Rail Coatings Market Size, Rolling Stock Demand, and Infrastructure Modernization

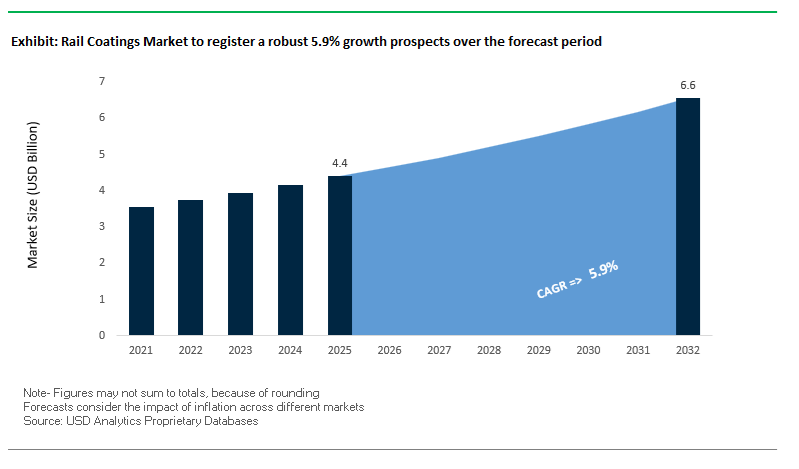

The global Rail Coatings Market was valued at $4.4 billion in 2025 and is projected to grow at a CAGR of 5.9% through 2032, reaching $6.6 billion by 2032. Growth is supported by increasing investments in rail infrastructure, freight modernization, and high-speed rail networks, where coatings play a critical role in corrosion protection, durability, and lifecycle cost reduction.

Rail coatings are applied across rolling stock (passenger and freight cars), locomotives, rail bridges, tracks, and station infrastructure, providing protection against abrasion, UV radiation, moisture, chemicals, and mechanical wear. Given the long service life expectations—often exceeding 20–30 years—coating systems must deliver high-performance adhesion, weatherability, and resistance to extreme operational conditions.

A key structural driver is the global push toward sustainable and efficient transportation systems, with governments investing heavily in rail to reduce carbon emissions and urban congestion. This is particularly evident in Europe, Asia-Pacific, and the Middle East, where new rail corridors, metro systems, and freight upgrades are driving demand for advanced coating solutions.

Additionally, the shift toward predictive maintenance and asset lifecycle optimization is increasing the importance of coatings that not only protect but also enable real-time performance monitoring. Sustainability is also influencing material selection, with rising demand for low-VOC, waterborne, and high-solids coatings that comply with stringent environmental regulations.

Market Analysis: Waterborne Rail Coatings, Smart Monitoring Systems, and High-Durability Technologies Driving Market Evolution

Recent developments in the Rail Coatings Market highlight a strong transition toward sustainable formulations, digital integration, and high-performance durability technologies. In September 2025, Sherwin-Williams introduced the CarClad® Water-Based platform, including primer and topcoat systems designed for rail cars. These coatings deliver 15–20 years of service life while significantly reducing VOC emissions, positioning waterborne technologies as a viable alternative to traditional solvent-based epoxies.

Performance-driven innovation is also shaping infrastructure applications. PPG’s CORAFLON® Platinum coatings—based on FEVE fluoropolymer technology—have demonstrated minimal color degradation (around 6% over five years), making them highly suitable for rail stations and exposed assets in high-UV and polluted environments.

Digitalization is emerging as a key differentiator. Jotun’s Smart Coating Technologies (January 2026) incorporate reactive or sensor-enabled layers that allow operators to detect corrosion and coating degradation in real time. This supports predictive maintenance strategies, reducing downtime and improving operational efficiency across rail networks.

Environmental compliance is driving formulation changes. Jotun’s ultra-low VOC epoxy coatings (November 2025) enable rail manufacturers to meet tightening environmental standards while maintaining high-build protection and faster drying times, improving productivity in manufacturing facilities.

Strategic consolidation and portfolio expansion are strengthening competitive positioning. Kansai Helios’ integration of the Weilburger Railway division enhances its role as a system supplier in Europe, offering both liquid and powder coating solutions for rail applications. Meanwhile, Hempel’s “Accelerate to Win” strategy emphasizes corrosion-resistant coatings for rail infrastructure, aligning with broader industrial growth initiatives.

