Market Overview: Smart Factory, EV Powertrain, and High-Temperature Bearings Drive Sensor Bearing Market Expansion

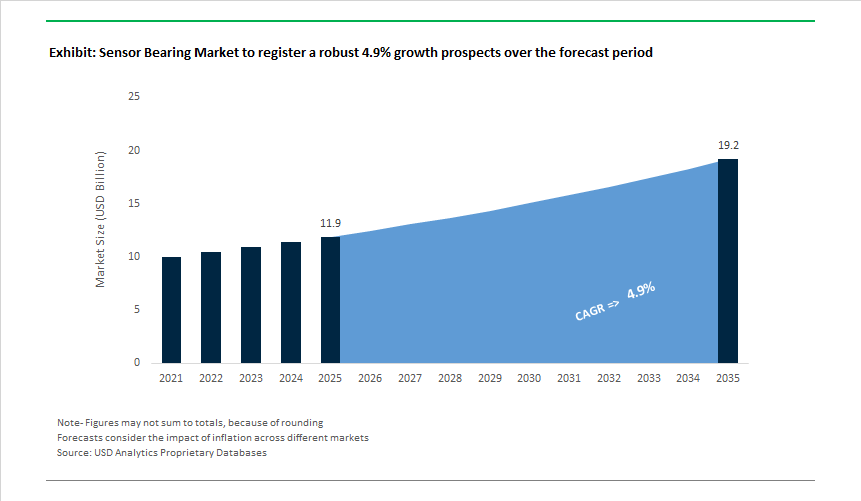

The Sensor Bearing Market is valued at USD 11.9 billion in 2025 and is projected to reach USD 19.2 billion by 2035, growing at a 4.9% CAGR as bearings transition from mechanical wear components into data-generating, decision-enabling subsystems. This evolution is being driven by the combined forces of smart factory deployment, electrified powertrains, and rising intolerance for unplanned downtime across capital-intensive industries.

At a strategic level, demand is shifting from “fit-and-forget” bearings toward integrated mechatronic units that continuously monitor rotational speed, torque, temperature, vibration, and load conditions. For manufacturers and asset owners, the economic logic is compelling: predictive maintenance enabled by embedded sensing can reduce unplanned downtime by around 20% or more, protect adjacent equipment, and extend asset life. As a result, sensor bearings are increasingly specified upfront in new equipment designs rather than retrofitted as aftermarket upgrades, locking suppliers into long equipment lifecycles.

Industrial automation and Industry 4.0 remain the largest pull factors. High-speed machinery, robotics, conveyors, and process equipment now operate within tightly optimized production windows where bearing failure can cascade into multi-line shutdowns. Sensor bearings integrate directly with factory analytics platforms, feeding real-time condition data into IIoT systems and enabling maintenance decisions based on actual operating stress rather than fixed service intervals. This shifts bearings from a maintenance cost center into a performance and uptime lever for plant operators.

Electrified mobility represents a structurally different growth vector. In EV powertrains, bearings increasingly serve dual roles: mechanical support and embedded sensing for speed, torque, and rotor position, all of which are essential for motor control, efficiency optimization, and functional safety. A significant and growing share of new EV platforms now incorporate integrated sensing at the bearing level, reflecting OEM preference for compact, highly reliable architectures that reduce part count and simplify calibration. In this context, sensor bearings directly influence vehicle range, efficiency, and fault detection, elevating their strategic importance within the drivetrain.

Technology architecture is also evolving. Wireless sensor bearings, already accounting for a meaningful share of new installations, are reshaping installation economics by eliminating wiring complexity, reducing failure points, and enabling deployment in distributed or hard-to-access assets. This is particularly relevant in large industrial facilities, wind turbines, and automated warehouses, where cabling costs and maintenance access dominate total ownership cost. Wireless integration accelerates scalability across IIoT networks and supports faster digital retrofits.

