Sludge Treatment Chemicals Market Valuation 2025–2034: $10.5 Billion to $17.3 Billion at 5.7% CAGR Driven by Advanced Dewatering Polymers and PFAS Compliance

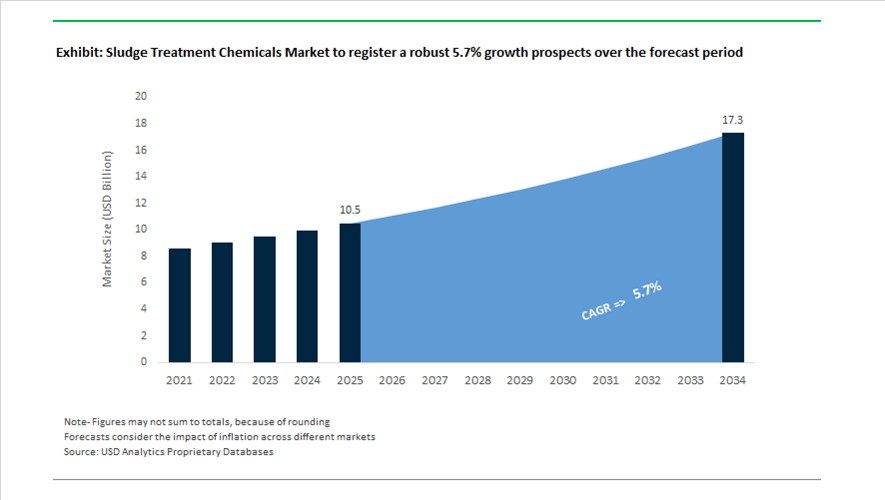

The global sludge treatment chemicals market is valued at $10.5 billion in 2025 and is projected to reach $17.3 billion by 2034, registering a CAGR of 5.7%. Growth is supported by increasing municipal wastewater generation, stricter effluent discharge norms, PFAS and micropollutant removal mandates, industrial sludge recycling requirements, and rising adoption of high-performance flocculants, coagulants, ferric salts, lime stabilizers, and conditioning polymers. Advanced sludge dewatering polymers, cationic polyacrylamides, ferric chloride for phosphorus removal, and customized catalyst systems for advanced oxidation processes are becoming central to plant efficiency and regulatory compliance. Digitalization in wastewater management and the shift toward biodegradable polymer chemistries are reshaping procurement strategies across utilities and industrial treatment operators.

In January 2024, Solenis announced a $193 million expansion of its Virginia manufacturing site, strengthening production capacity for high-demand sludge dewatering polymers and clarification chemistries. In February 2024, Solenis and PhaBuilder initiated collaboration on polyhydroxyalkanoate-based flocculants, introducing biodegradable alternatives to conventional synthetic polymers for sludge conditioning. In July 2024, Kemira acquired Norit’s UK reactivation business, enhancing its integrated approach to activated carbon regeneration and PFAS removal from sludge streams. Early 2024 also saw Solenis acquire CedarChem, reinforcing its position in coagulants and flocculants for industrial wastewater treatment.

Strategic acquisitions and capacity expansion accelerated in 2025. In March 2025, India commissioned its first AI-powered sewage treatment plant, deploying machine learning algorithms for real-time adjustment of chemical dosing based on sludge density and inflow variability, improving polymer efficiency and reducing overdosing. In April 2025, Solenis completed the acquisition of NCH Corporation, significantly expanding its specialty water treatment portfolio across municipal and industrial sludge dewatering segments. In October 2025, SNF Group signed a €135 million agreement to acquire Syensqo’s Oil & Gas division, strengthening its technology portfolio for high-performance sludge conditioning polymers and friction reduction agents, with closure expected in Q1 2026. In November 2025, Veolia expanded its U.S. hazardous sludge treatment footprint through the acquisition of Clean Earth, enhancing recovery and specialized disposal capabilities.

