Pre-Painted Metal Market Size, Coil Coating Demand, and Infrastructure-Led Growth

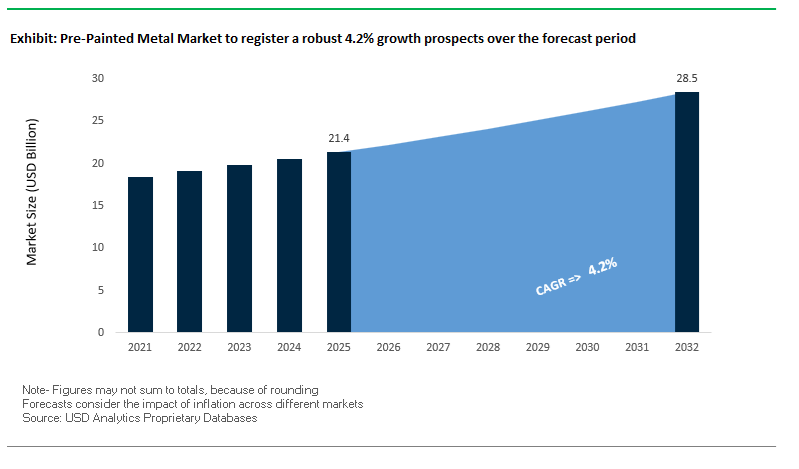

The global Pre-Painted Metal Market was valued at $21.4 billion in 2025 and is projected to grow at a CAGR of 4.2% through 2032, reaching $28.5 billion by 2032. Growth is primarily driven by expanding demand in construction, appliances, transportation, and industrial applications, where pre-painted (coil-coated) metals offer enhanced durability, corrosion resistance, and aesthetic consistency.

Pre-painted metal, typically steel or aluminum coated through continuous coil processes, provides factory-controlled coating quality, ensuring uniform thickness, adhesion, and finish compared to post-fabrication painting. This makes it highly suitable for roofing, wall cladding, HVAC systems, white goods, and automotive components, particularly in environments requiring long-term weather resistance and reduced maintenance.

A key structural driver is the growth of urban infrastructure and residential construction, especially in emerging economies such as India and Southeast Asia. Pre-painted metal is increasingly preferred due to its fast installation, lifecycle cost efficiency, and compatibility with modern modular construction techniques. Additionally, demand for energy-efficient building materials, such as cool roof systems, is further accelerating adoption.

Sustainability and process efficiency are also shaping the market. Coil coating is inherently more efficient than traditional painting methods, with lower waste, controlled emissions, and higher material utilization rates. Innovations in low-temperature curing, bio-based coatings, and advanced pigment technologies are further aligning the market with global decarbonization goals.

Market Analysis: Capacity Expansion, Laser-Based Coil Innovation, and Sustainable Material Integration Driving Market Evolution

Recent developments in the Pre-Painted Metal Market highlight a strong convergence of capacity expansion, process innovation, and sustainability-driven transformation. A major growth initiative is ArcelorMittal Nippon Steel India’s expansion of color-coated steel capacity to 1.0 million tonnes (ramp-up through 2026), targeting high-growth applications in residential roofing and industrial cladding across Asia.

Technological innovation is reshaping manufacturing efficiency. PPG’s commercialization of laser-based coil curing technology (January 2026) replaces conventional gas-fired ovens with targeted laser energy, reducing energy consumption by up to 40% and significantly lowering the carbon footprint of pre-painted metal production. This represents a major advancement in energy-efficient coil coating processes.

Product innovation is enhancing performance and durability. Tata Steel’s next-generation galvanized pre-painted steel (November 2025) introduces a magnesium-aluminum-zinc alloy substrate, addressing the long-standing issue of cut-edge corrosion and extending product lifespan in coastal and high-humidity environments.

Regional expansion and product differentiation are also key trends. BlueScope Steel’s investment in COLORBOND® technology (October 2025) integrates infrared-reflective pigments to reduce heat absorption, supporting energy-efficient building designs in tropical climates. Meanwhile, AkzoNobel’s restructuring of its industrial coatings division (February 2026) highlights the continued profitability and strategic importance of its coil coatings business.

Sustainability initiatives are becoming central to competitive positioning. Beckers Group’s transition to 50% bio-attributed and recycled raw materials (March 2026) reflects the industry’s push toward low-carbon value chains, while WEG’s low-temperature curing coatings (February 2026) enable reduced energy consumption and compatibility with advanced substrates.

