Silver Salt Market Valuation 2025–2034: $1.9 Billion to $3.7 Billion at 7.7% CAGR Supported by PV Metallization, Pharmaceutical APIs, and High-Purity Electronics

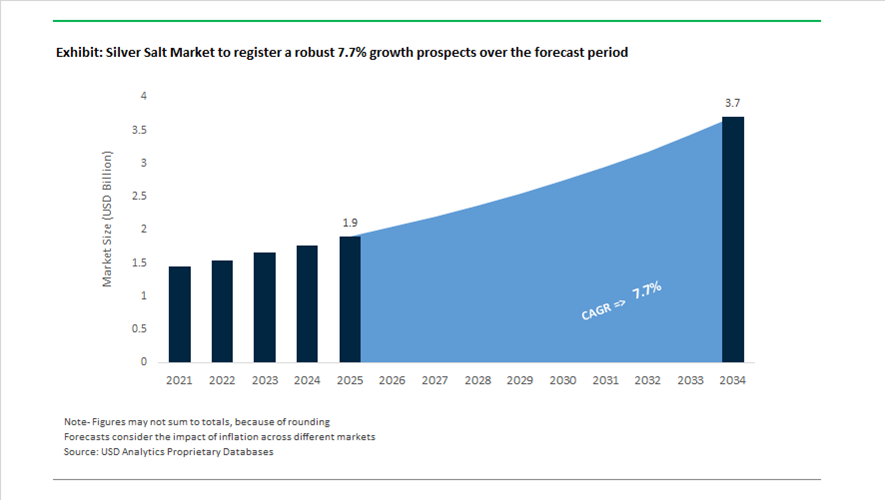

The global silver salt market is valued at $1.9 billion in 2025 and is projected to reach $3.7 billion by 2034, registering a CAGR of 7.7%. Growth is driven by expanding demand for high-purity silver nitrate, silver oxide, silver sulfate, and specialty silver precursors used in photovoltaic (PV) metallization pastes, conductive adhesives, semiconductor plating solutions, antimicrobial coatings, pharmaceutical active ingredients (APIs), and advanced catalysts. Silver salts function as critical intermediates for synthesizing silver powders, silver nanoparticles, and silver-coated conductive materials, making supply stability and refining integration central to market competitiveness. Rising silver prices and volatile treatment charges (TCs) are accelerating structural shifts in vertical integration and silver thrifting technologies.

In February 2024, researchers at the University of California, Riverside announced a breakthrough cancer biosensor utilizing silver nanoparticles synthesized from high-purity silver nitrate. This innovation reinforced demand for ultra-refined silver salt precursors in biomedical diagnostics and nanomaterial applications. During 2024–2025, the merger integration of Ames Goldsmith and Pyromet was finalized, creating a consolidated refining and silver chemical platform with enhanced capabilities in silver nitrate and silver oxide production. The integration strengthened supply reliability for medical-grade and electronics-grade silver salts, positioning the combined entity as a key supplier to semiconductor plating and antimicrobial markets.

Throughout 2025, structural capacity expansion and vertical integration reshaped the competitive environment. In March 2025, Shanghai Metals Market reported a surge in domestic silver nitrate capacity in China, driven by explosive demand for PV silver powder used in solar cell metallization. At the same time, downstream silver paste producers in China pursued independent silver nitrate production qualifications to secure raw material supply and mitigate rising processing fees. In mid-2025, Heraeus Precious Metals expanded its specialty silver chemicals capacity in Dresden under the Silicon Saxony cluster, targeting 5G infrastructure and semiconductor fabrication applications that rely on silver salts for conductive plating and interconnect materials. In late 2025, Ames Goldsmith introduced silver-coated copper (AgCu) flakes derived from silver salt precursors, enabling electronics manufacturers to reduce silver content by 30–50% while maintaining conductivity standards.