Infrastructure investments and sustainability initiatives define the 2025–2026 outlook. Kemira’s ferric chloride capacity expansion in Tarragona, Spain, announced in late 2024 and scheduled for completion in 2026, targets growing EU demand for phosphorus removal and biogas digestion enhancement. BASF’s X3D® catalyst shaping technology, launched in late 2025, is being adapted for wastewater treatment applications, with a new German production facility expected to commence operations in 2026 to serve advanced oxidation processes. In March 2025, SNF Group reported EcoVadis Platinum status and disclosed that 92% of its 2024 revenues align with UN Sustainable Development Goals, alongside a target to reduce carbon footprint by 15% by 2030 via low-energy polymer manufacturing. These developments indicate that sustainability-driven polymer innovation, AI-enabled dosing optimization, integrated hazardous sludge services, and regulatory tightening on micropollutants are central forces shaping the sludge treatment chemicals market trajectory toward $17.3 billion by 2034.

Key Trends and High-Impact Opportunities in the Global Sludge Treatment Chemicals Market

Municipal Shift Toward High-Efficiency Dewatering Polymers to Control OPEX

Municipal wastewater treatment plants are under mounting financial pressure as landfill tipping fees and sludge transportation costs escalate across developed economies. In major urban regions of the United States and Europe, disposal-related expenses are projected to increase by 12 to 15% in 2025, forcing utilities to reassess sludge handling strategies at a system-wide level. As a result, municipalities are increasingly mandating the use of high-performance sludge dewatering chemicals that can materially increase cake solids content and reduce haulage volumes.

Operational data from early 2025 case studies indicate that improving cake dryness from a conventional 18% to beyond 25% delivers a disproportionate cost benefit. Each incremental one% increase in solids content can reduce total disposal costs by 5 to 8% due to lower transport frequency and reduced landfill mass. This economic multiplier is accelerating adoption of ultra-high molecular weight synthetic polymers engineered to deliver stronger floc formation and shear resistance in high-stress equipment such as centrifuges and belt filter presses. Policy support is reinforcing this trend. In May 2025, the U.S. Environmental Protection Agency issued guidance linked to the $2.5 billion FY 2025 Clean Water State Revolving Fund, explicitly encouraging utilities to deploy energy-efficient sludge management technologies. This federal signal is pushing chemical conditioning programs that lower downstream energy demand for thermal drying and incineration, repositioning advanced polymers as a strategic lever for long-term OPEX control rather than a consumable expense.

Industrial Zero Liquid Discharge Compliance Driving Demand for Specialized Coagulants

In parallel, industrial wastewater treatment is being reshaped by stricter water scarcity and discharge regulations, particularly in water-stressed regions. Mandates such as those enforced by the Central Pollution Control Board for the Ganga basin are compelling power generation, textile, and chemical manufacturers to adopt Zero Liquid Discharge architectures. These systems operate under extreme salinity and contaminant loads, rendering conventional coagulants and flocculants ineffective.

The power sector alone accounted for roughly 37% of ZLD-related chemical demand in 2024, driven by retrofitting of flue gas desulfurization streams with evaporators and crystallizers. These high-TDS environments require specialized coagulants and anti-scalants capable of maintaining performance in saturated brines while preventing fouling and scaling. Importantly, recent financial analysis published in November 2025 shows that ZLD investments now deliver an economic internal rate of return of approximately 16.38% when water reuse and avoided discharge penalties are accounted for. This reframes ZLD chemical programs from regulatory overhead into value-enabling components of financially viable water recycling assets.

Sludge-to-Carbon Conversion Enabled by CCU Pre-Treatment Chemicals

The emergence of sludge-derived biochar as both a carbon sequestration medium and a functional adsorbent is opening a new opportunity frontier for sludge treatment chemicals. Pyrolysis of conditioned wastewater sludge at temperatures between 500 and 700 degrees Celsius is gaining traction as a pathway to convert waste solids into stable carbon products used in wastewater polishing, soil amendment, and industrial adsorption.

Research published in early 2025 indicates that diverting sludge toward construction material substitution and alternative fuel pathways could reduce global carbon emissions by roughly 25 million tons annually. Achieving this outcome at scale depends on chemical pre-treatment solutions that enhance fixed carbon yield and control ash composition during thermal conversion. Beyond biochar, innovation is extending into bio-electrochemical systems. Studies in 2025 demonstrate that sludge-derived hydrochar can function as an electrocatalyst in Microbial Electrosynthesis platforms, enabling CO2 conversion into multi-carbon compounds. When sludge is conditioned with optimized chemical programs, carbon recovery efficiencies as high as 45.44% have been observed, positioning pre-treatment chemicals as a critical enabler of carbon capture and utilization strategies within the wastewater sector.

