Refinish Paint Market Size, Collision Repair Demand, and Automotive Aftermarket Growth

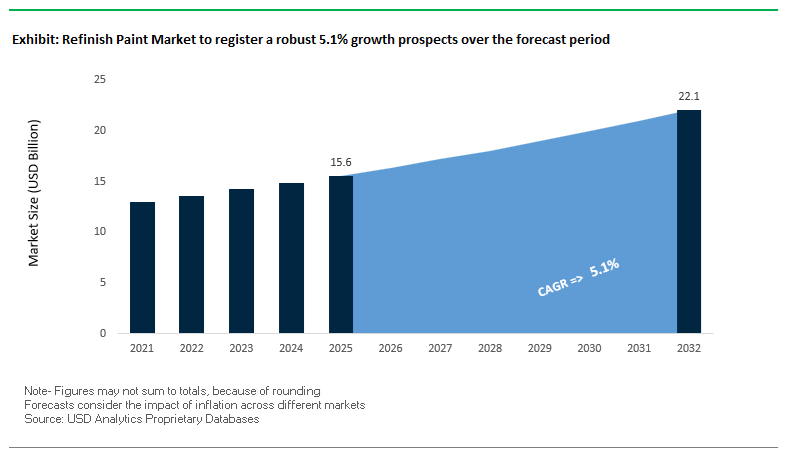

The global Refinish Paint Market was valued at $15.6 billion in 2025 and is projected to grow at a CAGR of 5.1% through 2032, reaching $22.1 billion by 2032. Growth is driven by expanding demand in the automotive aftermarket, particularly in collision repair, vehicle restoration, and cosmetic upgrades, where refinish coatings are essential for restoring appearance, corrosion protection, and OEM-level finish quality.

Refinish paints—including basecoats, clearcoats, primers, and specialty coatings—are engineered to replicate original factory finishes while meeting the operational requirements of body shops, such as fast curing, ease of application, and cost efficiency. The increasing complexity of automotive finishes, including metallic, pearlescent, and multi-layer coatings, is driving demand for advanced refinish systems capable of precise color matching and high durability.

A key structural driver is the steady increase in vehicle parc (total vehicles in use) globally, particularly in emerging markets where vehicle ownership is rising. Additionally, the aging vehicle fleet in developed markets is increasing the frequency of repair and repaint cycles, supporting consistent aftermarket demand.

Sustainability and regulatory compliance are also shaping the market. There is a strong shift toward waterborne basecoats, low-VOC clearcoats, and energy-efficient curing technologies, enabling body shops to reduce emissions while maintaining performance standards.

Market Analysis: Industry Consolidation, Ultra-Fast Curing Systems, and Digital Color Technologies Driving Market Evolution

Recent developments in the Refinish Paint Market highlight a convergence of industry consolidation, performance innovation, and digital transformation. The most significant structural shift is the $25 billion merger agreement between AkzoNobel and Axalta (April 2026), which consolidates leading refinish brands such as Sikkens®, Lesonal®, Spies Hecker®, and Standox® under one entity. This merger is expected to accelerate innovation in digital color matching, sustainable resin systems, and global distribution efficiency.

Performance innovation is focused on improving shop productivity. PPG’s DELTRON® NXT DC7020 clearcoat offers extremely fast curing (5 minutes at 60°C), significantly reducing cycle times and energy consumption in repair facilities. Additionally, PPG’s SC300 Series targets the value segment with fast-drying, VOC-compliant clearcoats, addressing the needs of high-volume repair shops.

Color technology is becoming increasingly sophisticated. BASF’s “Driving the Proxy” collection introduces next-generation interference pigments that bridge the gap between complex OEM finishes and refinish replication, enabling body shops to accurately reproduce “liquid metal” and multi-dimensional color effects.

Integration of protective solutions is expanding the scope of refinish systems. 3M’s self-healing paint protection films (PPF) and ceramic coatings are increasingly incorporated into refinish workflows, providing post-application protection against UV exposure and minor abrasions, effectively extending the lifecycle of refinished surfaces.

Digitalization is transforming application processes. SATA’s smart spray gun technology (2026) introduces real-time monitoring of pressure and temperature, enabling more consistent application quality and reducing rework through data-driven process control.

Regional expansion and operational efficiency are also shaping competitive dynamics. Sherwin-Williams reported strong growth in its automotive refinish segment (2025), while Jotun’s expansion into Southeast Asia and the Middle East focuses on localized formulations suited to high-humidity and high-temperature environments.

At the same time, AkzoNobel’s pre-merger restructuring (October 2025), including factory consolidations, reflects the industry’s push toward centralized, high-efficiency production models to maintain margins amid fluctuating demand.

