Retail Ready Packaging Market Size, Overview, and Growth Outlook (2025–2034)

Retail Ready Packaging Market to Surpass $154 Billion by 2034 Driven by Labor Efficiency and Sustainable Corrugated Solutions

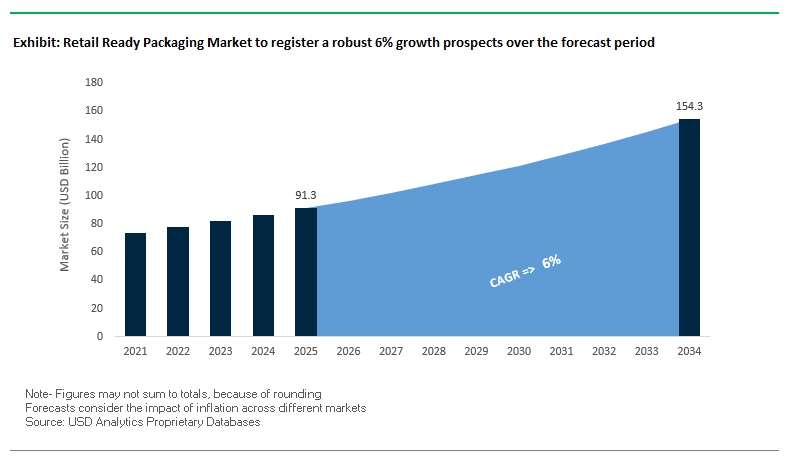

The global retail ready packaging (RRP) market is projected to grow from $91.3 billion in 2025 to $154.2 billion by 2034, registering a CAGR of 6%. This growth is fueled by the increasing adoption of sustainable corrugated materials, in-store labor reduction strategies, and visually appealing packaging designs. RRP is rapidly becoming a critical tool for retailers, brands, and manufacturers seeking operational efficiency, shelf-ready merchandising, and enhanced product visibility.

Key Insights for industry professionals and buyers:

- In-Store Labor Reduction: RRP enables products to be stocked directly on shelves, reducing handling time by up to 40%, and significantly cutting labor costs.

- High Corrugated Board Recovery: About 90% of corrugated materials are recovered for recycling, reinforcing RRP as a sustainable packaging solution.

- Streamlined Supply Chain: By shipping products ready-to-sell from manufacturing sites, RRP reduces touchpoints, minimizes damage risk, and improves logistics efficiency.

- Enhanced Product Visibility: Packaging designs extend a brand’s visual identity from shipping cartons to retail shelves, boosting brand recognition.

- Sustainability and Innovation: Companies are integrating recyclable materials, nanocoatings, and fiber-based e-commerce solutions, supporting both environmental and operational goals.

Market Analysis: Strategic Investments and Technological Innovations Are Shaping Global Retail Ready Packaging Growth

The retail ready packaging market is experiencing dynamic developments across sustainability, automation, and innovative design. In August 2025, Smurfit Kappa Group reported strong corrugated box volumes, reflecting robust demand in e-commerce and modern retail formats. Simultaneously, Loop Industries acquired a site in Gujarat, India, for its “Infinite Loop” manufacturing facility, signaling potential future innovations in plastic-based RRP solutions.

The emphasis on environmental sustainability continues to shape the market. In July 2025, O-I Glass validated early sustainability achievements and aligned operations with Paris-aligned carbon targets, while Mondi launched sustainable packaging solutions for the pet food sector, demonstrating functional and eco-friendly RRP applications.

Technological advancements are also redefining packaging capabilities. In April 2025, DS Smith partnered with a Canadian startup to develop nanocoating technology, enhancing barrier performance for sensitive food products. Earlier in March 2025, DS Smith introduced a fiber-based e-commerce bag for a Danish beauty retailer, exemplifying cross-channel applicability of sustainable packaging. The merger of Smurfit Kappa and WestRock in September 2024 created Smurfit WestRock, expanding global reach and consolidating expertise in innovative RRP solutions.

Retail Ready Packaging Market: Trends and Opportunities Reshaping Retail Efficiency

Integration of Shelf-Life Monitoring and Smart Labeling Technologies

A major trend in the retail ready packaging (RRP) market is the growing adoption of smart labeling technologies to enhance freshness monitoring, inventory accuracy, and food safety. Time-temperature indicators (TTIs), once a niche solution, are now becoming mainstream for managing perishable goods across retail supply chains. These indicators provide irreversible color changes when products are exposed to temperature abuse, offering a clear and immediate signal to both retailers and consumers. By reducing food waste and safeguarding product integrity, TTIs are helping brands and retailers meet sustainability and quality goals simultaneously. Beyond perishables, QR codes and scannable barcodes integrated into RRP are being used to streamline inventory tracking. A retail supply chain study highlights how real-time stock visibility enables automated reordering, reducing reliance on manual shelf checks while optimizing on-shelf availability. Together, these smart solutions transform RRP into not just a merchandising tool but also a data-driven asset that aligns with the growing digitalization of retail operations.