At the high-performance edge, aerospace and extreme-duty applications continue to push material and sensing limits. Bearings operating in environments approaching ultra-high temperatures and rotational speeds require advanced materials, stable signal integrity, and robust sensing architectures that function where conventional electronics fail. While niche in volume, these applications act as technology proving grounds, with innovations often cascading into industrial and energy markets over time.

Market Analysis: Strategic Shifts, Technology Innovation and Capacity Expansions

The global Sensor Bearing landscape experienced rapid transformation, with OEMs intensifying their focus on mechatronics, aerospace-grade materials, and EV-first bearing architectures. In November 2025, SKF unveiled a major strategic update during its Capital Markets Day, outlining the planned separation of its Automotive and Industrial divisions. This move is designed to strengthen the Industrial segment’s focus on high-margin Sensor Bearings, Condition Monitoring, and Integrated Sensing Solutions that form the backbone of predictive maintenance in modern industrial environments. That same month, SKF introduced ARCTIC15, a next-generation bearing steel engineered for exposure to extreme temperatures and corrosive conditions. This innovation directly addresses the growing demand for high-stress High-Speed Rotation applications such as aeroengines, electric aircraft systems, and advanced turbines. Complementing its strategic and materials advancements, SKF also launched The Patent Bay, a platform designed to share selected clean rotation and sensor-bearing technologies, reinforcing the company’s leadership in sustainable innovation.

Asia-Pacific and Japan continue to be epicentres of production expansion and precision sensing breakthroughs. In October 2025, NTN Corporation patented an AI-driven displacement sensor bearing with a notable 14% improvement in monitoring accuracy, signalling a leap forward in Industrial Automation, robotics, and high-precision motion systems. On the other hand, in September 2025, NSK expanded its smart bearing manufacturing capacity by 22%, positioning the company to meet escalating global demand from both the Automotive and Industrial IoT sectors. Automotive electrification also accelerated sensor-bearing adoption: throughout 2024, leading Asia-Pacific EV manufacturers integrated ceramic hybrid sensor bearings to enhance thermal resilience, torque measurement accuracy and motor efficiency. Earlier in April 2024, SKF introduced a dedicated EV deep groove ball bearing sensor, optimised for torque sensing and energy efficiency - a design aligned with the fast-evolving EV Powertrain requirements. In parallel, NSK advanced mechatronic sensing with magnetostrictive torque-bearing systems in 2024, enabling superior real-time monitoring and predictive maintenance across automotive and industrial platforms.

The mining and heavy-equipment industries also demonstrated increased adoption of sensor-bearing solutions. At a major Tech & Innovation Summit in December 2024, SKF showcased its Insight sensor-bearing system, engineered for harsh, high-load environments common in mining operations. This solution highlights the sector’s transition from periodic inspections to continuous monitoring architectures, improving asset utilisation and reducing catastrophic failures. The combination of material science innovation, advanced mechatronics, capacity expansions and government-backed digital transformation programs is setting the stage for robust long-term demand for sensor bearings across EV, aerospace, industrial automation and IIoT ecosystems.

Sensor Bearing Market Trends and Opportunities

Trend 1: Embedded Vibration and Temperature Sensing with Edge Analytics

Industrial operators are rapidly moving away from centralized data acquisition toward edge-enabled sensor bearings that process vibration, load, and temperature signatures locally and transmit only actionable insights. This architectural shift is reducing network congestion while enabling faster, physics-informed decisions at the machine level.

A major inflection point has been the deployment of fiber-optic sensing directly inside bearing rings. In 2024–2025, SKF expanded its Insight portfolio with Fiber Bragg Grating (FBG)-based sensor bearings for high-load spindles. Embedded FBGs provide micron-level strain and temperature resolution with zero electromagnetic interference, enabling accurate load mapping even in inverter-rich environments. This capability allows “mid-cut” process corrections in machining—optimizing feed rates and tool life based on real structural stress rather than preset intervals.

