Single Point Anchor Reservoir Market Size, Overview, and Growth Outlook (2025–2034)

Deepwater and Ultra-Deepwater Expansion Propels the Global Single Point Anchor Reservoir Market Toward $7.6 Billion by 2034

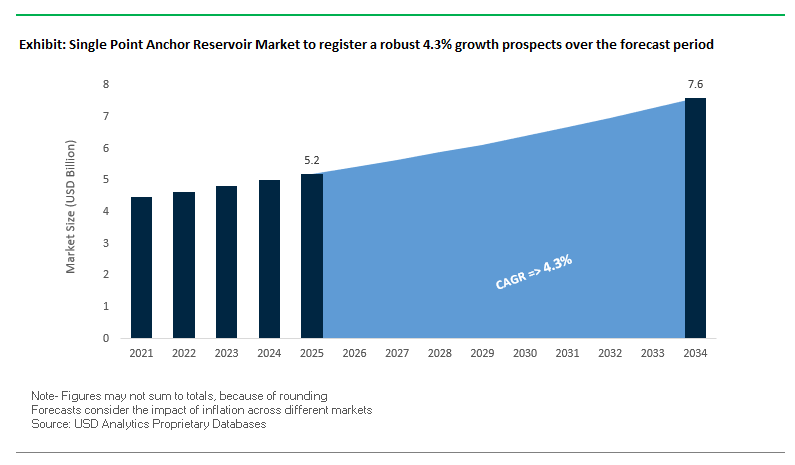

The global single point anchor reservoir (SPAR) market is projected to grow from $5.2 billion in 2025 to $7.6 billion by 2034, reflecting a CAGR of 4.3%, driven by deepwater and ultra-deepwater offshore oil and gas development, technological innovation, and operational efficiency requirements. SPAR platforms are increasingly adopted for water depths exceeding 5,000 feet, providing stable and reliable solutions where conventional fixed platforms are not feasible.

Key Insights for Industry Professionals:

- Deepwater Dominates Deployment: Over 85% of SPAR installations are in the Gulf of Mexico, demonstrating a strong concentration in ultra-deepwater fields.

- Buoyancy and Stability as Core Advantages: Cylindrical hulls provide exceptional resistance to wind, waves, and currents, ensuring operational reliability for drilling and production.

- High-Pressure Technology Unlocks New Resources: Chevron’s Anchor project operates at up to 20,000 psi, enabling extraction from previously inaccessible reservoirs.

- On-Site Storage and Riser Protection Enhance Flexibility: SPARs offer enclosed hull storage for oil or gas and protect critical risers, a key differentiator from other floating platforms.

- Operational Efficiency and Technological Advancement: Companies are leveraging advanced engineering and design innovations to reduce downtime and maximize production in challenging offshore environments.

SPARs remain essential for industry professionals and investors seeking to optimize deepwater production capabilities, minimize environmental risk, and leverage high-performance offshore technologies.

Market Analysis: Strategic Acquisitions and Technological Milestones Are Reshaping the Single Point Anchor Reservoir Industry

The SPAR market has experienced significant technological innovation, mergers, and operational expansions, underscoring its critical role in offshore oil and gas production. In August 2024, Chevron commenced oil and gas production from the Anchor project in the Gulf of Mexico, deploying its first 20,000 psi deepwater technology, a milestone demonstrating both reliability and operational innovation. February 2023 saw MODEC complete the topsides integration of the Carioca FPSO, the world’s largest SPAR platform, destined for Brazil’s Mero field, highlighting increasing scale and engineering complexity.

In July 2025, Chevron completed the acquisition of Hess Corporation, expanding its deepwater portfolio and consolidating its presence in key basins. Other industry moves include European companies acquiring U.S.-based high-performance adhesive specialists in July 2025, mergers creating a $1.4 billion reusable packaging leader in February 2025, and Vessl Inc.’s Development Agreement with Tempra Technology in January 2025 to optimize self-heating packaging technologies.