Innovation in aesthetics and functionality is also gaining traction. BASF’s “Driving the Proxy” collection introduces advanced pigment technologies for rail coatings, enabling high-end visual finishes while maintaining the durability required for high-speed rail exteriors.

Investment realignment is further shaping the market. AkzoNobel’s divestment of its Indian subsidiary (February 2026) provides capital to modernize its rail coating production capabilities in Europe and North America, supporting compliance with upcoming sustainability mandates.

Market Trend: EN 45545-2 HL3 Fire Safety Compliance Driving Shift to Phenolic Epoxy and Intumescent Coatings

The rail coatings market in Europe is undergoing a fundamental material transition as EN 45545-2 fire safety standards reach full enforcement across all rolling stock categories, including metros and light rail systems. The requirement to meet Hazard Level 3 performance benchmarks is forcing coating manufacturers and OEMs to replace conventional polyester systems with phenolic epoxy and modified epoxy coatings engineered for fire resistance and low smoke toxicity.

Under HL3 classification for interior applications, coatings must meet strict smoke toxicity thresholds, with a Conventional Index of Toxicity below 0.75. This requirement has accelerated the phase-out of halogenated flame retardants due to their contribution to toxic gas emissions during combustion. In response, manufacturers are deploying advanced intumescent phenolic epoxy systems that expand under heat exposure, forming a protective char layer that limits smoke generation and toxic emissions.

Heat release performance is another critical parameter. Coatings must achieve a Maximum Average Rate of Heat Emission below 60 kW per square meter under ISO 5660-1 cone calorimeter testing. Achieving this level of performance requires precise formulation control and the integration of specialized fire-retardant additives. While these advanced coatings increase material costs by approximately 15% to 20%, they are becoming essential for participation in European rail tenders, where non-compliance results in immediate disqualification.

This regulatory shift is driving innovation in fire-resistant coating chemistries and creating a clear segmentation between compliant and non-compliant suppliers. Manufacturers that can meet HL3 benchmarks are gaining preferential positioning in high-value rail infrastructure projects across Europe.

Market Trend: High-Visibility Coatings Enhancing Machine Vision and PTC Integration in North American Freight Rail

In North America, rail coatings are evolving beyond passive visibility solutions toward active integration with automated monitoring and control systems. Regulatory frameworks from the Federal Railroad Administration, combined with the increasing deployment of Positive Train Control systems, are driving the development of high-visibility integrated coatings designed to enhance machine vision capabilities.

Traditional retroreflective decals used on freight cars are being replaced or supplemented by advanced coating systems that maintain high reflectivity over extended service periods. Modern formulations are engineered to retain approximately 80% of their initial retroreflectivity after five years of UV exposure, compared to around 50% retention for standard decal systems. This significantly reduces the occurrence of low-visibility or “dark car” incidents in automated rail yards.

In addition to human visibility, coatings are now being optimized for compatibility with lidar and other sensing technologies used in automated inspection systems. New high-visibility coatings are designed to achieve contrast ratios of at least 3:1 against ballast and natural backgrounds, improving detection accuracy for railcar-mounted sensors and trackside monitoring systems.

This convergence of coatings technology and digital rail infrastructure is creating a new category of functional coatings that contribute directly to operational safety and automation efficiency. As rail networks continue to modernize, demand for machine-vision-compatible coatings is expected to increase across freight and passenger segments.

Market Opportunity: Graphene-Reinforced Polyurea Coatings Extending Service Life of Hopper Car Liners

The integration of graphene nanoplatelets into polyurea coatings represents a significant opportunity in the rail freight segment, particularly for hopper car liners exposed to abrasive and corrosive materials such as coal, potash, and minerals. These advanced coatings address long-standing challenges related to wear resistance, adhesion, and permeability.

Incorporating approximately 0.5% graphene nanoplatelets by weight has been shown to reduce Taber abrasion loss by around 40% over 1,000 cycles. This enhancement effectively doubles the service life of hopper car liners before mechanical breakthrough occurs, reducing maintenance frequency and improving asset utilization for rail operators.

