Prefilled Syringe Packaging Market Size, Overview, and Growth Outlook (2025–2034)

Prefilled Syringe Packaging Market Set to Surge to $2.1 Billion by 2034 Fueled by Biologics and Patient-Centric Innovations

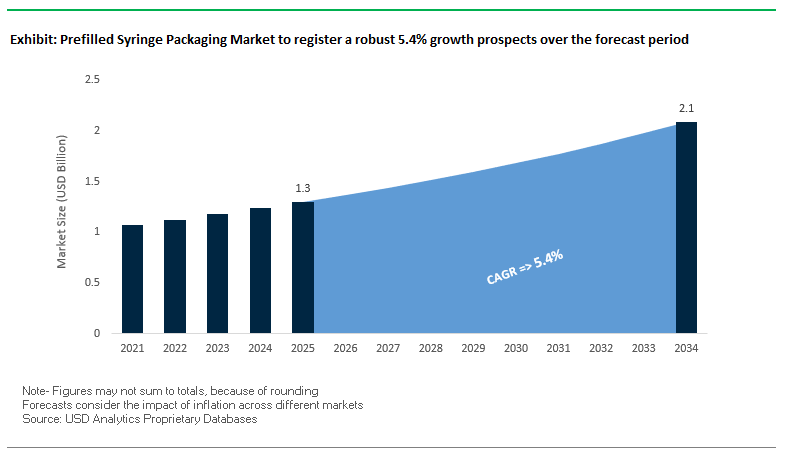

The global prefilled syringe packaging market is projected to grow from $1.3 billion in 2025 to $2.1 billion by 2034, at a CAGR of 5.4%, driven by the increasing demand for biologics, biosimilars, and patient-friendly drug delivery systems. Prefilled syringes enhance patient safety, dosage accuracy, and ease of self-administration, which is especially critical for chronic disease management. The growing shift from traditional glass to polymeric materials like Cyclo-Olefin-Polymer (COP) provides higher break resistance, better drug compatibility, and design flexibility, enabling pharmaceutical companies to meet evolving healthcare needs.

Key Insights for industry professionals and buyers:

- Biologics Driving Packaging Innovation: Sensitive drugs require specialized syringes to maintain stability and efficacy over shelf life.

- Enhanced Patient Safety and Self-Administration: Prefilled syringes reduce dosage errors and needlestick injuries, supporting home use and patient independence.

- Transition to Advanced Polymers: COP and similar materials offer superior break resistance, lower risk of drug interaction, and greater design flexibility.

- Integrated Safety Features are Essential: Passive needle shields and auto-retracting needles are increasingly mandated to meet regulatory and safety requirements.

- Simplified Healthcare Operations: Prefilled formats reduce preparation errors in hospitals and clinics, enhancing operational efficiency.

- Growing Biologics and Chronic Disease Management: Rising adoption of injectables for diabetes, autoimmune disorders, and vaccines boosts market demand.

- Sustainability and Circularity Trends Emerging: Companies are exploring recyclable polymer components and environmentally conscious solutions.

Market Analysis: Industry Advancements Showcase Integration of Nanocoatings, Recyclable Materials, and Regulatory-Approved Prefilled Syringes

Recent developments in the prefilled syringe packaging industry emphasize safety, sustainability, and technological innovation. In August 2025, Trinseo launched a recycling project in China with an annual production capacity of 5,000 tons of recycled polycarbonate, supporting the circular economy and sustainable syringe components. That month, a Nano Letters study introduced an inhibitor-modified atomic layer deposition (ALD) strategy for ultrathin films, which could transform high-barrier syringe packaging, enhancing drug stability.

Regulatory approvals are also accelerating innovation. In July 2025, the U.S. FDA approved GSK’s Shingrix prefilled syringe, eliminating the need for reconstitution and simplifying administration for healthcare professionals and patients. Strategic partnerships, such as the June 2025 Covestro-PolySource distribution deal, are expanding access to advanced polymeric materials, bolstering production capacity and material availability for the pharmaceutical sector.

Additional innovations target safety, efficiency, and tracking. In April 2025, IL Group delivered tamper-evident labeling solutions to Exela Pharma Sciences, meeting regulatory compliance for COC syringes. In March 2025, Schreiner Group and SCHOTT Pharma launched prefilled syringes with RFID tags, optimizing hospital inventory management. Earlier initiatives include BD’s November 2024 release of the Neopak™ XtraFlow™ Glass Prefillable Syringe, and September 2024 capacity expansion in France, both addressing growing biologics demand.

