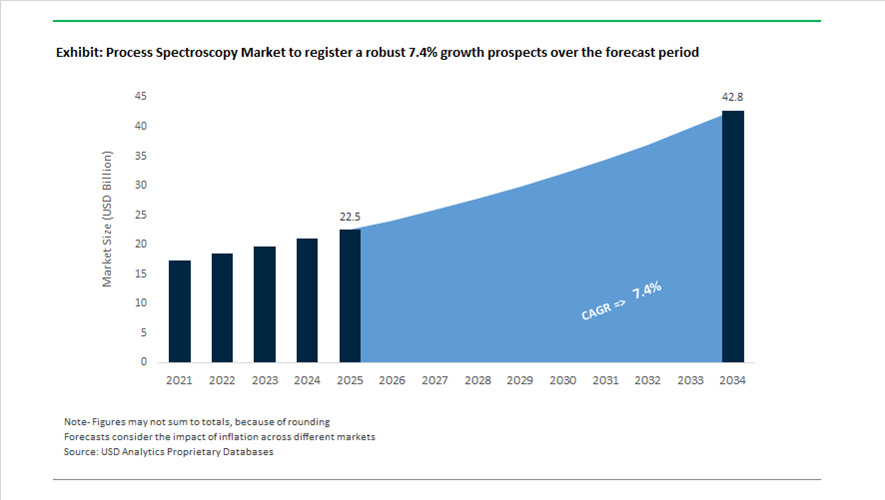

Process Spectroscopy Market Valued at $22.5 Billion in 2025, Projected to Reach $42.8 Billion by 2034 at 7.4% CAGR

The global process spectroscopy market is valued at $22.5 billion in 2025 and is projected to reach $42.8 billion by 2034, expanding at a strong CAGR of 7.4%. Growth is fueled by rising adoption of in-line FT-NIR spectroscopy, Raman spectroscopy, gas chromatography-mass spectrometry (GC-MS), optical dissolved oxygen sensors, plasma focused ion beam SEM systems, and AI-integrated analytical software platforms across chemical manufacturing, oil and gas refining, semiconductor fabrication, pharmaceuticals, food processing, and energy infrastructure. Manufacturers are shifting from offline lab testing toward real-time, in-process analytics to enhance yield optimization, catalyst protection, energy efficiency, and regulatory compliance.

Technological momentum accelerated in early 2024. In January 2024, NeoSpectra partnered with Eurofins QTA to deliver handheld near-infrared (NIR) analysis systems for food and agriculture, enabling on-site compositional verification and reducing lab turnaround times. In February 2024, Bruker launched the BEAM FT-NIR spectrometer, a single-point instrument engineered for direct integration into pipelines and conveyor systems. Utilizing FT-NIR technology with a RockSolid™ interferometer, the system brings laboratory-grade spectral precision to continuous process environments handling solids. In March 2024, Bruker expanded its diagnostics and microscopy capabilities through the acquisition of ELITechGroup and Phasefocus, enhancing real-time cell monitoring and phenotypic analysis capabilities for bioprocessing control. In April 2024, Shimadzu introduced ELEM-SPOT, the first element-selective GC-MS capable of selectively detecting oxygen and nitrogen compounds in biofuels, preventing catalyst degradation in refining processes by more than 80%. In September 2024, Yokogawa released the OpreX Intelligent Manufacturing Hub, integrating robotic process automation and advanced visualization tools to convert high-volume spectral data into actionable operational insights.

Integration of automation and high-precision sensing intensified in 2025. In March 2025, Honeywell completed the $2.16 billion acquisition of Sundyne, linking high-pressure flow control with Honeywell’s process spectroscopy and automation systems for petrochemical and energy clients. In late 2025, Thermo Fisher Scientific launched the Helios™ MX1 Plasma Focused Ion Beam Scanning Electron Microscope, a fully automated platform designed to accelerate semiconductor process diagnostics and yield ramp-up. In December 2025, ABB introduced AeroStar™ optical dissolved oxygen sensors capable of measuring down to 4 parts per billion in power and semiconductor steam systems, reducing maintenance requirements by 70% compared to electrochemical alternatives. These developments highlight the convergence of spectral analytics, high-resolution imaging, and industrial automation in high-stakes manufacturing environments.