Accelerated Adoption of Bio-Based Flocculants in the Food and Beverage Industry

The food and beverage sector is emerging as the fastest-moving adopter of bio-based sludge treatment chemicals, driven by corporate ESG commitments and brand-led sustainability strategies. In 2024, F&B applications accounted for more than 29% of global sludge treatment chemical revenues, reflecting both high organic load generation and strong regulatory scrutiny. Leading producers are now actively replacing synthetic polyacrylamides with biodegradable alternatives such as bacteria-based flocculants, chitosan derivatives, and starch-based polymers.

This transition is not symbolic. Bio-based flocculants offer tangible downstream advantages, including non-toxicity and the ability to repurpose treated sludge as animal feed or organic fertilizer, directly supporting circular economy models. In March 2024, BASF expanded its bioflocculant manufacturing capacity at its Ludwigshafen site, signaling industrial-scale commitment to this shift. Looking forward, the bacteria-based bioflocculant segment alone is expected to generate an absolute dollar opportunity exceeding $1.3 billion over the next decade. For chemical suppliers, this represents a premium growth pathway where regulatory alignment, ESG value creation, and waste valorization converge into a durable competitive advantage.

Sludge Treatment Chemicals Market Share and Segmentation Insights

Flocculants Dominate the Sludge Treatment Chemicals Market for Efficient Sludge Dewatering

Flocculants accounted for 38.60% of the sludge treatment chemicals market in 2025, reflecting their essential role in wastewater sludge processing and solid-liquid separation. Most flocculants are high-molecular-weight polymers such as polyacrylamides, which bind suspended particles together to form larger flocs that settle or filter more easily during sludge treatment. These chemicals significantly improve sludge thickening, dewatering efficiency, and water recovery, reducing the overall volume of sludge that must be transported or disposed of. A key 2025 technology trend is the development of advanced cationic flocculants with tailored molecular weight and charge density, optimized for different sludge types including municipal biosolids, industrial wastewater sludge, and digested sludge, enabling higher cake solids and lower polymer dosage requirements.

Municipal Wastewater Treatment Drives Sludge Treatment Chemical Consumption

Municipal wastewater treatment plants represent the largest end-use segment in the sludge treatment chemicals market, accounting for 52.80% of global demand in 2025 due to the massive volumes of wastewater processed in urban infrastructure systems. These facilities generate significant quantities of sludge from residential, commercial, and institutional wastewater streams, requiring chemical treatment to enable effective sludge stabilization and disposal. Increasing population growth, urbanization, and stricter wastewater discharge standards continue to expand municipal treatment capacity worldwide. A major 2025 industry trend is the increasing focus on biosolids beneficial reuse, where treated sludge is converted into nutrient-rich biosolids for agricultural land application, driving demand for conditioning chemicals, stabilization agents, and pathogen reduction treatments to meet regulatory safety requirements.

Sludge Treatment Chemicals Market Competitive Landscape

The global sludge treatment chemicals market in 2026 is shaped by ultra-high-performance flocculants, AI-driven smart dosing, and circular sludge valorization strategies. Leading players are focusing on bio-based polymers, PFAS removal technologies, and integrated water management platforms to reduce disposal costs and enhance resource recovery efficiency.

Kemira Oyj Strengthens Bio-Based Flocculants and Circular Sludge Solutions for Municipal and Industrial Markets

Kemira Oyj leads the sludge treatment chemicals market with €2.8 billion in 2025 revenue, driven by strong demand in municipal wastewater and industrial water treatment. Its renewable solutions strategy targets €500 million in revenue by 2030, with 2026 scaling of bio-based sludge dewatering polymers replacing petroleum-derived polyacrylamides. The company’s advanced flocculants improve sludge cake dryness, directly lowering landfill and transport costs. Alignment with European Sustainability Reporting Standards enhances its focus on carbon footprint reduction in sludge management. Kemira’s integrated portfolio of coagulants and flocculants supports both municipal and fiber-intensive industries. Its emphasis on total cost of ownership optimization strengthens its leadership in sustainable water chemistry.