Transformative Trends and Emerging Opportunities in the Prefilled Syringe Packaging Market

Adoption of High-Barrier Polymer Syringes for Sensitive Biologics

The prefilled syringe packaging market is undergoing a fundamental shift with the adoption of polymer syringes, particularly those made from cyclic olefin copolymer (COC), to address the stability and safety challenges of biologics. A 2025 ResearchGate study highlighted how COC syringes eliminate the need for silicone oil lubrication, a major cause of protein aggregation in glass syringes. Additionally, these systems avoid the use of tungsten pins, preventing leachables that compromise biologic stability. Beyond contamination risks, polymer syringes demonstrate superior protein stability compared to glass, as confirmed in the Journal of Pharmaceutical Sciences. When subjected to stress and agitation during transport, biologics in COC syringes showed reduced aggregation, which is vital for maintaining efficacy. With the global biologics pipeline expanding rapidly, the demand for packaging that ensures product integrity through complex cold chain logistics is accelerating adoption of polymer syringes. This trend positions COC-based syringes as a high-growth segment for next-generation injectable therapies.

Integration of Safety-Engineered Devices to Mitigate Needlestick Injuries

Regulatory frameworks are pushing manufacturers toward incorporating safety-engineered devices in prefilled syringes to safeguard healthcare workers. The EU Medical Devices Regulation (MDR), fully enforced since May 2021, has heightened safety and performance requirements, making compliance-driven innovation essential. This regulatory pressure is fueling industry launches such as SCHOTT Pharma’s 2025 polymer syringe platform, designed with integrated safety mechanisms to reduce needlestick risks. These devices provide user-friendly functionality for healthcare professionals while aligning with occupational safety mandates. The market is further driven by growing awareness of the cost burden associated with workplace injuries and compensation claims. Safety-engineered prefilled syringes are no longer optional but increasingly the baseline expectation in both hospital and home-care environments, strengthening their role in global adoption strategies.

Development of Connected and Smart Syringes for Adherence Monitoring

The rise of digital health is creating opportunities for prefilled syringes with embedded connectivity features. Smart syringes equipped with Bluetooth or NFC sensors can capture real-time data on dosing events, providing objective adherence records for clinical trials. Flex, a medtech innovator, has showcased how these systems help validate therapeutic efficacy by supplying accurate patient-use data—overcoming a major limitation of self-reported adherence. Beyond clinical trials, smart dosing platforms enable remote monitoring of patients with chronic conditions, such as diabetes or rheumatoid arthritis, where precise, frequent injections are critical. By feeding dose information into cloud-based platforms, healthcare providers gain a powerful tool to optimize therapy outcomes and reduce costly non-compliance. As healthcare systems worldwide shift toward digital-first strategies, connected syringe packaging is emerging as a cornerstone for precision medicine and value-based care.

Advanced Lyophilized Drug Product Platforms for Cold Chain Independence

Dual-chamber prefilled syringes represent a major opportunity to improve drug stability and reduce cold chain reliance. These systems separate lyophilized drug substances from liquid diluents until the point of use, simplifying reconstitution while preserving drug potency. SCHOTT Pharma’s dual-chamber innovations consolidate what traditionally required three separate containers into a single device, minimizing preparation errors and improving patient convenience. By stabilizing sensitive biologics in dry form, lyophilized syringe systems drastically reduce dependence on ultra-cold logistics, which remain cost-prohibitive and unreliable in developing markets. A recent industry report on lyophilized injectables emphasized that this approach broadens global access to biologics, making advanced therapies viable even in resource-limited settings. As biologics and cell/gene therapies dominate drug pipelines, lyophilization-enabled prefilled syringes are set to play a pivotal role in unlocking new growth opportunities for packaging manufacturers while addressing one of the industry’s most critical infrastructure challenges.

Competitive Landscape: Leading Prefilled Syringe Packaging Companies are Driving Innovation Through Advanced Materials and Patient-Centric Designs

The global prefilled syringe packaging market is dominated by companies that excel in biologics-compatible materials, safety-enhanced syringes, and integrated delivery systems. These leaders differentiate themselves through material innovation, production capacity expansions, and sustainable practices.

BD (Becton, Dickinson and Company): Setting Global Standards in Prefilled Syringes and High-Viscosity Drug Delivery

BD is a world leader in prefillable drug delivery systems, offering glass and polymer syringes, self-injection devices, and needle technologies. Its BD Neopak™ XtraFlow™ syringe, launched in November 2024, features an optimized cannula and needle length for high-viscosity drugs. The September 2024 manufacturing expansion in France increased production capacity to meet rising biologics demand. BD focuses on providing end-to-end solutions, from development to commercialization, establishing itself as a trusted partner for pharmaceutical companies.

