Powder Coatings Market Size, Energy-Efficient Technologies, and Industrial Coating Demand

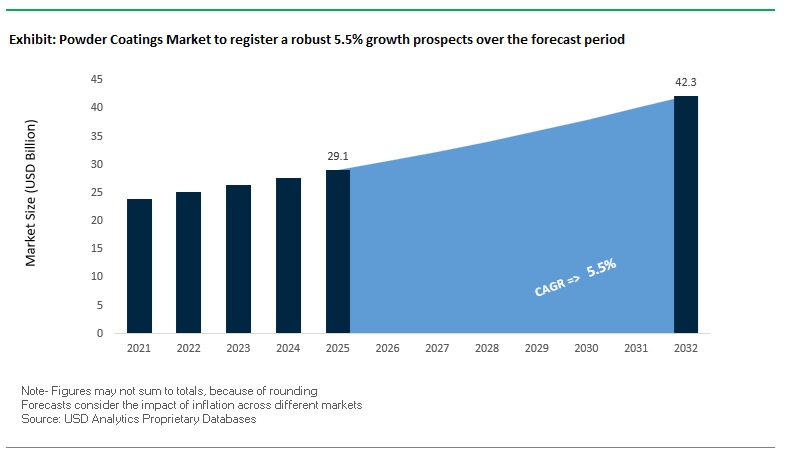

The global Powder Coatings Market was valued at $29.1 billion in 2025 and is projected to grow at a CAGR of 5.5% through 2032, reaching $42.3 billion by 2032. This growth is driven by increasing adoption across automotive, construction, appliances, general industrial, and energy sectors, where powder coatings provide durability, corrosion resistance, and environmental advantages over liquid coatings.

Powder coatings are widely recognized for their solvent-free composition, resulting in near-zero VOC emissions and high material utilization efficiency due to minimal overspray waste. These attributes position powder coatings as a preferred solution in industries facing stringent environmental regulations and decarbonization targets. Additionally, their ability to deliver thick, uniform coatings with superior edge protection and mechanical performance makes them suitable for heavy-duty industrial applications.

A key structural driver is the growing demand for energy-efficient and sustainable manufacturing processes, particularly in sectors such as appliances, EV components, and architectural aluminum. Powder coatings are increasingly being adopted as replacements for multi-layer liquid systems, reducing process complexity and lifecycle emissions.

The market is also benefiting from advancements in low-temperature curing powders, functional coatings, and digital color customization, enabling application on heat-sensitive substrates such as plastics and composites. This is expanding the addressable market into new applications, including electronics and lightweight materials.

Market Analysis: Laser-Based Curing Breakthrough, Regional Capacity Expansion, and Sustainability-Led Innovation

Recent developments in the Powder Coatings Market highlight strong momentum in process innovation, regional manufacturing expansion, and sustainability-focused product development. A major technological breakthrough is PPG’s laser-based powder curing system (February 2026), developed in partnership with IPG Photonics and Whirlpool. This innovation replaces traditional gas-fired ovens with targeted laser energy, significantly reducing energy consumption, floor space requirements, and processing time, while enabling coating of temperature-sensitive substrates.

Regional expansion strategies are strengthening global supply chains. AkzoNobel’s production facility in Gwalior, India, operational since 2024, enhances capacity for South Asia’s infrastructure and consumer electronics markets, reflecting the region’s growing demand for powder coatings.

Market players are also focusing on integrated coating solutions and sustainability certifications. Kansai Helios’ expansion in Italy positions the company as a “system supplier” offering liquid, e-coat, and powder coatings, while its Environmental Product Declaration (EPD)-certified powder coatings address increasing demand for transparent sustainability metrics in architectural and industrial applications.

Strategic initiatives are reinforcing long-term growth. Hempel’s “Accelerate to Win” strategy (January 2026) includes expanding its powder coatings portfolio within energy and infrastructure sectors, while Jotun’s continued revenue growth highlights the resilience of powder coatings amid geopolitical and economic volatility.