Single Point Anchor Reservoir (SPAR) Market: Trends and Opportunities Driving Offshore Energy Transformation

Strategic Deployment in Deepwater Gas Development and LNG Export

The Single Point Anchor Reservoir (SPAR) market is witnessing strong demand from deepwater gas development projects and LNG export infrastructure. SPAR platforms are increasingly selected for mega-projects that require stability, deck space, and subsea integration capacity. Shell’s Perdido platform in the Gulf of Mexico is a benchmark for this trend. Operational since 2010, it serves as a hub for multiple offshore fields—Great White, Tobago, and Silvertip—processing up to 200 million cubic feet of natural gas per day. This demonstrates the ability of SPAR structures to serve as centralized processing facilities for extensive subsea tie-backs, enabling scalable offshore development.

The SPAR design provides exceptional stability in deepwater environments, with a large deck area to accommodate heavy gas processing modules and LNG pre-treatment units. This inherent advantage is especially valuable for operators looking to develop complex, capital-intensive offshore projects. As LNG export markets expand—driven by Asia-Pacific demand and European energy diversification—SPARs are becoming integral in supporting large-scale subsea tie-back networks and ensuring the reliability of deepwater natural gas supply chains.

Life Extension and Brownfield Retrofitting for Mature Assets

A second major trend is the life extension of existing SPAR platforms and retrofitting of brownfield offshore assets to maximize production. Operators are shifting away from costly decommissioning toward enhancing recovery and leveraging existing infrastructure. For example, BP’s Atlantis Phase 3 development, sanctioned in 2019 with a $1.3 billion investment, added a new subsea production system tied to the existing platform, unlocking an additional 400 million barrels of oil equivalent.

Projects like Atlantis Drill Centre 1 Expansion (DC1X) and expansions at Mad Dog field show the industry’s strategy of using existing manifolds, risers, and topside facilities to access untapped reserves. This approach avoids building entirely new infrastructure while capturing additional hydrocarbons, extending the economic life of offshore fields. For the SPAR market, this trend creates sustained demand for retrofitting solutions, subsea integration, and structural upgrades that optimize mature asset performance in a cost-efficient way.

Integration of Digital Twin and Advanced Analytics for Predictive Maintenance

The complex, capital-intensive nature of SPAR platforms makes them a prime candidate for digital twin and advanced analytics deployment. By creating a virtual replica of offshore assets and integrating real-time sensor data, operators can predict maintenance needs, optimize uptime, and improve long-term financial performance. A 2025 case study highlighted how a digital twin system deployed on an offshore facility reduced downtime, identified inefficiencies, and cut inspection costs significantly.

Quantitative research supports its financial viability. An MIT-sponsored 2024 thesis modeled digital twin adoption for deepwater facilities, showing an improved Net Present Value (NPV) of $211 million over 27 years through predictive maintenance and reduced reliance on costly physical inspections. For the SPAR market, the adoption of digital twin solutions represents a transformative opportunity to extend asset lifespans, reduce operational risks, and boost returns on investment in deepwater oil and gas operations.

Design Adaptation for Carbon Capture and Storage (CCS) Hubs

As the energy transition accelerates, a promising opportunity lies in repurposing SPAR infrastructure for carbon capture and storage (CCS). Instead of decommissioning, operators can transform SPAR hulls and subsea systems into permanent CO₂ storage hubs. A 2025 article from World Oil emphasized the potential of converting decommissioning liabilities into revenue-generating assets by reusing offshore wells for CO₂ injection.

Industry leaders such as Aker Solutions are already advancing this opportunity. With decades of subsea expertise, Aker is re-engineering subsea equipment for CO₂ injection, as demonstrated in the Northern Lights CCS project in Norway, operational since September 2024. For the SPAR market, CCS adaptation not only creates a new revenue stream but also positions SPAR platforms as critical infrastructure in the net-zero economy, ensuring their relevance well beyond traditional oil and gas extraction.

Competitive Landscape: Leading SPAR Manufacturers Are Driving Deepwater Innovation, High-Pressure Technology, and Offshore Operational Efficiency

The global SPAR market is dominated by highly specialized offshore engineering and production companies, leveraging advanced technology, project execution capabilities, and sustainability initiatives to maintain leadership.