Digital ecosystem expansion continues into 2026. In February 2026, Agilent Technologies expanded its collaboration with Virscidian to integrate OpenLab CDS with Analytical Studio, automating high-throughput purification and analytical workflows for pharmaceutical production. In the same month, Sappi partnered with ABB to implement advanced fiber measurement and real-time spectroscopy systems at its Netherlands mill, modernizing a legacy facility with continuous compositional monitoring. The process spectroscopy market is increasingly defined by in-line FT-NIR systems for solids, element-selective GC-MS for catalyst protection, AI-driven data integration platforms, handheld NIR for agriculture, semiconductor-focused SEM automation, optical ppb-level oxygen sensing, and cloud-connected analytical software integration. Real-time process optimization, semiconductor fabrication growth, and energy efficiency mandates are driving sustained expansion across industrial analytics platforms globally.

Transformational Trends and High-Value Opportunities in the Process Spectroscopy Market

AI-Driven Decision Support and Cloud-Integrated Spectral Analytics

Process spectroscopy is undergoing a structural shift from being a passive measurement tool to an active decision-support system embedded within production workflows. Across pharmaceuticals, specialty chemicals, and advanced materials, manufacturers are moving away from static chemometric models toward AI-enabled architectures that continuously learn from process variability. This transition is driven by the need to reduce batch failures, maintain regulatory compliance in real time, and shorten response cycles in increasingly complex manufacturing environments.

A defining milestone in this shift emerged in May 2025 with the commercialization of AI-embedded Near-Infrared spectroscopy platforms designed for pharmaceutical production. These systems apply adaptive machine-learning algorithms that automatically recalibrate spectral models as raw material attributes, temperature, or humidity fluctuate. By eliminating the need for periodic manual recalibration, manufacturers can maintain uninterrupted compliance with 21 CFR Part 11 while reducing analyst intervention and validation overhead. The operational impact is significant, particularly in high-throughput solid dose and continuous API manufacturing lines where calibration drift historically caused costly downtime.

Cloud integration is amplifying the strategic value of these systems. Industry surveys conducted in late 2025 indicate that although only around 12% of industrial analytical workflows are fully AI-integrated today, adoption is accelerating rapidly as cloud latency drops and cybersecurity frameworks mature. Through Model Context Protocol and secure cloud pipelines, real-time spectral data is increasingly being fed into enterprise AI agents that correlate molecular signals with yield, energy consumption, and financial performance. This convergence is transforming spectroscopy outputs into operational intelligence, enabling plant managers and executives to make faster, data-backed decisions across global production networks.

Proliferation of Ruggedized Fiber-Optic Probes for In-Line Monitoring

Another structural trend reshaping the process spectroscopy market is the rapid replacement of offline and at-line sampling with ruggedized, in-line fiber-optic probes. Industries operating under extreme process conditions, including petrochemicals, refining, and mineral processing, are prioritizing real-time molecular visibility to reduce lag between deviation and correction. Traditional batch sampling not only introduces contamination risk but also delays corrective action, often resulting in off-spec material and yield losses.

By late 2025, equipment suppliers had widely commercialized next-generation spectroscopy probes engineered with sapphire windows, corrosion-resistant alloys, and high-pressure seals. These designs allow direct immersion into aggressive chemical streams, high-temperature reactors, and abrasive slurries without compromising signal integrity. The shift from hours-long laboratory turnaround to second-by-second in-line feedback is enabling operators to detect fouling, phase changes, or compositional drift almost instantly, significantly improving process stability and asset utilization.

In parallel, portability and ruggedization are extending spectroscopy beyond fixed plants. Mining and metals operations are increasingly adopting handheld and field-deployable Raman and LIBS systems integrated with global mineral libraries. These platforms allow rapid ore characterization at the mine face, preventing low-value or contaminated material from entering downstream processing circuits. This capability is becoming a competitive necessity as operators face tighter margins and rising energy costs, making early-stage decision accuracy a direct driver of profitability.

Continuous Bioprocess Monitoring in Pharma 4.0 Manufacturing

The transition from batch-based pharmaceutical production to continuous manufacturing has created a non-negotiable demand for real-time Process Analytical Technology. Spectroscopy, particularly Raman and Near-Infrared techniques, has emerged as the backbone of continuous quality assurance by enabling in-line monitoring of Critical Quality Attributes throughout the production lifecycle.