Product innovation is targeting both performance and aesthetics. PPG’s Envirocron® Extreme Protection Edge Plus addresses edge coverage challenges in industrial components, enabling powder coatings to replace multi-coat liquid systems. Meanwhile, Axalta’s “Solar Boost” color trend reflects increasing demand for customized, high-impact finishes in automotive and consumer applications.

Digitalization is also enhancing accessibility. TIGER Coatings’ expansion of its WebShop platform enables faster procurement of specialized powders, particularly for small and mid-sized coaters requiring on-demand customization and rapid turnaround times.

Market Trend: Zero-VOC Powder Coatings Replacing PVDF Liquid Systems in Architectural Aluminum Applications

The architectural aluminum coatings market is undergoing a decisive transition from solventborne liquid coatings, particularly PVDF 70% Kynar systems, toward high-performance powder coatings such as super durable polyesters and hyper-durable fluoropolymers. This migration is strongly aligned with evolving sustainability frameworks including LEED v5 carbon neutrality mandates and the tightening energy efficiency standards under California Title 24. Powder coatings provide a near-zero VOC alternative compared to traditional liquid systems that typically contain 350–450 g/L of VOCs, enabling manufacturers to eliminate the need for capital-intensive Regenerative Thermal Oxidizers and significantly reduce compliance costs.

Material efficiency is a critical differentiator driving this transition. Modern powder coating lines equipped with advanced reclaim systems achieve transfer efficiencies of 95–98%, compared to only 35–60% in liquid spray processes where overspray losses and solvent evaporation reduce usable yield. This improvement directly lowers raw material consumption and enhances cost predictability in large-scale façade and extrusion coating operations.

Performance parity with premium liquid fluoropolymers has also been achieved, removing historical barriers to adoption. Hyper-durable powder coatings now consistently meet AAMA 2605 standards, demonstrating over 10 years of South Florida weathering with minimal color change below ΔE 5.0. In addition, these coatings exhibit superior film hardness in the range of 2H to 3H pencil hardness, improving scratch resistance and long-term durability in high-exposure environments. These attributes are positioning powder coatings as a dominant solution in sustainable architectural coatings and high-performance aluminum finishing systems.

Market Trend: Low-Temperature Cure Powder Coatings Unlocking MDF and Wood Substrate Applications

Low-temperature cure powder coatings are expanding the addressable market for powder technology into the commercial furniture coatings and kitchen cabinetry sectors, particularly for Medium-Density Fiberboard and engineered wood substrates. Operating at cure temperatures of 120–130°C, significantly lower than conventional 180–200°C powder curing systems, these formulations enable coating of heat-sensitive substrates without compromising structural integrity or surface quality.

Energy efficiency gains are substantial, with curing oven energy consumption reduced by approximately 30–40%, directly lowering manufacturing operational costs and carbon emissions. This is becoming increasingly relevant as furniture manufacturers integrate sustainability metrics into procurement and production strategies.

From a materials engineering perspective, maintaining lower substrate temperatures prevents outgassing from MDF cores, which is a primary cause of defects such as pinholing and surface pitting. Advanced low-cure powder formulations provide a seamless, 360-degree encapsulation that acts as an effective moisture barrier. This enhances durability and extends the service life of MDF-based products by more than 50% in high-humidity environments such as kitchens and bathrooms, addressing a key limitation of traditional wood coatings.

Production throughput is also significantly improved. Current 2026 benchmarks for UV-curable and low-temperature thermal powder coatings indicate a complete hang-to-box cycle time of under 20 minutes. This represents a major efficiency advantage over multi-stage liquid coating processes that require extended flash-off and drying periods. The combination of speed, durability, and environmental performance is accelerating adoption across high-volume furniture manufacturing and interior wood coatings markets.

Market Opportunity: US EPA NESHAP Revisions Creating Forced Substitution Toward Non-HAP Powder Coatings

The 2026 revisions to the National Emission Standards for Hazardous Air Pollutants under 40 CFR Part 63 Subpart MMMM by the U.S. Environmental Protection Agency are creating a regulatory-driven inflection point for powder coatings adoption in industrial metal finishing. The updated rule introduces a targeted 10–15% reduction in allowable organic HAP emissions for existing coating facilities, accompanied by stringent 12-month rolling compliance requirements that significantly increase monitoring complexity for solvent-based coating systems.

