Pre-Painted Steel Market Size, Export Momentum, and Sustainable Construction Demand

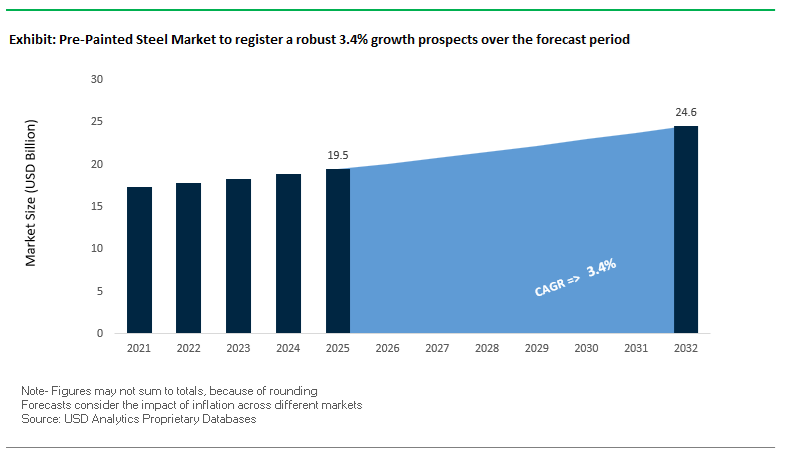

The global Pre-Painted Steel Market was valued at $19.5 billion in 2025 and is projected to grow at a CAGR of 3.4% through 2032, reaching $24.6 billion by 2032. This steady growth reflects rising demand across construction, appliances, automotive, and renewable energy sectors, where pre-painted steel delivers corrosion resistance, aesthetic consistency, and faster installation efficiency.

A major structural driver is the increasing adoption of pre-painted galvanized (PPGI) and pre-painted galvalume steel in modern construction. These materials offer enhanced durability, reduced maintenance, and compatibility with modular building systems, making them particularly attractive in urban infrastructure and residential roofing applications.

Global trade dynamics are also playing a critical role. India’s return as a net exporter of steel in FY 2025–26, with exports rising 35.9% to 6.6 million tonnes, highlights the growing competitiveness of value-added steel products such as pre-painted steel in international markets, particularly across Europe and the Middle East. This trend underscores the shift toward higher-margin, coated steel products in global trade flows.

Sustainability is becoming a defining factor in purchasing decisions. Pre-painted steel is increasingly positioned as a “green construction material”, especially when combined with low-carbon steel substrates, energy-efficient coatings, and reflective pigments that reduce building heat loads. Regulatory frameworks such as the EU’s Carbon Border Adjustment Mechanism (CBAM) are further incentivizing the use of low-emission steel products, reshaping competitive dynamics across regions.

Market Analysis: Capacity Expansion, Laser-Curing Breakthroughs, and Green Steel Policies Reshaping Market Dynamics

Recent developments in the Pre-Painted Steel Market highlight a convergence of capacity expansion, process innovation, and policy-driven transformation. India’s infrastructure-driven growth is supported by Tata Steel’s Kalinganagar expansion (April 2026), which enhances the supply of high-quality substrates for premium pre-painted steel used in automotive and appliance applications.

Technological innovation is significantly improving manufacturing efficiency. The commercialization of laser-cured pre-painted steel by PPG and Whirlpool (January 2026) represents a major advancement, reducing carbon emissions by 40% by eliminating traditional gas-fired ovens. This technology is expected to play a key role in decarbonizing appliance manufacturing supply chains.

Regional capacity expansion is strengthening supply chains. BlueScope Steel’s Western Sydney metal coating line (February 2026) is designed to meet growing demand for COLORBOND® steel, incorporating infrared-reflective pigments that improve thermal performance in urban environments. Additionally, Baosteel’s aggressive export strategy focuses on high-margin pre-painted steel products for global appliance and solar markets.

Policy frameworks are reshaping competitive positioning. ArcelorMittal’s focus on XCarb® low-carbon steel aligns with the EU’s CBAM, which favors domestically produced, lower-emission materials. Similarly, Saudi Arabia’s Vision 2030 mandates for C5-M corrosion-resistant pre-painted steel in mega-projects such as NEOM are driving localized production and partnerships.

