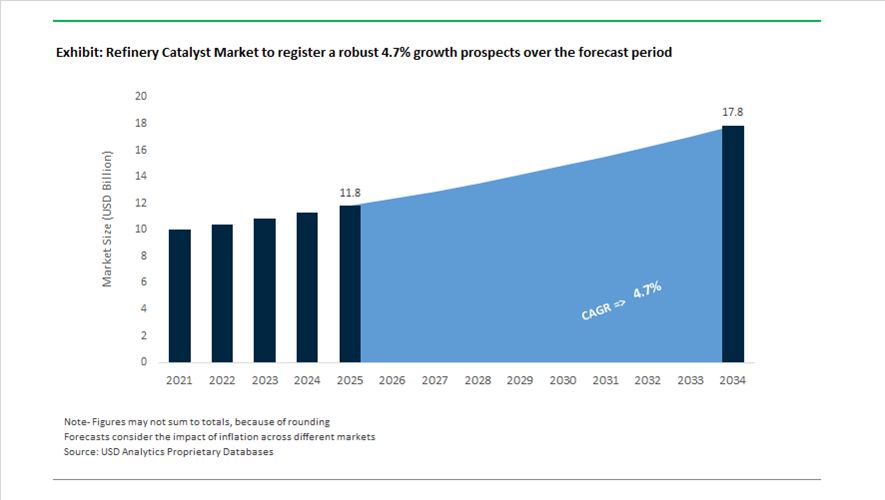

Refinery Catalyst Market Valued at $11.8 Billion in 2025, Projected to Reach $17.8 Billion by 2034 at 4.7% CAGR

The global refinery catalyst market is valued at $11.8 billion in 2025 and is projected to reach $17.8 billion by 2034, expanding at a CAGR of 4.7%. Growth is anchored in rising demand for hydroprocessing catalysts, fluid catalytic cracking (FCC) catalysts, hydrocracking systems, renewable diesel catalyst solutions, sustainable aviation fuel (SAF) catalysts, hydrogen reforming catalysts, and blue hydrogen process technologies. Refiners are investing in ultra-low-sulfur fuel production, feedstock flexibility, and refinery repurposing to support decarbonization and green fuel mandates. Catalyst performance optimization, AI-enabled process control, and geometry-enhanced catalyst structures are emerging as differentiating capabilities.

Strategic consolidation accelerated in 2025 and into 2026. In May 2025, Honeywell agreed to acquire Johnson Matthey’s Catalyst Technologies business for £1.8 billion, with closing expected in the first half of 2026. This transaction integrates Johnson Matthey’s blue hydrogen, ammonia, and SAF catalyst portfolio into Honeywell UOP’s refining and petrochemical solutions platform. In early 2025, W.R. Grace completed the acquisition of Advanced Refining Technologies (ART), strengthening its hydroprocessing catalyst leadership for ultra-low-sulfur diesel (ULSD) and renewable feedstock upgrading. In late 2025, Albemarle agreed to divest a controlling stake in Ketjen, its refining catalyst division, to KPS Capital Partners for approximately $660 million, with closing finalized in early 2026 to allow Albemarle to refocus on lithium operations.

Technology innovation is reshaping refinery economics. In August 2024, Grace introduced the Grace-IDP™ iron deactivation protocol to mitigate iron contamination in FCC units, enabling refiners to process heavier crude slates while maintaining catalyst activity and gasoline yield. In late 2024, ART launched the ENDEAVOR™ catalyst system engineered for hydroprocessing vegetable oils and waste fats into renewable diesel and jet fuel. In November 2024, BASF announced construction of its first industrial-scale X3D® 3D-printed catalyst plant in Ludwigshafen, confirming in December 2025 that the facility remains on schedule for Q1 2026 startup. These 3D-printed catalysts feature complex geometries that reduce pressure drop and increase accessible surface area, improving throughput and energy efficiency.