Equally important is the shift to on-bearing edge algorithms. Leading mechatronics suppliers now embed signal processing that converts wavelength shifts or magnetic signals into parameters such as cage speed, axial load, and vibration harmonics. Processing data at the source has reduced data transmission volumes by up to 90%, while improving early detection of white etching cracks (WEC) and lubrication starvation—two dominant precursors of catastrophic bearing failure.

A 2025 smart-spindle case study from a global machine tool OEM demonstrated that integrating fiber-optic sensor bearings delivered live cutting-force visibility without compromising spindle stiffness. The result was higher utilization of installed capacity, as machines could be safely pushed closer to their true mechanical limits.

Trend 2: High-Temperature, EMI-Resilient Sensor Bearings for EV Traction Motors

The electrification of transport is imposing extreme requirements on bearings: high rotational speeds, wide temperature envelopes, and immunity to inverter-induced electrical noise. Sensor bearings are emerging as a core enabler of compact, high-efficiency electric drivetrains.

Automotive-grade solutions introduced in 2025, including those from NTN-SNR, are now rated for continuous operation from –40°C to 160°C while supporting speeds approaching 40,000 rpm. These units integrate magnetic angle sensing directly into the bearing assembly, delivering precise rotor position feedback required for advanced synchronous motors.

A critical technical driver is electric discharge mitigation. High-frequency switching in SiC and GaN inverters generates common-mode voltages that can cause discharge pitting and premature bearing failure. Recent patent activity highlights the use of specialized greases, insulated bearing architectures, and shielded sensor housings to suppress discharge currents while preserving clean magnetic signals.

From a system perspective, integrated sensor bearings are enabling resolver elimination. By replacing external position sensors with ready-to-mount mechatronic bearings, OEMs are shortening motor length, reducing mass, and simplifying assembly—while meeting ISO 26262 functional safety requirements for steering, braking, and autonomous-ready platforms.

Opportunity 1: Mandatory Digitization of Wind Turbine Mainshaft Bearings

The scaling of offshore wind to 20+ MW turbine classes has turned bearing condition monitoring into a contractual necessity rather than a discretionary upgrade. Mainshaft bearing failures now carry seven-figure repair costs once vessel mobilization and crane time are included.

With turbines such as those announced in 2025 by Siemens Gamesa, operators are increasingly adopting availability-linked warranties that require continuous health data to guarantee uptime levels approaching 97%. Sensor bearings provide the load spectra and vibration data needed to support these guarantees.

Condition monitoring is already at scale. NSK reported in 2025 that its CMS solutions are deployed across 40,000+ wind turbines globally, detecting failure modes such as hydrogen embrittlement and surface peeling well before visible damage occurs.

Policy alignment is reinforcing adoption. Incentive frameworks in the UK and Germany increasingly favor projects that demonstrate predictive maintenance capability, as real-time monitoring reduces the Levelized Cost of Energy (LCOE) by avoiding weather-driven emergency repairs. For large offshore arrays, sensor bearings capable of real-time WEC detection are becoming a prerequisite for insurance underwriting and project finance.

Opportunity 2: Hygienic, Washdown-Ready Sensor Bearings for Food and Pharma

Stringent hygiene regimes in food processing and pharmaceuticals are creating a high-growth niche for sealed, contamination-proof sensor bearings that eliminate external mounts and wiring.

Traditional bolt-on vibration sensors introduce crevices that act as bacterial harbors. In 2025, manufacturers are shifting to fully integrated, washdown-ready smart bearings, such as solutions within ABB’s Ability™ ecosystem, where sensors are encapsulated within the bearing housing. These units withstand aggressive chemical cleaning while maintaining signal integrity.

Lubrication remains the dominant failure mode in hygienic environments—accounting for ~80% of bearing failures in food processing. Smart sensor bearings now incorporate ultrasonic acoustic sensing and temperature monitoring to assess grease condition in real time. Early detection of overheating—often linked to over-greasing or contamination—prevents unplanned line stoppages.

Connectivity design is also evolving. To preserve sterile zones, many systems now use Bluetooth Low Energy (BLE) or NFC, allowing technicians to assess bearing health remotely via mobile devices without entering high-care areas. This not only improves uptime but also materially reduces cross-contamination risk.