Standardization efforts are also gaining momentum. Discussions at World Paint and Coatings Week 2026 around VOC reporting standards for coil coating lines signal increasing alignment across industry players to support transparent “green steel” certifications for global construction markets.

Market Trend: High-Build PVDF Powder Coatings Reshaping Sustainable Roofing and Architectural Panel Manufacturing

The pre-painted metal coatings market is undergoing a structural transformation as building and construction stakeholders shift from solventborne PVDF liquid coatings to high-build PVDF powder coatings for roofing systems and architectural wall panels. This transition is closely aligned with LEED v5 decarbonization targets and California Title 24 ultra-low emission standards, positioning powder coatings as a critical enabler of sustainable building envelope solutions.

A key driver is the elimination of volatile organic compound emissions. Conventional 70% PVDF liquid coatings typically contain 350–450 g/L of VOCs, necessitating the use of Regenerative Thermal Oxidizers for emission control. In contrast, PVDF powder coatings operate at near-zero VOC levels, allowing coil coating lines to bypass solvent recovery infrastructure and significantly reduce energy consumption associated with air pollution control systems. This shift improves both environmental compliance and operational cost structures for coil coaters.

Performance advantages are equally compelling. PVDF powder coatings enable a single-pass dry film thickness of 50–100 µm, compared to 20–25 µm for liquid systems. This results in a twofold to fourfold increase in mechanical barrier protection against corrosion, UV exposure, and environmental degradation. Despite the higher film build, these coatings maintain the industry-standard 70% resin-to-pigment ratio, ensuring long-term color retention and durability exceeding 30 years in exterior applications.

Operational efficiency is further enhanced by the inherent material utilization benefits of powder coating technology. Modern coil coating lines achieve transfer efficiencies of 95–98%, with overspray fully recoverable and reusable. This solvent-free, closed-loop process reduces total material waste by 20–30% compared to conventional liquid spray or roll-coating methods, strengthening the economic case for PVDF powder adoption in high-volume pre-painted metal production.

Market Trend: Chrome-Free Pretreatment Technologies Becoming Standard in Appliance-Grade Pre-Painted Metal

The white goods and appliance coatings segment is witnessing widespread adoption of chrome-free pretreatment systems, replacing legacy hexavalent and trivalent chromium-based phosphates with advanced zirconium, silane, and titanium chemistries. This transition is driven by tightening environmental regulations, occupational safety requirements, and the need to eliminate hazardous heavy metals from industrial coating processes.

Zirconium-based conversion coatings are emerging as the preferred alternative due to their ability to deliver zero-heavy-metal surface preparation. Compared to traditional zinc-chrome phosphate systems, these technologies reduce hazardous waste sludge generation by up to 90%, significantly lowering disposal costs and environmental liabilities for manufacturers. This is particularly relevant for large-scale appliance OEMs operating high-throughput coil coating and sheet processing lines.

Performance benchmarks for chrome-free pretreatments have reached parity with legacy systems. Hybrid silane-zirconium coatings demonstrate corrosion resistance exceeding 1,000 hours in Neutral Salt Spray testing under ASTM B117 conditions on both cold-rolled steel and galvanized substrates. This ensures long-term adhesion and coating integrity, meeting the durability requirements of refrigerators, HVAC systems, and laundry appliances.

From a process optimization standpoint, chrome-free pretreatments operate effectively at ambient temperatures in the 20–30°C range. This eliminates the need for heated treatment stages required in conventional phosphate lines, which typically operate at 50–70°C. As a result, manufacturers achieve a 15–20% reduction in pretreatment line energy consumption, contributing to broader decarbonization and cost-efficiency objectives within the pre-painted metal industry.

Market Opportunity: US EPA NESHAP Subpart SSSS Driving Mandatory Transition to Low-HAP Coil Coating Technologies

The 2026 revisions to the National Emission Standards for Hazardous Air Pollutants under Subpart SSSS, implemented by the U.S. Environmental Protection Agency, are creating a regulatory inflection point for the pre-painted metal and coil coating industry. The updated framework introduces stricter emission caps for hazardous air pollutants, effectively mandating a transition toward low-HAP and zero-VOC coating technologies for major source facilities.