Strategic investments and technological substitution trends intensified in 2026. In November 2025, Johnson Matthey announced the commissioning phase of its new precious metals and PGM refinery, scheduled to become fully operational by 2027, significantly enhancing its ability to supply ultra-high-purity silver precursors for industrial catalysts and pharmaceutical synthesis. In January 2026, AIKO confirmed achieving 10 GW of silver-free mass production at its Zhuhai facility using copper electroplating technology, signaling a competitive challenge to traditional silver salt demand in PV metallization. In February 2026, Silox India secured funding for its Dahej expansion project to increase output of specialized inorganic chemicals, including silver-based catalysts used in pharmaceutical manufacturing. These developments highlight the dual forces shaping the silver salt market through 2034: high-growth electronics and biomedical applications driving purity requirements upward, while material substitution and silver thrifting strategies exert pricing and volume pressures across the value chain.

Silver Salt Market Trends and Opportunities: Supply Deficit, Medical-Grade Demand, and Electronics-Driven Growth

Structural Shift from Photographic Decline to High-Value Specialty Silver Halide Applications

The Silver Salt market is undergoing a structural demand realignment, where declining consumer photographic usage is being offset by sustained demand in industrial radiography and medical imaging applications. While traditional film photography has transitioned into a niche segment, silver-halide-based specialty films continue to demonstrate strong relevance in sectors requiring archival permanence, high resolution, and tamper-proof traceability.

In industrial environments, particularly aerospace and nuclear power, Non-Destructive Testing (NDT) continues to rely on silver-based radiographic films compliant with standards such as ASTM E94. These films provide long-term record integrity, a critical requirement for certifying structural components. Similarly, in healthcare, analog X-ray imaging systems remain operational in cost-sensitive diagnostic centers, where silver halide films deliver superior contrast and diagnostic accuracy compared to digital substitutes in certain use cases.

A parallel trend strengthening supply-side dynamics is the emergence of silver recovery from spent radiographic films, which contain approximately 1.5% to 2% silver content. With silver prices reaching historic highs in early 2026, closed-loop recycling systems achieving 90% to 99% recovery efficiency are becoming a vital secondary feedstock source. This is reinforcing a circular supply chain model within the silver salt market, particularly for high-purity silver nitrate and silver chloride production.

Silver Bullion Scarcity and Price Volatility Reshaping Procurement Strategies

The Silver Salt market is increasingly influenced by macroeconomic volatility and persistent supply deficits in silver bullion, creating pricing pressure across the value chain. In February 2026, The Silver Institute confirmed the sixth consecutive year of global silver deficit, estimated at 67 million ounces, driven by strong industrial demand and declining above-ground inventories in key trading hubs.

Silver prices surged to a record $83.64 per ounce in early 2026, introducing a new layer of financial market-driven volatility into what was traditionally an industrial raw material supply chain. Heightened geopolitical tensions and rising sovereign debt levels have amplified silver’s role as a safe-haven asset, increasing speculative inflows and disrupting pricing predictability for silver salt manufacturers.

To manage this volatility, producers and downstream users are transitioning from Just-in-Time procurement models to strategic inventory buffering, with stockpiles extended to 6–8 weeks of supply. This shift reflects a broader trend toward risk-mitigated sourcing strategies, where supply assurance and price hedging are becoming critical operational priorities. Consequently, silver salt pricing is increasingly dictated by global bullion market dynamics, reinforcing the need for integrated procurement and financial risk management frameworks.

Rising Demand for Antimicrobial Silver Salts in Advanced Wound Care and Medical Devices

The healthcare sector represents the most robust growth avenue for the Silver Salt market, driven by rising cases of chronic wounds, hospital-acquired infections (HAIs), and antimicrobial resistance. Silver salts, particularly silver nitrate, are gaining widespread adoption in advanced wound care formulations and antimicrobial medical coatings, due to their broad-spectrum bactericidal properties.