Market Share Analysis: Sensor Bearing Market

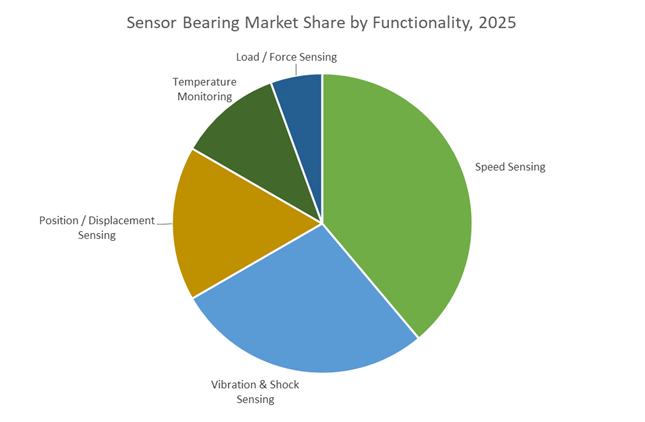

Market Share by Functionality: Speed-Sensing Bearings Anchor Closed-Loop Motion Control Architectures

Speed-sensing bearings account for approximately 35% of the Sensor Bearing Market because they sit at the core of closed-loop control systems that define modern electric drivetrains and automated machinery. Unlike temperature or load-sensing variants, speed feedback is non-negotiable for real-time torque modulation, regenerative braking, and motion synchronization, making it the first functionality OEMs integrate when upgrading to “smart” bearings. The segment’s dominance is reinforced by the rapid escalation of operating speeds in EV powertrains: integrated sensor bearings qualified for up to 40,000 RPM are now essential for compact, high-efficiency 800V e-drive motors, where higher rotational speed directly translates into smaller motor size and lower copper losses. Precision has become an equally powerful driver—2025-generation bearings can deliver up to 4× higher pulse resolution per revolution, enabling stable control at near-zero speeds, a requirement for autonomous parking, robotic arms, and precision conveyors. From a system-engineering perspective, advances in embedded algorithms have pushed torque prediction accuracy up by ~50%, dramatically improving digital twin fidelity and reducing overdesign margins in early-stage vehicle and industrial equipment development. Finally, improved **magnetic flux immunity—now roughly double that of earlier encoders—**allows speed-sensing bearings to be mounted closer to high-power electric motors without signal corruption, reinforcing their role as the default functionality in dense, electrified architectures.

Market Share by Application: Automotive Demand Scales Sensor Bearings Into Mass-Market Intelligence Components

Automotive represents the largest application segment with around 40% market share, reflecting the convergence of electrification, vehicle automation, and functional integration at the wheel and drivetrain level. Speed-sensing bearings have moved from niche components to embedded system enablers, with nearly half of modern ABS and ESC platforms now relying on integrated sensor bearings instead of externally mounted sensors. This shift is driven by both performance and economics: integrating the sensor directly into the bearing reduces assembly steps, improves signal reliability, and shields sensitive electronics from debris, vibration, and thermal cycling. Reliability metrics are now a decisive buying factor—automotive-grade sensor bearings are designed for 15-year service lives, a threshold that has helped OEMs reduce warranty exposure by double-digit percentages while supporting extended vehicle ownership cycles. Electrification further amplifies demand: collaborative OEM–Tier 1 programs have demonstrated that low-friction, sensor-integrated hub units can extend EV driving range by up to 3%, a material gain in a market where marginal efficiency improvements strongly influence consumer choice. Speed-sensing bearings also play a critical role in millisecond-level wheel-speed monitoring, enabling smoother regenerative braking and higher energy recovery without compromising stability on low-friction surfaces. Taken together, high production volumes, measurable efficiency gains, and safety-critical functionality firmly position automotive as the primary application shaping market share dynamics in the sensor bearing market.