Barrier performance is also significantly improved. Graphene-enhanced polyurea coatings demonstrate a 70% reduction in water vapor transmission rates, providing superior protection against moisture ingress and corrosion of the underlying steel structure. This is particularly important in regions with high humidity or frequent precipitation, where corrosion risks are elevated.

The combination of mechanical durability and enhanced barrier properties positions graphene-reinforced polyurea as a next-generation solution for heavy-duty rail applications. Adoption is expected to increase as operators seek to reduce lifecycle costs and improve reliability in bulk material transport.

Market Opportunity: Low-Temperature Cure Polysiloxane Coatings Expanding Maintenance Windows in Cold Climate Rail Networks

Low-temperature cure polysiloxane coatings are creating a substantial opportunity in rail infrastructure maintenance, particularly in cold climate regions such as Canada and Northern Europe. These coatings are engineered to cure at temperatures where conventional polyurethane systems fail, enabling year-round maintenance operations.

Modern LTC polysiloxane systems can be applied at temperatures as low as −5°C, extending the maintenance window by approximately 45 to 60 days annually in regions with prolonged winter conditions. This increased flexibility allows rail operators to optimize maintenance schedules and reduce backlog accumulation during warmer months.

Energy efficiency is a key advantage. By eliminating the need for heated curing enclosures or temporary shelters, operators can reduce energy consumption by approximately 30% per railcar during refurbishment processes. This contributes to both cost savings and environmental sustainability goals.

From a regulatory perspective, these coatings also align with environmental standards such as those enforced under the Canadian Environmental Protection Act. High-solids polysiloxane formulations typically maintain VOC levels below 250 g/L while delivering superior gloss retention and long-term weatherability associated with inorganic coating systems.

The ability to combine low-temperature application, high durability, and environmental compliance positions LTC polysiloxane coatings as a critical enabler for efficient rail maintenance in challenging climatic conditions.

Rail Coatings Market Share and Segmentation Insights: Refurbishment Cycle Dominance and Direct Procurement Strategies

By Life Cycle: Refurbishment Segment Leads Driven by Long Asset Lifespan and Maintenance Demand

The refurbishment segment dominated the rail coatings market with a 58.9% share in 2025, primarily driven by the extended lifecycle of rolling stock and recurring maintenance requirements. Rail assets such as locomotives, passenger coaches, and freight wagons typically operate for 25–40 years, necessitating multiple repainting cycles every 5–10 years to maintain corrosion protection, aesthetic livery standards, and regulatory compliance. This recurring demand significantly boosts the consumption of high-performance rail coatings, including anti-corrosion primers and durable topcoats. Additionally, the presence of aging rail fleets across developed regions such as Europe, North America, and Japan has intensified refurbishment activities, often surpassing new OEM demand. As governments prioritize cost-effective asset life extension and rail infrastructure modernization, refurbishment coatings continue to represent the largest volume segment, reinforcing their critical role in the global rail coatings market.

By Sales Channel: Direct Sales Channel Dominates with Specification Compliance and Long-Term Contracts

The direct sales segment accounted for a leading 46.8% share of the rail coatings market in 2025, reflecting the importance of technical compliance and direct supplier relationships in railway coating procurement. Rail coatings must meet stringent standards such as EN 45545 for fire safety, along with requirements for low-VOC emissions, corrosion resistance, and anti-graffiti performance, making direct engagement with manufacturers essential for ensuring full certification, documentation, and warranty support. Major rail operators, including Amtrak, SNCF, Deutsche Bahn, and Indian Railways, typically procure coatings through multi-year framework agreements directly with coating manufacturers, enabling consistent supply, competitive pricing, and tailored product specifications. This direct procurement model also supports large fleet maintenance programs and standardized coating systems across rail networks. As demand grows for high-performance, regulation-compliant rail coatings, the direct sales channel continues to play a pivotal role in market expansion and operational efficiency.

