Energy-Efficient Cool Roof Technologies and Restoration-Led Demand Driving Moderate Growth

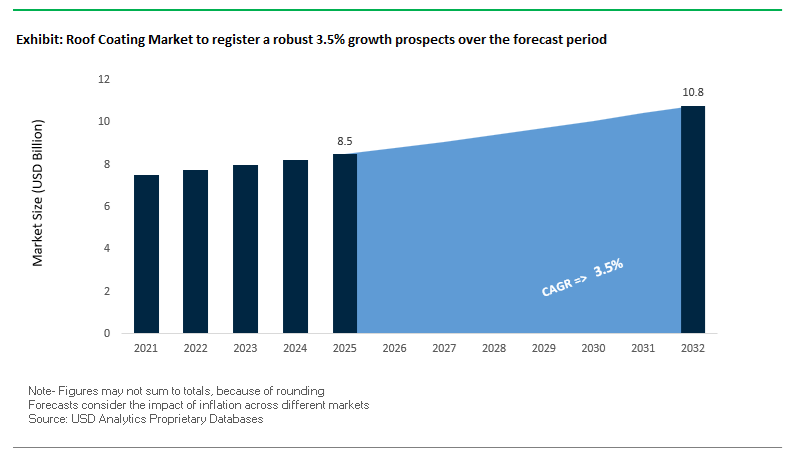

The global Roof Coating Market is positioned for steady expansion, with the market valued at $8.5 billion in 2025 and projected to reach $10.8 billion by 2032, growing at a CAGR of 3.5% during 2025–2032. Unlike high-growth specialty coatings segments, this market is characterized by stable, maintenance-driven demand cycles, particularly across commercial, industrial, and residential building stock requiring periodic refurbishment. The shift toward roof restoration over full replacement has become a defining structural driver, as building owners prioritize cost optimization, lifecycle extension, and sustainability compliance.

A major growth pillar is the rising adoption of cool roof coatings and reflective membranes, which significantly reduce heat absorption and lower building energy consumption. With urban heat island mitigation becoming a regulatory and ESG priority, governments and municipalities are increasingly encouraging the deployment of high solar reflectance index (SRI) coatings. This trend is particularly pronounced in regions with high cooling demand, where reflective coatings directly translate into reduced HVAC energy consumption and operational cost savings.

Simultaneously, the market is undergoing a formulation-level transformation, driven by tightening environmental regulations and the phase-out of hazardous chemicals. The industry-wide transition toward PFAS-free roof coating systems, announced in March 2026, reflects proactive alignment with upcoming regulatory frameworks in Europe and North America. This shift is reshaping resin chemistry, pushing manufacturers to innovate in fluorine-free waterproofing technologies without compromising durability or weather resistance.

Another structural trend is the increasing integration of multi-functional coatings that combine waterproofing, insulation, UV resistance, and durability into a single system. These solutions are gaining traction in both new construction and retrofit applications, particularly in logistics hubs, warehouses, and data centers where thermal efficiency and asset protection are critical. Overall, the market is evolving toward performance-driven, energy-efficient, and regulation-compliant roofing solutions, supported by long-term infrastructure renewal cycles.

Market Analysis: Renewable Curing Technologies, System Selling Strategies, and Regulatory Shifts Redefining Market Competition

The competitive landscape of the roof coating market is being reshaped by technological innovation, strategic portfolio expansion, and regulatory-driven product evolution. In October 2025, AkzoNobel introduced its IONOMY™ ecosystem, a transformative initiative aimed at enabling coil coating manufacturers to transition toward renewable energy-based curing processes. By replacing conventional gas-intensive thermal ovens with radiation or induction curing technologies, this ecosystem significantly reduces carbon emissions in pre-painted metal roofing production, aligning with decarbonization goals across the construction value chain.

Product portfolio expansion remains a central strategy among leading players. In November 2025, Sika rebranded and expanded its Sealing & Protection range, introducing solutions such as Sika® Waterproofer & Protector, a liquid-applied membrane designed for residential and light commercial roof restoration. This move reflects a targeted push toward distribution channel penetration via independent builders’ merchants, strengthening accessibility and brand visibility in fragmented regional markets.

From a systems integration perspective, Holcim’s “Strategy 2026” milestone underscores a major shift toward end-to-end roofing solutions. With its roofing division expected to reach $6 billion in sales by 2026, the company highlighted that 80% of revenue now comes from system selling, where insulation, membranes, and high-performance coatings are delivered as a unified package. This approach enhances value capture while simplifying procurement for large-scale commercial projects.