EU REACH Chromate Restriction Accelerating Chrome-Free Automotive Refinish Primer Adoption Across EU-27

The tightening of chemical regulations under European Chemicals Agency (ECHA) and the European Commission is fundamentally reshaping the automotive refinish paint market, particularly in anti-corrosion primer technologies. The transition of Chromium (VI) substances from REACH authorization to full restriction under Annex XIV marks a decisive regulatory pivot toward chrome-free refinish coatings. With the December 2025 policy update and January 2026 Q&A clarifications, traditional authorization pathways for hexavalent chromium are being phased out, compelling bodyshops and coating manufacturers to adopt compliant alternatives. This regulatory shift is driving demand for chrome-free epoxy primers, phosphate-based corrosion inhibitors, and REACH-compliant refinish coatings, making regulatory compliance a central purchasing criterion across the EU automotive aftermarket.

The impact extends deep into the refinish coatings supply chain, as nearly 40 industrial applications of chromium trioxide are set to be eliminated ahead of the July 2026 compliance deadline. Leading manufacturers such as AkzoNobel and BASF are accelerating innovation in chrome-free primer surfacers that deliver equivalent corrosion protection, with salt spray resistance reaching up to 1,000 hours. This transition is catalyzing a broad reformulation cycle in automotive refinish products, driving R&D investments in high-performance, non-toxic coating chemistries and reinforcing the shift toward sustainable automotive refinishing solutions in Europe.

China’s GB 38508-2025 VOC Regulation Driving Rapid Transition to Waterborne and Ultra-High Solid Refinish Coatings

China’s evolving environmental regulatory framework is emerging as a major force in the global refinish paint market, particularly through the revision of GB 38508 standards targeting volatile organic compounds (VOCs). Spearheaded by the Ministry of Industry and Information Technology (MIIT), the March 2026 revision plan aims to eliminate regulatory loopholes and enforce stricter VOC emission limits across automotive refinish coatings, cleaners, and additives. This regulatory tightening is expected to significantly reduce allowable VOC content in ready-to-use refinish paints, accelerating the shift toward waterborne basecoats and ultra-high solid (UHS) coatings as the industry standard for compliance in China’s automotive aftermarket.

Regional enforcement trends are already demonstrating measurable market transformation. Cities such as Shenzhen and Shanghai have implemented stricter local VOC regulations, resulting in a 20–30% increase in waterborne basecoat adoption among large collision repair centers in 2025. This transition is not only reducing emissions but also reshaping procurement strategies, with refinish coating manufacturers prioritizing low-VOC formulations, high-solids content technologies, and eco-friendly automotive paints. As China continues to lead regulatory-driven demand, the market is witnessing accelerated innovation in sustainable refinish coatings, positioning Asia-Pacific as a high-growth hub for compliant coating technologies.

Low-Bake Clearcoat Technology Emerging as a Critical Enabler for Electric Vehicle Aluminum Refinish Applications

The rapid expansion of the electric vehicle (EV) fleet is creating a specialized demand segment within the automotive refinish coatings market, centered on low-temperature curing technologies. Traditional high-bake curing processes above 140°C are incompatible with EV architectures, as they risk damaging battery management systems and distorting lightweight aluminum panels. This has accelerated the development of low-bake clearcoats that cure at 70–85°C, aligning with the thermal safety thresholds of EV components while maintaining premium surface finish and durability. As EV adoption increases globally, this niche is evolving into a high-value growth avenue for advanced refinish coating systems.

From a sustainability and operational efficiency perspective, low-bake technologies offer compelling advantages. AkzoNobel has reported that next-generation systems such as Sikkens Autowave Optima reduce process times by up to 50% while lowering energy consumption and carbon emissions by approximately 60%. Simultaneously, BASF has expanded the production of Product Carbon Footprint (PCF)-optimized coatings using renewable electricity, aligning with OEM and aftermarket decarbonization targets. These innovations are reinforcing low-bake clearcoats as a strategic solution for EV refinish applications, particularly for aluminum-intensive vehicle structures in premium and next-generation mobility segments.

Waterborne Basecoat Systems Becoming the Default Standard for Low-VOC Automotive Refinish Compliance and Material Efficiency

Waterborne basecoat technology is transitioning from a regulatory alternative to the dominant standard in the global automotive refinish paint market, driven by tightening VOC regulations and increasing sustainability mandates. Advances in pigment dispersion and formulation chemistry have significantly enhanced material efficiency, with companies such as Axalta reporting that modern waterborne systems achieve full coverage in approximately 1.5 coats compared to three coats required for conventional solvent-borne paints. This translates into a 15% reduction in material consumption per repair, directly improving cost efficiency and throughput for collision repair centers while supporting compliance with low-VOC emission standards.