Clinical data highlights the effectiveness of silver-infused dressings in managing bioburden in chronic wounds, including diabetic foot ulcers and pressure ulcers. These formulations inhibit the formation of drug-resistant biofilms, positioning silver salts as a critical component in modern wound management protocols. This is driving demand for high-purity, medical-grade silver nitrate, particularly in regulated healthcare markets.

Beyond wound care, silver salts are increasingly integrated into antimicrobial coatings for medical devices, including catheters and surgical instruments. This trend is supported by a global push to reduce infection rates in clinical settings. Innovations in controlled-release technologies are further enhancing product performance. Companies such as Imbed Biosciences are advancing synthetic matrix dressings with controlled ionic silver release, enabling localized antimicrobial action while minimizing systemic toxicity risks. These advancements are accelerating regulatory approvals and expanding the addressable market for silver salts in clinical applications.

Expansion of Silver-Based Conductive Inks for Printed Electronics and Solar Applications

The rapid evolution of printed electronics, flexible devices, and renewable energy systems is creating a high-growth opportunity for silver salts as precursors in conductive ink formulations. By early 2026, the electronics sector accounted for over 60% of total industrial silver consumption, underscoring its dominance as a demand driver.

Silver-based conductive inks are preferred due to their ability to achieve up to 80% of bulk metallic silver conductivity, making them essential for precision circuit printing, semiconductor packaging, and advanced interconnect technologies. The expansion of 5G infrastructure, IoT ecosystems, and wearable healthcare devices is further accelerating demand for flexible and stretchable electronic components enabled by silver inks.

In parallel, the solar photovoltaic (PV) industry remains a critical consumption segment. Despite ongoing efforts to reduce silver usage through thrifting, conductive silver inks remain indispensable for front-side metallization and interconnection in high-efficiency solar cells. The global push toward renewable energy and decarbonization is sustaining long-term demand for silver-based materials in PV manufacturing.

Additionally, emerging applications such as in-mold electronics and flexible biosensors are expanding the functional scope of silver salts in next-generation device architectures. These innovations require materials with high adhesion, mechanical flexibility, and electrical performance, positioning silver salts as a foundational component in the future of flexible and printed electronics markets.

Silver Salt Market Share and Segmentation Insights

Silver Nitrate Leads Market as Core Precursor for Catalysts, Reagents, and Specialty Silver Compounds

Silver nitrate accounted for 38% of the Silver Salt Market by product type in 2025, reflecting its role as the primary precursor for manufacturing a wide range of silver compounds and its extensive use in analytical chemistry, catalysis, and industrial chemical synthesis. It is widely utilized in chemical manufacturing, laboratory titration processes, and specialty applications requiring high reactivity and purity. Silver nitrate serves as the backbone of the silver chemicals value chain, supporting downstream production of silver oxide, silver halides, and other derivatives. In 2025, growing demand for silver-based catalysts and specialty chemicals continues to reinforce its dominance, while adjacent segments such as silver oxide benefit from increasing use in button cell batteries and wearable electronics.

Electronics Segment Drives Silver Salt Demand with Strong Growth in Photovoltaics and Advanced Devices

Electronics accounted for 30% of the Silver Salt Market by application in 2025, driven by rising demand for silver-based materials in photovoltaic cells, semiconductors, and electronic components. Silver salts are essential in metallization pastes used in solar panels, making the electronics sector a key growth engine for the market. Expansion of renewable energy infrastructure and solar installations continues to support high consumption levels. Additionally, miniaturization of electronic devices and growth in wearable technologies contribute to demand for silver oxide batteries. In 2025, increasing integration of silver materials in energy storage and next-generation electronics is strengthening market relevance, offsetting the long-term decline in traditional photography-related applications.

Silver Salt Market Competitive Landscape

The 2026 silver salt market is shaped by elevated silver prices and resilient demand from semiconductors, photovoltaics, and diagnostics. Industry leaders are prioritizing silver-thrifting technologies, closed-loop recycling, and localized refining to ensure stable supply of high-purity silver nitrate, silver oxide, and conductive materials.

