Mineral-Based Durability and Corrosion Protection Driving Sustainable Growth

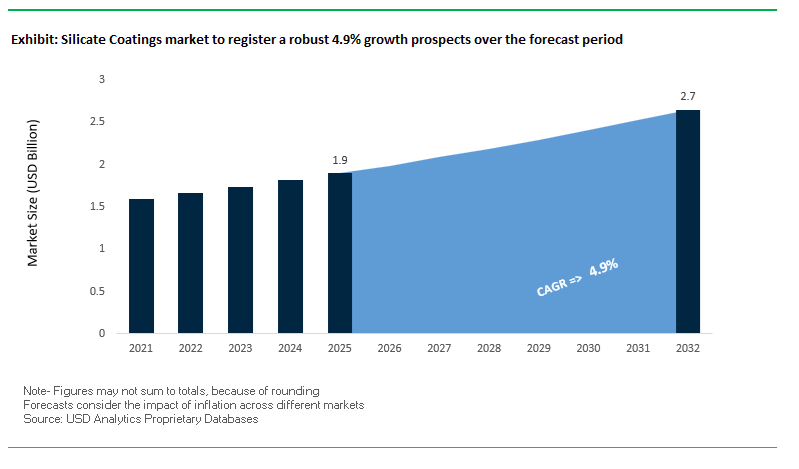

The global Silicate Coatings Market is witnessing steady expansion, underpinned by rising demand for mineral-based, breathable, and highly durable coating systems across construction, infrastructure, and industrial applications. The market was valued at $1.9 billion in 2025 and is projected to reach $2.7 billion by 2032, growing at a CAGR of 4.9% during 2025–2032. This growth trajectory reflects the increasing preference for inorganic coating technologies, particularly potassium and lithium silicate systems, which offer superior adhesion to mineral substrates, UV stability, and long-term durability.

A core structural driver is the growing emphasis on low-VOC, environmentally compliant coatings, especially in Europe and North America. Silicate coatings inherently align with sustainability mandates due to their mineral composition, non-film-forming nature, and extended lifecycle performance, making them ideal for green building certifications and heritage restoration projects. Additionally, their breathability and resistance to microbial growth make them highly suitable for historic structures, façades, and moisture-sensitive substrates.

Another significant growth factor is the rising adoption of inorganic zinc-silicate coatings in industrial and marine sectors. These coatings provide exceptional corrosion resistance, particularly for steel structures exposed to harsh environments such as offshore platforms, bridges, and energy infrastructure. The global push toward “Green Steel” production and infrastructure decarbonization is further accelerating demand for high-performance silicate primers that ensure extended asset life with minimal maintenance.

The market is also benefiting from advancements in hybrid silicate systems, where traditional mineral coatings are enhanced with silicone or polymer additives to improve water repellency, flexibility, and weather resistance without compromising breathability. This hybridization trend is expanding the applicability of silicate coatings into more demanding climates and modern construction requirements, positioning them as a critical component in sustainable and high-performance building materials.

Market Analysis: Hybrid Silicate Innovation, Corrosion Standards Compliance, and Strategic Localization Driving Competitive Momentum

The competitive landscape of the silicate coatings market is being shaped by material innovation, regulatory alignment, and geographic expansion strategies, as manufacturers respond to evolving performance and sustainability requirements. In March 2026, Wacker Chemie introduced SILRES® BS 6922, a functional silicone additive designed to enhance the water repellency of silicate coatings while preserving their intrinsic breathability. This innovation supports the growing demand for hybrid silicate systems, particularly in regions facing extreme weather conditions.

Industrial demand for corrosion protection continues to drive capacity expansion. In March 2026, PPG announced the expansion of its inorganic zinc-silicate production to meet rising demand for products such as Dimetcote®. This move is closely tied to new infrastructure mandates in the U.S. and Europe, where high-performance coatings are required for “Green Steel” structures, reinforcing the strategic importance of silicate primers in next-generation infrastructure projects.

Regulatory developments are playing a critical role in shaping product innovation. Following the January 2026 update to ISO 12944 corrosion protection standards, leading manufacturers including AkzoNobel and Jotun initiated the reformulation of their silicate-based shop primers to comply with stricter VOC limits and durability classifications. This reflects a broader industry shift toward compliance-driven innovation, where performance and environmental standards converge.