A critical regulatory change is the removal of the Startup, Shutdown, and Malfunction exemptions, which previously allowed temporary deviations from emission limits. With continuous compliance now required, manufacturers using solventborne coatings face heightened operational risk and compliance costs. This is accelerating the adoption of powder coatings and high-solids liquid systems that inherently generate lower emissions and simplify regulatory adherence.

The revised regulation also places increased scrutiny on chromium-based pretreatment processes. Enhanced reporting requirements for chromium emissions in spray zones are effectively disincentivizing the continued use of hexavalent and trivalent chromium systems. As a result, chrome-free pretreatment technologies are rapidly becoming the regulatory benchmark for US-based coil coaters, creating a clear pathway for investment in zirconium and silane-based systems.

These regulatory dynamics are expected to drive capital expenditure in next-generation coil coating lines, including powder coating integration and advanced pretreatment upgrades, positioning compliant manufacturers to gain competitive advantage in a tightening environmental policy landscape.

Market Opportunity: China VOCs Phase 4 and GB 30981-2025 Standards Accelerating Global Adoption of Zero-VOC Pre-Painted Metal

The implementation of the VOCs Phase 4 Action Plan by the Ministry of Ecology and Environment, supported by mandatory standards GB 30981.1-2025 and GB 30981.2-2025, is reshaping the global pre-painted metal supply chain. Effective from June 2026, these standards impose the most stringent limits to date on VOC emissions, formaldehyde content, and heavy metals in industrial coatings.

For the coil coating sector, compliance with these standards effectively restricts the use of conventional solventborne systems, positioning powder coatings and waterborne technologies as the primary pathways to achieving “Green Product” certification. This is particularly impactful in high-volume applications such as construction panels, appliances, and infrastructure materials, where regulatory compliance is directly linked to market access.

Under China’s 15th Five-Year Plan, state-owned enterprises and public infrastructure projects are mandated to prioritize chrome-free and low-VOC pre-painted metal solutions. This policy direction is targeting a 60% domestic adoption rate of clean coating technologies by 2030, creating a substantial demand pipeline for environmentally compliant coated steel products.

In addition, the 2026 GB standards are strategically aligned with international regulatory frameworks such as the EU Carbon Border Adjustment Mechanism. By ensuring that Chinese exports meet zero-VOC and chrome-free thresholds, manufacturers can maintain competitiveness in European and North American markets. This alignment is fostering a globally harmonized shift toward sustainable pre-painted metal coatings, while opening export-driven growth opportunities for producers that invest early in compliant technologies.

Pre-Painted Metal Market Share and Segmentation Insights

By Number of Coating Layers: Double-Coat Systems Lead with Optimal Performance-Cost Balance

The double-coat system segment dominated the pre-painted metal market with a 52.5% share in 2025, driven by its ideal balance between corrosion protection, UV durability, and cost efficiency. Typically consisting of an epoxy primer combined with a polyester topcoat, this system has become the industry standard for building cladding, roofing systems, and home appliances, where long-term performance and aesthetic consistency are critical. Double-coat systems deliver excellent color retention, surface uniformity, and resistance to environmental degradation, making them highly suitable for exterior architectural applications. While multi-coat systems (three or more layers) are used in premium projects such as high-rise facades with fluorocarbon coatings, their higher cost limits widespread adoption. Conversely, single-coat systems often lack sufficient durability for outdoor exposure, reinforcing the dominance of double-coat configurations. This strong combination of performance reliability, economic feasibility, and scalability positions double-coat systems as the backbone of the global pre-painted metal market.

By Sales Channel: Direct Sales Channel Dominates with High-Volume Contracts and Specification Control

The direct sales segment accounted for a leading 55.4% share of the pre-painted metal market in 2025, reflecting the importance of large-scale procurement and stringent specification compliance. Major end users, including construction companies and appliance manufacturers, procure pre-painted steel and aluminum coils directly from leading producers such as BlueScope, ArcelorMittal, and Nippon Steel, often in bulk coil or sheet formats. This direct engagement eliminates intermediary costs and ensures consistent quality, timely delivery, and competitive pricing for high-volume production needs. Additionally, architectural projects increasingly require precise coating specifications, including color, gloss levels, durability standards, and warranty compliance, which are typically defined by architects and project consultants. Direct supply relationships enable full traceability, certification, and adherence to building codes and project-specific requirements. As demand grows for high-performance coated metal solutions in construction and manufacturing, the direct sales channel continues to strengthen its dominance in the global pre-painted metal market.