Gerresheimer AG: Combining Customization and Sustainability for High-Performance Prefilled Syringes

Gerresheimer offers glass and polymer syringes with Gx® Performance Levels, providing systematic customization for different drug delivery needs. The company prioritizes sustainability, aiming for 100% renewable electricity and a 50% CO2 reduction by 2030. Its products integrate seamlessly into fill-and-finish processes, reducing total cost of ownership and offering tailored features including needle configurations, volumes, and material options to meet complex pharmaceutical requirements.

Stevanato Group: Delivering High-Value Prefilled Syringes with Advanced Coating Technology

Stevanato Group’s Alba® glass syringes feature a cross-linked silicone oil coating, reducing sub-visible particles and ensuring superior gliding performance—critical for auto-injectors. Its March 2023 collaboration with Recipharm for soft mist inhalers demonstrates its ability to provide integrated, high-value solutions. The company offers comprehensive services, including engineering, manufacturing, and testing, supporting clients throughout the drug lifecycle.

West Pharmaceutical Services, Inc.: Enhancing Prefilled Syringe Safety and Regulatory Compliance Through Elastomer Expertise

West provides components for prefilled syringes, including plungers, stoppers, and containment systems. Its elastomer technology ensures safe, effective delivery of medicines. In August 2024, West published an eBook on navigating combination product regulations, reflecting its role as an industry guide for compliance and regulatory strategy.

SCHOTT Pharma: Expanding Capacity and Specializing in Biologics-Compatible Prefilled Syringes

SCHOTT Pharma offers high-quality glass and polymer syringes, including the TOPPAC freeze polymer syringe for temperature-sensitive mRNA therapies. In August 2025, the company launched a new syringe and cartridge glass tubing facility in India, becoming Asia’s largest producer, supporting the growing demand for biologics and GLP-1 injectables. SCHOTT Pharma emphasizes localized supply, zero-defect manufacturing, and advanced material solutions.

Prefilled Syringe Packaging Market Share Insights, 2025-2034

Single-Chamber Designs Dominate Market Share by Design in the Prefilled Syringe Packaging Industry

Single-chamber prefilled syringes command an overwhelming 82% market share, reflecting their position as the industry’s gold standard for drug delivery. Their simplicity, cost-effectiveness, and compatibility with both small-molecule drugs and the expanding class of biologics make them the default platform for most pharmaceutical companies. These designs reduce dosing errors, improve patient compliance, and integrate seamlessly with automated fill-finish lines, ensuring scalability for high-volume therapies like vaccines and autoimmune disease treatments. Dual-chamber syringes, while accounting for a smaller share, are increasingly vital for lyophilized and unstable drugs, showcasing growth as biologics requiring on-demand reconstitution gain traction. Customized syringes remain niche but are strategically important in areas like viscous biologics, needle-safety technology, and light-sensitive formulations. The segmentation highlights how the market is bifurcating between high-volume standardized formats and specialized innovations, with single-chamber designs retaining dominance while advanced drug delivery drives growth in smaller, high-value segments.

Autoimmune Diseases Lead Market Share by Application in the Prefilled Syringe Packaging Industry

Autoimmune disease treatments represent the largest application segment at 25%, fueled by the explosion of biologic therapies such as Humira®, Enbrel®, and emerging biosimilars. These chronic therapies demand frequent self-administration, positioning prefilled syringes as the most patient-friendly delivery format by ensuring accuracy, reducing preparation steps, and enhancing compliance. Diabetes follows closely, supported by the surge in insulin delivery and the meteoric rise of GLP-1 receptor agonists, which require specialized prefilled formats for safety and precision. Oncology is rapidly gaining share as subcutaneous biologics become mainstream in outpatient care, reducing reliance on infusion centers and lowering healthcare costs. Vaccines, solidified during the COVID-19 pandemic, remain a major application due to speed, dose accuracy, and safety advantages over vials. Antithrombotics and anaphylaxis represent smaller but mission-critical markets where dose reliability and rapid administration are non-negotiable. Collectively, these applications emphasize that chronic disease management and biologics adoption are the twin engines driving prefilled syringe demand, with strong spillover effects across therapeutic categories.