Strategic localization is emerging as a key growth lever, particularly in high-potential markets. Keimfarben’s September 2025 licensing agreement with Zydex Industries in India enables localized production of advanced silicate mineral paints, targeting the rapidly expanding Indian infrastructure and restoration sector. This approach reduces supply chain complexity while enhancing market penetration in emerging economies.

In marine and energy applications, silicate coatings are gaining traction due to their thermal resistance and anti-corrosive properties. AkzoNobel’s December 2025 partnership with Winning Shipping in China and its involvement in deep-sea drilling vessel projects (2024–2025) highlight the deployment of silicate-based coatings in extreme operational environments, where durability and performance are critical.

Performance validation through real-world applications is further strengthening market confidence. BEECK Mineral Colours’ 2025 restoration projects using Renosil and Beeckosil systems demonstrate the long-term effectiveness of silicate coatings on diverse substrates, including commercial and heritage structures. Meanwhile, Sherwin-Williams reported strong growth in its Protective & Marine segment in 2025, driven by increased adoption of heavy-duty silicate primers and tank linings in industrial applications.

Additionally, innovations such as Dalton Enterprises’ QuickPatch H2O (November 2024) reflect the emergence of silicate-hybrid repair systems that enable rapid, chemically compatible surface preparation prior to coating application, improving workflow efficiency and coating performance.

Hempel’s “Accelerate to Win” strategy (January 2026) further reinforces the focus on asset-lifetime-extending technologies, with silicate-based anti-corrosive coatings playing a central role in achieving emission reduction targets across marine and energy sectors.

Market Trend: EPA 2026 VOC Regulations Position Silicate Coatings as Ultra-Low Emission Benchmark for Architectural Applications

The 2025/2026 update to the U.S. Environmental Protection Agency’s National Volatile Organic Compound (VOC) Emission Standards is accelerating the transition toward inorganic coating technologies, with silicate coatings emerging as a structurally compliant solution for mineral substrates. The revised regulatory cap of 50 g/L VOC across most architectural coating categories places significant pressure on conventional acrylic and latex systems, which often require reformulation to remain compliant. In contrast, potassium silicate coatings inherently operate at VOC levels below 1 g/L, exceeding regulatory thresholds by more than 95%, positioning them as a future-proof coating technology in low-emission construction ecosystems. This intrinsic advantage is driving increased adoption in green building certifications and government-funded infrastructure projects where VOC minimization is a critical procurement parameter. Additionally, silicate coatings meet stringent vapor permeability benchmarks exceeding 30 perms under ASTM E96, enabling effective moisture diffusion through mineral substrates such as concrete and masonry. This breathability significantly reduces the risk of moisture entrapment, which is directly associated with a 15% to 20% increase in spalling and substrate degradation in non-permeable coating systems. As building envelope design increasingly prioritizes durability and moisture management, silicate coatings are becoming a preferred specification in both new construction and refurbishment of mineral-based structures.

Market Trend: EU CPR 2026 Enforcement Accelerates Adoption of Non-Combustible and Low-Carbon Silicate Coatings

The enforcement of the revised EU Construction Products Regulation (CPR) in January 2026 is fundamentally reshaping façade coating specifications, with a strong emphasis on mineral compatibility, fire safety, and lifecycle carbon performance. Silicate coatings, which chemically bond with mineral substrates through a silicification process, are gaining prominence as a compliant and high-performance alternative to organic coatings. Under the EN 13501-1 fire classification system mandated by CPR 2026, silicate coatings consistently achieve A2-s1, d0 ratings, confirming their non-combustible nature and minimal smoke emission. This is particularly critical in high-rise residential and commercial construction, where insurance providers and regulatory authorities are increasingly restricting the use of combustible façade materials. In parallel, lifecycle assessment requirements under EN 15804+A2 are reinforcing the environmental advantages of silicate coatings, which demonstrate a 30% to 40% lower Global Warming Potential compared to silicone-resin and acrylic alternatives. This reduction is primarily attributed to the absence of petroleum-derived binders and lower embodied carbon in mineral-based raw materials. As sustainability metrics become embedded in permitting processes and investor-driven ESG frameworks, silicate coatings are transitioning from niche applications in heritage restoration to mainstream adoption in modern, energy-efficient building systems.