Competitive Landscape: Mechatronic Integration, Advanced Materials and Predictive Monitoring Strategies

The competitive landscape in the Sensor Bearing Market is shaped by companies that combine precision mechanics, embedded electronics, AI-driven monitoring, and advanced material science. Leading players are shifting from traditional bearing manufacturing to integrated sensing platforms, enabling real-time diagnostic capabilities and predictive analytics for critical assets. Competitiveness is increasingly linked to innovation in smart factory automation, EV mechatronics, wireless sensor integration, and extreme-temperature durability.

SKF Group - Strengthening Leadership in Iiot and Condition Monitoring

SKF dominates global sensor-bearing solutions through a comprehensive portfolio that integrates bearings, sensors, and digital monitoring into unified platforms. Its SKF Insight bearing line eliminates the need for external sensors, maximising uptime in predictive maintenance programs. The company continues to expand capabilities in circular manufacturing, remanufacturing, and sustainable bearing technologies. SKF’s strategic portfolio includes motor encoder units, steering encoder systems and EV-specific sensor bearings, positioning it as a preferred partner for electric powertrain OEMs. With manufacturing consolidation focused on high-tech facilities, SKF is aggressively scaling its advanced mechatronic solutions strategy.

Schaeffler Group - Motion Technology Leader With Deep Mechatronic Expertise

Schaeffler’s competitive advantage lies in its integration of bearings, drive motors, precision gearboxes and sensing systems. Its prominent role in Industrial Automation-particularly robotics-strengthens its position as a system-level partner rather than a component vendor. The company continues to expand its precision manufacturing capabilities for EV powertrain components in China, reinforcing global market penetration. Under its "Roadmap 2025," Schaeffler is accelerating innovation in smart bearings and torque-sensing solutions tailored for robotics, chassis systems, and transmission applications, supported by strong design synergies across its mechatronics portfolio.

NTN-SNR - Pioneer in Active Sensor Bearing (ASB®) Technology

NTN-SNR remains a technological trailblazer with its patented Active Sensor Bearing (ASB®) technology, foundational for accurate rotary speed measurement in mobility applications. The company’s angle sensor bearings play a critical role in optimising synchronous electric motor efficiency in EVs. Its development of TMR (Tunnel Magnetoresistance) sensing solutions provides exceptional low-speed resolution-essential for autonomous vehicles, off-road systems and advanced traction control. NTN-SNR’s mastery of magnetic measurement and compact integration solutions cements its position as a premier mechatronics partner for global automotive OEMs.

NSK Ltd. - Tribology Pioneer With AI-Enabled Mechatronic Sensing

NSK leverages world-class expertise in tribology and mechatronics to develop compact, maintenance-free sensor bearings designed for long-term reliability. Its products offer double the magnetic flux resistance of conventional alternatives, making them ideal for heavy industrial machinery and IIoT environments. The company is investing aggressively in materials innovation, including Super-TF steel and DLC coatings, engineered for durability under contamination and poor lubrication. With a global network of dedicated Technology Centers, NSK provides rapid customisation support for complex integrated sensing applications across industries.

The Timken Company - High-Performance Bearings For Extreme Industrial Conditions

Timken specialises in robust engineered bearings suited for demanding industrial, aerospace and automotive applications. Its SENSOR-PAC wheel bearing package delivers zero-speed sensing for ABS and traction control systems and is engineered for debris resistance, corrosion protection and thermal shock stability. Timken’s proprietary steel alloys and surface treatments extend bearing lifespan in high-load industrial environments. Its strategy of embedding sensors internally without altering the bearing’s dimensional envelope ensures high load capacity and space efficiency-an essential requirement for EV Powertrain architectures.

Germany continues to define the technological frontier of the sensor bearing market, driven by its dominance in mechatronics, rail systems, and humanoid robotics. In December 2025, Schaeffler unveiled a next-generation planetary gear actuator integrating an electric motor, two-stage gearbox, and high-resolution encoder-based sensor bearing into a single compact unit. This launch—showcased at CTI Berlin and positioned for CES 2026—signals a decisive shift toward edge-intelligent bearings that enable torque, position, and vibration analytics inside robotic joints.