Sustainability-led product innovation continues to gain traction. SSAB’s GreenCoat® steel, utilizing bio-based oils, is targeting European projects requiring fossil-free certification, while BlueScope’s portfolio restructuring emphasizes investment in electric arc furnace (EAF)-based low-carbon steel production.

Market Trend: PVDF Powder Coatings Driving Zero-VOC Transition in Architectural Pre-Painted Steel Applications

The pre-painted steel coatings market is undergoing a structural shift as architectural specifications for roofing systems and wall panels transition from solventborne PVDF liquid coatings to zero-VOC PVDF powder coatings. This transition is directly aligned with LEED v5 decarbonization requirements and California Title 24 energy regulations, both of which emphasize reduced embodied carbon and the elimination of volatile organic compound emissions in building envelope materials.

A critical advantage of PVDF powder coatings lies in their near-zero VOC profile. Conventional 70% PVDF liquid coatings typically contain 350–450 g/L of VOCs, requiring coil coating facilities to install and operate Regenerative Thermal Oxidizers for solvent abatement. Powder-based systems eliminate this requirement entirely, reducing both capital expenditure and ongoing energy consumption associated with emissions control infrastructure. This provides a measurable improvement in operational efficiency and carbon footprint reduction for large-scale steel coil coating operations.

Material utilization efficiency is another major driver. Advanced powder coating lines achieve transfer efficiencies of 95–98%, significantly outperforming liquid coating systems where solvent evaporation and overspray losses reduce usable material yield. With 100% recyclability of overspray powder, manufacturers are reporting a 25% to 30% reduction in total material waste, improving cost control and supporting circular manufacturing practices.

Performance enhancements further strengthen the value proposition. PVDF powder coatings enable a single-pass dry film thickness of 50–100 µm, compared to 20–25 µm for liquid coatings. This increased film build improves resistance to abrasion, scratching, and handling damage during transport and installation. At the same time, modern PVDF powder formulations maintain long-term color stability with ΔE≤5.0 over 20 years in high-UV exposure environments, meeting stringent architectural durability standards.

Market Trend: Chrome-Free Pretreatment Technologies Standardizing Sustainable Surface Preparation in Steel Coating Lines

The transition toward chrome-free pretreatment technologies is becoming a defining trend in the pre-painted steel industry, particularly within appliance manufacturing and coated steel supply chains. Traditional hexavalent chromium phosphate systems are being phased out in favor of zirconium and silane-based chemistries that eliminate hazardous waste and improve environmental compliance.

Zirconium-based pretreatment systems offer near-zero hazardous sludge generation, representing a significant reduction compared to chromium-based conversion coatings that produce high volumes of toxic waste. This shift is enabling manufacturers to align with zero-hazardous-waste production strategies while reducing disposal costs and regulatory liabilities associated with heavy metal handling.

From a performance standpoint, modern zirconium-silane hybrid systems deliver corrosion resistance exceeding 1,000 hours in Neutral Salt Spray testing under ASTM B117 standards on both cold-rolled and galvanized steel substrates. This ensures long-term coating adhesion and corrosion protection, achieving parity with traditional chrome-based systems while supporting safer and more sustainable manufacturing practices.

Operational efficiency gains are also significant. Chrome-free pretreatment processes typically operate at ambient temperatures between 20°C and 30°C, eliminating the need for heated phosphate baths that traditionally operate around 60°C. This results in a 15–20% reduction in energy consumption across pretreatment lines, contributing to lower operating costs and improved energy efficiency metrics in steel coating facilities.

Market Opportunity: US EPA NESHAP Subpart SSSS Revisions Accelerating Adoption of Inherently Compliant Coating Systems

The 2026 revisions to the National Emission Standards for Hazardous Air Pollutants under Subpart SSSS, implemented by the U.S. Environmental Protection Agency, are creating a strong regulatory push toward zero-VOC and low-HAP coating technologies in the pre-painted steel industry. The updated regulation mandates a 15% reduction in organic hazardous air pollutant emissions for existing facilities and eliminates legacy Startup, Shutdown, and Malfunction exemptions, requiring continuous compliance across all operating conditions.