Regulatory momentum is reinforcing this opportunity. In January 2025, updated guidance from U.S. regulators explicitly emphasized in-line spectroscopic monitoring as a cornerstone of modern pharmaceutical quality systems. At the same time, the introduction of a dedicated USP chapter addressing PAT lifecycle management has provided manufacturers with a clearer compliance pathway for real-time release testing. Together, these developments are accelerating investment in spectroscopy platforms capable of supporting closed-loop control and automated batch release.

The opportunity is especially pronounced in biologics and RNA-based therapeutics. Industry data from mid-2025 shows that continuous bioprocessing supported by spectroscopic feedback can reduce facility footprints by 30% to 50% while delivering superior batch-to-batch consistency. By maintaining continuous molecular visibility from upstream transcription through downstream purification and fill-finish, manufacturers can reduce variability, accelerate scale-up, and improve regulatory confidence in complex biologic products.

Molecular Waste Sorting and Feedstock Qualification for the Circular Economy

Beyond regulated industries, the circular economy is emerging as one of the fastest-growing opportunity areas for process spectroscopy. Advanced recycling and chemical recovery systems depend on precise, high-speed identification of complex waste streams, a task that cannot be achieved through conventional mechanical sorting alone. Spectroscopic sensors are now the core intelligence layer of modern recycling infrastructure.

By early 2025, leading recycling facilities had integrated Near-Infrared and Raman spectroscopy with AI-based pattern recognition to achieve near-perfect polymer identification accuracy, even in the presence of dyes, fillers, and surface contamination. This capability is critical for producing feedstocks pure enough for chemical recycling, where even minor compositional errors can disrupt pyrolysis, depolymerization, or solvent-based recovery processes.

Spectroscopy is also becoming essential downstream, particularly in monitoring pyrolysis oil quality in real time. The commissioning of large-scale chemical recycling plants in 2025 highlighted the importance of continuous molecular characterization to stabilize output quality and maximize carbon savings. By enabling real-time adjustments to feedstock blends and operating conditions, spectroscopic systems support recycling pathways that can reduce CO2 emissions by more than 30% compared to incineration, aligning industrial performance with tightening sustainability mandates.

Process Spectroscopy Market Share and Segmentation Insights

Molecular Spectroscopy Leads Process Analytical Technologies for Real-Time Industrial Monitoring

Molecular spectroscopy accounted for 58.60% of the Process Spectroscopy Market by technology in 2025, reflecting its broad application across real time industrial process monitoring and quality analysis. Technologies such as near infrared spectroscopy, Raman spectroscopy, Fourier transform infrared spectroscopy, and ultraviolet visible spectroscopy enable rapid, non destructive analysis of chemical composition, moisture content, and product quality parameters. These analytical tools are widely used in pharmaceutical production, chemical manufacturing, and food processing industries where continuous process monitoring is required. In 2025, increasing adoption of Process Analytical Technology frameworks has accelerated deployment of molecular spectroscopy systems, enabling real time quality monitoring and data driven process control across advanced manufacturing environments.

Pharmaceutical and Biotechnology Manufacturing Drives Adoption of Process Spectroscopy Systems

Pharmaceuticals and biotechnology represented 34.80% of the Process Spectroscopy Market by end user industry in 2025, driven by regulatory frameworks that encourage real time monitoring and quality by design manufacturing approaches. Process spectroscopy technologies are widely integrated into pharmaceutical production lines to monitor blending, granulation, drying, and coating operations while ensuring product quality and process consistency. The high value of pharmaceutical products supports investment in advanced analytical instrumentation that reduces production variability and batch failure risks. In 2025, growing adoption of continuous pharmaceutical manufacturing has increased demand for integrated spectroscopy systems, enabling closed loop monitoring and automated process control within modern drug production facilities.

Process Spectroscopy Market Competitive Landscape

The global process spectroscopy market in 2026 is defined by AI-driven chemometrics, digital twin integration, and miniaturized spectral sensors enabling real-time decision-making. Industry leaders are aligning with CCUS, bioprocessing, and EV battery manufacturing demands, transforming spectroscopy into a core Industry 4.0 analytical backbone.