Market Opportunity: Lithium Silicate Densifiers Advancing High-Performance Concrete Flooring in Automated Industrial Facilities

The rapid expansion of gigafactories, automated warehouses, and high-throughput logistics hubs is creating strong demand for advanced concrete densification technologies, with lithium silicate formulations emerging as the preferred solution. Unlike sodium and potassium silicates, lithium silicate offers a smaller molecular structure that enables deeper penetration into the concrete matrix while avoiding expansion-related defects such as Alkali-Silica Reaction. Performance evaluations indicate that lithium silicate densifiers can increase the surface hardness of standard 3,000 psi concrete by 35% to 45% on the Mohs scale, significantly reducing dust generation and surface wear in high-traffic industrial environments. This is particularly relevant for facilities operating Autonomous Mobile Robots, where surface integrity directly impacts operational efficiency and maintenance cycles. Furthermore, treated surfaces maintain a Dynamic Coefficient of Friction exceeding 0.42 under wet conditions, meeting ANSI A326.3 safety standards and reducing slip-related risks. Advanced formulations introduced in 2026 achieve penetration depths of 5 mm to 8 mm, forming a permanent crystalline structure within the concrete substrate. This eliminates issues associated with delamination and coating failure commonly observed in topical sealers, which typically degrade within 18 to 24 months under heavy mechanical stress. As industrial operators prioritize lifecycle durability and safety compliance, lithium silicate densifiers are becoming a critical specification in next-generation flooring systems.

Market Opportunity: Ethyl Silicate Zinc-Rich Primers Expanding Role in Corrosion Protection for Critical Infrastructure

Ethyl silicate-based inorganic zinc-rich primers are gaining strategic importance in 2026 as infrastructure owners seek high-performance corrosion protection systems for bridges, ports, and industrial steel assets. These coatings function through a cathodic protection mechanism, effectively acting as a sacrificial zinc layer that prevents substrate corrosion even in aggressive environments. Modern inorganic zinc-rich primer formulations are required to contain a minimum of 85% zinc by weight in the dry film, in accordance with ASTM D520 Type II standards, enabling over 15,000 hours of salt spray resistance under ASTM B117 testing protocols when used within a multi-coat system. In addition to corrosion resistance, ethyl silicate binders offer rapid curing characteristics, achieving tack-free status within 15 to 30 minutes at moderate humidity levels. This significantly enhances throughput in fabrication facilities, reducing total coating cycle times by approximately 25% compared to conventional epoxy-based systems. Thermal stability is another key advantage, with ethyl silicate coatings maintaining structural integrity at temperatures up to 400°C, making them suitable for applications in transit infrastructure, petrochemical facilities, and exhaust-exposed steel structures. As global investment in resilient infrastructure accelerates, ethyl silicate zinc-rich primers are positioned as a high-value solution within the protective coatings segment, combining durability, efficiency, and compliance with stringent performance standards.

Silicate Coatings Market Share and Segmentation Insights: Mineral-Based Architectural Applications and Distributor-Led Supply Networks

By Application: Architectural Mineral Wall Coatings Lead with Breathability and Eco-Friendly Performance

The architectural wall coatings (mineral paint) segment dominated the silicate coatings market with a 34.5% share in 2025, driven by its superior breathability, long-term durability, and sustainability advantages. Silicate coatings based on potassium silicate and sodium silicate chemistry chemically bond with mineral substrates such as masonry, brick, concrete, and render, creating a highly durable and weather-resistant surface. A key differentiator is their vapor permeability, allowing water vapor to escape while preventing moisture buildup, making them ideal for historic building restoration, heritage structures, and modern eco-friendly construction projects. Additionally, silicate paints are completely free from VOCs, organic solvents, and biocides, aligning with stringent green building standards and sustainable architecture trends. This combination of non-toxic formulation, exceptional longevity, and compatibility with mineral substrates continues to drive strong adoption in both residential and commercial construction, reinforcing the segment’s leadership in the global silicate coatings market.