Climate resilience is also emerging as a key differentiator. At the International Roofing Expo (January 2026), GAF advanced its FORTIFIED™ roofing program, training over 1,100 professionals to deploy coating systems designed to withstand extreme wind and hail conditions. This aligns with increasing insurance requirements and risk mitigation strategies in climate-sensitive regions, positioning high-performance coatings as a critical component of resilient infrastructure.

Operational expansion is further strengthening supply chain efficiency. Sika’s July 2025 opening of a 280,000 sq ft distribution hub in Leeds, UK, enhances the distribution of liquid-applied membranes and coatings across Northern Europe, directly addressing the surge in re-roofing demand in aging urban infrastructure.

Innovation in functional performance is another key battleground. In January 2026, PPG accelerated the commercialization of multi-functional cool roof coatings that combine waterproofing with thermal insulation while maintaining high solar reflectance even in polluted environments. These advanced systems now account for nearly 30% of PPG’s premium roofing revenue, indicating strong market acceptance of energy-efficient solutions.

Meanwhile, RPM International continues to benefit from the structural shift toward maintenance-driven construction spending, with its roof restoration and sealant segment emerging as a consistent growth driver within its Construction Products Group.

Market Trend: U.S. DOE Efficiency Standards Accelerating Adoption of High-SRI Cool Roof Coatings in Manufactured Housing

The roof coatings market in the United States is being reshaped by updated federal energy efficiency standards targeting manufactured housing. The implementation of the Energy Conservation Program for Manufactured Housing, alongside legislative backing through federal incentive structures, is driving widespread adoption of high-albedo cool roof coatings as a core component of energy-efficient building envelopes.

Under 2026 compliance criteria, roof coatings applied to manufactured homes must achieve high Solar Reflectance Index performance, ensuring that roof surface temperatures remain within 10°F to 15°F of ambient conditions. This represents a substantial improvement compared to traditional asphalt-based roofing systems, which can exceed ambient temperatures by 50°F to 90°F. The ability to reduce heat absorption directly lowers cooling loads, making cool roof coatings a critical solution in both residential and light commercial applications.

Financial incentives are reinforcing this transition. Homes that meet advanced energy efficiency benchmarks, including the integration of high-performance roof coatings, are eligible for federal tax credits of up to $5,000 under the 45L program when achieving Zero Energy Ready Home certification. This is encouraging builders and developers to incorporate reflective coatings into standardized construction practices.

At a macro level, the energy impact is significant. Estimates indicate that widespread deployment of high-SRI roof coatings, combined with improved insulation systems, can generate cumulative annual energy savings exceeding $2 billion across the U.S. building stock. This positions cool roof coatings as a key technology in national energy reduction strategies and decarbonization initiatives.

Market Trend: France RE2020 Regulation Driving Low-GWP Roof Coatings with Verified Life Cycle Assessments

In Europe, regulatory pressure is shifting from operational energy performance toward embodied carbon reduction, with France’s RE2020 framework setting a precedent for low-global-warming-potential construction materials. The regulation’s tightened thresholds for 2026 are compelling coating manufacturers to prioritize low-GWP formulations supported by transparent lifecycle data.

The allowable carbon footprint for new residential construction has been significantly reduced, with thresholds for single-family homes decreasing by approximately 17% from prior benchmarks. This is forcing specifiers to select roof coatings that contribute minimal carbon impact within the overall building lifecycle. Products lacking verified environmental credentials risk disqualification from new construction projects.

Compliance with lifecycle assessment standards has become mandatory. Under EN 15804+A2, coating manufacturers must provide detailed Environmental and Health Declaration Forms that quantify emissions across the product lifecycle. Failure to supply compliant LCA documentation can increase the calculated construction carbon index by approximately 50 kg CO2 equivalent per square meter, potentially exceeding regulatory limits and preventing project approval.

These requirements are driving innovation in resin selection, formulation chemistry, and raw material sourcing, with a focus on reducing embodied carbon without compromising durability or weather resistance. As a result, low-GWP roof coatings are emerging as a premium segment within the European market, particularly in France where regulatory enforcement is most advanced.