Pre-Painted Metal Market Competitive Landscape Driven by Green Steel, Advanced Coatings, and Regional Manufacturing Expansion

The pre-painted metal market is intensifying as global leaders invest in sustainable coating technologies, carbon-reduced steel substrates, and localized manufacturing. Competition is shaped by innovation in PPGI and pre-painted aluminum, CBAM compliance, and demand from construction, EV, and renewable energy sectors.

ArcelorMittal Strengthens CBAM-Compliant Coated Steel with XCarb® and Granite® Innovations

ArcelorMittal S.A. continues to lead the pre-painted steel market through advanced organic coated steel solutions aligned with European environmental regulations. The company’s 2026 CapEx guidance of $4.5 billion to $5.0 billion underscores its focus on expanding coated steel and electrical steel capacity to support green mobility and infrastructure. Its Granite® HDX and Silky Shine product lines deliver high-durability performance in aggressive environments, while recent innovations emphasize XCarb® carbon-reduced steel substrates for sustainable pre-painted applications. ArcelorMittal’s integration of CBAM-compliant production processes is expected to enhance competitiveness against imports in Europe. The company’s solutions are widely adopted in architectural cladding, industrial roofing, and EV battery housing applications. This strategic positioning reinforces its dominance in high-performance, low-carbon pre-painted metal solutions.

Tata Steel Expands Value-Added Pre-Painted Steel Portfolio with Digital Distribution and Capacity Growth

Tata Steel Limited is rapidly scaling its presence in the pre-painted galvanized steel (PPGI) market across South Asia through capacity expansion and product premiumization. Its ₹15,000 crore CapEx plan for FY2025-2026 includes a 0.7 MTPA HRPGL facility at Tarapur, targeting automotive coated steel demand. The company is strategically shifting toward value-added pre-painted and galvanized products, aiming for a 40 MTPA domestic capacity by 2030. Tata Steel’s digital platform Aashiyana recorded a 60% YoY GMV increase, reflecting strong traction in e-commerce-driven steel distribution for residential construction. Its flagship brands, Tata BlueScope (Colorbond®) and Tata Shaktee, dominate roofing and rural retail segments. This integrated approach of digitalization, capacity expansion, and premium coatings strengthens its leadership in India’s fast-growing construction materials market.

Nippon Steel Accelerates High-Performance Pre-Painted Steel for Energy and Urban Heat Mitigation

Nippon Steel Corporation is advancing its competitive edge in the pre-painted metal market through high-margin “Super-Core” materials and global expansion strategies. The company is focusing on hybrid coating technologies that combine corrosion resistance with aesthetic performance, including visible-light-responsive and heat-reflective coatings for urban heat island mitigation. Its expansion into U.S. and ASEAN markets is supported by specialized Zn-Al-Mg coated pre-painted steel targeting solar energy infrastructure. Recent innovation includes ultra-durable Super-Alloy-Coated Steel engineered for offshore wind applications, offering over 30 years of corrosion resistance. Nippon Steel’s strong integration with automotive and electronics sectors enables tailored solutions for appliances and EV components. This diversification into renewable energy and high-tech applications strengthens its global market positioning.

Baosteel Expands Global Footprint with Integrated Overseas Production and High-Volume PPGI Solutions

Baoshan Iron & Steel Co., Ltd. is leveraging its scale and strategic investments to dominate high-volume pre-painted metal markets across Asia and the Middle East. The company’s $4 billion investment in Saudi Arabia supports its expansion into MENA’s Vision 2030 infrastructure projects, establishing localized production capabilities. Baosteel reported a 40.5% increase in net profit in 2025, driven by domestic demand linked to equipment renewal policies. Its strategy of integrated overseas production enables it to bypass anti-dumping tariffs and strengthen regional supply chains. The company offers specialized PPGI and PPGL products with high-gloss and anti-fingerprint coatings for the home appliance sector. This combination of scale, localization, and product innovation reinforces Baosteel’s leadership in cost-competitive coated steel solutions.