SBM Offshore N.V.: Pioneering Floating Production Solutions with Fast4Ward® and Advanced SPAR Platforms

SBM Offshore provides SPARs, FPSOs, and TLPs with a focus on safety, efficiency, and performance optimization. Its Fast4Ward® FPSO units standardize deepwater field development and reduce project delivery times. The company continues to secure major FPSO contracts globally and invests in floating wind and wave energy projects as part of its New Energy segment, reflecting innovation and diversification.

Chevron Corporation: Expanding Deepwater SPAR Portfolio with Industry-First High-Pressure Technology

Chevron is a leading operator and investor in SPAR developments, including the Anchor project, which operates at 20,000 psi, enabling access to ultra-deepwater resources. The company strengthened its portfolio with the Hess Corporation acquisition in July 2025. Chevron focuses on affordable, reliable, and lower-carbon energy solutions, combining innovation with operational excellence in deepwater production.

Technip Energies N.V.: Delivering Engineering Excellence and Sustainable Offshore Solutions

Technip Energies provides SPARs, FPSOs, and FLNG systems, backed by advanced engineering and project management capabilities. Its EcoLutions portfolio emphasizes sustainability, and proprietary FLNG technology enables at-sea gas liquefaction. The company’s focus on innovative offshore solutions supports the energy transition while ensuring safe and efficient project delivery.

Hyundai Heavy Industries Co., Ltd.: Leveraging Shipbuilding Expertise for Complex Offshore SPAR Projects

Hyundai Heavy Industries offers SPARs, FPSOs, semi-submersibles, and offshore wind foundations. Its core strength lies in shipbuilding and offshore engineering capabilities, allowing delivery of large-scale, complex projects on schedule. The company focuses on strategic partnerships and product innovation to maintain leadership in offshore production systems.

Mitsubishi Heavy Industries, Ltd.: Integrating Engineering Excellence for SPARs and Renewable Offshore Solutions

Mitsubishi Heavy Industries delivers a wide range of floating production systems, including SPARs and FPSOs, leveraging its engineering and technological expertise. Its strategic focus spans offshore oil and gas, renewable energy, and nuclear power, providing integrated solutions for deepwater operations while ensuring efficiency, safety, and sustainability.

Single Point Anchor Reservoir Market Share Insights, 2025-2034

Truss SPAR Leads Market Share by Type in the Single Point Anchor Reservoir (SPAR) Industry

Truss SPAR platforms command 60% of the global SPAR market, cementing their role as the industry’s preferred deepwater production solution. Their dominance is a direct result of their structural efficiency, reduced steel requirements, and adaptability across a wide range of water depths compared to conventional cylindrical hulls. By replacing heavy solid sections with a lighter truss framework, this design significantly lowers CAPEX while maintaining stability and payload capacity, aligning with operator goals to optimize project economics in ultra-deepwater fields. The growing concentration of offshore investment in regions like the U.S. Gulf of Mexico, Brazil, and West Africa reinforces demand for truss SPARs, as these areas prioritize scalable, cost-effective floating production systems. Conventional SPARs remain in legacy fleets, and Cell SPARs serve niche environments, but the truss design defines the future trajectory of the SPAR platform market.

Marine Oil Drill Stations Dominate Market Share by Application in the SPAR Platform Industry

Marine oil drill stations account for 90% of SPAR platform applications, reflecting the sector’s almost exclusive reliance on SPARs for deepwater oil and gas production. Their exceptional motion stability, capacity to host heavy topsides, and compatibility with dry-tree wells make them indispensable for ultra-deepwater drilling and production, where conventional floating solutions face technical or economic limitations. These characteristics provide operators with a stable, long-term production asset that can support both drilling and processing while reducing intervention costs. Other theoretical applications—such as buoys, research stations, and communication hubs—hold negligible shares due to the prohibitively high CAPEX of deploying billion-dollar SPAR infrastructure outside oil and gas. As such, SPAR platforms remain strategically linked to global offshore energy investment cycles, with marine oil drill stations defining the overwhelming majority of industry demand.