Market adoption trends reinforce the strategic importance of waterborne coatings, which now account for nearly 50% of revenue in the low-VOC automotive coatings segment as of early 2026. The Asia-Pacific region, particularly China and India, is driving this expansion due to increasingly stringent environmental regulations and rising vehicle parc density. Furthermore, the growing prevalence of complex automotive finishes such as metallics, pearls, and tinted clearcoats is favoring waterborne technologies, which offer superior flake orientation and color consistency. As a result, waterborne basecoat systems are not only enabling regulatory compliance but also enhancing aesthetic performance, positioning them as a cornerstone technology in next-generation automotive refinishing.

Refinish Paint Market Share and Segmentation Insights: Body Shop Dominance and High-Performance 2K Systems Driving Growth

By Sales Channel: Automotive Body Shops Lead with Collision Repair Demand and Professional Expertise

The automotive body shops segment dominated the refinish paint market with a 61.2% share in 2025, driven primarily by the high volume of collision repair and vehicle restoration activities. Accident-related repairs remain the largest demand generator for automotive refinish coatings, including color-matched basecoats, primers, and clearcoats, with independent and franchise repair networks such as Fix Auto and Carrosserie playing a central role. These facilities are equipped with advanced spray booths, controlled environments, and computerized color matching systems, ensuring precise application and OEM-quality finishes. The complexity of modern coating systems, including multi-layer basecoat/clearcoat technologies, requires trained technicians and certified equipment, significantly limiting the role of DIY applications. As vehicle parc continues to grow globally and insurance-backed repair volumes increase, professional body shops remain the backbone of the automotive refinish paint market, supported by rising demand for high-quality, durable, and aesthetically consistent automotive coatings.

By Component Configuration: Two-Component (2K) Systems Dominate with OEM-Grade Performance and Fast Cure Cycles

The two-component (2K) segment held a dominant 76.5% share of the refinish paint market in 2025, driven by its superior durability, chemical resistance, and fast curing performance. These systems, based on urethane chemistry with isocyanate hardeners, deliver excellent scratch resistance, UV stability, and solvent resistance, meeting stringent OEM-quality standards for automotive refinishing. 2K coatings are widely used for both clearcoats and basecoats, ensuring long-lasting finish quality and protection against environmental exposure. A key advantage is their rapid curing capability, with modern formulations capable of curing at ambient conditions or low-bake temperatures around 60°C, allowing body shops to complete repairs within hours instead of days. This significantly improves throughput, operational efficiency, and turnaround time for repair centers. The combination of high-performance coatings, faster repair cycles, and superior finish quality continues to reinforce the dominance of 2K systems in the global automotive refinish paint market.

Competitive Landscape of the Refinish Paint Market

Axalta Leads Market with AI-Driven Color Systems and Energy-Efficient Refinish Technologies

Axalta Coating Systems is the benchmark player in the refinish paint market, driven by strong financial performance and technological innovation. In 2025/26, the company achieved a record adjusted EBITDA of $1,128 million with a 22.0% margin. Its TintMaster AI™ platform enables real-time formulation adjustments, improving color accuracy by up to 29% for complex multi-layer coatings. Axalta is also advancing low-temperature curing systems, reducing energy consumption and CO₂ emissions in body shops. Its expansion of training academies in Asia-Pacific strengthens its ability to capture growth in emerging markets.

PPG Strengthens Market Leadership with Digital Ecosystems and Advanced Color Design

PPG Industries, Inc. is a key player in the refinish paint market, leveraging its strong R&D capabilities and digital ecosystem. Its PPG LINQ™ platform integrates automated mixing and spectrophotometer synchronization, reducing material waste by up to 30% and minimizing human error. The company’s “Parallels” design theme introduces advanced color technologies tailored for both EVs and traditional vehicles. PPG is also investing in UV-curable refinish coatings, enhancing curing speed and efficiency. Strategic collaborations with automotive manufacturers further reinforce its leadership in the global refinish market.

AkzoNobel Expands Global Presence with Sustainable Refinish Systems and AI Integration

AkzoNobel N.V. is a major competitor in the refinish paint market, leveraging its Sikkens® and Lesonal® brands. The company has improved profitability through pricing strategies and continues to expand globally. Its innovations include AI-driven inspection technologies that detect coating defects and corrosion, improving maintenance efficiency. AkzoNobel is also focusing on bio-attributed resins in basecoat formulations, reducing environmental impact. Its investment in advanced manufacturing facilities supports growing demand for high-performance refinish coatings.