By Distribution Channel: Industrial Wholesalers and Distributors Lead with Professional Supply and Bulk Project Support

The industrial wholesalers and distributors segment accounted for a leading 41.1% share of the silicate coatings market in 2025, reflecting the specialized nature of these coatings and their reliance on professional application expertise. Silicate coatings require specific substrate preparation, pH compatibility, and application techniques, as they lack organic binders and behave differently from conventional paints. As a result, they are primarily distributed through industrial channels that cater to professional contractors, plasterers, and facade specialists. These distributors provide not only bulk packaging options such as pails, drums, and intermediate bulk containers (IBCs) but also technical field support and training, ensuring proper application and performance. Additionally, large-scale projects such as facade renovation, concrete densification, and heritage restoration rely on wholesalers for consistent supply, logistics efficiency, and on-site support. This strong alignment with professional users and project-scale demand solidifies the dominance of distributor-led channels in the global silicate coatings market.

Competitive Landscape of the Silicate Coatings Market

AkzoNobel Disrupts Market with Scaled Silicate Technology and Professional Training Ecosystem

AkzoNobel N.V. is emerging as a major force in the silicate coatings market, leveraging its industrial scale to bring mineral coatings into the mainstream. In 2026, the company launched the Dulux Trade Pure Silicate range in the DACH region, offering up to a 25-year performance guarantee for exterior applications. Its strong financial performance, with a 14.5% EBITDA margin, supports investment in high-margin sustainable coatings. AkzoNobel has also developed a certified applicator training network across 45 centers, ensuring proper application of technically demanding silicate systems. Its planned merger with Axalta further strengthens its global coatings portfolio.

KEIM Maintains Market Leadership with Pure Silicate Innovation and Sustainability Excellence

KEIM-Farben GmbH is the benchmark player in the silicate coatings market, particularly in heritage and premium construction segments. Its Soldalit® range dominates the sol-silicate segment, combining silica-sol and potassium silicate binders for superior substrate bonding. KEIM’s coatings are defined by zero VOCs, zero plasticizers, and Cradle-to-Cradle Gold certification, aligning with growing demand for sustainable materials. With architectural applications accounting for over 68% of market revenue, KEIM’s focus on high-performance eco-friendly solutions reinforces its leadership.

Sherwin-Williams Expands Market Reach with Infrastructure-Focused Silicate Technologies

The Sherwin-Williams Company is leveraging its extensive distribution network to scale silicate coatings in commercial and infrastructure markets. Its expanded manufacturing capacity supports growth in mineral-based coatings, while its General Industrial division is advancing silicate-zinc primers for corrosion protection and fire resistance. The company’s strong financial position enables continued investment in innovation and market expansion, particularly in large-scale infrastructure projects.

PPG Drives Innovation with Multifunctional Silicate Coatings for Data Centers and Infrastructure

PPG Industries, Inc. is a key innovator in the silicate coatings market, focusing on multifunctional solutions. Its latest developments include silicate-based thermal barrier coatings for data centers, reducing cooling loads by up to 15%. The company is also strengthening its focus on high-performance coatings through strategic divestments, allowing greater investment in advanced silicate technologies. PPG’s expertise in protective and marine coatings positions it strongly in infrastructure and energy sectors.

BEECK Strengthens Technical Leadership with Pure Silicate Formulation Expertise and Healthy Building Solutions

Beeck'sche Farbwerke GmbH (BEECK) is a specialist leader in the silicate coatings market, focusing on pure silicate formulations. Its Active Silicate Formulation (ASF) process creates a permanent chemical bond with substrates, preventing peeling and enhancing durability. The company is expanding into Asia-Pacific markets, targeting high-growth regions. BEECK’s naturally alkaline coatings provide inherent mold and bacteria resistance, aligning with the “healthy building” movement. Its investment in photocatalytic technologies further enhances its position in sustainable construction.

Nippon Paint Drives APAC Growth with Cost-Effective Silicate Solutions and Urban Renewal Focus

Nippon Paint Holdings Co., Ltd. is a dominant player in the Asia-Pacific silicate coatings market, leveraging its scale and localized strategy. With strong revenue growth and a 43% regional market share, the company is promoting dispersion silicate paints as cost-effective alternatives to traditional coatings. Its innovations include silicate-modified protective films under the n-SHIELD brand, offering enhanced durability and UV resistance. Nippon Paint’s focus on urban renewal and public housing projects positions it strongly in high-growth markets.