Tanaka scales hybrid sintering silver technologies and localized IVD integration in Asia

Tanaka Precious Metals is expanding its footprint in semiconductor-grade silver salts through strategic entry into India and Southeast Asia, aligning with localized electronics manufacturing trends. Its TS-985 hybrid sintering silver adhesive combines metallic and hydrogen bonding to deliver superior thermal conductivity for Generation 7 IGBT modules. The company is strengthening its diagnostics segment by integrating silver-based colloidal reagents into a full IVD manufacturing system, reducing lead times by 30%. Tanaka is also advancing its circular supply chain through expanded precious metal recycling operations under its Renaissance Plan. Its vertically integrated model supports consistent production of high-purity silver nitrate and bonding materials for power electronics and medical applications.

Heraeus advances silver-thrifting pastes and closed-loop refining for PV and electronics

Heraeus Precious Metals is focusing on optimizing silver utilization amid price volatility, with projections placing silver between $43 and $62 per ounce in 2026. The company is developing advanced silver-thrifting pastes for TOPCon and HJT solar cells to reduce material consumption while maintaining conversion efficiency. Its closed-loop refining model enables industrial clients to recycle silver waste into ultra-high-purity silver salts for electroplating and semiconductor applications. Heraeus is also expanding production of conductive inks for 5G and IoT infrastructure, where purity and conductivity are critical. Its integrated services span refining, trading, and advanced materials engineering for high-growth electronics and energy applications.

Ames Goldsmith deploys AgCu technologies and expands refining to offset high silver costs

Ames Goldsmith is addressing rising silver prices through silver-thrifting innovations such as silver-coated copper (AgCu) and high-aspect-ratio silver flakes. These materials enable manufacturers to maintain conductivity while significantly reducing silver content in conductive adhesives and pastes. The integration of Pyromet and Silver Phoenix has expanded its refining capacity in the U.S., ensuring stable supply of silver nitrate and silver oxide. The company is also entering green hydrogen markets with silver-based materials for fuel cells and electrolysis systems. Its portfolio includes applications across medical imaging, aerospace, and traditional photography alongside advanced electronics.

Metalor expands global refining and ESG traceability with digital transparency platforms

Metalor Technologies has expanded its global refining network with the commissioning of its Hong Kong facility, supporting electronics manufacturing in the Greater Bay Area. The acquisition of Gannon & Scott increases its presence in North American e-waste recycling and precious metal recovery. Its Swiss Precious Metals Transparency Platform (SPMTP) enables traceability of silver used in electroplating salts, addressing ESG and compliance requirements. The company is prioritizing production of silver cyanide and silver potassium cyanide for precision electroplating applications. Its operations are closely aligned with demand from high-reliability electronics and luxury finishing sectors.

Mitsubishi Materials scales circular recovery and AI-driven innovation in silver salt production

Mitsubishi Materials is expanding silver recovery from e-waste and IT asset disposal streams through its Resource Circulation Division. The company is applying materials informatics to identify dopants that enhance performance in photocatalysts and antimicrobial silver compounds. Increasing the ratio of recycled inputs in refining operations is improving cost efficiency amid elevated silver prices. Its Electronic Materials segment focuses on high-purity silver nitrate and low-thermal-expansion composites for automotive sensors and power modules. Expansion in the United States supports broader recovery and refining capabilities across global markets.

United States Silver Salt Market Reinforced by Thrifting Technologies and Federal-Backed Purity Expansion

The United States silver salt industry is undergoing structural recalibration as cost pressure, semiconductor localization, and defense procurement converge. In October 2025, Ames Goldsmith Corporation announced advancements in silver-coated copper systems designed to reduce absolute silver intensity in conductive adhesives. These AgCu innovations directly respond to silver prices approaching USD 50 per ounce, enabling performance parity with traditional silver nitrate-derived systems while materially improving cost efficiency across electronics and photovoltaic formulations. This thrifting-driven innovation is becoming a defining capability for U.S. silver salt suppliers as downstream customers demand conductivity optimization rather than pure metal loading.

