parallel demand driver. Deployment of solar-powered water pumps has accelerated sharply, with India serving as a primary installation hub, including positive displacement variants for deep-well and off-grid irrigation applications. Together, regulatory pressure, localized manufacturing, and renewable integration position India as a structurally high-growth market for positive displacement pump suppliers.

Saudi Arabia: Desalination Scale-Up and Reliability-Critical Applications

Saudi Arabia’s positive displacement pumps market is closely aligned with Vision 2030 infrastructure development, water security, and oil and gas reliability requirements. At Engineering Day 2025, Grundfos unveiled its next-generation TPE3 intelligent pump series, directly targeting the Kingdom’s expanding HVAC, district cooling, and sustainable building projects. Water infrastructure remains a central driver. Large-scale investments linked to NEOM and Red Sea Global developments are triggering demand for high-pressure positive displacement pumps capable of precise chemical dosing and corrosion resistance in desalination environments.

In the energy sector, reliability and predictive maintenance are shaping pump selection. Saudi Aramco’s 2025 operational updates emphasize the integration of IoT-enabled diaphragm pumps across remote oilfield operations, with the objective of reducing unplanned downtime and improving asset availability. These requirements favor digitally connected positive displacement pumps designed for harsh operating conditions. Saudi Arabia’s market profile is therefore defined by mission-critical applications where uptime, dosing accuracy, and remote monitoring capabilities are decisive.

China: Industrial Policy Support and Export Market Reorientation

China’s positive displacement pumps industry in 2025 is shaped by industrial policy support, environmental enforcement, and export diversification. The Ministry of Industry and Information Technology’s 2025–2026 work plan explicitly prioritizes the development of high-end machinery, encouraging domestic production of chemical-resistant and metallocene-compatible positive displacement pumps for advanced industrial processes. Environmental regulation is a major catalyst. National Zero Liquid Discharge mandates in the textile and chemical sectors have driven a surge in installations of high-head reciprocating pumps for brine concentration and effluent recovery during 2025.

On the export front, Chinese manufacturers are adapting to global trade headwinds by pivoting toward ASEAN and European markets. This strategy focuses on competitively priced yet high-efficiency gear and lobe pumps tailored for machinery, metals processing, and general industrial use. As a result, China’s market is increasingly bifurcated between domestic demand for regulation-compliant, high-performance pumps and export-oriented production emphasizing cost efficiency and rapid customization.

Germany: Energy Efficiency Leadership and High-Specification Applications

Germany remains a technology reference market for positive displacement pumps, driven by energy efficiency mandates, pharmaceutical-grade precision, and export resilience. The European Commission’s Energy+ Pumps initiative, strongly supported by German manufacturers such as Wilo and Allweiler, is accelerating adoption of high-efficiency circulators in domestic and industrial heating systems. These programs are pushing the market toward digitally controlled, low-energy pump solutions with extended lifecycle performance.

Precision applications are gaining prominence. German pump producers expanded production capacity in mid-2025 for hygienic diaphragm pumps serving pharmaceutical, biotech, and nutrition markets, a trend reinforced by consolidation in the global pump sector following the ITT and SPX FLOW transaction. Despite domestic economic headwinds, German manufacturers reported resilient export demand in 2025 from the Middle East and Southern Europe for high-pressure industrial process pumps. Germany’s market profile is therefore defined by efficiency-driven innovation, stringent quality standards, and sustained export competitiveness.

Comparative Overview of Country-Level Dynamics in the Positive Displacement Pumps Industry

Positive Displacement Pumps Market County Level Snapshot

|

Country

|

Core 2025 Focus Areas

|

Implications for Positive Displacement Pumps

|

|

United States

|

Infrastructure funding, municipal upgrades, M&A consolidation

|

Strong demand for smart, leak-free, and sanitary PD pumps

|

|

India

|

Water reuse mandates, Make in India manufacturing, solar pumping

|

Rapid adoption of high-viscosity and hygienic PD pump systems

|

|

Saudi Arabia

|

Desalination projects, oil and gas reliability, smart buildings

|

Growth in high-pressure and IoT-enabled PD pumps

|

|

China

|

Industrial policy support, ZLD enforcement, export diversification

|

Rising demand for chemical-resistant and high-head PD pumps

|

|

Germany

|

Energy efficiency programs, pharma-grade precision, exports

|

Leadership in efficient, high-specification PD pump technologies

|

Positive Displacement Pumps Market Report Scope

Positive Displacement Pumps Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$20.1 Billion

|

|

Market Size (2034)

|

$31.2 Billion

|

|

Market Growth Rate

|

5%

|

|

Segments

|

By Pump Type (Reciprocating Pumps, Rotary Pumps), By Pressure Range (Low Pressure, Medium Pressure, High Pressure), By Drive Type (Electric Driven, Engine Driven, Pneumatic Driven, Hydraulic Driven), By End-Use Industry (Oil & Gas, Water & Wastewater, Chemical Processing, Food & Beverage, Pharmaceutical & Biotechnology, Pulp & Paper, Mining & Slurry Handling)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Flowserve Corporation, Grundfos Holding AS, Xylem Inc., ITT Inc., IDEX Corporation, SPX FLOW Inc., Sulzer Ltd., KSB SE & Co. KGaA, Wilo SE, Ingersoll Rand Inc., Alfa Laval AB, Nikkiso Co. Ltd., Verder International BV, Weir Group PLC, Roto Pumps Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Positive Displacement Pumps Market Segmentation

By Pump Type

- Reciprocating Pumps

- Rotary Pumps

By Pressure Range

- Low Pressure

- Medium Pressure

- High Pressure

By Drive Type

- Electric Driven

- Engine Driven

- Pneumatic Driven

- Hydraulic Driven

By End-Use Industry

- Oil & Gas

- Water & Wastewater

- Chemical Processing

- Food & Beverage

- Pharmaceutical & Biotechnology

- Pulp & Paper

- Mining & Slurry Handling

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Positive Displacement Pumps Industry

- Flowserve Corporation

- Grundfos Holding AS

- Xylem Inc.

- ITT Inc.

- IDEX Corporation

- SPX FLOW Inc.

- Sulzer Ltd.

- KSB SE & Co. KGaA

- Wilo SE

- Ingersoll Rand Inc.

- Alfa Laval AB

- Nikkiso Co. Ltd.

- Verder International BV

- Weir Group PLC

- Roto Pumps Ltd.

*- List not Exhaustive