Powder coatings inherently qualify as non-HAP materials under the revised framework, positioning them as a strategically advantageous alternative. Facilities transitioning to powder coatings can utilize the “Compliant Material Option,” which eliminates the need for costly quarterly stack testing and continuous emissions parameter monitoring typically required for liquid coating operations. This reduces both operational expenditure and regulatory risk, particularly for small and mid-sized manufacturers that face resource constraints in maintaining compliance infrastructure.

The regulatory pressure is effectively creating a “forced substitution” window, where continued reliance on high-HAP coatings becomes economically and operationally unsustainable. As a result, powder coatings are expected to capture increased share in sectors such as automotive components, industrial machinery, and general metal fabrication, where compliance costs are a critical decision factor.

Market Opportunity: China VOCs Phase 4 Standards Driving Large-Scale Adoption of Powder Coatings in Industrial Manufacturing

The implementation of the VOCs Phase 4 Action Plan by the Ministry of Ecology and Environment, supported by mandatory standards GB 30981.1-2025 and GB 30981.2-2025, is significantly accelerating the adoption of powder coatings across China’s industrial coatings market. Effective from June 2026, these standards impose stringent limits on VOC emissions and hazardous substances, including formaldehyde and heavy metals, across 62 industrial sectors.

In high-volume manufacturing segments such as metal furniture, appliances, and consumer electronics, compliance with these standards is effectively mandating a transition toward zero-VOC or ultra-low-VOC coating technologies. Powder coatings, due to their solvent-free composition, are emerging as the default compliance pathway. This regulatory push is reinforced by procurement policies under the 15th Five-Year Plan, where state-owned enterprises and public infrastructure projects are required to prioritize environmentally compliant materials.

This has resulted in a projected 25% increase in powder coating specifications across applications such as public transportation systems, telecommunications equipment, and utility housing infrastructure. Additionally, the introduction of hazard classification labeling under the GB standards is enhancing the export competitiveness of powder-coated products. Coatings that achieve the lowest hazard classification simplify compliance with EU and US import regulations, providing manufacturers with improved access to international markets.

Powder Coatings Market Share and Segmentation Insights

By Coating Method: Electrostatic Spray Deposition (ESD) Leads with High Efficiency and Premium Finish Quality

The electrostatic spray deposition (ESD) segment dominated the powder coatings market with a substantial 78.4% share in 2025, driven by its superior finish quality, application efficiency, and scalability in industrial coating processes. ESD technology enables the application of uniform thin films ranging from 50 to 150 microns, delivering excellent smoothness, high gloss, and enhanced edge coverage, making it the preferred method for architectural aluminum coatings, automotive wheels, household appliances, and general metal finishing applications. A key growth driver is its high transfer efficiency, with advanced corona and tribo spray guns achieving 85–95% powder utilization, significantly reducing material waste. Additionally, integrated powder reclaim systems further enhance sustainability and cost-effectiveness compared to traditional methods like fluidized bed coating or flame spraying. This combination of high-performance coating quality, reduced waste, and operational efficiency cements ESD as the industry standard in the global powder coatings market.

By Sales Channel: Direct Sales Channel Dominates with OEM Customization and Technical Support Integration

The direct sales segment accounted for the largest 48.6% share of the powder coatings market in 2025, reflecting the growing need for customized coating solutions and direct technical collaboration with manufacturers. Major OEMs across automotive, appliances, furniture, and industrial equipment sectors increasingly partner directly with powder coating producers to develop proprietary formulations, including custom color matching, gloss levels, surface textures, and optimized curing schedules. This direct engagement enables faster innovation and ensures coatings meet precise performance and aesthetic requirements. Furthermore, manufacturer involvement provides critical technical application support, including optimized spray gun settings, efficient reclaim system management, and precise curing parameters, especially for complex chemistries such as epoxy, polyester, hybrid, urethane, and fluoropolymer powder coatings. By ensuring consistent coating performance, process optimization, and quality assurance, the direct sales channel continues to strengthen its leadership position in the global powder coatings market.