This regulatory tightening significantly increases the compliance burden for facilities using solventborne coatings. The requirement to implement continuous parameter monitoring systems for abatement equipment introduces additional capital and operational costs. As a result, manufacturers are increasingly evaluating inherently compliant coating technologies such as PVDF powder coatings, which eliminate the need for thermal oxidizers and complex emissions monitoring infrastructure.

The regulatory framework effectively creates a transition pathway where powder coatings and high-solids or waterborne alternatives become the preferred compliance strategy. This is expected to accelerate capital investment in powder-compatible coil coating lines and drive increased adoption across construction, appliance, and industrial steel applications.

Market Opportunity: China VOCs Phase 4 and GB 30981-2025 Standards Creating Large-Scale Demand for Zero-VOC Pre-Painted Steel

The implementation of the VOCs Phase 4 Action Plan by the Ministry of Ecology and Environment, supported by mandatory standards GB 30981.1-2025 and GB 30981.2-2025, is generating substantial demand for zero-VOC and chrome-free pre-painted steel products across China’s industrial ecosystem. Effective from June 2026, these standards impose the strictest limits on VOC emissions, formaldehyde content, and heavy metals in coatings used for construction, appliances, and infrastructure.

For the pre-painted steel industry, compliance with these standards effectively mandates the use of powder coatings or advanced waterborne systems, particularly in safety-critical applications such as public infrastructure and large-scale urban development projects. This regulatory shift is reinforced by procurement policies under the 15th Five-Year Plan, which require state-owned enterprises to prioritize environmentally compliant steel products.

This policy direction is driving a significant reallocation of demand, with an estimated $2.5 billion annual shift away from solventborne coated steel toward zero-VOC alternatives by 2027. Manufacturers that invest in compliant coating technologies are positioned to capture this growing demand, particularly in sectors such as transportation infrastructure, residential construction, and industrial equipment.

In addition, alignment with global environmental standards enhances the export competitiveness of Chinese pre-painted steel products. By meeting zero-VOC and chrome-free requirements, manufacturers can more easily access markets in Europe and North America, where regulatory scrutiny on embedded emissions and hazardous substances continues to intensify.

Pre-Painted Steel Market Share and Segmentation Insights: HDG Substrate Dominance and Direct Mill-to-Manufacturer Supply Chains

By Substrate Type: Hot-Dip Galvanized (HDG) Steel Leads with Superior Corrosion Protection and Formability

The hot-dip galvanized (HDG) segment dominated the pre-painted steel market with a 58.4% share in 2025, driven by its proven corrosion protection performance, cost efficiency, and widespread industrial adoption. HDG steel provides excellent sacrificial protection, making it the preferred substrate for building cladding, roofing systems, garage doors, and HVAC applications, where long-term durability in outdoor environments is critical. Its well-established global supply chain and competitive pricing further reinforce its position as the standard base material for coil-coated steel products. Additionally, HDG substrates offer excellent formability and weld-through capability, enabling efficient roll-forming, stamping, and fabrication processes in construction and manufacturing industries. Surface pre-treatment technologies such as zirconium and phosphate coatings enhance paint adhesion and coating performance, ensuring long-lasting finishes. This combination of durability, manufacturability, and cost-effectiveness continues to drive the dominance of HDG in the global pre-painted steel market.

By Sales Channel: Direct Sales Channel Leads with Mill-Level Integration and Just-in-Time Supply Efficiency

The direct sales segment accounted for a leading 52.1% share of the pre-painted steel market in 2025, reflecting the increasing preference for mill-to-manufacturer supply models and streamlined procurement strategies. Large-scale end users, including roofing manufacturers, appliance producers, and automotive component suppliers, procure pre-painted HDG and Galvalume steel directly from steel mills and coil coating facilities to secure volume-based pricing, consistent material quality, and reliable supply continuity. This direct engagement enables enhanced coordination between steel production lines and downstream manufacturing operations, supporting just-in-time (JIT) delivery systems that minimize inventory costs and improve operational efficiency. Furthermore, direct relationships facilitate better control over coating specifications, color consistency, and performance standards, ensuring compliance with project requirements. As demand for high-quality pre-painted steel in construction and industrial applications continues to grow, the direct sales channel is expected to remain a critical driver of market efficiency and expansion.