Competitive Landscape of the Rail Coatings Market

PPG Leads Market with Digital Innovation and High-Performance Rail Coating Systems

PPG Industries, Inc. remains the technological vanguard of the rail coatings market, supported by strong financial performance and advanced R&D capabilities. In Q1 2026, the company reported a 7% revenue increase to $3.93 billion, with its Performance Coatings segment achieving a 16% margin. Its PPG LINQ™ platform integrates AI-driven color matching and cloud-based asset tracking, reducing material waste by up to 25% in locomotive refinishing projects. The SIGMAGLIDE® and SIGMASHIELD® product lines are industry benchmarks for underframe protection, offering resistance to ballast impact and de-icing chemicals. PPG is also developing UV-curable rail primers, enabling instant-dry repairs and reducing downtime by up to 30%.

AkzoNobel Strengthens Market Position with Sustainable Coatings and Hydrogen-Based Technologies

AkzoNobel N.V. is a major player in the rail coatings market, leveraging its Industrial Excellence strategy and global product portfolio. The company reported a 14.5% EBITDA margin in Q1 2026 and is progressing toward a strategic merger with Axalta. Its innovations include hydrogen-powered spray booth technology, enabling zero-emission coating applications for next-generation trains. The Interpon® D series incorporates bio-attributed resins, reducing the carbon footprint of rail infrastructure by 20%. These initiatives position AkzoNobel as a leader in sustainable and high-performance rail coatings.

Axalta Drives High-Speed Rail Innovation with Advanced Coating and Digital Application Technologies

Axalta Coating Systems is a key innovator in the rail coatings market, particularly in high-speed rail (HSR) applications. Its Imron® coatings are widely used for rail exteriors, offering high gloss retention and resistance to aerodynamic stress at speeds above 350 km/h. The company’s NextJet technology enables digital, non-atomized coating application, eliminating overspray and allowing precise branding without masking. Axalta’s designation as a preferred supplier for global OEMs such as Alstom and CRRC strengthens its position in international rail projects.

Hempel Leads Sustainability and Digital Monitoring with Advanced Rail Coating Systems

Hempel A/S is a leader in the rail coatings market, focusing on sustainability and lifecycle optimization. Its Hempadur and Hempafire coatings provide anti-corrosion and passive fire protection for rail infrastructure, including tunnels and metro systems. The company has achieved significant environmental impact, helping customers reduce CO₂ emissions through optimized coating systems. Its “Digital Twin” initiative introduces embedded microsensors that monitor coating health in real time, potentially extending recoating intervals by up to 40%.

Jotun Expands Regional Leadership with High-Durability and Anti-Graffiti Coating Technologies

Jotun Group is a dominant player in the rail coatings market, particularly in the Middle East and Asia-Pacific regions. The company reported record revenues driven by strong infrastructure growth. Its Jotacote Universal S120 primer is widely used for freight rail applications, providing high-build protection in a single coat. Jotun also leads in anti-graffiti coatings, offering polysiloxane topcoats that allow easy cleaning without damaging surfaces. Its expansion in Southeast Asia supports growing demand for metro and high-speed rail systems.

Nippon Paint Expands APAC Leadership with Energy-Efficient and High-Performance Rail Coatings

Nippon Paint Holdings Co., Ltd. is a major player in the rail coatings market, leveraging its strong presence in Asia. The company reported significant revenue growth, supported by recovery in passenger rail demand. Its innovations include solar-reflective coatings that reduce rail surface temperatures by up to 15°C, improving efficiency and durability. Nippon Paint’s integration with regional supply chains ensures cost-effective production of polyurethane coatings, while its focus on Southeast Asia’s expanding rail market positions it for sustained growth.

China’s High-Speed Rail Coatings Innovation Driving Ultra-Low VOC and Smart Infrastructure Growth

China continues to dominate the global rail coatings market with its massive high-speed rail network and rapid shift toward intelligent, low-VOC coating technologies. The development of ultra-low drag coatings for CR450 bullet trains (2025–2026) is a major breakthrough, enhancing aerodynamic performance and reducing energy consumption—key priorities in next-generation rail systems.

Regulatory updates in 2025 are accelerating the transition toward aqueous PVDC dispersions and solvent-free powder coatings, reinforcing China’s commitment to environmentally sustainable rail infrastructure. The integration of smart coatings embedded with microsensors enables real-time monitoring of corrosion and structural fatigue, marking a significant leap in predictive maintenance. Furthermore, large-scale investments in R&D hubs in Shanghai are advancing UV-resistant and noise-reduction coatings, while robotic spray technologies are improving application precision and reducing material waste. Innovations such as FEVE powder coatings with 30+ years durability are strengthening China’s leadership in long-life rail infrastructure solutions.