Standardization of Modular Designs for Cross-Retailer Compatibility

Another significant trend is the standardization of modular RRP formats, designed to meet multiple retailer requirements while improving supply chain efficiency. Instead of producing retailer-specific RRP, consumer packaged goods (CPG) brands are now moving towards universal tray and case sizes that fit across diverse store planograms. This reduces packaging complexity and associated costs while ensuring consistent in-store merchandising. Retailers are pushing for modular RRP that adheres to the industry-recognized “Five Easies”—easy to identify, open, shop, replenish, and recycle. According to industry reports, standardized RRP can reduce shelf replenishment times by up to 40%, a critical improvement for labor-constrained retail environments. This shift also enhances sustainability by minimizing packaging waste, reducing transport inefficiencies, and promoting recyclability across retail networks. Ultimately, standardized modular designs are emerging as a cornerstone of retail-ready packaging innovation, driving both operational and environmental benefits.

Development of High-Performance Bio-Based and Compostable RRP

The global shift away from plastic packaging is creating strong opportunities for bio-based and compostable RRP solutions. Paperboard and corrugated packaging are replacing plastic in fresh produce and bakery applications, with innovations like Mondi’s 2025 corrugated and solid board punnets offering stackable, plastic-free alternatives that are both recyclable and compostable. For applications requiring higher barrier performance, advanced coatings are playing a critical role. BASF’s ecovio® biopolymer is an example of a compostable coating that provides moisture and grease resistance, enabling paper and board trays to be used for food categories such as pastries and ready meals. These innovations make bio-based RRP not only functional and durable but also aligned with circular economy regulations and consumer demand for plastic-free shopping experiences. As regulatory bans on single-use plastics expand, demand for sustainable RRP solutions will continue to accelerate.

Optimization of RRP for E-Commerce Fulfillment and Last-Mile Delivery

The rise of omnichannel retail and last-mile logistics is opening opportunities for dual-purpose RRP designs that can function as both in-store displays and shipping containers. Companies like The Royal Group are pioneering designs that eliminate the need for additional outer cartons, allowing products to ship directly to consumers in their retail-ready trays. This reduces packaging layers, lowers fulfillment costs, and minimizes waste—critical for retailers facing rising e-commerce volumes. Furthermore, dual-purpose RRP enhances click-and-collect and dark-store operations by eliminating secondary packing steps, thus improving fulfillment speed and efficiency. According to logistics studies, this packaging optimization is becoming indispensable for retailers striving to create seamless omnichannel experiences while reducing last-mile delivery costs. As e-commerce continues to blur the line between physical and digital retail, RRP engineered for both display and transport is set to become a high-growth segment in the packaging landscape.

Competitive Landscape: Top Industry Players Are Driving Sustainability, Efficiency, and Innovation in Retail Ready Packaging

The retail ready packaging industry is highly competitive, with leading companies leveraging sustainability, automation, and premium design capabilities to differentiate themselves. Key players focus on reducing labor costs, improving recyclability, and delivering end-to-end packaging solutions.

Smurfit Kappa Group (Smurfit WestRock): Leading End-to-End RRP Solutions with Advanced Virtual Shelf Optimization

Smurfit Kappa provides a comprehensive range of paper-based packaging, including Wrap Split Pack, which allows trays to split into single-facing rows for flexible merchandising. Its ShelfSmart VR tool simulates packaging performance on shelves, enabling brands to optimize designs pre-production. The merger with WestRock created a global leader in sustainable packaging with expanded geographic footprint and product diversity. Smurfit Kappa’s end-to-end solutions combine innovation, design, and logistics to meet retailer and brand requirements effectively.

DS Smith Plc: Pioneering Circular Economy Solutions in Retail Ready Packaging

DS Smith offers RRP and in-store displays designed to enhance brand presence and streamline supply chains. The company emphasizes circular economy principles, employing a closed-loop recycling model for paper and corrugated materials. Recent innovations include fiber-based e-commerce bags and TapeBack packaging, eliminating single-use plastics and improving recyclability. Designers trained in Circular Design Principles ensure packaging meets metrics for recycled content, recyclability, and waste reduction, providing a competitive edge.