United States: FDA Guidance, Polymer Syringes, and Outsourced Fill-Finish Expansion

The United States prefilled syringe packaging market is driven by FDA regulations, which encourage adoption due to their role in improving patient safety, reducing drug waste, and minimizing medication errors. Oversight from the Food and Drug Administration (FDA) and related agencies ensures that prefilled syringes meet strict safety and efficacy requirements, making them increasingly attractive to pharmaceutical manufacturers. A key innovation trend is the shift toward polymer syringes (COP/COC), which offer improved performance over glass, particularly for biologics that are sensitive to delamination, particulate formation, or breakage.

Another critical focus area is particulate and siliconization control. To comply with stricter quality standards, manufacturers are introducing baked-on silicone coatings and advanced visual inspection systems to minimize risks of immunogenicity. Convergence with auto-injectors and safety devices is also a growing trend, driven by the need to prevent needlestick injuries and enable home-care administration. On the business front, companies like Baxter have expanded injectable portfolios with new prefilled syringe products, such as its Regadenoson Injection launch. Additionally, there is a growing reliance on Contract Manufacturing Organizations (CMOs) for outsourced fill-finish services, providing flexibility, capacity, and speed-to-market for pharmaceutical companies seeking efficient packaging solutions.

European Union: PPWR, EMA Standards, and Robotics in Aseptic Filling

The European Union is shaping its prefilled syringe packaging market through a mix of sustainability regulations and pharmaceutical quality standards. The Packaging and Packaging Waste Regulation (PPWR), effective February 2025, requires recyclability and reusability, compelling syringe packaging manufacturers to align with circular economy objectives. In parallel, Commission Regulation (EU) 2024/3190, effective January 2025, bans bisphenol A (BPA) in food-contact materials, influencing material choices for medical and pharmaceutical packaging.

The European Medicines Agency (EMA) plays a critical role, emphasizing risk-based approaches and quality-by-design principles in packaging for biologics and injectables. By 2028, a harmonized recycling label will be mandatory, further pushing pharmaceutical companies toward standardized, transparent packaging practices. Meanwhile, the EU market is witnessing significant adoption of advanced aseptic filling technologies, including isolators and robotics, to maintain sterility and minimize human involvement. These developments reflect Europe’s dual emphasis on regulatory compliance and cutting-edge packaging technologies.

China: Pharmacopoeia Revisions, Regulatory Alignment, and Circular Packaging

China’s prefilled syringe packaging market is undergoing transformation through regulatory harmonization and sustainability initiatives. The National Medical Products Administration (NMPA) introduced the 2025 Medical Device Industry Standards Revisions Plan, aiming to align local regulations with international frameworks, improving compliance and facilitating market entry for global syringe manufacturers. The Chinese Pharmacopoeia 2025 edition, released in March 2025 and effective October 2025, introduces a new Container Closure Integrity (CCI) chapter, strengthening requirements for injectable packaging.

These revisions also align with ICH Q4B guidance principles, ensuring international consistency in quality standards. On the sustainability front, Chinese companies like Jingxing Packaging Materials Co. are implementing circular economy models, using recycled materials and reprocessing production scraps to minimize waste. With stricter standards and sustainability integration, China is positioning itself as both a regulatory-driven and innovation-oriented market for prefilled syringe packaging.

India: Localized Glass Tubing Production and Shift Toward Ready-to-Use Packaging

India’s prefilled syringe packaging market is being reshaped by both foreign investment and domestic regulatory frameworks. SCHOTT’s decision to locally manufacture syringe and cartridge glass tubing through a direct technology transfer from Germany is a milestone, positioning India as Asia’s largest producer of syringe-grade glass tubing. This move aligns with the “Make in India” initiative and bolsters healthcare supply chain self-sufficiency while supporting rising biologics demand.

Pharmaceutical companies in India are increasingly adopting polymer syringes (COP/COC) to avoid risks such as glass delamination, particularly for high-viscosity drugs used in auto-injectors. There is also a clear industry shift from traditional vials to ready-to-use dose formats, driven by efficiency, safety, and reduced preparation time. The Central Drugs Standard Control Organization (CDSCO) enforces strict quality standards, ensuring that Indian manufacturers remain globally competitive. Together, these dynamics are making India a regional hub for both syringe packaging innovation and large-scale manufacturing.

Japan: PMDA Oversight, Stringent Labeling, and Safety-Driven Packaging

Japan’s prefilled syringe packaging market is highly regulated by the Pharmaceuticals and Medical Devices Agency (PMDA), which requires “tempu bunsho” inserts—detailed Japanese-language leaflets providing comprehensive drug and safety information. The Japanese Pharmacopoeia (JP), regularly revised with PMDA involvement, sets clear quality standards for packaging materials and syringes used in pharmaceutical applications.