Competitive Landscape of the Pre-Painted Steel Market

ArcelorMittal Leads Low-Carbon Innovation with XCarb® and AI-Driven Coating Systems

ArcelorMittal remains the global benchmark in the pre-painted steel market, particularly in sustainable production. By 2026, the company achieved a 47.7% reduction in Scope 1 and 2 emissions compared to 2018 levels, with a carbon intensity of 1.79 tCO₂e per tonne of steel. Its XCarb® brand leads in low-carbon steel solutions, supported by significant R&D investments and the launch of 38 new products in 2025. The integration of AI-driven quality management systems enhances efficiency and reliability across coating lines. ArcelorMittal is also investing in renewable energy capacity to support its electric arc furnace operations, reinforcing its leadership in green steel and advanced coating technologies.

Nippon Steel Expands Global Capacity with Intelligent Steel and AI-Driven Coating Technologies

Nippon Steel Corporation is a major player in the pre-painted steel market, focusing on high-value-added products and global expansion. The company reported strong production growth and increased revenue, driven by demand for advanced coated steels. Its “Intelligent Steel” initiative integrates AI and digital technologies to enhance coating performance and product quality. Nippon Steel is also investing heavily in global capacity expansion and strategic acquisitions to strengthen its presence in key markets. Its focus on defense, energy, and advanced manufacturing sectors positions it strongly in next-generation coated steel solutions.

BlueScope Steel Dominates Branded Pre-Painted Steel with Premium Residential Solutions

BlueScope Steel is a leader in the branded pre-painted steel market, particularly in residential construction. Its COLORBOND® and COLORSTEEL® brands are widely recognized for durability and aesthetic appeal. The company has improved cost efficiency and productivity while maintaining strong shareholder returns. BlueScope’s strategic focus on premium value-added products ensures resilience in fluctuating construction markets. Its continued investment in operational efficiency and asset optimization strengthens its leadership in high-quality pre-painted steel for residential and commercial applications.

SSAB Drives Fossil-Free Steel Innovation with Bio-Based Coatings and GreenCoat® Solutions

SSAB AB is at the forefront of the fossil-free steel movement, offering the first commercial zero-carbon steel products in 2026. Its GreenCoat® range incorporates bio-based coating technologies, replacing fossil-based oils with renewable alternatives such as rapeseed oil. The company’s integration of renewable energy across its production processes ensures a low-carbon value chain. SSAB’s expertise in high-strength steel allows for lightweight yet durable pre-painted products, making it a preferred choice for sustainable construction and infrastructure projects.

Tata Steel Advances Digital Steelmaking with High-End Coated Products and E-Commerce Integration

Tata Steel is transforming into a digital leader in the pre-painted steel market, focusing on high-end downstream products and innovative sales models. The company achieved record production and delivery volumes in 2026, supported by growth in its Automotive & Special Products segment. Its digital platforms have significantly increased sales efficiency, reflecting strong adoption of e-commerce in the steel industry. Tata Steel’s commitment to Net Zero and investments in electric arc furnace technology reinforce its focus on sustainable and digitally enabled steel production.

POSCO Leads Smart Manufacturing with AI-Driven Coating and Advanced Materials Innovation

POSCO is a key innovator in the pre-painted steel market, leveraging smart factory technologies to enhance product quality and efficiency. Its AI-driven process control systems optimize coating adhesion and material performance, particularly for aerospace and EV applications. POSCO is also investing in advanced materials such as graphene-enhanced coatings and carbon nanotube technologies, enabling the development of ultra-durable steel products. Its strong focus on renewable energy applications and modular construction positions it as a leader in high-performance coated steel solutions.

India Pre-Painted Steel Market: Infrastructure Powerhouse and Green Steel Transition

India is currently the most dynamic market in the global pre-painted steel industry, driven by large-scale infrastructure development and strong policy support for domestic manufacturing. Government initiatives such as the National Steel Policy (updated 2025) and the PLI scheme for specialty steel are accelerating investments in high-tensile pre-painted galvanized (PPGI) products, particularly for industrial roofing and white goods.

Mega infrastructure programs like the Gati Shakti National Master Plan are fueling demand for pre-painted sandwich panels in logistics parks, airports (e.g., Jewar Airport), and industrial corridors. Major investments, including ArcelorMittal Nippon Steel’s $6.7 billion expansion at Hazira, highlight the country’s focus on scaling high-quality production.