Market Opportunity: Self-Healing Elastomeric Roof Coatings Enabling Cost-Effective Restoration of Aging School Infrastructure

The aging infrastructure of public school buildings in the United States is creating a strong opportunity for self-healing elastomeric roof coatings as an alternative to full roof replacement. Budget constraints and the need for rapid refurbishment are driving school districts toward restoration strategies that extend asset life while minimizing capital expenditure.

High-solids elastomeric acrylic coatings are engineered to accommodate thermal expansion and contraction, allowing them to reflow and seal micro-cracks that develop over time. This self-healing capability significantly enhances long-term roof integrity, particularly for metal roofing systems exposed to cyclical temperature fluctuations.

Field performance data indicates that these coatings can extend the service life of aging metal roofs by 15 to 20 years. This defers the need for costly tear-off and replacement projects, enabling school districts to allocate limited budgets more efficiently across maintenance and modernization initiatives.

Maintenance efficiency is another key benefit. Self-healing coatings have demonstrated a 35% reduction in leak-related maintenance calls over a five-year period compared to conventional acrylic coatings. This reduction in reactive maintenance supports more predictable budgeting and improves facility reliability, which is critical for educational institutions operating under fixed funding cycles.

Market Opportunity: Fluid-Applied Silicone Roof Coatings Expanding in Hurricane-Prone High-Velocity Zones

Fluid-applied silicone roof coatings are gaining significant traction in hurricane-prone regions, particularly in areas subject to stringent wind and weather resistance standards. In High-Velocity Hurricane Zones such as South Florida, compliance with rigorous testing protocols is essential for material selection in roofing systems.

Silicone coatings offer superior wind-uplift resistance when applied to structurally sound substrates. These systems can withstand negative pressure conditions that often exceed the performance limits of traditional single-ply roofing membranes, making them well-suited for extreme weather environments.

A critical performance advantage is resistance to ponding water. Unlike acrylic coatings, which can degrade under prolonged water exposure, silicone coatings are inherently hydrophobic and maintain adhesion and structural integrity even after continuous immersion for extended periods. This is particularly relevant in regions with high rainfall and poor drainage conditions.

Adhesion strength is a key parameter in certification testing. High-performance silicone coatings are required to achieve minimum peel adhesion values of 2.0 pounds per linear inch across a variety of substrates, including modified bitumen, metal, and thermoplastic membranes. This ensures that the coating system remains intact during severe wind events and contributes to long-term roof durability.

The combination of weather resilience, low maintenance requirements, and regulatory compliance is positioning fluid-applied silicone coatings as a preferred solution in climate-sensitive roofing markets, particularly as extreme weather events increase in frequency and intensity.

Roof Coating Market Share and Segmentation Insights: Flat Roof Dominance and Distributor-Led Professional Supply Chains

By Roof Type: Flat (Low-Slope) Roofs Lead with High Demand in Commercial and Industrial Applications

The flat (low-slope) roof segment dominated the roof coating market with a substantial 70.2% share in 2025, driven by its widespread use across commercial, industrial, and multi-family residential buildings. Structures such as warehouses, manufacturing facilities, office complexes, and apartment buildings predominantly feature flat roofs, making them the primary application area for fluid-applied roof coatings including acrylic, silicone, polyurethane, and PMMA systems. These roofs are particularly vulnerable to ponding water, UV exposure, and membrane degradation, increasing the need for elastomeric and reflective roof coatings that provide waterproofing, leak prevention, and energy efficiency. A key growth driver is the cost-effective restoration capability of coatings, which extend roof lifespan without requiring expensive tear-off and replacement. This combination of maintenance efficiency, durability, and energy-saving performance continues to reinforce the dominance of flat roof coatings in the global market.

By Sales Channel: Specialty Roofing Distributors Lead with Contractor Support and Warranty Compliance

The specialty roofing and construction distributors segment held a leading 46.6% share of the roof coating market in 2025, reflecting the importance of professional contractor supply networks and technical service support. Roof coatings for commercial applications are typically installed by licensed roofing contractors, who rely on specialized distributors for product availability, technical guidance, and access to application equipment such as spray rigs. These distributors also provide manufacturer-certified training programs, ensuring proper installation and optimal coating performance. Additionally, system warranty requirements—often ranging from 10 to 20 years—mandate procurement through authorized distributors, as proof of purchase and compliance documentation are essential for validation. This restricts the role of big-box retail and direct DIY sales in large-scale projects. As demand increases for high-performance waterproof roof coatings and energy-efficient roofing solutions, distributor-led channels remain critical in supporting professional application and ensuring long-term system reliability.