Green fuel and hydrogen catalyst investments intensified through 2025 and 2026. In September 2025, Clariant signed an agreement with SYPOX to supply catalysts for the world’s largest electric steam methane reformer, scheduled for 2026 operation, targeting up to 40% lower CO₂ emissions versus traditional reformers. In 2024, Montana Renewables converted idle hydrotreater capacity into the largest SAF production facility in the Western Hemisphere using Topsoe catalyst technology, demonstrating refinery repurposing viability. In January 2026, Topsoe secured a major agreement with Tangshan Jinlihai for SAF production in China and announced a leadership transition aligned with a 2026 strategy centered on industrializing Solid Oxide Electrolyzer Cell catalyst production for the hydrogen economy. Meanwhile, in 2024, Jubilant Ingrevia’s Bharuch facility was recognized by the World Economic Forum as a Global Lighthouse for deploying AI and real-time analytics in catalyst synthesis.

The refinery catalyst market is increasingly defined by hydroprocessing catalyst consolidation, FCC iron tolerance innovation, renewable diesel upgrading systems, SAF catalyst commercialization, 3D-printed catalyst geometries, electric steam methane reformer technology, hydrogen economy catalyst scaling, and AI-driven refinery optimization platforms. As refiners pivot toward lower-carbon fuels and feedstock flexibility, catalyst technology remains central to operational efficiency, regulatory compliance, and long-term energy transition strategy.

High-Impact Trends and Monetizable Opportunities in the Refinery Catalyst Market

Accelerated Shift Toward Hydroprocessing Catalysts for Bio-Feedstock Co-Processing

The refinery catalyst market is undergoing a structural transformation as refiners repurpose existing hydroprocessing units to co-process bio-based feedstocks alongside conventional fossil streams. This shift is no longer experimental. It is now a core decarbonization pathway driven by renewable fuel mandates, SAF blending targets, and carbon intensity reduction programs across North America, Europe, and Asia-Pacific.

By November 2025, the global investment pipeline for sustainable fuel hydroprocessing projects had reached approximately USD 50 billion, encompassing more than 250 active or planned facilities. Most of these projects are built around Hydroprocessed Esters and Fatty Acids technology, which requires advanced hydrotreating and hydrocracking catalysts capable of handling high oxygen content, metal contaminants, and variable triglyceride compositions. Nickel-molybdenum and palladium-based catalyst systems are increasingly specified due to their ability to deliver triglyceride conversion rates exceeding 97% while maintaining long cycle lengths under severe operating conditions.

Large-scale renewable refineries illustrate the catalyst intensity of this trend. High-capacity facilities processing multiple feedstocks such as used cooking oil, animal fats, and vegetable oils demand catalysts with superior resistance to phosphorus, alkali metals, and organic nitrogen. Catalyst replacement cycles, regeneration economics, and contaminant tolerance have become strategic decision variables rather than purely technical considerations. As refiners push bio-feedstock ratios higher, catalyst suppliers are capturing incremental value through customized formulations, pre-treatment catalyst packages, and performance-based service contracts.

Strategic Investment Surge in Catalytic Crude Oil-to-Chemicals Pathways

A second transformative trend in the refinery catalyst market is the pivot toward catalytic crude oil-to-chemicals configurations. With long-term transportation fuel demand plateauing, national oil companies and integrated refiners are restructuring assets to maximize petrochemical yield directly from crude barrels. Catalytic COTC technologies are emerging as a capital-efficient alternative to traditional refinery-petrochemical integration.

Megascale projects now under execution target direct conversion of 50 to 80% of crude feedstock into high-value chemicals such as ethylene, propylene, and aromatics. Fully integrated complexes designed to process around 400,000 barrels per day are expected to produce close to 9 million tons of chemicals and base oils annually once fully ramped up between 2025 and 2026. These configurations depend on highly specialized cracking, hydroprocessing, and aromatics catalysts that can operate under extreme severity while delivering unprecedented selectivity.

Compared with conventional refineries that typically yield only 10 to 15% petrochemicals, emerging catalytic routes are targeting chemical yields approaching 70%. This step-change in yield fundamentally alters catalyst demand patterns. Instead of optimizing for fuels stability and octane, refiners are prioritizing catalysts that maximize olefin production, manage coke formation, and maintain stability under ultra-high conversion conditions. The economic impact is material, with COTC deployment projected to contribute meaningfully to national GDP growth in producer economies by the end of the decade.