Technological advancements include antimicrobial and anti-dust coatings tailored for polluted urban environments, while sustainability initiatives such as green hydrogen-based DRI processes are enabling the production of low-carbon “green pre-painted steel.” The market is also strengthened by strict BIS Quality Control Orders (QCO) regulating imports, ensuring domestic competitiveness and quality standards.

China Pre-Painted Steel Market: High-End Functional Coatings and Digital Manufacturing

China is transitioning from volume dominance to high-end specialization in pre-painted steel, focusing on advanced coatings and digital manufacturing technologies. Environmental mandates under the “Blue Sky” policy are forcing upgrades to low-VOC and solvent-free coating lines, improving sustainability across the sector.

Technological innovation includes ultra-durable PVDF coatings offering over 30 years of color retention, especially for coastal skyscrapers. The country is also leveraging AI-enabled digital twin coating lines, capable of predicting coating thickness with high precision and reducing material waste.

Key growth areas include the EV supply chain, where pre-painted steel is used in motor housings and battery enclosures, and 5G infrastructure, requiring dielectric-coated steel for base station enclosures. Additionally, innovations such as 3D digital printed PCM finishes are expanding applications in premium construction and interior design.

United States Pre-Painted Steel Market: Reshoring and ESG-Driven Innovation

The U.S. pre-painted steel market is being reshaped by reshoring initiatives, sustainability mandates, and infrastructure investments. The Bipartisan Infrastructure Law is driving demand for pre-painted steel in transportation systems, sound barriers, and public transit hubs.

Environmental regulations, particularly PFAS-free mandates, are accelerating the shift toward bio-based resin coatings, aligning with ESG and LEED certification requirements. Technological innovations include Cool Roof coatings for energy efficiency and self-healing coatings that automatically repair surface damage using microcapsule technology.

The expansion of electric arc furnace (EAF) steel production is providing low-carbon substrates, while blockchain-based traceability systems are enhancing supply chain transparency. Growth in residential metal roofing and EV-related applications further strengthens the U.S. market outlook.

Germany Pre-Painted Steel Market: Green Steel Leadership and Advanced Coating Technologies

Germany is the global leader in low-carbon pre-painted steel production, focusing on sustainability, advanced engineering, and high-performance applications. Government support for green steel initiatives is enabling the production of CO₂-reduced pre-painted coils for automotive and construction sectors.

Technological advancements include near-infrared (NIR) curing systems, reducing energy consumption by up to 25%, and thermochromic coatings that adapt to temperature changes for passive building cooling. Strict compliance with EU building regulations is driving demand for insulated metal panels (IMPs), while innovations in anti-graffiti and easy-clean coatings are supporting infrastructure projects such as high-speed rail networks.

Germany is also pioneering the use of recycled-content steel substrates (90%+ scrap) without compromising coating quality, reinforcing its leadership in sustainable and circular manufacturing.

Brazil Pre-Painted Steel Market: Protectionism and Agribusiness Demand

Brazil has emerged as a protected yet rapidly growing market in the pre-painted steel sector, driven by strong domestic demand and trade policies. The imposition of anti-dumping duties (2026) on imports from China and India has boosted local production and utilization rates.

The agribusiness sector is a major demand driver, with widespread use of corrosion-resistant pre-painted steel for silos and grain storage systems. Government initiatives such as the Nova Indústria Brasil (NIB) plan are supporting modernization of coating technologies, while the adoption of ZAM (zinc-aluminum-magnesium) substrates is significantly improving corrosion resistance.

Infrastructure projects, including housing programs like Minha Casa, Minha Vida, are further increasing demand for pre-painted roofing solutions. Innovations in thermoplastic-coated steel for offshore oil and gas applications and improvements in supply chain efficiency are strengthening Brazil’s market position.

Vietnam Pre-Painted Steel Market: Electronics Hub and Export Growth

Vietnam is rapidly emerging as a key global hub in the pre-painted steel market, driven by foreign investments and its role as an alternative manufacturing base. Significant investments by Korean and Japanese firms are expanding coil coating capacity, particularly for electronics applications.