Competitive Landscape of the Powder Coatings Market

AkzoNobel Leads Powder Coatings Market with Laser-Curing Innovation and Sustainable Solutions

AkzoNobel N.V. continues to dominate the powder coatings market through its Interpon® portfolio and strong operational execution. In 2026, the company achieved a 14.2% adjusted EBITDA margin, reflecting high-value product strategies. A major breakthrough is its partnership with IPG Photonics to introduce laser-curing technology, reducing energy consumption by up to 40% compared to conventional curing methods. The company has also expanded its U.S. production capabilities with a €50 million upgrade to its Waukegan facility. Its Interpon D series remains the industry benchmark, with bio-attributed formulations developed in collaboration with BASF and Arkema to reduce carbon footprint.

PPG Expands Market Presence with Digital Ecosystems and EV-Focused Powder Coatings

PPG Industries, Inc. is a key player in the powder coatings market, leveraging its scale and technological expertise. In Q1 2026, the company reported strong financial performance with increased net sales and improved cash flow. PPG has introduced eco-friendly powder coatings with enhanced corrosion resistance, particularly for coastal and high-humidity environments. Its PPG LINQ™ platform integrates AI-driven color matching and cloud-based inventory systems, improving operational efficiency. The company is also targeting the automotive sector, which accounts for over 30% of market demand, by developing dielectric powder coatings for EV battery housings.

Sherwin-Williams Strengthens Market Position with Circular Economy and Supply Chain Resilience

The Sherwin-Williams Company is a major competitor in the powder coatings market, supported by its strong financial performance and global distribution network. The company expanded its North American powder coating production capacity in 2026 to meet rising demand from heavy machinery and agricultural sectors. Its Powdura® ECO series leads in sustainability, incorporating up to 25% recycled PET without compromising durability. Sherwin-Williams has also strengthened supply chain resilience by diversifying resin sourcing and expanding regional production, ensuring stability amid raw material volatility.

Axalta Drives Innovation in Mobility Coatings with UV-Curable Powder Technologies

Axalta Coating Systems is a leading player in the powder coatings market, particularly in automotive and mobility applications. The company achieved record financial performance in 2025, with a 22.0% EBITDA margin. In 2026, Axalta introduced its “Solar Boost” color innovation and expanded its portfolio of UV-curable powder coatings, enabling low-temperature curing for heat-sensitive substrates such as furniture and plastics. Its designation as a global supplier for BMW reinforces its leadership in automotive coatings. Axalta’s focus on advanced powder technologies strengthens its position in high-performance and energy-efficient coatings.

Jotun Expands Global Leadership with Advanced Barrier and Smart Powder Coatings

Jotun Group is a dominant player in the powder coatings market, particularly in energy and infrastructure applications. The company achieved record revenues exceeding NOK 34 billion, supported by strong growth in marine and protective coatings. Its latest innovations include Advanced Barrier Technologies, offering a 30% improvement in abrasion resistance for pipelines and offshore assets. Jotun is also developing smart powder coatings with embedded sensors for early failure detection in industrial infrastructure. Its expansion in the Middle East and Asia-Pacific strengthens its leadership in high-growth regions.

BASF Strengthens Industry Backbone with Advanced Resins and Sustainable Powder Solutions

BASF SE plays a critical role in the powder coatings market as a supplier of advanced resins and coating technologies. Its “Driving the Proxy” color trends highlight innovations in multi-color and liquid-metal-like finishes. BASF’s integration with the Zhanjiang Verbund site ensures stable supply of key raw materials for polyurethane powder coatings. The company is also collaborating with AkzoNobel to develop bio-based raw materials, targeting a 25% reduction in CO₂ emissions per kilogram of powder produced. BASF’s focus on sustainability and advanced materials reinforces its position as a key enabler of next-generation powder coatings.

China Powder Coatings Market: Sustainable Transformation and EV-Driven Growth

China remains the global leader in the powder coatings market, transitioning rapidly toward eco-friendly, high-performance formulations under strong regulatory and policy support. Government initiatives such as the “Blue Sky Defense War” and the 14th Five-Year Plan have accelerated the shift from solvent-based coatings to electrostatic powder coatings (S2P mandate), significantly reducing VOC emissions.