India’s Rail Coatings Market Expansion Fueled by Infrastructure Modernization and Safety Regulations

India is emerging as one of the fastest-growing markets in railway coatings, driven by extensive infrastructure expansion and modernization initiatives. The National Rail Plan 2030 is pushing the adoption of high-performance corrosion-resistant coatings, including zinc silicate and epoxy systems, across new track and bridge infrastructure.

Safety remains a key focus, with mandatory implementation of fire-retardant interior coatings for LHB coaches introduced in 2025. The rapid expansion of metro rail networks—spanning over 1,000 km—has significantly increased demand for anti-graffiti and easy-clean coatings. Domestic manufacturing is also strengthening, with companies like Berger and Asian Paints investing in automated coating lines under the “Make in India” initiative. Technological innovations such as solar-reflective coatings reducing coach temperatures by up to 5°C and anti-carbonation coatings for coastal railway bridges are further driving adoption of advanced rail coating solutions across the country.

Germany’s Leadership in Digital Rail Coatings and Sustainable High-Solid Systems

Germany is at the forefront of integrating digitalization and sustainability in rail coatings, aligning with its Industry 4.0 strategy. The adoption of self-healing coatings with microcapsule technology is revolutionizing maintenance by automatically repairing micro-cracks, significantly extending asset lifespan.

Digital transformation is evident through the implementation of data-driven coating lifecycle management systems, enabling predictive maintenance for rail fleets such as Deutsche Bahn. Sustainability initiatives have accelerated the shift toward Ultra-High-Solid (UHS) coatings, reducing solvent emissions while maintaining performance. Germany is also advancing antimicrobial coatings for passenger interiors, reflecting increased hygiene awareness. The use of UV-curable coatings for metal components and station interiors enables rapid processing with minimal energy use, while strategic acquisitions are consolidating the country’s position in high-precision rail coating technologies.

United States Rail Coatings Market Driven by Regulatory Compliance and Freight Sector Resilience

The United States rail coatings industry is undergoing transformation driven by stringent environmental regulations and the growing demand for durable freight infrastructure. The EPA’s PFAS-free mandates (2025–2026) are prompting a shift toward bio-based and alternative resin systems, redefining coating formulations across the market.

Infrastructure investments under the Infrastructure Investment and Jobs Act (IIJA) are supporting large-scale refurbishment of rail bridges using moisture-cured urethane primers, enhancing corrosion resistance. The freight rail segment is expanding rapidly, increasing demand for polyurethane and epoxy coatings designed for heavy-duty applications. Technological advancements include the use of robotic coating applicators for electric locomotives, improving efficiency and consistency. Additionally, innovations such as graffiti-resistant clearcoats and supply chain regionalization efforts are strengthening the resilience and sustainability of the US rail coatings market.

Saudi Arabia’s Rail Coatings Market Growth Accelerated by Mega Infrastructure Projects

Saudi Arabia is rapidly emerging as a key market for high-performance rail coatings, driven by ambitious infrastructure projects under Vision 2030. Projects such as NEOM’s “The Line” and the Saudi Landbridge are generating substantial demand for sand-abrasion-resistant coatings capable of withstanding extreme desert conditions.

Government initiatives are promoting the adoption of low-VOC coatings aligned with sustainability goals like the Green Riyadh program. Technological innovations include solar-reflective coatings that reduce rail temperatures by up to 15°C, preventing track deformation. The country is also witnessing expansion in local manufacturing capacity, particularly in acrylic and epoxy coatings. Key applications include fusion-bonded epoxy (FBE) coatings for underground tunnels and fluoropolymer coatings for high-speed rail systems, ensuring durability in harsh environmental conditions.

Indonesia’s High-Speed Rail Expansion Driving Demand for Advanced Protective Coatings

Indonesia is positioning itself as a regional leader in rail coatings, supported by large-scale investments in high-speed rail infrastructure. The Jakarta-Bandung high-speed rail project alone utilized over 1.2 million liters of protective coatings, highlighting the scale of demand in the country.