Federal policy has further strengthened domestic positioning. Following CHIPS Act subsidy disbursements, U.S.-based producers have expanded ultra-high-purity silver nitrate and silver salt production lines to support advanced wafer metallization at newly commissioned logic and memory mega-fabs. Beyond electronics, strategic mineral integration has emerged as a differentiator. In late 2025, Americas Gold and Silver Corporation partnered with the U.S. government to advance antimony processing at the Galena Complex, enabling access to co-elements critical for advanced alloy salts used in defense and aerospace systems. Defense demand is also rising for silver-based antimicrobial coatings and silver-salt electrolytes in high-reliability thermal batteries. Regulatory oversight is tightening in parallel, with the EPA’s 2025 updates mandating stricter recovery protocols for silver chloride waste, accelerating investment in closed-loop silver salt recovery technologies. Innovation momentum remains visible, as Technic Inc. showcased next-generation engineered silver powders and salts at LOPEC 2025 and TechBlick Boston, targeting flexible electronics and additively manufactured circuitry.

Germany Silver Salt Market Anchored by Recycling Scale and Hydrogen Economy Integration

Germany’s silver salt market is distinguished by its leadership in precious metal recycling, hydrogen technologies, and regulated specialty applications. Heraeus Holding GmbH announced a planned €300 million investment through 2026 to expand global recycling capacity, with a specific emphasis on recovering silver from industrial catalysts. This recycled feedstock is increasingly redirected into high-purity silver salt production, reducing exposure to primary metal volatility while aligning with Europe’s circular economy mandates.

Strategically, silver salts are becoming embedded in Germany’s hydrogen value chain. In March 2025, Heraeus entered a technology partnership with Freudenberg e-Power Systems to develop catalyst-coated membranes for PEM fuel cells, where high-purity silver and platinum salts enhance electrochemical efficiency and durability. Medical technology has also emerged as a growth vector. Heraeus’ January 2025 acquisition of Umicore’s platinum-containing APIs business signals a broader expansion into high-value medical metal salts, including silver-based wound-care and antimicrobial formulations. Sustainability commitments reinforce competitiveness, as Heraeus transitioned its precious metal salt operations toward 100% green electricity by end-2025. On the regulatory front, German manufacturers standardized low-toxicity silver halide variants in 2025 to remain compliant with evolving EU chemical safety directives affecting consumer photography and film applications.

Japan Silver Salt Market Defined by Lithography Purity and Advanced Energy Applications

Japan remains a critical global hub for ultra-high-purity silver salts, closely linked to semiconductor lithography, electric mobility, and next-generation energy systems. In late 2025, Shin-Etsu Chemical finalized an ¥83 billion investment in Gunma to produce silver-based photoresists and silver salt precursors essential for EUV lithography. This facility reinforces Japan’s role in supplying contamination-controlled silver nitrate and derivative salts required for sub-5 nm semiconductor manufacturing.

Energy transition applications are expanding silver salt demand beyond semiconductors. In early 2025, Wacker Asahikasei Silicone inaugurated a Tsukuba facility producing silver-filled thermal interface materials for 800V EV power modules, where silver salts function as conductive additives supporting heat dissipation. In photovoltaics, Japanese R&D centers have pivoted from conventional silver paste toward silver-salt-based transparent conductive films designed for perovskite solar cells, reflecting a shift toward material efficiency and optical performance. Surface finishing innovation continues as Technic Japan introduced cyanide-free semi-bright silver salts in late 2025, enabling safer electronics plating chemistries. Additionally, Japanese smart grid pilot programs are deploying silver-based electrolytes to improve conductivity and resilience in high-voltage transmission systems.

China Silver Salt Market Shaped by Policy Protectionism and Infrastructure-Scale Consumption

China’s silver salt industry is characterized by aggressive capacity scaling, policy-driven localization, and infrastructure-led consumption. Metalor Technologies announced plans to expand its Suzhou site by 2026, consolidating and enlarging operations to strengthen production of high-technology silver coatings and chemical solutions. This move aligns with China’s broader objective of securing domestic supply chains for precious metal derivatives.