United States: Regulatory Pressure and Digitalization Driving SPAR Adoption

The United States SPAR market is strongly shaped by the Bureau of Safety and Environmental Enforcement (BSEE), which enforces stringent standards for offshore oil and gas operations in the Outer Continental Shelf (OCS). These regulations include detailed requirements for equipment design, operational practices, and real-time monitoring systems, ensuring that SPAR platforms meet the highest standards of safety and environmental compliance. The Gulf of Mexico remains the epicenter of U.S. deepwater and ultra-deepwater exploration, with projects like the Shell Perdido SPAR, operating at 2,438 meters, setting benchmarks as the world’s deepest platform.

A key market trend is the integration of digital twin technology and real-time monitoring systems to improve offshore operational efficiency and enhance safety. Companies are investing heavily in AI-driven predictive maintenance and automated inspection systems, which help reduce downtime and minimize operational risks in SPAR deployments. Furthermore, the U.S. Department of the Interior continues to push for advanced safety and environmental safeguards in offshore drilling, directly influencing the design, technology adoption, and sustainability features of upcoming SPAR installations.

Brazil: Pre-Salt Field Developments Fueling Large-Scale SPAR Projects

The Brazil SPAR market is expanding rapidly due to the country’s pre-salt fields, which require advanced floating production systems for deep and ultra-deepwater operations. These reserves are among the most promising globally, creating significant demand for large-scale SPAR platforms. In February 2023, Modec completed the topsides integration of the Carioca FPSO, the world’s largest SPAR platform, designed for the Mero field offshore Brazil. This milestone highlights both the scale of engineering complexity and the level of capital investment in the region.

Petrobras, the state-owned energy giant, is the leading force in Brazil’s SPAR market, driving numerous projects in the pre-salt layer. Its investments are setting global benchmarks for deepwater engineering and floating production systems. Additionally, Brazil’s focus on sustainable industry practices, such as reverse logistics regulations, is shaping supply chain accountability, which may influence future component packaging, recycling, and material use in SPAR construction and maintenance.

Norway: Strong Regulatory Framework and Hybrid Energy for SPAR Platforms

The Norway SPAR market is driven by both government regulations and strong industrial expertise. Aker Solutions was awarded a FEED (Front-End Engineering and Design) contract by Statoil for the Aasta Hansteen field, which includes the world’s largest SPAR platform in the Norwegian Sea. This project underscores Norway’s role as a pioneer in deepwater SPAR deployment.

The Norwegian government has established one of the world’s most comprehensive regulatory frameworks for offshore operations, emphasizing safety, reliability, and environmental sustainability. A significant trend is the push toward hybrid power solutions, such as integrating renewable energy sources with offshore oil platforms, to reduce emissions and improve operational efficiency. Moreover, the Norwegian Petroleum Directorate (NPD) is promoting exploration in new parts of the Norwegian Continental Shelf, further driving demand for SPAR-based deepwater solutions.

China: Expanding Offshore Exploration and Rising Demand in the South China Sea

The China SPAR market is gaining momentum as the country expands its offshore exploration activities, particularly in the South China Sea, to meet its growing energy demand. The National Development and Reform Commission (NDRC) and the Ministry of Ecology and Environment (MEE) are also advancing sustainability through stricter pollution control measures under the 14th Five-Year Plan.

Alongside oil and gas investments, the Chinese government is promoting remanufacturing industries and green technologies, offering tax incentives to companies that adopt environmentally sustainable practices. This dual strategy of energy expansion and green development is likely to encourage innovation in SPAR platform design, focusing not only on operational performance but also on sustainability and reduced environmental footprint.

India: Licensing Policies and Incentives for Deepwater Exploration

The India SPAR market is being supported by the government’s Hydrocarbon Exploration and Licensing Policy (HELP), which establishes a uniform licensing system for all hydrocarbons. This policy encourages greater exploration in deepwater and ultra-deepwater fields, creating future opportunities for SPAR platforms.