Specialized Upgrading Catalysts for Pyrolysis Oil Integration

Chemical recycling has created one of the fastest-growing opportunity segments for refinery catalyst suppliers. Pyrolysis oil derived from plastic waste contains high levels of oxygenates, chlorine, olefins, and unstable compounds that deactivate standard refinery catalysts. This has opened a premium market for foulant-resistant hydrotreating and hydrocracking catalysts designed specifically for circular feedstock upgrading.

By early 2024, at least sixteen pyrolysis units with capacities of 10 kilotons per annum were scheduled to come online in Europe through 2025, with similar momentum building in North America and Asia. This capacity expansion is part of a broader infrastructure push estimated at USD 100 billion globally to enable 20 to 30% recycled content in plastic packaging. Each of these projects requires tailored catalyst systems capable of hydrodeoxygenation, dechlorination, and olefin saturation without rapid deactivation.

From an economic standpoint, advances in catalytic depolymerization and upgrading are projected to reduce the average cost of chemical recycling by nearly 37.5% by 2040. Refiners integrating pyrolysis oil into existing units are increasingly relying on catalyst suppliers not only for materials but also for feedstock qualification, contaminant management strategies, and regeneration planning. This positions upgrading catalysts as a recurring, high-margin revenue stream rather than a one-time equipment input.

Propylene Maximization Through High-Zeolite FCC Catalyst Systems

The growing imbalance between propylene demand and gasoline consumption is reshaping FCC catalyst strategies worldwide. Refiners are increasingly transforming FCC units into petrochemical production assets by deploying high-zeolite catalyst systems and ZSM-5 additives engineered for maximum light olefin selectivity.

Roughly 35% of global propylene supply is already produced via FCC operations, and this share continues to rise, particularly in Asia-Pacific where new steam cracking capacity is capital intensive. Case studies from 2025 demonstrate that customized FCC catalyst formulations can improve propylene yields by more than 1.5 weight%, translating directly into substantial margin uplift given propylene’s premium pricing relative to transportation fuels.

Demand is accelerating for hierarchical H-ZSM-5 additives with tailored mesoporosity that enhance diffusion, suppress coke formation, and maintain hydrothermal stability under severe cracking conditions. These additives enable refiners to push conversion severity without sacrificing catalyst life, aligning FCC operations with downstream polypropylene and chemical integration strategies. For catalyst suppliers, propylene-focused FCC solutions represent a scalable opportunity with strong repeat demand driven by short catalyst replacement cycles and continuous formulation optimization.

Refinery Catalyst Market Share and Segmentation Insights

FCC Catalysts Lead Global Refinery Catalyst Consumption as Petrochemical-Oriented Refining Gains Momentum

FCC catalysts accounted for 42.80% of the refinery catalyst market in 2025, reflecting the central role of fluid catalytic cracking (FCC) units in modern refinery conversion processes. FCC technology converts heavy gas oils and vacuum gas oils into gasoline, LPG, and light olefins, making it one of the largest catalyst-consuming processes in refining operations. Continuous optimization of feedstock flexibility and product yield drives sustained demand for advanced zeolite-based FCC catalyst formulations. A critical 2025 industry shift is the increasing petrochemical integration within refining complexes, where FCC units are optimized to maximize propylene and butylene production for petrochemical feedstocks. This trend is accelerating the development of FCC catalysts designed for enhanced olefin selectivity while preserving gasoline yield and catalyst stability.

Gasoline Yield Optimization Drives Catalyst Demand Across Global Refinery Operations

Gasoline yield optimization remains the leading application in the refinery catalyst market, capturing 38.60% of global catalyst demand in 2025 due to the continued dominance of gasoline in global transportation fuel consumption. Refiners rely on advanced catalyst technologies in fluid catalytic cracking and catalytic reforming units to maximize high-octane gasoline output while meeting stringent fuel quality regulations. A major industry challenge in 2025 is octane preservation amid tightening aromatics and benzene regulations, which restrict traditional octane boosters such as reformate and alkylate streams. As a result, refiners increasingly depend on optimized FCC catalyst formulations with advanced zeolite structures and tailored matrix compositions that enhance octane generation while limiting undesirable aromatics formation in finished gasoline blends.