Germany Leading Mineral-Based Silicate Coatings Innovation with AI-Driven Petrification Technologies

Germany stands as the global benchmark in the silicate coatings market, driven by its leadership in mineral-based coating technologies and sustainable construction practices. The transition toward advanced sol-silicate hybrid coatings is transforming the architectural coatings landscape, particularly with the integration of AI-driven rheology modeling that ensures optimal silicification and 100% bonding with mineral substrates.

The country’s strong regulatory push toward zero-VOC coatings under Green Building Certification frameworks such as DGNB is accelerating demand for inorganic silicate coatings with natural mold resistance. Strategic developments, including major acquisitions in the mineral coatings space, highlight the industry’s shift toward specialized high-performance solutions. Germany is also pioneering photocatalytic silicate coatings capable of neutralizing harmful urban pollutants such as NOx and SO₂, supporting smart city initiatives. Infrastructure programs like the Renovation Wave are further boosting demand for breathable silicate finishes in heritage restoration, while circular manufacturing processes are enhancing sustainability by reducing energy consumption in potassium silicate production.

China Scaling High-Performance Silicate Coatings for Green Infrastructure and Industrial Applications

China is rapidly expanding its footprint in the global silicate coatings market, shifting toward environmentally compliant and high-value inorganic coating solutions. Government-backed initiatives such as the Green Building Materials Plan (2025–2026) are accelerating the adoption of low-emission mineral coatings, aligning domestic production with international sustainability standards.

Infrastructure expansion is a key driver, with extensive use of zinc-silicate primers in maritime ports to combat corrosion in saline environments. Large-scale projects such as the South-to-North Water Diversion initiative are boosting demand for potassium silicate-based sealants that enhance concrete durability. The country is also modernizing manufacturing processes, with a significant proportion of producers adopting energy-efficient electric fusion technologies. Additionally, the integration of silicate coatings in agriculture as eco-friendly protective layers is reducing dependence on chemical pesticides. Enhanced standardization efforts are aligning Chinese products with global certifications, strengthening export potential.

United States Driving High-Purity Silicate Coatings Demand in Semiconductor and Infrastructure Sectors

The United States silicate coatings market is being reshaped by the growing demand for high-performance coatings in advanced industries such as semiconductors, electric vehicles, and infrastructure. Technological advancements include the development of nano-enhanced silicate coatings offering superior thermal stability and scratch resistance for EV battery applications.

Infrastructure investments under federal programs are driving demand for zinc-silicate anti-corrosive coatings in bridge retrofitting and steel protection. Regulatory tightening under the Clean Air Act is encouraging the adoption of zero-VOC mineral paints in sensitive environments such as hospitals and schools. Product innovations such as cool roof silicate coatings with high solar reflectance are gaining traction in heat-prone regions. Additionally, increased investments in colloidal silica production are supporting domestic semiconductor manufacturing growth, while the marine sector is benefiting from biocide-free silicate foul-release coatings that improve efficiency and environmental compliance.

Japan Advancing Nano-Silica Coatings for Electronics, Automotive, and Precision Applications

Japan is a global leader in nano-silica coatings technology, focusing on precision engineering applications across electronics, automotive, and advanced materials sectors. Innovations in nano-scale fumed silica additives are addressing traditional brittleness challenges, enabling flexible and durable silicate coatings for high-performance applications.

The country is leveraging silicate coatings in EV lightweighting and fire-resistant automotive components, while high-purity formulations are supporting semiconductor manufacturing processes such as chemical mechanical planarization. Advanced manufacturing techniques, including AI-based particle size monitoring, are ensuring consistent product quality. Japan is also investing in disaster-resilient infrastructure through seismic-resistant mineral coatings, enhancing structural durability. Cross-sector innovations, including the use of silicate technologies in eco-friendly packaging and consumer applications, further demonstrate Japan’s leadership in high-value coating solutions.

Saudi Arabia Driving Demand for High-Temperature Silicate Coatings in Mega Infrastructure Projects

Saudi Arabia is emerging as a high-growth market in the silicate coatings industry, driven by large-scale infrastructure developments under Vision 2030. The deployment of silicate coatings in projects such as NEOM is driven by their ability to withstand extreme heat conditions exceeding 50°C, making them ideal for desert environments.