WestRock Company: Integrating Automation and Fiber-Based Expertise for Retail Efficiency

WestRock delivers a broad portfolio of RRP, including corrugated containers and folding cartons, for sectors like e-commerce, food, and personal care. The company’s merger with Smurfit Kappa in September 2024 strengthened its global position. WestRock’s packaging automation expertise supports clients in filling labor gaps, optimizing throughput, and minimizing downtime, offering a comprehensive, end-to-end packaging solution.

Mondi Group: Driving Sustainability and High-Barrier Innovations in Paper-Based RRP

Mondi develops innovative paper-based packaging, including corrugated solutions and stand-up pouches, aligned with circular economy principles. Its ThinkBox initiative enables collaborative innovation with clients. Recent projects include sustainable solutions for pet food and FunctionalBarrier Paper Ultimate, supporting high-barrier and eco-friendly applications. An August 2025 biomass power plant expansion underscores Mondi’s commitment to energy-efficient production.

Georgia-Pacific LLC: Vertically Integrated Operations Enabling Consistent and Sustainable RRP

Georgia-Pacific leverages a vertically integrated model, controlling the supply chain from sustainable forestry to corrugated production. Its Brand Ready Packaging enhances brand communications while meeting retailer and customer needs. The company operates one of the largest recycling businesses, with over $15 billion invested since 2014 to improve sustainability and manufacturing efficiency. Georgia-Pacific provides consistent, reliable, and environmentally responsible RRP solutions.

Retail Ready Packaging Market Share Insights, 2025-2034

Die-Cut Containers dominate Market Share by Packaging Type in Retail Ready Packaging (RRP)

Die-cut containers (55%) are the RRP workhorse, balancing printable brand real estate, easy-open features, and structural strength to move from DC to shelf in seconds—crucial where the Amazon Effect compresses replenishment windows. Corrugated trays ( 25%) optimize strength-to-weight for beverages, canned goods, and household chemicals, excelling in automation compatibility and damage reduction. Shrink-wrapped trays ( 12%) trade down to capex-light visibility, yet face sustainability headwinds due to film usage and inferior openability. Plastic corrugated trays ( 5%) win in closed-loop, reusable pools for bakery/produce where hundreds of cycles amortize cost, while display-ready pallets ( 3%) serve high-velocity promos (club and big-box) to slash touch points and labor minutes per SKU. The share pattern reflects retailers’ KPI stack—stocking time, planogram compliance, damage rate, and total landed cost—with fiber-based RRP leading due to recyclability, print quality, and supply-chain robustness.

Food & Beverages lead Market Share by End-Use in Retail Ready Packaging (RRP)

Food & Beverages ( 60%) dominate RRP adoption because labor minutes saved per case directly impact margins in high-frequency, low-unit-value FMCG (snacks, dairy, beverages), making shelf-ready, perforated, and print-matched solutions standard to accelerate facing, reduce out-of-stocks, and drive sell-through velocity. Consumer goods ( 25%) balance brand blocking and shelf discipline, using premium die-cut containers to protect higher-value items (beauty, toys, small electronics) while still enabling rapid shelf activation. Healthcare & Pharmaceuticals ( 8%) layer tamper evidence, child-resistance cues, and clear IFUs onto RRP, ensuring compliance without sacrificing replenishment speed. Retail private label ( 5%) scales quickly thanks to centralized spec control and network mandates, often setting the retailer-wide RRP playbook that national brands must follow; Other ( 2%) categories adopt under retailer pressure. Overall, end-use shares mirror the operational calculus of modern stores: RRP is a merchandising and labor-efficiency technology, and Food & Beverages capture the largest benefit from reduced touches, faster displays, and recyclable fiber footprints.

United States: CHIPS and Science Act Accelerating Advanced Packaging Growth

The United States retail ready packaging market is witnessing robust growth fueled by government-backed initiatives and rising demand across semiconductors, automotive electronics, and consumer goods. A key development is the CHIPS and Science Act, under which the U.S. Department of Commerce announced a $5 billion grant program in April 2024 to strengthen advanced packaging technologies, particularly wafer-level packaging (WLP). This funding is strategically aimed at boosting domestic manufacturing resilience and reducing reliance on foreign supply chains. Leading companies such as Intel are actively expanding wafer-level packaging operations in the U.S., developing cutting-edge solutions for next-generation processors, AI-driven systems, and memory chips.