The market is witnessing growing investment in new materials and technologies that enhance the safety, durability, and performance of prefilled syringes. Post-market surveillance is also strict, with mandatory reporting of adverse drug reactions and device malfunctions, reinforcing the importance of high-quality, compliant packaging. These regulations and practices make Japan one of the most reliability-driven and safety-conscious markets for prefilled syringe packaging.

United Kingdom: MHRA Standards, Plastic Packaging Tax, and Streamlined Approvals

The United Kingdom’s prefilled syringe packaging market is guided by the Medicines and Healthcare products Regulatory Agency (MHRA), which enforces strict quality, labeling, and safety requirements. In 2022, the UK introduced the Plastic Packaging Tax (PPT), applying to all plastic packaging with less than 30% recycled content, incentivizing sustainable material adoption in syringe packaging. At the same time, the Packaging Code for Medicines provides clarity on labeling standards, ensuring that all critical patient information is legible and consistent across products.

The UK government has extended the acceptance of CE-marked medical devices until June 2028, allowing manufacturers more time to transition to UKCA standards. A notable trend is the adoption of expedited assessments for pre-vetted product changes under guidance from industry groups like PAGB, which accelerates packaging approval for new launches. These policies, combined with industry investments, make the UK market a compliance-driven and innovation-friendly environment for prefilled syringe packaging manufacturers.

Prefilled Syringe Packaging Market Report Scope

Prefilled Syringe Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1.3 Billion

|

|

Market Size (2034)

|

$2.1 Billion

|

|

Market Growth Rate

|

5.4%

|

|

Segments

|

By Material (Glass, Polymer), By Design (Single-Chamber, Dual-Chamber, Customized), By Application (Vaccines, Antithrombotics, Autoimmune Diseases, Diabetes, Anaphylaxis, Oncology, Others), By End-Use (Hospitals & Clinics, Ambulatory Surgical Centers, Home-Care Settings), By Closing System (Staked Needle Systems, Needle-Free Systems, Luer Lock Systems)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Becton, Dickinson and Company (BD), Gerresheimer AG, SCHOTT AG, Stevanato Group, West Pharmaceutical Services, Inc., AptarGroup, Inc., Nipro Corporation, Catalent, Inc., Terumo Corporation, Fresenius SE & Co. KGaA, Nemera, Amcor plc, ARaymond, Datwyler Holding Inc., Vetter Pharma

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Prefilled Syringe Packaging Market Segmentation

By Material

By Design

- Single-Chamber

- Dual-Chamber

- Customized

By Application

- Vaccines

- Antithrombotics

- Autoimmune Diseases

- Diabetes

- Anaphylaxis

- Oncology

- Others

By End-Use

- Hospitals & Clinics

- Ambulatory Surgical Centers

- Home-Care Settings

•By Closing System

- Staked Needle Systems

- Needle-Free Systems

- Luer Lock Systems

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Prefilled Syringe Packaging Market

- Becton, Dickinson and Company (BD)

- Gerresheimer AG

- SCHOTT AG

- Stevanato Group

- West Pharmaceutical Services, Inc.

- AptarGroup, Inc.

- Nipro Corporation

- Catalent, Inc.

- Terumo Corporation

- Fresenius SE & Co. KGaA

- Nemera

- Amcor plc

- ARaymond

- Datwyler Holding Inc.

- Vetter Pharma

* List Not Exhaustive

Methodology

The research methodology combines primary and secondary approaches to ensure data reliability and market accuracy for the Prefilled Syringe Packaging Market. Primary research included interviews with pharmaceutical executives, packaging engineers, medtech innovators, regulatory specialists, and supply chain stakeholders across key regions such as North America, Europe, China, India, Japan, and the UK. Secondary research encompassed analysis of company annual reports, regulatory databases, patents, sustainability reports, and verified industry publications, with special attention to developments in biologics-compatible materials, polymer syringes, dual-chamber systems, and smart/connected devices. Advanced data triangulation validated market sizing, growth projections, and segmentation, integrating macroeconomic indicators, biologics adoption trends, polymer and glass material pricing, and technological innovation rates. Forecasts were generated using both top-down and bottom-up approaches, while regional insights were contextualized against local regulations, safety standards, sustainability mandates, and evolving healthcare delivery models. This rigorous, multi-layered methodology by USDAnalytics ensures that the report delivers accurate, fact-based, and actionable intelligence aligned with the real-world dynamics of the global prefilled syringe packaging industry.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.