Technological innovation is focused on low-temperature curing powders (120–130°C), enabling coating on heat-sensitive substrates like plastics and MDF. Infrastructure expansion, particularly in ultra-high-voltage (UHV) power grids, is driving demand for dielectric powder coatings. The EV sector is a major growth driver, with increasing use of epoxy-based powder coatings for battery insulation and enclosures. Additionally, advancements such as FEVE-based super-durable powders are enhancing long-term UV resistance in architectural applications, strengthening China’s dominance in sustainable coating technologies.

India Powder Coatings Market: Infrastructure Boom and Manufacturing Localization

India is emerging as a high-growth market in the powder coatings industry, driven by infrastructure development, government incentives, and expanding domestic manufacturing. The PLI scheme for white goods is boosting local production of polyester-epoxy hybrid powder coatings, while the Gati Shakti National Master Plan is increasing demand for powder-coated architectural components across airports and railway stations.

The automotive sector is adopting thin-film powder coatings to reduce vehicle weight and improve efficiency, while agricultural machinery manufacturers are using TGIC-free polyester powders for enhanced corrosion resistance. Investments by major players in new automated manufacturing lines and the adoption of robotic coating booths are improving efficiency and material recovery rates. Regulatory pressure from environmental authorities is also accelerating the transition from liquid coatings to powder systems, reinforcing India’s growth trajectory.

United States Powder Coatings Market: Regulatory Innovation and EV Ecosystem Expansion

The U.S. powder coatings market is defined by strict environmental regulations and rapid growth in electric vehicles and infrastructure. The implementation of PFAS restrictions (2025–2026) is driving the development of PFAS-free powder coatings, ensuring compliance with evolving standards.

The EV sector is a key driver, with innovations in dielectric epoxy powders for high-voltage battery components and thermal management systems. Infrastructure investments under the Bipartisan Infrastructure Law are boosting demand for fusion-bonded epoxy (FBE) coatings for pipelines and rebar protection. Technological advancements such as UV-curable powder coatings are enabling faster production cycles, particularly in the furniture sector. Additionally, the use of recycled resins in powder formulations is supporting sustainability goals and ESG commitments.

Germany Powder Coatings Market: Precision Engineering and Digitalization Leadership

Germany leads the European powder coatings market through advanced manufacturing, sustainability, and Industry 4.0 integration. The adoption of AI-driven color matching and digital twin technologies is improving coating precision and reducing material waste.

Government initiatives supporting energy-efficient production systems, such as infrared curing ovens, are accelerating the transition to greener manufacturing processes. Innovation is also focused on bio-based powder resins and antimicrobial coatings for public infrastructure and healthcare applications. The demand for solar-reflective and hyper-durable coatings in smart buildings is increasing, while expansion in metallic and decorative powders is supporting premium automotive and furniture markets. Strict compliance with REACH regulations further reinforces Germany’s leadership in sustainable coating technologies.

Vietnam Powder Coatings Market: Emerging Manufacturing Hub

Vietnam is rapidly emerging as a key player in the powder coatings market, driven by the relocation of global manufacturing operations and strong export growth. The influx of electronics manufacturers is increasing demand for ESD powder coatings, while infrastructure development is boosting the use of C5-M rated coatings for coastal applications.

The country’s furniture export boom is driving demand for high-weatherability polyester powders, while investments in new production facilities are strengthening supply chains. Government incentives promoting clean production technologies are accelerating the adoption of powder coatings over traditional solvent-based systems. Additionally, growth in bicycle and e-bike manufacturing is creating new opportunities for powder coating applications.

Turkey Powder Coatings Market: Strategic Export Hub for EMEA

Turkey has positioned itself as a major powder coatings manufacturing and export hub, leveraging its strategic location and alignment with European standards. The country is expanding production of Qualicoat-certified architectural powders, catering to European and Middle Eastern markets.