SSAB Leads Fossil-Free Pre-Painted Steel Innovation with GreenCoat® Portfolio Expansion

SSAB is setting global benchmarks in sustainable pre-painted metal through its Fossil-Free™ steel and GreenCoat® product portfolio. The company reported record shipments of premium specialty steels in Q1 2026, driven by growing demand for green construction materials. GreenCoat® coatings utilize bio-based Swedish rapeseed oil, significantly reducing reliance on fossil-based solvents and lowering environmental impact. SSAB is also witnessing increased adoption in renewable energy applications, including solar mounting systems and wind turbine components, due to its lightweight and high-strength properties. Its strategic transition toward Electric Arc Furnaces (EAF) and hydrogen-based DRI production further reduces carbon emissions. This strong sustainability focus positions SSAB as a leader in low-carbon, high-performance pre-painted steel solutions for LEED-certified infrastructure.

China Pre-Painted Metal Market: High-Value Coatings and Infrastructure Expansion

China continues to dominate the global pre-painted metal market, shifting from volume-driven production toward high-value, functional coatings. Under the 2025–2026 Steel Industry Action Plan, the government is phasing out inefficient lines while promoting advanced continuous color coating lines (CCLs) to enhance product quality and efficiency.

Massive infrastructure investments under the “New Infrastructure” initiative are driving demand for pre-painted metals in 5G base stations, data centers, and UHV power grids. Technological advancements include widespread adoption of PVDF fluorocarbon coatings with self-cleaning properties, particularly for transport hubs and airports. China is also expanding capacity in Zhejiang and Shandong for decorative printed metals (wood-grain, stone textures), targeting premium appliances and interiors. Sustainability efforts such as near-zero emission (NZE) coil lines with RTO systems and leadership in solar PV mounting systems using Al-Mg-Zn substrates further reinforce China’s global dominance.

India Pre-Painted Metal Market: Infrastructure Boom and Export Acceleration

India is the fastest-growing market in the pre-painted metal sector, driven by large-scale infrastructure and housing programs. Government initiatives like PMAY and Gati Shakti are fueling demand for pre-painted roofing and cladding materials across residential and logistics projects.

Major investments by Tata Steel and JSW Steel are expanding capacity for thin-gauge pre-painted steel, particularly for white goods manufacturing. Technological innovation includes the adoption of Cool Roof coatings with high solar reflectivity to reduce urban heat. India has also become a net exporter of pre-painted coils, with strong growth in shipments to the Middle East and Southeast Asia. The development of dedicated coil coating clusters and the introduction of antimicrobial coated metals for healthcare and cold storage applications further strengthen India’s position as a high-growth market.

United States Pre-Painted Metal Market: Reshoring and Sustainable Coatings

The U.S. pre-painted metal market is being reshaped by domestic manufacturing incentives and strict environmental regulations. Policies targeting PFAS-free coatings are driving innovation in new resin chemistries for architectural applications.

Infrastructure investments under the IIJA are boosting demand for pre-painted metals in transportation and modular construction. The automotive sector is also a key growth driver, with increased use of ultra-high-strength pre-painted steel in EV battery enclosures. Innovations such as digital print-on-coil technology are enabling highly customized architectural finishes, while sustainability trends are promoting the use of bio-based resins and recycled substrates to meet ESG and LEED requirements.

Germany Pre-Painted Metal Market: Green Steel and Digital Traceability

Germany leads Europe’s pre-painted metal market through its focus on sustainability, advanced materials, and Industry 4.0 integration. The development of hydrogen-based “green steel” substrates is significantly reducing carbon emissions in automotive and construction applications.

Innovations include low-temperature curing coatings that reduce energy consumption, as well as blockchain-based material passports that provide full traceability of coating composition and carbon footprint. Germany is also driving demand for insulated metal panels (IMPs) under EU building efficiency regulations, while applications such as eco-facades and vertical forests are increasing the use of high-end pre-painted materials. Infrastructure upgrades, including railway modernization, are further supporting market growth.

Vietnam Pre-Painted Metal Market: Emerging Manufacturing Alternative

Vietnam is rapidly emerging as a key hub in the pre-painted metal market, benefiting from global supply chain diversification and strong export growth. Investments in coating facilities, such as the Dong Nai plant, are supporting production of ESD pre-painted sheets for electronics manufacturing.

Government incentives promoting clean production are accelerating the shift from post-painting to pre-painted assembly, reducing VOC emissions. The country’s coastal geography is driving innovation in C5-M rated corrosion-resistant coatings, while housing development programs are boosting demand for pre-painted roofing materials. Expansion of local companies like Hoa Sen Group is further strengthening Vietnam’s position in the global supply chain.