Competitive Landscape of the Roof Coating Market

PPG Leads Market with Digital Integration and High-Durability Roof Coating Systems

PPG Industries, Inc. remains a dominant force in the roof coating market, leveraging its strong financial performance and R&D capabilities. In Q1 2026, the company reported net sales of $3.93 billion with a 21.6% segment income margin. Its PPG LINQ™ platform enables AI-driven color matching and application optimization, reducing material waste by 15% in large-scale roofing projects. PPG has also integrated aerospace-grade durability into its coatings, targeting infrastructure requiring 25+ year service life. Its strategic divestment of architectural coatings allows greater focus on high-margin industrial roofing solutions.

Sherwin-Williams Strengthens Market Leadership with Cool Roof and Distribution Excellence

The Sherwin-Williams Company is a key leader in the roof coating market, driven by its extensive North American distribution network. The company has expanded its manufacturing and logistics capabilities, particularly with its Statesville facility. Its cool roof coatings can reduce surface temperatures by up to 30°C, improving energy efficiency and reducing thermal stress on substrates. Sherwin-Williams maintains a dominant position in reflective acrylic coatings, supported by strong demand for low-VOC, eco-friendly products in urban markets.

AkzoNobel Drives Sustainability with Infrared-Reflective and AI-Optimized Roof Coatings

AkzoNobel N.V. is a major player in the roof coating market, focusing on sustainability and innovation. The company achieved a 14.5% EBITDA margin in Q1 2026 and is progressing toward a merger with Axalta. Its “Rhythm of Blues” collection integrates infrared-reflective pigments, enabling darker colors to maintain high solar reflectance. AkzoNobel also utilizes AI-driven predictive modeling to optimize coating thickness and material usage, enhancing efficiency and reducing costs. Its strategic shift toward high-growth regions strengthens its competitive position.

Sika Expands Market Presence with Liquid-Applied Membranes and Thermochromic Innovations

Sika AG is a leading player in the roof coating market, particularly in waterproofing and building envelope solutions. Its liquid-applied membrane (LAM) portfolio is the fastest-growing segment, driven by ease of application and superior performance. The company has introduced thermochromic coatings that adjust reflectivity based on temperature, reducing HVAC costs by up to 23%. Sika’s focus on digital transformation and operational efficiency further strengthens its leadership in infrastructure and commercial roofing applications.

RPM Strengthens Specialty Segment with Self-Healing and High-Performance Roofing Solutions

RPM International Inc. is a major player in the roof coating market, particularly in specialty applications. Through its Carboline and Rust-Oleum brands, the company offers self-healing coatings that extend roof lifespan by up to 15 years in corrosive environments. Its acquisition of Dudick enhances its portfolio of chemical-resistant coatings for industrial facilities. RPM also leads in bituminous and polyurethane coatings, providing durable waterproofing solutions for high-traffic flat roofs.

Nippon Paint Drives APAC Growth with Advanced Reflective and BIPV-Compatible Coatings

Nippon Paint Holdings Co., Ltd. is a dominant force in the roof coating market in Asia-Pacific. The company has expanded its footprint through acquisitions and strategic integrations, capturing significant regional market share. Its innovations include microscopic glass bead technology, improving infrared reflectivity and energy efficiency. Nippon Paint is also developing coatings for building-integrated photovoltaics (BIPV), enabling direct solar panel integration with roofing materials. Its focus on high-growth construction markets positions it for sustained expansion.

United States Leading Roof Coating Retrofits with High-Performance and Smart Roofing Systems

The United States is at the forefront of the global roof coating market, driven by a strong shift toward roof restoration and recoating solutions rather than full replacements. Advanced materials such as Spray Polyurethane Foam (SPF) and silicone roof coatings are gaining widespread adoption due to their cost efficiency, with recoating costs significantly lower than initial installation, delivering strong lifecycle ROI for commercial assets.

Technological innovation is accelerating, highlighted by the launch of hundreds of sustainability-focused roofing products, including smog-reducing granules and UV-stable elastomers. Regulatory frameworks such as ENERGY STAR and Cool Roof Rating Council (CRRC) standards are making high-reflectance coatings essential for new commercial construction. Infrastructure sectors—including hospitals, airports, and retail complexes—are increasingly adopting sensor-integrated smart roofing systems for real-time monitoring of thermal performance. The widespread use of TPO membranes paired with acrylic topcoats is further enhancing durability and extending roof service life across industrial applications.