The market is increasingly shaped by heterogeneous integration, where multiple types of chips are combined into a single package to enhance performance and power efficiency. Research institutions, including the Georgia Institute of Technology, are pioneering disruptive technologies like roll-to-roll WLP processes and advanced microfluidic cooling systems, which promise to overcome thermal management and scalability challenges. Additionally, the surge in electric vehicle (EV) adoption is creating fresh opportunities, as automotive electronics require compact, reliable, and high-performance semiconductor packaging. Together, these trends position the U.S. as a leader in advanced retail ready packaging solutions across electronics, automotive, and high-tech industries.

European Union: EU Chips Act and PPWR Reshaping Retail Ready Packaging

The European Union retail ready packaging market is being reshaped by regulatory and funding initiatives, particularly the European Chips Act, which is mobilizing significant investments in semiconductor value chains, covering both front-end fabrication and back-end packaging. The EU is strategically strengthening its capabilities in wafer-level packaging and advanced integration technologies to reduce dependency on Asian suppliers. Programs such as Horizon Europe are channeling funds into R&D for bio-based and compostable packaging materials, enhancing sustainability in both semiconductor packaging and consumer goods markets.

Regulatory shifts are also driving industry transformation. The Packaging and Packaging Waste Regulation (PPWR), effective February 2025, mandates higher recyclability standards, compelling manufacturers to adopt eco-friendly packaging machinery and materials. European companies are investing in specialized applications across industrial automation, high-reliability automotive components, and medical devices, where compact packaging and durability are critical. This dual focus on innovation and sustainability ensures Europe remains competitive in the global retail ready packaging landscape while transitioning toward a circular economy model.

China: Domestic Expansion and Advanced Packaging Innovation

China’s retail ready packaging market is rapidly expanding under the country’s “14th Five-Year Plan”, which emphasizes digital transformation, intelligent manufacturing, and self-reliance in semiconductors. The government is fostering the growth of a comprehensive semiconductor ecosystem, where advanced packaging plays a central role in supporting consumer electronics, telecom, and industrial applications. Domestic companies are increasingly investing in fan-out packaging, 3D stacking technologies, and high-barrier materials, strengthening China’s competitive position against global rivals.

A notable trend in China is the rising demand for technologically advanced packaging with anti-counterfeiting features, enhanced durability, and barrier properties. This focus is particularly relevant in fast-growing sectors such as smartphones, telecom equipment, and connected devices. With large-scale production capacity and heavy investment in automation, Chinese firms are scaling retail ready packaging to serve both domestic and export markets. Combined with government-backed innovation, China is expected to remain a key growth hub for advanced and retail-ready packaging solutions.

India: Government Incentives and OSAT Expansion Driving Market Growth

In India, the Retail Ready Packaging Market is strongly supported by government-led schemes such as the Production Linked Incentive (PLI) and Design Linked Incentive (DLI) programs, which allocate substantial funds to strengthen the domestic semiconductor ecosystem. These initiatives are closely tied to the India Semiconductor Mission (ISM), which promotes investment in advanced packaging and outsourced semiconductor assembly and test (OSAT) services. Several approved projects under ISM highlight India’s growing role as a packaging and testing hub for global semiconductor supply chains.

Infrastructure and regulatory improvements are reinforcing this growth. The National Single Window System and emerging semiconductor parks provide streamlined approvals and plug-and-play ecosystems to attract global investors. Moreover, talent development programs such as Chips to Startup (C2S) are being rolled out to address the country’s skill gap in advanced packaging technologies. Alongside semiconductors, the expansion of retail, FMCG, and e-commerce sectors is driving adoption of innovative retail ready packaging solutions to meet growing consumer demand. India’s combined focus on policy support, infrastructure, and workforce development makes it a rising market for advanced retail ready packaging applications.

Japan: BBCube™ Innovation and Industry Leadership in Advanced Packaging

Japan’s retail ready packaging market is underpinned by technological leadership and innovation in advanced semiconductor packaging. Researchers at the Institute of Science Tokyo have developed BBCube™ technology, a novel 2.5D/3D chip integration method that improves performance, thermal efficiency, and scalability for next-generation electronic devices. This breakthrough highlights Japan’s role as a global hub for advanced packaging R&D. Japanese companies are also pioneering high-speed bonding techniques and next-generation adhesive materials for 3D integration, targeting high-performance computing (HPC) and AI-driven applications.

The Ministry of Economy, Trade and Industry (METI) is heavily supporting the revitalization of Japan’s semiconductor industry, with initiatives focused on materials, equipment, and packaging innovation. With a strong emphasis on quality, reliability, and miniaturization, Japan remains a critical player in wafer-level packaging and 3D stacking solutions. The integration of these innovations into retail ready packaging formats across electronics, consumer goods, and healthcare ensures that Japan continues to set benchmarks for performance and sustainability in global markets.