Refinery Catalyst Market Competitive Landscape

The 2026 refinery catalyst market is advancing toward high-severity FCC catalysts, hydroprocessing solutions, and renewable fuel co-processing technologies. Growth is driven by IMO fuel standards, ultra-low sulfur mandates, and increasing adoption of catalysts for SAF, renewable diesel, and crude-to-chemicals conversion.

Grace strengthens hydroprocessing leadership with full ART integration and FCC innovation for heavy feedstocks

W. R. Grace & Co. has consolidated its position in refinery catalysts through full ownership of the ART Hydroprocessing™ portfolio following Chevron JV acquisition. This integration strengthens capabilities in fixed and ebullated bed hydroprocessing catalysts for both conventional and renewable refining. The EnRich® catalyst portfolio is being scaled to support renewable diesel and sustainable aviation fuel production. PARAGON™ FCC catalyst technology improves iron tolerance and bottoms conversion, enabling processing of heavier, contaminated feedstocks. Strategic alignment with Chevron Lummus Global ensures early-stage integration of Grace catalysts in licensed refinery units. Focus on high-severity FCC and renewable co-processing enhances catalyst performance across evolving refinery configurations.

Honeywell UOP expands renewable catalyst dominance with major acquisition and integrated process technologies

Honeywell UOP is accelerating its refinery catalyst leadership through acquisition of Johnson Matthey’s Catalyst Technologies business for $1.7 billion, significantly expanding hydroprocessing and renewable fuel capabilities. The company operates over 50 licensed renewable units globally, focusing on conversion of waste feedstocks into SAF and renewable diesel. BDO-400 and BDO-500 deoxygenation catalysts have demonstrated operational success across multiple global installations. Integrated offerings combine catalysts, process technology, and equipment for refinery decarbonization and petrochemical integration. Focus on hydrogen and ammonia production supports transition to low-carbon refining. Strategic expansion strengthens position in energy transition and advanced refining solutions.

Albemarle optimizes refining catalyst exposure through Ketjen restructuring and high-activity catalyst focus

Albemarle Corporation is reshaping its refinery catalyst presence by divesting a 51% stake in its Ketjen business while retaining minority exposure to catalyst revenues. Ketjen reported $320 million in Q4 2025 sales with improved margins driven by favorable product mix and lower input costs. Strong capabilities in FCC and hydroprocessing catalysts support production of ultra-low sulfur diesel. EBITDA growth of 15% reflects continued demand for high-activity catalysts despite market volatility. Strategic restructuring allows Albemarle to prioritize lithium and energy storage investments. Continued involvement in refining catalysts maintains exposure to steady cash flow from established markets.

Topsoe advances low-carbon hydroprocessing catalysts with HyBRIM technology and global SAF expansion

Topsoe A/S is strengthening its refinery catalyst portfolio through intensive R&D investment focused on decarbonization and green hydrogen integration. The company invested DKK 753 million in 2025 to develop advanced catalyst technologies supporting over 100 process applications. The TK-580 HyBRIM™ catalyst enables ultra-low sulfur diesel production with sulfur levels below 10 ppm. Strategic agreements across Asia-Pacific support deployment of catalysts for sustainable aviation fuel production. Technologies such as PhosTrap™ and TK-series enable efficient hydrodeoxygenation in renewable fuel processes. Leadership transition in 2026 supports acceleration of Power-to-X and low-carbon fuel initiatives.

BASF enhances catalyst competitiveness through ECMS autonomy and circular catalyst lifecycle strategies

BASF SE is strengthening its refinery catalyst business through its Environmental Catalyst and Metal Solutions division operating under a differentiated governance model. The company projects €6.2–€7.0 billion EBITDA in 2026 while maintaining strong margins in its catalyst portfolio. Operational autonomy enables faster response to evolving refinery and emissions regulations. Integration with the Zhanjiang Verbund site supports regional supply of high-performance catalysts. Focus on catalyst recycling and metal reuse enhances sustainability and lifecycle efficiency. Strategic emphasis on circular economy principles aligns with decarbonization goals in refining and petrochemical industries.