Thermo Fisher Advances AI-Driven Spectroscopy with NVIDIA Partnership and Bioprocess Expansion

Thermo Fisher Scientific is advancing its “Science at Scale” strategy through AI-enabled spectroscopy and global bioprocess expansion. In January 2026, it partnered with NVIDIA to integrate edge AI and accelerated computing into process spectrometers for real-time spectral analysis and autonomous optimization. The company expanded bioprocessing hubs in South Korea and Singapore while opening a collaboration center in Philadelphia to support Process Analytical Technology (PAT) adoption. Product innovation includes the Krios 5 Cryo-TEM and advanced spectral flow cytometry solutions for high-resolution molecular analysis. The $9.4 billion acquisition of Clario strengthens its digital data integration capabilities across clinical and industrial workflows. This positions Thermo Fisher as a leader in AI-integrated spectroscopy for pharmaceutical and advanced materials applications.

Bruker Strengthens Cleantech Leadership with High-Field Spectroscopy and Battery Research Systems

Bruker is executing a cleantech-focused growth strategy centered on high-field magnetic resonance and vibrational spectroscopy technologies. The company targeted 300 basis points of margin expansion by 2026 through a $120 million cost optimization program, with LSMS and Optics divisions maintaining resilience. In October 2025, it secured a major order for 800 MHz Magnetic Resonance systems to support real-time battery material analysis. Integration of NanoString enhances spatial biology capabilities combined with spectroscopic imaging for biopharma validation. Bruker’s high-field NMR and EPR platforms are critical for solving next-generation battery chemistry challenges. This positions the company at the forefront of spectroscopy applications in energy storage and post-genomics research.

ABB Drives CCUS Measurement Innovation with Integrated Gas Analysis and Digital Twin Platforms

ABB Measurement & Analytics is leading decarbonization measurement through integrated spectroscopy solutions for CCUS infrastructure. In February 2026, it launched a fully integrated gas analyzer system combining FTIR, laser spectroscopy, and gas chromatography technologies. The CCS 360 digital twin platform enables real-time simulation and optimization of carbon capture processes. The acquisition of Födisch Group strengthens ABB’s emissions monitoring capabilities for industrial sectors. Its ACF5000 FTIR system provides high-precision measurement of CO2 and trace gases in high-pressure environments. ABB’s turnkey solutions position it as a critical enabler of carbon management and industrial decarbonization.

Sartorius Expands Bioprocess Spectroscopy with Continuous Manufacturing and Cell Therapy Integration

Sartorius is strengthening its leadership in integrated bioprocessing through advanced spectroscopic PAT tools and infrastructure expansion. The company reported €3.5 billion in 2025 revenue with a strong EBITDA margin of 29.7%, driven by stable equipment demand and consumables growth. Its new Songdo mega-site in South Korea will serve as a hub for biopharma R&D and localized spectroscopy integration. The acquisition of MATTEK enhances capabilities in 3D tissue modeling combined with analytical monitoring. Sartorius is expanding applications in cell therapy manufacturing through real-time spectral monitoring of cell health. This positions the company as a key player in continuous bioprocessing and precision medicine analytics.

Agilent Accelerates Lab of the Future Vision with AI Diagnostics and Sustainable Spectroscopy Systems

Agilent Technologies is driving innovation in AI-integrated spectroscopy and sustainable laboratory systems under its “Lab of the Future” vision. The InfinityLab Pro iQ Series launched at ASMS 2025 delivers intelligent real-time feedback and meets MyGreenLab ACT EcoLabel 2.0 standards. The company generated $6.95 billion in 2025 revenue, with growth driven by GLP-1 therapeutics and metabolomics applications. Sustainability initiatives include certified refurbishment centers supporting circular economy models for analytical instruments. Agilent also introduced 21 CFR Part 11 compliant software to enhance data integrity in regulated environments. This strengthens its position in high-precision, compliant, and eco-efficient spectroscopy solutions.

Yokogawa Pioneers Industrial Autonomy with AI Spectral Agents and Advanced Infrared Sensing

Yokogawa Electric is advancing industrial autonomy through AI-powered spectroscopy and automation platforms. In October 2025, it deployed autonomous AI control agents in an Aramco facility to optimize gas processing using real-time spectral data. The AQ6377E Optical Spectrum Analyzer enables high-precision MWIR measurements for environmental and industrial applications. Its collaboration with Toyota on lunar rover development highlights expansion into advanced sensing technologies. The OpreX Plant Stewardship platform integrates spectroscopy into lifecycle optimization and decarbonization strategies. Yokogawa’s focus on AI-driven control systems positions it as a leader in autonomous industrial operations and energy efficiency.