Solenis Expands High-Efficiency Flocculant Portfolio with Performance-Based Dewatering Solutions

Solenis is reinforcing its position as a global water and sludge treatment leader with operations spanning 160 countries and 78 manufacturing facilities. Its Zetag™ and Praestol™ flocculants are engineered to maximize sludge dewatering efficiency, with proven increases in cake dryness from 20% to 25% delivering multimillion-dollar cost savings for large municipal plants. The company’s performance guarantee model differentiates its offerings in cost-sensitive wastewater treatment operations. Strategic pricing adjustments of 4%–10% in EMEA ensure sustained investment in R&D and supply chain stability. Integration of NCH and Diversey expands its reach into industrial sectors such as food processing and pulp and paper. Solenis’ focus on high-performance polymers and operational efficiency positions it strongly in the evolving sludge treatment landscape.

SNF Group Advances High-Performance Water-Soluble Polymers Through Strategic Acquisitions and Sustainability Leadership

SNF Group remains the global leader in water-soluble polymers, strengthening its sludge treatment chemicals portfolio through targeted acquisitions and innovation in flocculant chemistry. The acquisition of Syensqo’s Oil & Gas division enhances its expertise in rheology modifiers and viscosifiers with cross-applicability to sludge dewatering. Additional acquisitions in the U.S. market expand its localized production and specialty chemical capabilities. SNF’s EcoVadis Platinum rating places it in the top 1% globally, supporting its competitiveness in ESG-driven procurement contracts. Its product innovation focuses on low-acrylamide-residue and hyper-branched flocculants, delivering superior shear stability in high-speed centrifuge applications. The company’s scale and sustainability credentials reinforce its leadership in advanced sludge treatment polymers.

Kurita Water Industries Accelerates Digital Water Solutions and PFAS Mitigation Technologies

Kurita Water Industries is positioning itself as a digital leader in sludge treatment through its CORR system, integrating chemical treatment with real-time facility monitoring to enable efficient wastewater recovery. Its PSV-27 strategy allocates significant investment toward innovation, including microbial fuel cell technology that converts sludge into energy. The company’s 2026 “BeyondPFAS” solutions address tightening global regulations by enabling advanced removal of persistent contaminants such as PFOS and PFOA. Kurita’s approach combines chemical treatment with digital optimization to enhance operational efficiency and sustainability. Strong fiscal performance and decarbonization achievements reinforce its role as a preferred partner in industrial water treatment. Its focus on digitalization and regulatory compliance strengthens its competitive positioning.

Veolia Strengthens Sludge-to-Energy Leadership with MemGas™ Technology and Full WTS Integration

Veolia is advancing its dominance in sludge treatment chemicals and technologies through full integration of its Water Technologies and Solutions division, unlocking €90 million in cost synergies. Its MemGas™ technology converts sludge-derived biogas into renewable natural gas, transforming wastewater plants into energy-producing assets. The company’s GreenUp 2027 strategy prioritizes micropollutant removal and resource recovery, including phosphorus and metal extraction from sludge. Veolia’s “BeyondPFAS” offering provides comprehensive solutions from detection to chemical destruction of contaminants. Operational projects such as the Seine Aval facility highlight its capability to manage high-volume sludge with reduced environmental impact. Its integrated ecological transformation model positions it as a global leader in circular sludge management.

Ecolab (Nalco Water) Integrates AI-Driven Smart Dosing and Water Stewardship in Sludge Treatment

Ecolab’s Nalco Water division is leading digital transformation in sludge treatment through its 3D TRASAR™ platform, which uses AI and real-time analytics to optimize flocculant dosing and reduce chemical consumption by up to 20%. The acquisition of Ovivo’s ultrapure water business strengthens its presence in high-tech industries requiring stringent sludge treatment standards. Its “Net Zero Water” strategy emphasizes wastewater reuse and positions sludge as a resource for industrial water recovery. With annual sales of approximately $16 billion, Ecolab leverages scale and innovation to link sludge treatment efficiency with clients’ sustainability and Scope 3 emission goals. Its focus on intelligent water management systems enhances operational efficiency and environmental performance.

China Sludge Treatment Chemicals Market Accelerates Under Harmless Disposal and Low-Carbon Mandates

China’s sludge treatment chemicals market is being reshaped by binding national mandates that prioritize harmless disposal, energy efficiency, and carbon reduction. Under the final phase of the 14th Five-Year Plan, the National Development and Reform Commission has required urban sludge harmless disposal rates to exceed 90% by 2025. This policy has triggered a sharp increase in demand for high-performance dewatering polymers and advanced flocculants capable of handling sludge streams with elevated silt loads and heavy metal concentrations, which are characteristic of many Chinese municipalities. With annual sludge generation surpassing 70 million tons as of 2024, municipal authorities are prioritizing chemicals that minimize secondary pollution and reduce downstream treatment complexity.