Technological advancements include the development of bonded metallic powders that improve aesthetic performance and recyclability. The automotive sector is driving demand for powder coatings, particularly for EV components and assembly plants in the Marmara region. Additionally, innovations in textured and soft-touch finishes are enhancing product differentiation in the appliance sector. Government support for R&D in nanotechnology-based coatings is further strengthening Turkey’s competitive position.

Brazil Powder Coatings Market: Agribusiness and Heavy Equipment Demand

Brazil’s powder coatings market is closely tied to its leadership in agriculture, mining, and heavy equipment manufacturing. Demand is driven by the need for high-gloss, UV-stable coatings for agricultural machinery and industrial equipment.

Government initiatives such as the Nova Indústria Brasil plan are supporting investments in energy-efficient coating technologies. The expansion of production capacity in regions like Santa Catarina is strengthening supply for motors and transformers, while advancements in thermoplastic powder coatings are supporting subsea oil and gas applications. Environmental regulations are encouraging the transition from anodizing to powder coatings in architecture, while innovations such as anti-graffiti coatings are gaining traction in urban infrastructure projects.

Powder Coatings Market Report Scope

Powder Coatings Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$29.1 Billion

|

|

Market Size (2032)

|

$42.3 Billion

|

|

Market Growth Rate

|

5.5%

|

|

Segments

|

By Resin Type (Thermoset Powder Coatings, Thermoplastic Powder Coatings, UV-Curable Powder Coatings), By Coating Method (Electrostatic Spray Deposition, Fluidized Bed Coating, Electrostatic Fluidized Bed Process, Flame Spraying), By Substrate Material (Metallic Substrates, Non-Metallic Substrates), By End-Use Industry (Automotive and Transportation, Consumer Appliances, Building and Construction, Furniture, Agriculture, Construction, and Earthmoving, General Industrial, Oil and Gas), By Curing Technology (Thermal Curing, Low-Temperature Curing, Radiation Curing), By Functional Property (Anti-Corrosive, High-Durability, Anti-Microbial, Decorative), By Sales Channel (Direct Sales, Specialty Coating Distributors, Custom Coating Job Shops)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Akzo Nobel N.V., PPG Industries, Inc., The Sherwin-Williams Company, Axalta Coating Systems Ltd., Jotun A/S, Nippon Paint Holdings Co., Ltd., Kansai Paint Co., Ltd., TIGER Coatings GmbH and Co. KG, Asian Paints Limited, RPM International Inc., Hempel A/S, Berger Paints India Limited, Teknos Group, IFS Coatings, Protech Group

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Powder Coatings Market Segmentation

By Resin Type

- Thermoset Powder Coatings

- Polyester

- Epoxy-Polyester Hybrids

- Pure Epoxy

- Polyurethane

- Acrylic

- Thermoplastic Powder Coatings

- Polyvinyl Chloride

- Nylon

- Polyolefins

- Polyvinylidene Fluoride

- UV-Curable Powder Coatings

By Coating Method

- Electrostatic Spray Deposition

- Fluidized Bed Coating

- Electrostatic Fluidized Bed Process

- Flame Spraying

By Substrate Material

- Metallic Substrates

- Non-Metallic Substrates

By End-Use Industry

- Automotive and Transportation

- Consumer Appliances

- Building and Construction

- Furniture

- Agriculture, Construction, and Earthmoving

- General Industrial

- Oil and Gas

By Curing Technology

- Thermal Curing

- Low-Temperature Curing

- Radiation Curing

By Functional Property

- Anti-Corrosive

- High-Durability

- Anti-Microbial

- Decorative

By Sales Channel

- Direct Sales

- Specialty Coating Distributors

- Custom Coating Job Shops

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Powder Coatings Industry

- Akzo Nobel N.V.

- PPG Industries, Inc.

- The Sherwin-Williams Company

- Axalta Coating Systems Ltd.

- Jotun A/S

- Nippon Paint Holdings Co., Ltd.

- Kansai Paint Co., Ltd.

- Tiger Coatings GmbH & Co. KG

- Asian Paints Limited

- RPM International Inc.

- Hempel A/S

- Berger Paints India Limited

- Teknos Group

- IFS Coatings

- Protech Group

*- List not Exhaustive