Clariant drives olefin-focused catalyst growth with CATOFIN technology and global PDH expansion

Clariant is expanding its refinery catalyst footprint through strong demand for on-purpose olefin production technologies. The CATOFIN™ catalyst system continues to demonstrate high reliability in propane dehydrogenation, with successful restart of the Ningxia Runfeng PDH plant in 2025. The company reported a 17.8% EBITDA margin in 2025, supported by strong catalyst segment performance. Ongoing performance improvement programs target CHF 80 million in cost savings to sustain margin expansion. Global deployment includes over 45 projects adding more than 30 million tons of propylene capacity. Strong presence in China supports growth in petrochemical-integrated refining and olefin production markets.

United States: SAF-Centric Catalyst Scale-Up and Portfolio Realignment

The United States refinery catalyst landscape is being structurally reshaped by the rapid scaling of Sustainable Aviation Fuel and renewable diesel infrastructure, coupled with aggressive portfolio realignment by incumbent technology providers. In November 2025, NXTClean Fuels selected Topsoe as the technology licensor for the largest greenfield SAF project in the U.S., located in Oregon. The deployment of HydroFlex™ and H2bridge™ catalyst systems positions the facility to reach 50,000 barrels per day of renewable diesel and SAF by 2029, reinforcing the U.S. as a global testbed for next-generation hydroprocessing catalysts. Parallel to greenfield investments, refiners continued accelerating adoption of high-activity hydrotreating catalysts through 2025 to comply with EPA Tier 3 gasoline sulfur limits of 10 ppm, increasing demand for advanced guard beds and sulfur-tolerant formulations.

Strategic consolidation has further tightened the competitive landscape. In May 2025, Honeywell agreed to acquire Johnson Matthey’s Catalyst Technologies business for £1.8 billion, strengthening U.S. supply chains for blue hydrogen, ammonia, and lower-emission fuel catalysts. This was followed by W. R. Grace & Co. completing the acquisition of Chevron’s stake in Advanced Refining Technologies in November 2025, gaining full control of the EnRich® catalyst portfolio tailored for renewable diesel and SAF pretreatment. In parallel, Albemarle divested a 51% stake in its Ketjen business to KPS Capital Partners, enabling sharper focus on FCC and clean-fuel catalyst innovation. Beyond fuels, catalyst demand is also expanding into circularity, with Honeywell UOP and Avangard Innovative scaling UpCycle Process Technology in Texas to convert waste plastics into refinery-grade feedstocks using specialized catalytic systems.

Saudi Arabia: Localization and Crude-to-Chemicals Catalyst Demand

Saudi Arabia’s refinery catalyst market is increasingly defined by localization and Vision 2030-driven downstream integration. In April 2025, Axens completed the expansion of Axens Catalyst Arabia Limited in Dammam, establishing the Middle East’s first facility dedicated to Tail Gas Treatment Catalysts. With sulfur recovery efficiencies reaching 99.9%, this site directly supports stricter emissions control while reducing regional dependence on imports. By January 2026, localized production had already lowered catalyst import reliance by an estimated 15% for sulfur recovery units.

Catalyst demand is also being pulled by Aramco’s crude-to-chemicals strategy, which prioritizes heavy-duty FCC catalysts capable of bypassing traditional fuel pathways to maximize olefin yields. The new ACAL facility is supplying next-generation low-temperature catalysts that reduce refinery energy intensity and capital expenditure, particularly for gas processing and sulfur management units. These developments position Saudi Arabia as a regional hub for sulfur recovery and high-severity FCC catalyst deployment, aligned with long-term petrochemical integration objectives.

China: Antimony Substitution and Refining-to-Chemicals Acceleration

China’s refinery catalyst market is undergoing rapid adaptation to supply chain controls and state-led modernization mandates. Following antimony export restrictions implemented in 2024, domestic refiners and international suppliers pivoted toward titanium-based and antimony-free catalyst chemistries. Clariant announced major launches of such alternatives for 2026, ensuring continuity in FCC and hydrotreating operations amid constrained raw material access.

At the policy level, the Ministry of Industry and Information Technology’s 2025 petrochemical work plan has forced refiners toward high-end catalyst adoption, prioritizing LPG olefinicity and high-octane naphtha production. Large integrated sites in Zhejiang and Shandong have accelerated the deployment of advanced FCC catalysts to raise propylene yields in line with the government’s 5% annual petrochemical value-add growth target. Circularity is also emerging as a catalyst demand vector, highlighted by BASF commissioning its loopamid plant in Caojing in late 2025, using catalytic recycling to convert PA6 waste back into virgin-quality monomers.