With over $42 billion allocated for rail development through 2026, Indonesia is focusing on expanding its network beyond 3,500 km. Technological advancements in nanotechnology-based coatings are delivering up to 40% longer service life, making them ideal for tropical climates. The rapid expansion of metro systems is driving demand for anti-graffiti and self-cleaning coatings, while stricter enforcement of ASTM and ISO standards is improving quality benchmarks. Investments in local technical service centers are also addressing the growing need for skilled coating applicators, ensuring sustainable industry growth.

France’s Leadership in Sustainable and Bio-Based Rail Coating Innovations

France is leading the European rail coatings market with a strong emphasis on sustainability and bio-based innovation. Backed by EU funding initiatives, including a €37 billion sustainable transport fund, France is accelerating the development of next-generation coating technologies for rolling stock.

The launch of bio-based epoxy resins derived from industrial waste for TGV M trains represents a significant advancement in eco-friendly coatings. Technological innovations such as acoustic-dampening coatings are reducing noise pollution in urban rail systems, while large-scale infrastructure projects like the Grand Paris Express are utilizing ultra-durable powder coatings. Compliance with EU regulations, including microplastic reporting requirements, is driving the development of biodegradable protective films. Additionally, increasing adoption of waterborne polyurethane topcoats for high-gloss, scratch-resistant finishes is enhancing both aesthetics and durability in high-speed passenger trains.

Rail Coatings Market Report Scope

Rail Coatings Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$4.4 Billion

|

|

Market Size (2032)

|

$6.6 Billion

|

|

Market Growth Rate

|

5.9%

|

|

Segments

|

By Resin Type (Epoxy, Polyurethane, Acrylic, Polyester, Fluoropolymers, Specialty Hybrids), By Technology (Water-borne Coatings, Solvent-borne Coatings, Powder Coatings, UV-Cured Coatings), By Rolling Stock (Locomotives, Passenger Coaches, Freight Wagons), By Application Area (Exterior Coatings, Interior Coatings, Infrastructure), By Coating Layer (Primers, Fillers and Putties, Basecoats, Topcoats, Tank Linings), By Life Cycle (OEM, Refurbishment), By Functional Property (Anti-Corrosion, Anti-Graffiti and Easy-Clean, Fire Retardant, Abrasive and Stone-Chip Resistance, Solar Reflective, Anti-Microbial), By Sales Channel (Direct Sales, Specialty Railway Maintenance Distributors, EPC)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

PPG Industries, Inc., Akzo Nobel N.V., The Sherwin-Williams Company, Axalta Coating Systems Ltd., Kansai Paint Co., Ltd., Nippon Paint Holdings Co., Ltd., Hempel A/S, BASF SE, Jotun Group, RPM International Inc., WEILBURGER Coatings GmbH, Teknos Group, Mäder Group, Berger Paints India Limited, Beckers Group

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Rail Coatings Market Segmentation

By Resin Type

- Epoxy

- Polyurethane

- Acrylic

- Polyester

- Fluoropolymers

- Specialty Hybrids

By Technology

- Water-borne Coatings

- Solvent-borne Coatings

- Powder Coatings

- UV-Cured Coatings

By Rolling Stock

- Locomotives

- Passenger Coaches

- Freight Wagons

By Application Area

- Exterior Coatings

- Interior Coatings

- Infrastructure

By Coating Layer

- Primers

- Fillers and Putties

- Basecoats

- Topcoats

- Tank Linings

By Life Cycle

By Functional Property

- Anti-Corrosion

- Anti-Graffiti and Easy-Clean

- Fire Retardant

- Abrasive and Stone-Chip Resistance

- Solar Reflective

- Anti-Microbial

By Sales Channel

- Direct Sales

- Specialty Railway Maintenance Distributors

- EPC

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Rail Coatings Industry

- PPG Industries, Inc.

- Akzo Nobel N.V.

- The Sherwin-Williams Company

- Axalta Coating Systems Ltd.

- Kansai Paint Co., Ltd.

- Nippon Paint Holdings Co., Ltd.

- Hempel A/S

- BASF SE

- Jotun Group

- RPM International Inc.

- WEILBURGER Coatings GmbH

- Teknos Group

- Mader Group

- Berger Paints India Limited

- Beckers Group

*- List not Exhaustive