Turkey Pre-Painted Metal Market: Strategic Export Bridge for EMEA

Turkey has established itself as a strategic pre-painted metal manufacturing and export hub, serving European and Middle Eastern markets. Government incentives, including VAT exemptions, are supporting modernization of color-coating lines and enhancing production efficiency.

Technological advancements include the adoption of bonded metallic coating technologies for premium automotive and architectural applications. The HVAC sector is a major demand driver, utilizing epoxy-polyester hybrid coatings for outdoor units. Turkey is also investing in vertical integration through continuous galvanizing lines, ensuring high-quality substrates. Growth in sandwich panels for cold chain logistics and alignment with European standards further strengthen Turkey’s global competitiveness.

South Korea Pre-Painted Metal Market: Functional Innovation and Smart Materials

South Korea is a leader in high-tech pre-painted metal solutions, focusing on smart materials and electronics applications. Innovations such as VCM (Vinyl Coated Metal) and PCM (Pre-Coated Metal) are enabling high-definition digital patterns for premium appliances.

The country is also advancing self-healing coatings using micro-capsule technology, improving durability in consumer electronics. Investments in carbon capture-integrated production lines are positioning South Korea as a pioneer in net-zero pre-painted steel manufacturing. Strict low-VOC regulations are driving adoption of waterborne and UV-cured coatings, while specialized products such as anti-fingerprint (AFP) coatings are gaining traction in kitchenware and elevator interiors. Additionally, demand for high-weatherability coatings in offshore wind infrastructure highlights South Korea’s leadership in functional and sustainable pre-painted metal technologies.

Pre-Painted Metal Market Report Scope

Pre-Painted Metal Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$21.4 Billion

|

|

Market Size (2032)

|

$28.5 Billion

|

|

Market Growth Rate

|

4.2%

|

|

Segments

|

By Substrate Metal (Steel, Aluminum, Copper and Other Specialty Metals), By Coating Material (Polyester, Silicon Modified Polyester, Fluoropolymers, Plastisol, Polyurethane, Epoxy, Bio-based), By Number of Coating Layers (Single-Coat System, Double-Coat System, Multi-Coat), By End-Use Industry (Building and Construction, Home Appliances, Automotive and Transportation, Consumer Electronics, Furniture, Energy), By Application (Coil Coating, Sheet Coating), By Functional Property (Aesthetic, Cool Roof, Anti-Bacterial, Anti-Corrosive and Chemical Resistant, Self-Cleaning), By Sales Channel (Direct Sales, Service Centers and Toll Coaters, Specialty Metal Distributors)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Nippon Steel Corporation, ArcelorMittal, BlueScope Steel Limited, Tata Steel Limited, POSCO, JFE Steel Corporation, China Baowu Steel Group Corp., Ltd., SSAB, JSW Steel Limited, Ternium S.A., Novelis Inc., United Arab Can Manufacturing Limited, Nucor Corporation, NLMK Group, SeAH Steel Corporation

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Pre-Painted Metal Market Segmentation

By Substrate Metal

- Steel

- Hot-Dip Galvanized

- Electro-Galvanized

- Galvalume

- Cold-Rolled Steel

- Aluminum

- Copper and Other Specialty Metals

By Coating Material

- Polyester

- Silicon Modified Polyester

- Fluoropolymers

- Plastisol

- Polyurethane

- Epoxy

- Bio-based

By Number of Coating Layers

- Single-Coat System

- Double-Coat System

- Multi-Coat

By End-Use Industry

- Building and Construction

- Home Appliances

- Automotive and Transportation

- Consumer Electronics

- Furniture

- Energy

By Application

- Coil Coating

- Sheet Coating

By Functional Property

- Aesthetic

- Cool Roof

- Anti-Bacterial

- Anti-Corrosive and Chemical Resistant

- Self-Cleaning

By Sales Channel

- Direct Sales

- Service Centers and Toll Coaters

- Specialty Metal Distributors

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Pre Painted Metal Industry

- Nippon Steel Corporation

- ArcelorMittal

- BlueScope Steel Limited

- Tata Steel Limited

- POSCO

- JFE Steel Corporation

- China Baowu Steel Group Corp., Ltd.

- SSAB

- JSW Steel Limited

- Ternium S.A.

- Novelis Inc.

- United Arab Can Manufacturing Limited

- Nucor Corporation

- NLMK Group

- SeAH Steel Corporation

*- List not Exhaustive