Germany: Industrialized Innovation in Catalysts and Hydrogen

Germany remains the epicenter of high-complexity catalyst innovation, with commercialization timelines now replacing pilot-scale experimentation. BASF is on track to commission the world’s first commercial-scale 3D-printed catalyst plant in Ludwigshafen in Q1 2026. Using X3D technology, these catalysts feature engineered geometries that increase active surface area and reactor throughput, directly improving refinery unit economics. Earlier, BASF launched the Fourtiva FCC catalyst in August 2024, leveraging Advanced Innovative Matrix technology to boost butylene yields while reducing coke formation in European refineries.

Hydrogen-linked catalyst innovation is also advancing rapidly. In 2025, BASF and ExxonMobil signed a joint development agreement to scale methane pyrolysis, operating a demonstration unit capable of producing 2,000 tonnes per year of hydrogen with approximately 80% lower energy intensity than electrolysis. Complementing this, Topsoe received Catalyst Producer of the Year recognition at ERTC 2025 for its SiliconTrap™ and TK-3000 Series catalysts, which extend renewable fuel unit cycle life by 25 to 30%, reinforcing Germany and broader Europe as leaders in renewable feedstock catalyst systems.

Refinery Catalyst Industry: Country-Level Strategic Snapshot

Refinery Catalyst Market County Level Snapshot

|

Country / Region

|

Strategic Catalyst Focus

|

Structural Impact

|

|

United States

|

SAF, renewable diesel, plastic recycling catalysts

|

Greenfield projects, portfolio consolidation, circular feedstocks

|

|

Saudi Arabia

|

Sulfur recovery and C2C FCC catalysts

|

Import substitution, energy-efficient downstream integration

|

|

China

|

Antimony-free FCC, refining-to-chemicals catalysts

|

Supply chain resilience, higher olefin yields

|

|

Germany

|

3D-printed catalysts, hydrogen-linked systems

|

Industrialized innovation, renewable feedstock optimization

|

Refinery Catalyst Market Report Scope

Refinery Catalyst Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$11.8 Billion

|

|

Market Size (2034)

|

$17.8 Billion

|

|

Market Growth Rate

|

4.7%

|

|

Segments

|

By Type (FCC Catalysts, Hydroprocessing Catalysts, Catalytic Reforming Catalysts, Isomerization Catalysts, Alkylation Catalysts, Renewable & Bio-Feedstock Catalysts), By Material (Zeolites, Metals, Chemical Compounds), By Application (Gasoline Yield Optimization, Diesel Production, Sustainable Aviation Fuel Production, Olefins & Petrochemical Feedstocks, Sulfur Recovery & Emission Control)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Honeywell UOP, BASF SE, W. R. Grace & Co., Topsoe, Albemarle Corporation, Clariant AG, Axens SA, Shell Catalysts & Technologies, Johnson Matthey, Evonik Industries AG, Chevron Lummus Global, Sinopec Group, Nippon Ketjen Co. Ltd., Ami Organics, Criterion Catalysts & Technologies

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Refinery Catalyst Market Segmentation

By Type

- FCC Catalysts

- Hydroprocessing Catalysts

- Catalytic Reforming Catalysts

- Isomerization Catalysts

- Alkylation Catalysts

- Renewable & Bio-Feedstock Catalysts

By Material

- Zeolites

- Metals

- Chemical Compounds

By Application

- Gasoline Yield Optimization

- Diesel Production

- Sustainable Aviation Fuel Production

- Olefins & Petrochemical Feedstocks

- Sulfur Recovery & Emission Control

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Refinery Catalyst Industry

- Honeywell UOP

- BASF SE

- W. R. Grace & Co.

- Topsoe

- Albemarle Corporation

- Clariant AG

- Axens SA

- Shell Catalysts & Technologies

- Johnson Matthey

- Evonik Industries AG

- Chevron Lummus Global

- Sinopec Group

- Nippon Ketjen Co. Ltd.

- Ami Organics

- Criterion Catalysts & Technologies

*- List not Exhaustive