China Advancing High-Performance Roof Coatings with Nanotechnology and Industrial Expansion

China is transitioning toward high-value, functional roof coatings, integrating advanced technologies into its industrial ecosystem. The adoption of AI-driven digital twin coating lines is enabling precise control of coating thickness, reducing material waste while ensuring defect-free application.

Regulatory initiatives under the updated “Blue Sky Defense War” policies are accelerating the shift toward waterborne and powder-based roof coatings, reducing reliance on solvent-heavy systems. China’s massive infrastructure expansion, particularly in 5G networks and data centers, is driving demand for dielectric roof coatings that enhance thermal management. Innovations such as PVDF fluorocarbon coatings with 30+ years durability and increased use of intumescent fire-protective coatings in EV battery manufacturing facilities are reinforcing China’s leadership in high-performance roofing solutions. The acrylic segment continues to dominate due to its cost-effectiveness and high reflectivity, making it a preferred choice across industrial developments.

India Emerging as a Solar-Ready and Cool Roof Coating Market Leader

India is rapidly becoming a major growth hub in the roof coatings market, driven by government-led sustainability initiatives and infrastructure expansion. Programs such as the PM Surya Ghar rooftop solar initiative are boosting demand for solar-reflective coatings that prevent heat accumulation beneath photovoltaic panels, improving system efficiency.

State-level Cool Roof policies are mandating high Solar Reflective Index (SRI) coatings for commercial and public buildings, accelerating adoption across urban centers. The market is witnessing a strong shift toward TPO membranes and liquid-applied polyurethane systems, which offer long-term durability and leak-proof performance. Innovations such as pre-engineered coated metal panels for faster solar installation are transforming the construction landscape. Additionally, the growing importance of the renovation segment—accounting for a significant share of demand—is driving large-scale adoption of cool roof retrofits to improve energy efficiency in aging infrastructure.

Saudi Arabia’s Mega Projects Driving Demand for Extreme-Environment Roof Coatings

Saudi Arabia is a key growth market in the roof coating industry, fueled by large-scale developments under Vision 2030. Projects such as NEOM and “The Line” are creating significant demand for high-performance coatings capable of withstanding extreme desert conditions, including wide temperature fluctuations and abrasive sand exposure.

Technological advancements include the deployment of nanotechnology-enhanced epoxies and self-repairing polyurethane coatings, which extend maintenance cycles and improve durability. Regulatory policies promoting local manufacturing and sustainability are encouraging global players to establish domestic production facilities. High-reflectance coatings are widely used in airports, data centers, and industrial buildings to reduce cooling loads and improve energy efficiency. The rapid growth of TPO roofing systems, known for their weldable seams and solar reflectivity, further highlights Saudi Arabia’s focus on advanced roofing solutions tailored for harsh climates.

Germany Leading Digitalized and Sustainable Roof Coating Solutions in Europe

Germany is at the forefront of the European roof coatings market, driven by its commitment to sustainability, digitalization, and energy efficiency. Compliance with the EU Energy Performance of Buildings Directive (EPBD) has made reflective roof coatings a standard requirement for building retrofits, supporting climate-neutral construction goals.

Advanced technologies such as AI-driven UV-LED curing systems are optimizing energy consumption during coating application. Germany is also promoting green steel substrates combined with low-temperature curing coatings, reducing carbon emissions in manufacturing processes. Digital innovations, including blockchain-based material passports, are enhancing traceability and compliance with ESG standards. High demand for antimicrobial reflective coatings in healthcare and public infrastructure further demonstrates the country’s leadership in functional and sustainable coating solutions. Strategic industry consolidation is also enabling the expansion of ultra-high-solid and waterborne coating technologies across the European market.

Vietnam Emerging as a High-Growth Market for Advanced Roof Coating Systems

Vietnam is rapidly developing into a key market for roof coatings, supported by strong industrial growth and increasing foreign direct investment. Regulatory frameworks such as QCVN 19:2024 are enforcing strict TVOC limits, accelerating the transition toward waterborne and low-emission coating systems.

Urban expansion in cities like Ho Chi Minh City and Hanoi is driving demand for high-reflectance roof coatings in residential and commercial construction, particularly in projects targeting EDGE and LEED certification. Technological advancements include the use of nanotechnology-enhanced elastomeric coatings, offering waterproofing, UV resistance, and thermal insulation. The influx of large-scale investments in manufacturing and hospitality infrastructure is further boosting demand for premium polyurethane and acrylic coating systems. Additionally, innovative solutions such as liquid-applied coatings for thermal insulation in dense urban housing are addressing the unique architectural needs of the region.