United States: Miniaturization, Bioprocess Control, and Infrastructure-Linked Demand

The United States process spectroscopy industry is advancing through targeted R&D expansion, biopharmaceutical process control, and infrastructure-led instrumentation demand. In late 2025, leading instrument manufacturers such as Agilent and Thermo Fisher Scientific increased domestic R&D expenditure by an estimated 3 to 5%, prioritizing the miniaturization of GC-MS and LC-MS platforms. This push reflects growing requirements for mobile pharmaceutical testing, on-site environmental monitoring, and decentralized quality control. In parallel, Thermo Fisher expanded its Bioprocess Design Centers in December 2025, integrating chemically defined media development with real-time spectroscopic monitoring to support continuous biomanufacturing and process analytical technology adoption.

Instrumentation performance benchmarks are reinforcing U.S. leadership. At the 73rd ASMS conference in mid-2025, U.S. firms introduced the InfinityLab Pro iQ Series, setting new reference points for intelligent mass detection up to m/z 3,000 for peptides and oligonucleotides. Beyond life sciences, infrastructure electrification is shaping demand. In September 2025, ABB committed an additional $110 million to U.S. manufacturing across Virginia, Puerto Rico, and Mississippi, increasing the installed base of dielectric and transformer oil spectroscopy used in grid reliability and data center operations. Adoption is also broadening in agriculture, with the USDA’s 2025 report noting a 5% rise in non-citrus fruit production, accelerating the deployment of NIR spectroscopy for non-destructive quality sorting in high-throughput packing facilities.

Germany: Research-Driven Precision and Industry 4.0 Integration

Germany’s process spectroscopy market is characterized by deep academic-industrial collaboration, battery research leadership, and standardized digitalization across chemical parks. In December 2025, the Max Planck Institute for Solid-State Research in Stuttgart procured an aggregate $25 million suite of high-field magnetic resonance systems from Bruker, including 800 MHz and 100 MHz NMR platforms, to support in operando battery materials research. This investment highlights Germany’s emphasis on spectroscopy as a core tool for understanding degradation mechanisms in next-generation energy storage systems.

Industrial deployment is aligning with the Industry 4.0 roadmap. German chemical clusters have standardized the use of vacuum FTIR systems to eliminate atmospheric interference during catalytic investigations, improving reproducibility in continuous processing environments. Sustainability is also influencing procurement decisions. In 2025, German spectroscopy manufacturers achieved MyGreenLab ACT EcoLabel 2.0 certification for new platforms by incorporating oil-free pumping technologies and lowering energy consumption. These developments position Germany as a reference market for high-precision, low-footprint process spectroscopy solutions.

China: Domestic Instrumentation, AI Control, and Digital Manufacturing

China’s process spectroscopy landscape is being reshaped by industrial modernization policies, AI-enabled process control, and digital transformation in pharmaceuticals and agriculture. Under the 2025–2026 MIIT Work Plan, the government prioritized domestic development of high-end optical spectrum analyzers for 5G and emerging 6G network testing, reducing reliance on imported instrumentation. This policy support is accelerating local innovation in optical and vibrational spectroscopy platforms tailored for high-frequency communications and advanced materials.

Operational efficiency gains are increasingly data-driven. In October 2025, autonomous AI control agents commissioned by Yokogawa in partnership with Aramco demonstrated the use of real-time spectroscopy data to reduce chemical consumption and energy use in large-scale gas processing operations linked to China and the Middle East. The pharmaceutical sector is also advancing digitally. The rollout of cloud-based OpreX Quality Management Systems in early 2025 enabled automated quality assurance for both traditional and modern medicines, embedding spectroscopy into end-to-end digital manufacturing workflows. In agriculture, precision mandates under the Made in China 2025 final phase are driving investment in wireless sensor spectroscopy to improve labor productivity and reduce water use by 35%.

Switzerland: Inspection-Led Growth and Localization Strategy

Switzerland remains a high-value hub for process spectroscopy, driven by inspection technologies, sustained R&D intensity, and adaptive supply chain strategies. In response to a 39% U.S. import tariff on Swiss-made goods, Mettler-Toledo revised its 2025 outlook and accelerated localized assembly of process analytics components in North America. This shift is designed to preserve competitiveness while maintaining Swiss-led innovation in core spectroscopic modules.