The energy sector is a major application area, with widespread adoption of high-heat silicate coatings to prevent corrosion under insulation in refineries. Sustainability initiatives under the Saudi Green Initiative are promoting the use of solvent-free silicate coatings, aligning with environmental goals. Additionally, the expansion of desalination infrastructure is driving demand for silicate-based concrete densifiers to enhance durability. Product innovations such as self-cleaning silicate facades are further improving maintenance efficiency by leveraging high UV exposure to break down pollutants, reinforcing Saudi Arabia’s role as a key market for extreme-environment coatings.

India Emerging as a High-Growth Market for Silicate Coatings in Infrastructure and Sustainable Construction

India is witnessing significant growth in the silicate coatings market, driven by urbanization, infrastructure expansion, and increasing demand for sustainable construction materials. Government initiatives such as the Smart Cities Mission are promoting the use of breathable mineral coatings for public infrastructure and heritage preservation, ensuring long-term durability.

Manufacturing expansion, particularly in silica production, is supporting the growing demand for high-performance silicate coatings across industries. The adoption of zinc-silicate primers in railway infrastructure projects is enhancing corrosion protection, while the use of silicate floor hardeners is increasing in logistics and warehousing facilities. Regulatory frameworks such as BIS standards are formalizing quality benchmarks for inorganic coatings, boosting market confidence. Additionally, the rising consumer preference for eco-friendly natural paints is driving demand for dispersion silicate coatings in urban residential markets, positioning India as a key growth hub in the global silicate coatings industry.

Silicate Coatings Market Report Scope

Silicate Coatings market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1.9 Billion

|

|

Market Size (2032)

|

$2.7 Billion

|

|

Market Growth Rate

|

4.9%

|

|

Segments

|

By Product (Zinc Silicate Coatings, Potassium Silicate Coatings, Sodium Silicate Coatings, Lithium Silicate Coatings, Ethyl Silicate Coatings, Specialized Hybrid Silicates), By Coating Type (Pure Silicate Coatings, Dispersion Silicate Coatings, Calcified Silicate Coatings, Sol-Silicate Coatings), By Application (Anti-Corrosion Primers, Architectural Wall Coatings, Concrete Hardening and Densification, High-Temperature, Substrate Consolidation), By End-User Industry (Construction and Infrastructure, Marine and Offshore, Automotive and Transportation, Industrial Manufacturing, Aerospace and Defense), By Distribution Channel (Direct-to-Contractor, Industrial Wholesalers and Distributors, Specialized Retail Stores, Online)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

KEIM Mineral Paints, PPG Industries, Inc., Akzo Nobel N.V., Nippon Paint Holdings Co., Ltd., Teknos Group, Jotun Group, The Sherwin-Williams Company, Kansai Paint Co., Ltd., Wacker Chemie AG, Remmers Gruppe SE, BEECK Mineral Paints, Asian Paints Limited, Sika AG, Benjamin Moore and Co., Silacote USA LLC

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Silicate Coatings Market Segmentation

By Product

- Inorganic Zinc-Rich

- Organic Zinc-Rich

- Potassium Silicate Coatings

- Sodium Silicate Coatings

- Lithium Silicate Coatings

- Ethyl Silicate Coatings

- Specialized Hybrid Silicates

By Coating Type

- Pure Silicate Coatings

- Dispersion Silicate Coatings

- Calcified Silicate Coatings

- Sol-Silicate Coatings

By Application

- Anti-Corrosion Primers

- Architectural Wall Coatings

- Interior Decorative

- Exterior Facade

- Concrete Hardening and Densification

- High-Temperature

- Substrate Consolidation

By End-User Industry

- Construction and Infrastructure

- Marine and Offshore

- Automotive and Transportation

- Industrial Manufacturing

- Aerospace and Defense

By Distribution Channel

- Direct-to-Contractor

- Industrial Wholesalers and Distributors

- Specialized Retail Stores

- Online

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Silicate Coatings Industry

- KEIM Mineral Paints

- PPG Industries, Inc.

- Akzo Nobel N.V.

- Nippon Paint Holdings Co., Ltd.

- Teknos Group

- Jotun Group

- The Sherwin-Williams Company

- Kansai Paint Co., Ltd.

- Wacker Chemie AG

- Remmers Gruppe SE

- BEECK Mineral Paints

- Asian Paints Limited

- Sika AG

- Benjamin Moore & Co.

- Silacote USA LLC

*- List not Exhaustive