Brazil Strengthening Roof Coatings Demand Through Agribusiness and Industrial Infrastructure

Brazil’s roof coating market is driven by its strong agribusiness sector and increasing industrial infrastructure investments. Government policies, including anti-dumping duties on coated steel imports, are supporting domestic production of high-performance acrylic roof coatings.

Key applications include abrasion-resistant coatings for grain silos and mining facilities, which prevent heat-related material degradation in tropical climates. Infrastructure initiatives such as the Nova Indústria Brasil (NIB) plan are encouraging the adoption of energy-efficient coating technologies. Technological advancements, including ZAM alloy-compatible coatings, are improving corrosion resistance in coastal and industrial environments. The rising demand for polyurethane and bituminous waterproofing systems in high-rise residential construction is further contributing to market growth, alongside innovations in water management coatings for reservoirs and irrigation systems.

United Arab Emirates Driving Smart Roofing and Asset-Life Extension Technologies

The United Arab Emirates is emerging as a premium market in the roof coatings sector, focusing on asset longevity and smart city development. Strategic policies by organizations such as ADNOC are prioritizing asset-life extension through advanced coating technologies, including nanotechnology-based epoxies and moisture-cured systems.

Regulatory frameworks such as Dubai Municipality’s VOC limits are accelerating the adoption of waterborne coatings, which account for a significant share of market demand. High-profile infrastructure projects, including iconic skyscrapers and commercial developments, rely on polyurethane and fluoropolymer coatings to withstand extreme heat conditions. Technological innovations such as self-healing coatings are enhancing durability in high-traffic areas, while increasing localization of manufacturing is strengthening supply chain resilience. The growing use of recycled-material-based roof and façade coatings further reflects the UAE’s commitment to sustainability and energy efficiency in construction.

Roof Coating Market Report Scope

Roof Coating Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$8.5 Billion

|

|

Market Size (2032)

|

$10.8 Billion

|

|

Market Growth Rate

|

3.5%

|

|

Segments

|

By Chemistry (Elastomeric Coatings, Acrylic Coatings, Silicone Coatings, Polyurethane, Bituminous Coatings, Epoxy Coatings, Fluoropolymer Coatings), By Technology (Water-borne Coatings, Solvent-borne Coatings, 100% Solids), By Substrate (Asphalt, Metal, Membrane, Concrete, Plastic, Wood), By Roof Type (Flat, Steep-Slope Roofs), By End-Use Sector (Non-Residential, Residential), By Application (Maintenance and Retrofit, New Construction), By Sales Channel (Direct Sales, Specialty Roofing and Construction Distributors, Home Improvement Centers)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

PPG Industries, Inc., Akzo Nobel N.V., The Sherwin-Williams Company, BASF SE, RPM International Inc., Sika AG, GAF Materials Corporation, Henry Company, Nippon Paint Holdings Co., Ltd., Dow Inc., Hempel A/S, Kansai Paint Co., Ltd., Holcim, 3M Company, Johns Manville

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Roof Coating Market Segmentation

By Chemistry

- Elastomeric Coatings

- Acrylic Coatings

- Silicone Coatings

- Polyurethane

- Bituminous Coatings

- Epoxy Coatings

- Fluoropolymer Coatings

By Technology

- Water-borne Coatings

- Solvent-borne Coatings

- 100% Solids

By Substrate

- Asphalt

- Metal

- Membrane

- Concrete

- Plastic

- Wood

By Roof Type

By End-Use Sector

- Non-Residential

- Residential

By Application

- Maintenance and Retrofit

- New Construction

By Sales Channel

- Direct Sales

- Specialty Roofing and Construction Distributors

- Home Improvement Centers

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Roof Coating Industry

- PPG Industries, Inc.

- Akzo Nobel N.V.

- The Sherwin-Williams Company

- BASF SE

- RPM International Inc.

- Sika AG

- GAF Materials Corporation

- Henry Company

- Nippon Paint Holdings Co., Ltd.

- Dow Inc.

- Hempel A/S

- Kansai Paint Co., Ltd.

- Holcim

- 3M Company

- Johns Manville

*- List not Exhaustive