Despite broader economic headwinds, Switzerland’s product inspection segment recorded 8% growth in Q2 2025, supported by the integration of spectroscopy into high-speed food and pharmaceutical packaging lines. R&D commitment remains robust, with Swiss firms sustaining quarterly research expenditure of approximately $49.3 million throughout 2025, focusing on Raman model development for high-throughput process optimization. Switzerland’s role is therefore anchored in premium inspection solutions and advanced analytical modeling.

Japan: Sensitivity Enhancement and Optical Measurement Leadership

Japan’s process spectroscopy market is advancing through sensitivity-driven mass detection and breakthroughs in optical spectrum analysis. In mid-2025, Japanese analytical and electronics firms introduced next-generation LC-mass detection platforms, including the InfinityLab Pro iQ Series, leveraging advanced jet stream ionization to enhance biomolecule sensitivity. These systems are being positioned for pharmaceutical R&D, biologics characterization, and high-value analytical workflows.

Optical spectroscopy is another area of strength. In January 2025, Japanese manufacturers launched the AQ6377E Optical Spectrum Analyzer, engineered for rapid and accurate mid-wave infrared measurements in demanding industrial environments. This instrument supports applications ranging from semiconductor manufacturing to advanced materials processing, reinforcing Japan’s reputation for precision optical and infrared spectroscopy solutions.

Summary of Country-Level Dynamics in the Process Spectroscopy Industry

Process Spectroscopy Market County Level Snapshot

|

Country

|

Strategic Emphasis

|

Process Spectroscopy Impact

|

|

United States

|

Miniaturization, bioprocess monitoring, grid infrastructure

|

Growth in mobile MS, NIR, and dielectric fluid spectroscopy

|

|

Germany

|

Academic-industry research, Industry 4.0

|

High-field NMR, EPR, and vacuum FTIR standardization

|

|

China

|

Domestic instruments, AI control, digital pharma

|

Expansion of optical analyzers and real-time process analytics

|

|

Switzerland

|

Inspection systems, localization

|

Strong demand for inline spectroscopy and Raman modeling

|

|

Japan

|

Sensitivity and optical precision

|

Leadership in LC-MS detection and MWIR spectrum analysis

|

Process Spectroscopy Market Report Scope

Process Spectroscopy Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$22.5 Billion

|

|

Market Size (2034)

|

$42.8 Billion

|

|

Market Growth Rate

|

7.4%

|

|

Segments

|

By Technology (Molecular Spectroscopy, Atomic Spectroscopy, Mass Spectrometry), By Component (Hardware, Software, Services), By Application (Real-Time Monitoring, Quality Control & Quality Assurance, Process Optimization, Safety & Compliance), By End-User Industry (Pharmaceuticals & Biotechnology, Food & Beverage, Oil & Gas & Petrochemicals, Chemicals & Materials, Environmental & Utilities)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Thermo Fisher Scientific Inc., Bruker Corporation, Agilent Technologies Inc., ABB Ltd., Yokogawa Electric Corporation, Mettler-Toledo International Inc., Sartorius AG, Danaher Corporation, Shimadzu Corporation, Waters Corporation, PerkinElmer Inc., Endress+Hauser Group, Horiba Ltd., Buchi Labortechnik AG, Metrohm AG

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Process Spectroscopy Market Segmentation

By Technology

- Molecular Spectroscopy

- Atomic Spectroscopy

- Mass Spectrometry

By Component

- Hardware

- Software

- Services

By Application

- Real-Time Monitoring

- Quality Control & Quality Assurance

- Process Optimization

- Safety & Compliance

By End-User Industry

- Pharmaceuticals & Biotechnology

- Food & Beverage

- Oil & Gas & Petrochemicals

- Chemicals & Materials

- Environmental & Utilities

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Process Spectroscopy Industry

- Thermo Fisher Scientific Inc.

- Bruker Corporation

- Agilent Technologies Inc.

- ABB Ltd.

- Yokogawa Electric Corporation

- Mettler-Toledo International Inc.

- Sartorius AG

- Danaher Corporation

- Shimadzu Corporation

- Waters Corporation

- PerkinElmer Inc.

- Endress+Hauser Group

- Horiba Ltd.

- Buchi Labortechnik AG

- Metrohm AG

*- List not Exhaustive