Policy intervention is a defining feature. In September 2025, China’s Ministry of Commerce amended import rules for select silver and precious metal codes, shifting them from free to restricted status through March 2031 to protect domestic refining capacity. Demand fundamentals remain robust, as China continues to be the world’s primary consumer of nano-silver salts for 5G antenna coatings, supporting nationwide urban 5G coverage targets. Environmental enforcement is simultaneously intensifying. The Ministry of Ecology and Environment’s 2025 directives mandate a 95% recovery rate for silver from chemical manufacturing wastewater, compelling large-scale silver nitrate producers to upgrade effluent recovery systems. Renewable energy remains a major pull factor, with record solar installations in 2025 driving consumption of silver-nitrate-derived pastes and incentivizing upstream integration into silver salt production by domestic manufacturers.

Comparative Snapshot: Country-Level Silver Salt Industry Dynamics

Silver Salt Market County Level Snapshot

|

Country

|

Core Demand Drivers

|

Strategic Focus Areas

|

Regulatory and Policy Influence

|

|

United States

|

Semiconductors, defense, flexible electronics

|

Silver thrifting, UHP purity, domestic integration

|

CHIPS Act, EPA recovery mandates

|

|

Germany

|

Recycling, hydrogen, medical technologies

|

Circular silver salts, PEM fuel cell catalysts

|

EU chemical safety directives

|

|

Japan

|

EUV lithography, EV power modules, grid tech

|

Ultra-high purity photoresists, energy-grade additives

|

Industrial materials security

|

|

China

|

5G infrastructure, solar PV, refining

|

Capacity expansion, upstream integration

|

Import restrictions, 95% recovery rules

|

Silver Salt Market Report Scope

Silver Salt Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1.9 Billion

|

|

Market Size (2034)

|

$3.7 Billion

|

|

Market Growth Rate

|

7.7%

|

|

Segments

|

By Product Type (Silver Nitrate, Silver Chloride, Silver Bromide, Silver Iodide, Silver Fluoride, Silver Carbonate, Silver Oxide, Silver Sulfate), By Form (Crystalline & Powder, Aqueous Solutions, Granular, Colloidal & Nano-Dispersions), By Application (Electronics, Chemical Manufacturing, Medical & Healthcare, Photography & Imaging, Energy, Glass & Mirrors)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Ames Goldsmith Corporation, Heraeus Holding GmbH, Technic Inc., Metalor Technologies SA, Shin-Etsu Chemical Co. Ltd., Johnson Matthey PLC, Dowa Holdings Co. Ltd., Umicore NV, American Elements, Tanaka Precious Metals, BASF SE, Merck KGaA, Asahi Holdings Inc., Mitsubishi Materials Corporation, Hubei BlueSky New Material Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Silver Salt Market Segmentation

By Product Type

- Silver Nitrate

- Silver Chloride

- Silver Bromide

- Silver Iodide

- Silver Fluoride

- Silver Carbonate

- Silver Oxide

- Silver Sulfate

By Form

- Crystalline & Powder

- Aqueous Solutions

- Granular

- Colloidal & Nano-Dispersions

By Application

- Electronics

- Chemical Manufacturing

- Medical & Healthcare

- Photography & Imaging

- Energy

- Glass & Mirrors

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Silver Salt Industry

- Ames Goldsmith Corporation

- Heraeus Holding GmbH

- Technic Inc.

- Metalor Technologies SA

- Shin-Etsu Chemical Co. Ltd.

- Johnson Matthey PLC

- Dowa Holdings Co. Ltd.

- Umicore NV

- American Elements

- Tanaka Precious Metals

- BASF SE

- Merck KGaA

- Asahi Holdings Inc.

- Mitsubishi Materials Corporation

- Hubei BlueSky New Material Inc.

*- List not Exhaustive