The Directorate General of Hydrocarbons (DGH) is overseeing domestic exploration and production with a goal of maximizing output and reducing crude import dependency. Additionally, India’s concessional royalty regime for deepwater and ultra-deepwater fields is a major incentive, encouraging foreign and domestic investments in offshore exploration. These policy measures are gradually positioning India as a potential SPAR market in the Asia-Pacific region.

Canada: Offshore Petroleum Acts Supporting Safe and Sustainable SPAR Deployment

The Canada SPAR market operates under the Canada Petroleum Resources Act and the Canada Oil and Gas Operations Act, which regulate offshore oil and gas activities in federally controlled waters. These acts emphasize safety, environmental protection, and conservation of resources, aligning with Canada’s broader energy transition goals.

Key regulatory oversight comes from the Canada-Newfoundland and Labrador Offshore Petroleum Board and the Canada-Nova Scotia Offshore Petroleum Board, which manage shared jurisdiction with the federal government. While Canada’s offshore production is not as extensive as that of the U.S. or Brazil, the regulatory environment ensures that future SPAR installations will be developed under stringent environmental and operational standards, making the Canadian market reliable and compliance-driven for SPAR adoption.

Single Point Anchor Reservoir Market Report Scope

Single Point Anchor Reservoir Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$5.2 Billion

|

|

Market Size (2034)

|

$7.6 Billion

|

|

Market Growth Rate

|

4.3%

|

|

Segments

|

By Type (Conventional SPAR, Truss SPAR, Cell SPAR), By Application (Marine Oil Drill Station, Buoy, Marine Research Station, Maritime Communication Transfer Station), By Depth (Shallow Water, Deepwater, Ultra-deepwater)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

TechnipFMC PLC, SBM Offshore N.V., Aker Solutions, Bluewater Energy Services B.V., Modec Inc., Samsung Heavy Industries Co., Ltd., Hyundai Heavy Industries Co., Ltd., Mitsubishi Heavy Industries, Ltd., Bumi Armada Berhad, Technip Energies N.V., Baker Hughes Company, Halliburton, ExxonMobil, Shell, BP

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Single Point Anchor Reservoir Market Segmentation

By Type

- Conventional SPAR

- Truss SPAR

- Cell SPAR

By Application

- Marine Oil Drill Station

- Buoy

- Marine Research Station

- Maritime Communication Transfer Station

By Depth

- Shallow Water

- Deepwater

- Ultra-deepwater

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Single Point Anchor Reservoir Market

- TechnipFMC PLC

- SBM Offshore N.V.

- Aker Solutions

- Bluewater Energy Services B.V.

- Modec Inc.

- Samsung Heavy Industries Co., Ltd.

- Hyundai Heavy Industries Co., Ltd.

- Mitsubishi Heavy Industries, Ltd.

- Bumi Armada Berhad

- Technip Energies N.V.

- Baker Hughes Company

- Halliburton

- ExxonMobil

- Shell

- BP

* List Not Exhaustive

Methodology

USDAnalytics employs a robust and integrated research methodology to deliver actionable insights into the global Single Point Anchor Reservoir (SPAR) market. Our analysis combines extensive secondary research from industry publications, company disclosures, regulatory frameworks, and offshore engineering journals, with primary insights obtained from interviews with offshore engineers, energy project managers, and technology providers. Market sizing and forecasts are segmented by platform type (Conventional, Truss, Cell SPAR), application (Marine Oil Drill Stations, Buoys, Research Stations, Communication Transfer Stations), and water depth (Shallow, Deepwater, Ultra-Deepwater), while also evaluating adoption trends across key regions including the U.S., Brazil, Norway, China, India, and Canada. USDAnalytics closely examines growth drivers such as deepwater and ultra-deepwater exploration, high-pressure extraction technologies, digital twin integration for predictive maintenance, and sustainability initiatives including CCS adaptation and hybrid offshore energy solutions. Competitive intelligence covers strategic mergers, acquisitions, and technological innovations by leading players such as SBM Offshore, Chevron, Technip Energies, Hyundai Heavy Industries, and Mitsubishi Heavy Industries, providing industry professionals with actionable insights to optimize offshore operations, enhance safety, and improve economic returns in capital-intensive SPAR deployments.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.