Germany’s rail infrastructure further reinforces this leadership. In December 2025, Schaeffler received the Siemens Mobility Supplier Award after its sensorized axlebox bearings enabled the Velaro Novo to reach 405 km/h, using real-time load and thermal monitoring to ensure stability at extreme speeds. These developments align with Germany’s High-Tech Strategy 2025, which offers R&D tax incentives for AI-driven predictive maintenance and decarbonized bearing factories, anchoring Germany’s role as the global benchmark for intelligent rotation systems.

Japan: Ultra-Low Friction Bearings for EVs and Robotics

Japan is leveraging its structural dominance in precision bearings to deliver compact, sensor-integrated solutions for EVs and humanoid robots. At iREX 2025, NSK Ltd. introduced thin-section ball bearings and rotary actuators designed to minimize energy loss in autonomous robots, a critical factor for battery-powered mobility. These systems rely on high-fidelity sensor bearings that optimize motion control while reducing overall system power draw.

The EV segment is equally strategic. At the Japan Mobility Show 2025, NSK debuted a sensor-integrated deep groove ball bearing that cuts outer diameter by 10% and weight by 51%, while maintaining high-speed feedback for traction and braking systems. Targeting ¥4 billion in annual sales by 2030, NSK is scaling globally—aiming for 10 million units per year by 2026 for ball-screw electric brakes that depend on real-time bearing feedback—cementing Japan’s role in compact, low-friction sensor bearing architectures.

United States: Wireless Condition Monitoring and Aerospace Resilience

The U.S. sensor bearing market is being reshaped by wireless Industrial IoT integration and renewed aerospace sovereignty. In April 2024–2025, The Timken Company launched a wireless sensor and condition monitoring platform using mesh networking to transmit vibration and temperature data without hardwiring. This architecture reduces installation complexity and eliminates recurring fees, accelerating adoption across U.S. manufacturing plants pursuing Industry 4.0 retrofits.

Aerospace remains a parallel growth engine. In late 2025, SKF (with significant U.S. operations) introduced ARCTIC15, a high-temperature, corrosion-resistant steel engineered for aeroengine sensor bearings. Designed for next-generation engines targeting 20–25% fuel efficiency gains, ARCTIC15 supports integrated speed and thermal sensing at extreme operating limits. By late 2024, U.S. industrial data showed a 19% rise in IIoT connections, with one-third of new bearing installations featuring predictive monitoring—underscoring America’s pivot toward wireless, data-centric bearings.

Sweden & Italy: Super-Precision Sensor Bearing Excellence

Northern and Southern Europe are converging into a single super-precision manufacturing ecosystem under SKF’s global reorganization. In September 2025, SKF inaugurated its Airasca Center of Excellence in Italy—a fully automated, digitally connected facility dedicated to high-speed sensorized bearings. This site integrates R&D, prototyping, and final assembly, serving as SKF’s global hub for spindle bearings, electric motor sensors, and ultra-precision applications.

Concurrently, SKF redesigned its industrial organization to form a Specialized Industrial Solutions unit focused on emerging technologies such as magnetic bearings and sensor-rich motor systems. Sustainability underpins this strategy: in November 2025, SKF launched The Patent Bay from its Gothenburg headquarters, sharing low-friction and energy-efficient bearing designs to accelerate decarbonization—positioning Europe as the innovation center for precision sensor bearings.

China: Electrification Scale and Specialized e-Axle Bearings

China is transitioning from volume production to application-specific sensor bearings, aligned with its massive EV and robotics markets. In May 2025, NTN Corporation began mass production of resin-mold insulated sensor bearings for e-Axles, preventing electrical pitting in high-voltage EV systems—a critical reliability issue as China’s electrified fleet scales.