The country is a major producer of VCM (Vinyl Coated Metal) used in appliances and electronics, serving global brands like Samsung and LG. Government incentives for clean production are encouraging the adoption of energy-efficient coating technologies, while infrastructure development is driving demand for marine-grade pre-painted steel in coastal regions.

Product innovations such as matte and wrinkled finishes are gaining traction in export-oriented furniture markets, while alignment with ASEAN green building standards is promoting high-reflectivity coatings. These factors position Vietnam as a fast-growing player in the global supply chain.

Turkey Pre-Painted Steel Market: Strategic Export Hub and Technological Advancement

Turkey plays a crucial role as a bridge between European and Middle Eastern markets in the pre-painted steel industry. The integration of continuous galvanizing lines (CGL) with color coating lines (CCL) is improving substrate quality and enabling production of export-grade PPGI products.

Technological advancements include bonded metallic coatings that prevent pigment separation and enhance aesthetic quality. The HVAC sector is a major application area, with demand for epoxy-polyester hybrid coatings in outdoor units. Post-earthquake reconstruction efforts are driving the use of lightweight pre-painted steel for modular housing, while compliance with the EU’s Carbon Border Adjustment Mechanism (CBAM) ensures competitiveness in European markets.

Government support through export financing and innovation incentives is further strengthening Turkey’s position as a global supplier of high-quality pre-painted steel.

Pre-Painted Steel Market Report Scope

Pre-Painted Steel Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$19.5 Billion

|

|

Market Size (2032)

|

$24.6 Billion

|

|

Market Growth Rate

|

3.4%

|

|

Segments

|

By Substrate Type (Hot-Dip Galvanized, Galvalume, Electro-Galvanized, Zinc-Aluminum-Magnesium, Cold-Rolled), By Coating Chemistry (Regular Modified Polyester, Silicon Modified Polyester, Polyvinylidene Fluoride, Plastisol, Polyurethane, Epoxy), By Layer Configuration (Single-Coat System, Double-Coat System, Multi-Coat System), By Finish and Aesthetic (Solid Color Finish, Metallic and Pearlescent Finish, Textured and Embossed Finish, Print-Tech Finishes, Matte), By End-Use Industry (Building and Construction, Household Appliances, Transportation and Automotive, Furniture and Office Equipment, Consumer Electronics, Infrastructure and Energy), By Sales Channel (Direct Sales, Steel Service Centers and Toll Coaters, Metal Distributors and Wholesalers)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

ArcelorMittal, Nippon Steel Corporation, POSCO, Baoshan Iron and Steel Co., Ltd., BlueScope Steel Limited, Tata Steel Limited, JFE Steel Corporation, Nucor Corporation, Ternium S.A., SSAB, JSW Steel Limited, United States Steel Corporation, Hyundai Steel, Marcegaglia Carbon Steel, ThyssenKrupp Steel Europe AG

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Pre Painted Steel Market Segmentation

By Substrate Type

- Hot-Dip Galvanized

- Galvalume

- Electro-Galvanized

- Zinc-Aluminum-Magnesium

- Cold-Rolled

By Coating Chemistry

- Regular Modified Polyester

- Silicon Modified Polyester

- Polyvinylidene Fluoride

- Plastisol

- Polyurethane

- Epoxy

By Layer Configuration

- Single-Coat System

- Double-Coat System

- Multi-Coat System

By Finish and Aesthetic

- Solid Color Finish

- Metallic and Pearlescent Finish

- Textured and Embossed Finish

- Print-Tech Finishes

- Matte

By End-Use Industry

- Building and Construction

- Household Appliances

- Transportation and Automotive

- Furniture and Office Equipment

- Consumer Electronics

- Infrastructure and Energy

By Sales Channel

- Direct Sales

- Steel Service Centers and Toll Coaters

- Metal Distributors and Wholesalers

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Pre Painted Steel Industry

- ArcelorMittal

- Nippon Steel Corporation

- POSCO

- Baoshan Iron & Steel Co., Ltd.

- BlueScope Steel Limited

- Tata Steel Limited

- JFE Steel Corporation

- Nucor Corporation

- Ternium S.A.

- SSAB

- JSW Steel Limited

- United States Steel Corporation

- Hyundai Steel

- Marcegaglia Carbon Steel

- ThyssenKrupp Steel Europe AG

*- List not Exhaustive