BASF Leads Aesthetic Innovation with Advanced Pigment Technologies and Circular Chemistry

BASF SE is a key innovator in the refinish paint market, focusing on advanced color technologies and sustainability. Its Glasurit® and R-M® brands are known for complex pigment systems and high-end finishes, including liquid-metal effects for modern vehicles. BASF is integrating chemically recycled raw materials into its coatings, supporting circular economy initiatives. The company is also prioritizing waterborne coatings and smart curing technologies to meet stringent environmental regulations, reinforcing its leadership in high-performance refinish solutions.

Sherwin-Williams Expands Market Share with High-Efficiency and Waterborne Refinish Systems

The Sherwin-Williams Company is strengthening its position in the refinish paint market, particularly in North America. Its Ultra 7000® waterborne system offers superior coverage and blending performance, reducing paint usage and improving efficiency in repair operations. The company is investing in high-durability clearcoats and scratch-resistant finishes, targeting growth in collision repair centers. Its “Total Shop” strategy integrates cloud-based inventory management and distribution networks, increasing customer retention and operational efficiency.

Nippon Paint Drives APAC Growth with Integrated Refinish Solutions and Expansion into MRO Services

Nippon Paint Holdings Co., Ltd. is a major player in the refinish paint market, particularly in Asia-Pacific. The company reported strong revenue growth and improved profitability driven by recovery in automotive markets. Its strategic focus includes expanding into maintenance, repair, and operations (MRO) services, offering integrated solutions beyond traditional coatings. Nippon Paint is also leveraging localized production and supply chain integration to strengthen its position in emerging markets, reinforcing its leadership in high-growth regional refinish segments.

China Refinish Paint Market: Low-VOC Transformation and EV-Centric Repair Ecosystem

China leads the global refinish paint market through a combination of strict environmental regulation, EV-driven demand, and large-scale automotive parc expansion. The enforcement of GB 30981-2020 standards, with further tightening expected in 2026, is accelerating the transition toward low-VOC automotive refinish coatings, particularly waterborne basecoats and ultra-high-solid (UHS) clearcoats across Tier-1 and Tier-2 cities. These policies align with the national “Blue Sky” initiative, making China a key driver of eco-friendly automotive coatings adoption.

The rapid rise of electric vehicles has created demand for low-bake refinish systems operating at 70–85°C, essential for protecting sensitive EV battery systems and sensors. Domestic OEM ecosystems led by NIO and BYD are influencing refinishing standards, particularly in high-gloss and specialty finishes. On the supply side, BASF Coatings (Guangdong) Co. Ltd. expanded its Jiangmen facility to 30,000 tons annually in 2025, strengthening support for the growing network of professional body shops. Key applications include precision color matching for effect finishes and photocatalytic topcoats for environmental depollution infrastructure.

United States Refinish Paint Market: Digital Color Matching and Professional Body Shop Consolidation

The United States automotive refinish coatings market is defined by advanced color science, digitalization, and a highly organized collision repair ecosystem. Major players such as PPG Industries and Sherwin-Williams are accelerating adoption of cloud-connected color-matching systems, integrating spectrophotometers with automated mixing platforms. These technologies reduce paint waste by approximately 15% per repair, enhancing operational efficiency in high-throughput body shops.

Regulatory frameworks led by the Environmental Protection Agency and state-level agencies such as CARB are driving the shift toward waterborne and low-solvent refinish coatings, with increasing preference for UV-resistant acrylic resin systems over traditional polyurethanes. Workforce development is also a priority, with Axalta Coating Systems investing in “Refinish Academy” programs to train technicians in complex applications such as tri-coat and matte finishes. Key applications include high-volume passenger vehicle collision repair and customization coatings for light trucks and aftermarket upgrades.

India Refinish Paint Market: Infrastructure Expansion and Automotive Coating Capacity Growth

India represents a high-growth refinish paint market, supported by infrastructure development, rising vehicle ownership, and expanding domestic manufacturing. According to the Press Information Bureau, infrastructure investments under PM Gati Shakti are significantly increasing demand for protective and refinish coatings in commercial transport fleets, particularly in logistics and public mobility sectors.

On the supply side, companies such as Asian Paints and Kansai Nerolac are undertaking capacity expansion initiatives, including new facilities in Odisha and Rajasthan, aimed at doubling production by FY 2027. Product innovation is also reshaping the market, with the introduction of paint protection films (PPF), ceramic coatings, and advanced matte/gloss finishes targeting India’s expanding premium vehicle segment. Key applications include corrosion-resistant coatings for commercial vehicles and high-end detailing solutions for urban passenger cars.