Strategic realignment followed. In November 2025, Schaeffler divested its Chinese turbocharger business (~€100 million) to refocus domestic operations on humanoid robotics and Physical-AI ecosystems, partnering with robotics specialists. China’s Dongguan plant has also been designated a global hub for sensor-integrated electric-hydraulic brake systems, supporting the 10 million unit global capacity target by 2026—highlighting China’s role in high-volume, specialized sensor bearing production.

France: Aerospace MRO and Digital Human–Machine Interfaces

France is carving out leadership in the digital layer of sensor bearings, particularly for aerospace Maintenance, Repair, and Overhaul (MRO). In November 2025, NTN Europe announced a multi-year investment through 2030 to modernize its digital ecosystem, emphasizing man–machine collaboration and sensor-driven diagnostics across its plants.

With over 30 years of expertise in CFM56 engine bearings, NTN Europe is expanding into LEAP and GTF engines, where embedded sensors enable real-time health monitoring and lifecycle optimization. Complementing this industrial push, France’s Forindustrie 2025 initiative is deploying digital twins to train engineers in maintaining sensor-integrated aerospace bearings, reinforcing France’s position as a hub for high-value, data-driven bearing services.

2025 Strategic Matrix: Sensor Bearing Market by Country

Sensor Bearing Market Matrix

|

Country

|

Primary Market Focus

|

2025 Strategic Milestone

|

Key Material / Technology

|

|

Germany

|

Humanoid robotics & high-speed rail

|

Planetary gear actuator & Velaro Novo records

|

Sensorized axlebox & encoder units

|

|

Japan

|

EV compactness & low friction

|

NSK thin-section & EV deep-groove launches

|

Low-friction sensor bearings

|

|

United States

|

Wireless IIoT & aerospace

|

Timken wireless monitoring; ARCTIC15 steel

|

Wireless sensors; aero-grade steels

|

|

Italy / Sweden

|

Super-precision automation

|

Airasca Center of Excellence launch

|

High-speed spindle sensor bearings

|

|

China

|

e-Axle electrification & scale

|

Resin-mold insulated bearing mass production

|

Insulated EV sensor bearings

|

|

France

|

Aerospace MRO & digital twins

|

NTN Europe 2030 digital ecosystem

|

Engine-integrated sensor bearings

|

Sensor Bearing Market Report Scope

Sensor Bearing Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$11.9 Billion

|

|

Market Size (2035)

|

$19.2 Billion

|

|

Market Growth Rate

|

4.9%

|

|

Segments

|

By Functionality (Speed Sensing, Position / Displacement Sensing, Temperature Monitoring, Vibration & Shock Sensing, Load / Force Sensing), By Bearing Type (Ball Sensor Bearings, Roller Sensor Bearings, Magnetic Sensor Bearings, Linear Sensor Bearings), By Application (Automotive, Industrial, Aerospace, Railway, Robotics)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

SKF Group, Schaeffler Group, NSK Ltd., NTN Corporation, Timken Company, JTEKT Corporation, ABB Group, Nachi-Fujikoshi Corp., MinebeaMitsumi Inc., Fersa Bearings, ZWZ, C&U Group, LYC Bearing Corporation, NRB Bearings, Rexnord

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Sensor Bearing Market Segmentation

By Functionality

- Speed Sensing

- Position / Displacement Sensing

- Temperature Monitoring

- Vibration & Shock Sensing

- Load / Force Sensing

By Bearing Type

- Ball Sensor Bearings

- Roller Sensor Bearings

- Magnetic Sensor Bearings

- Linear Sensor Bearings

By Application

- Automotive

- Industrial

- Aerospace

- Railway

- Robotics

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Sensor Bearing Market

- SKF Group

- Schaeffler Group

- NSK Ltd.

- NTN Corporation

- Timken Company

- JTEKT Corporation

- ABB Group

- Nachi-Fujikoshi Corp.

- MinebeaMitsumi Inc.

- Fersa Bearings

- ZWZ

- C&U Group

- LYC Bearing Corporation

- NRB Bearings

- Rexnord

*- List not Exhaustive