Taiwan: Global Leader in Wafer-Level Packaging and High-Performance Solutions

Taiwan remains a global leader in semiconductor manufacturing and retail ready packaging, with companies like TSMC at the forefront of innovation. Taiwanese firms dominate the fan-out wafer-level packaging (FOWLP) space, which is essential for high-density applications requiring superior electrical performance and compact integration. With growing demand for consumer electronics, 5G infrastructure, and automotive semiconductors, Taiwan continues to expand its advanced packaging capacity to serve global markets.

The country’s leadership is further reinforced by its deep expertise in chip manufacturing, R&D investment, and ecosystem partnerships. By integrating wafer-level packaging innovations with sustainability initiatives, Taiwanese companies are not only supporting global technology brands but also ensuring that retail ready packaging solutions meet the performance, cost, and environmental requirements of the next decade’s digital economy.

Retail Ready Packaging Market Report Scope

Retail Ready Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$91.3 Billion

|

|

Market Size (2034)

|

$154.2 Billion

|

|

Market Growth Rate

|

6%

|

|

Segments

|

By Packaging Type (FI-WLP, FO-WLP, WLCSP, 3D TSV WLP, 2.5D TSV WLP, Nano WLP), By Technology (Electrochemical Deposition, Physical Vapor Deposition, Etch, Chemical Vapor Deposition, CMP, Other Technologies), By End-Use Industry (Consumer Electronics, IT & Telecommunication, Automotive, Healthcare, Aerospace & Defense, Industrial), By Application (Analog & Mixed-Signal Devices, MEMS, RF Devices, PMICs, Sensors, Other Applications)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Advanced Semiconductor Engineering (ASE), Amkor Technology, Taiwan Semiconductor Manufacturing Company (TSMC), Intel Corporation, JCET Group Co., Ltd., Samsung Electronics Co., Ltd., Lam Research Corporation, Applied Materials, Inc., Deca Technologies Inc., Fujitsu Limited, Tokyo Electron Ltd., Unisem (M) Berhad, Powertech Technology Inc., Chipbond Technology Corporation, Siliconware Precision Industries Co., Ltd. (SPIL)

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Retail Ready Packaging Market Segmentation

By Packaging Type

- FI-WLP

- FO-WLP

- WLCSP

- 3D TSV WLP

- 2.5D TSV WLP

- Nano WLP

By Technology

- Electrochemical Deposition

- Physical Vapor Deposition

- Etch

- Chemical Vapor Deposition

- CMP

- Other Technologies

By End-Use Industry

- Consumer Electronics

- IT & Telecommunication

- Automotive

- Healthcare

- Aerospace & Defense

- Industrial

By Application

- Analog & Mixed-Signal Devices

- MEMS

- RF Devices

- PMICs

- Sensors

- Other Applications

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Retail Ready Packaging Market

- Advanced Semiconductor Engineering (ASE)

- Amkor Technology

- Taiwan Semiconductor Manufacturing Company (TSMC)

- Intel Corporation

- JCET Group Co., Ltd.

- Samsung Electronics Co., Ltd.

- Lam Research Corporation

- Applied Materials, Inc.

- Deca Technologies Inc.

- Fujitsu Limited

- Tokyo Electron Ltd.

- Unisem (M) Berhad

- Powertech Technology Inc.

- Chipbond Technology Corporation

- Siliconware Precision Industries Co., Ltd. (SPIL)

* List Not Exhaustive

Methodology

USDAnalytics employs a rigorous, multi-layered methodology to analyze the global retail ready packaging (RRP) market, combining in-depth secondary research with targeted primary insights to provide actionable intelligence for industry professionals. Our approach begins with comprehensive secondary research, sourcing data from corporate filings, trade publications, regulatory documents, industry reports, and verified news outlets to identify trends in sustainability, automation, and packaging design innovations. Primary research includes interviews and surveys with key stakeholders such as packaging manufacturers, retailers, CPG companies, and e-commerce operators, capturing first-hand insights on operational efficiencies, shelf-ready merchandising, and end-use adoption patterns. USDAnalytics applies advanced quantitative methods to forecast market growth, integrating factors such as modular packaging adoption, labor reduction strategies, and bio-based or compostable material utilization. Regional regulatory impacts, circular economy initiatives, and supply chain efficiencies are carefully assessed to understand their influence on market dynamics. The analysis incorporates technology trends including smart labeling, time-temperature indicators, and dual-purpose RRP for e-commerce, as well as global investment activity and M&A movements, enabling strategic recommendations that address sustainability, cost optimization, and omnichannel retail challenges.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.