Germany Refinish Paint Market: Sustainable Coatings and Ecodesign Leadership

Germany sets the benchmark in the refinish coatings market through its strong focus on sustainability, regulatory compliance, and high-performance formulations. The influence of the European Green Deal is evident in the shift toward eco-friendly refinish coatings, circular material usage, and low-emission technologies. BASF Coatings has been recognized with awards such as MATERIALICA and German Ecodesign for innovations like “REVERENCE DARKNESS,” which incorporates recycled tire-derived carbon black, advancing circular economy practices in automotive coatings.

Technological transformation is also underway, with widespread adoption of chrome-free corrosion protection systems in response to REACH regulations, offering up to 1,000 hours of salt-spray resistance without hazardous materials. Additionally, the integration of UV-curing technologies in body shops is reducing energy consumption by over 30%, enabling faster repair cycles and improved sustainability metrics. Key applications include premium automotive refinishing and industrial coatings for high-performance machinery, reinforcing Germany’s leadership in sustainable coating innovation.

Japan Refinish Paint Market: Precision Coatings and High-Durability Automotive Finishes

Japan’s refinish paint market is characterized by its focus on precision coating technologies, durability, and lifecycle performance, supporting its export-oriented automotive industry. Leading companies such as Nippon Paint and Kansai Paint are advancing ultra-fine resin dispersions that enhance color depth, gloss retention, and UV resistance in refinish topcoats, particularly for high-exposure environments.

Regulatory alignment with strict environmental standards has led to the development of visible-light-responsive (VLR) coatings, capable of reducing VOC emissions and odors in semi-enclosed repair environments. Additionally, Japan’s broader push toward energy efficiency is influencing the adoption of solar-reflective coatings for commercial vehicles, improving thermal management and reducing cabin heat. Key applications include high-durability automotive coatings and advanced functional coatings for ADAS-integrated components, including anti-fogging glass systems, reinforcing Japan’s position in high-performance refinish technologies.

Refinish Paint Market Report Scope

Refinish Paint Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$15.6 Billion

|

|

Market Size (2032)

|

$22.1 Billion

|

|

Market Growth Rate

|

5.1%

|

|

Segments

|

By Product (Clearcoats, Basecoats, Primers and Fillers, Sealers and Adhesion Promoters), By Resin Type (Polyurethane, Acrylic, Epoxy, Alkyd, Vinyl, Polyester), By Technology (Water-borne Coatings, Solvent-borne Coatings, UV-Cured Coatings, Powder Coatings), By End-Use (Automotive Refinish, Marine Refinish, Aerospace Refinish, Industrial and Infrastructure Refinish, Furniture and Wood Restoration), By Sales Channel (Automotive Body Shops, Vehicle Dealerships, Fleet Maintenance Providers, DIY, Industrial MRO), By Component Configuration (Two-Component, One-Component)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Axalta Coating Systems Ltd., PPG Industries, Inc., BASF SE, Akzo Nobel N.V., The Sherwin-Williams Company, Nippon Paint Holdings Co., Ltd., Kansai Paint Co., Ltd., KCC Corporation, Jotun Group, Mipa SE, KAPCI Coatings, Bernardo Ecenarro S.A., Cromadex, Roberlo S.A., 3M Company

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Refinish Paint Market Segmentation

By Product

- Clearcoats

- Basecoats

- Primers and Fillers

- Sealers and Adhesion Promoters

By Resin Type

- Polyurethane

- Acrylic

- Epoxy

- Alkyd

- Vinyl

- Polyester

By Technology

- Water-borne Coatings

- Solvent-borne Coatings

- UV-Cured Coatings

- Powder Coatings

By End-Use

- Automotive Refinish

- Marine Refinish

- Aerospace Refinish

- Industrial and Infrastructure Refinish

- Furniture and Wood Restoration

By Sales Channel

- Automotive Body Shops

- Vehicle Dealerships

- Fleet Maintenance Providers

- DIY

- Industrial MRO

By Component Configuration

- Two-Component

- One-Component

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Refinish Paint Industry

- Axalta Coating Systems Ltd.

- PPG Industries, Inc.

- BASF SE

- Akzo Nobel N.V.

- The Sherwin-Williams Company

- Nippon Paint Holdings Co., Ltd.

- Kansai Paint Co., Ltd.

- KCC Corporation

- Jotun Group

- Mipa SE

- KAPCI Coatings

- Bernardo Ecenarro S.A.

- Cromadex

- Roberlo S.A.

- 3M Company

*- List not Exhaustive