Environmental policy is increasingly integrated with climate objectives. In January 2024, the Ministry of Ecology and Environment issued guidelines linking sewage treatment with carbon emission control, targeting the establishment of 100 low-carbon sludge treatment plants by late 2025. These facilities favor chemical programs that reduce incineration energy demand and improve sludge calorific value. Industrial water reuse mandates across sectors such as petrochemicals and textiles are further expanding demand for specialized thickening agents compatible with Zero Liquid Discharge systems. To meet year-end 2025 targets, China is completing an additional 20,000 tons per day of sludge treatment capacity, while domestic producers pivot toward bio-based flocculants under new Green Mode of Production standards aligned with national carbon peak goals.

Germany Sludge Treatment Chemicals Market Anchored by Phosphorus Recovery and Circular Economy Law

Germany represents a structurally advanced market where sludge treatment chemicals are increasingly linked to nutrient security and circular economy legislation. The country is the first globally to mandate phosphorus recovery from sewage sludge, requiring all large-scale plants to reclaim phosphorus by 2029. This regulation is catalyzing current investments in recovery technologies and specialized chemical precipitants, particularly iron- and aluminum-based systems optimized for ash processing. A landmark development is the Schkopau phosphorus recovery facility, where construction began in May 2025. The plant applies Ash2Phos technology to recover more than 90% of phosphorus from sludge ash.

The Schkopau project is a joint initiative between EasyMining and Gelsenwasser, designed to process approximately 30,000 tonnes of sludge ash annually and return recovered nutrients to agricultural fertilizer value chains. Regulatory readiness extends beyond nutrients. German producers, including BASF, have reformulated sludge treatment portfolios to eliminate D4, D5, and D6 siloxanes ahead of the 2026 EU REACH deadline. BASF also introduced a renewable-resource-derived flocculant in mid-2024, targeting a 10% reduction in sludge disposal costs. Federal policy documents underscore the strategic importance of sludge-derived phosphorus in reducing Germany’s reliance on imports from geopolitically sensitive regions.

United States Sludge Treatment Chemicals Market Reshaped by PFAS Regulation and Infrastructure Investment

The United States market is entering a transition phase defined by PFAS risk management, infrastructure investment, and digital optimization. On January 14, 2025, the Environmental Protection Agency released a draft sewage sludge risk assessment for PFOA and PFOS, signaling significant changes to chemical treatment protocols to prevent PFAS leaching during land application. This assessment, combined with the EPA’s December 2024 TSCA Final Rule, which removed low-volume exemptions for PFAS-containing chemicals in water treatment, is accelerating reformulation toward PFAS-free sludge conditioning chemistries.

Capacity expansion and consolidation are reinforcing domestic supply. Solenis committed USD 193 million in early 2024 to expand its Virginia facility, focusing on polyvinylamine polymers for industrial sludge and paper processing. In September 2025, Kemira signed a USD 150 million agreement to acquire Water Engineering, Inc., strengthening its U.S. industrial wastewater and sludge services footprint. Innovation continues at the application level, with Ashland introducing a coagulant in 2024 that improves oil and gas sludge dewatering efficiency by 20%, reducing secondary drying energy. Municipal utilities are also deploying AI-enabled smart dosing systems, delivering average chemical savings of 15% through real-time optimization.

Japan Sludge Treatment Chemicals Market Focused on Biogas, Carbon Utilization, and Material Cycles

Japan’s sludge treatment chemicals market is increasingly oriented toward energy recovery, carbon utilization, and material circularity. In February 2025, Asahi Kasei partnered with Kurashiki City to inaugurate a demonstration biogas purification system at the Kojima Sewage Treatment Plant. The system employs zeolite-based chemical adsorbents to produce high-purity biomethane from sewage sludge, improving the commercial viability of sludge-derived energy.

National climate strategy is reinforcing chemical innovation. Japan’s CCUS framework for 2025 emphasizes the capture and utilization of CO2 separated during sludge treatment to enable carbon-negative fuel pathways. Knowledge sharing is accelerating through the 19th IWA Conference on Sludge Management, hosted in Kyoto in October 2025 under the theme “Toward Material Cycle and Low Carbon Society,” highlighting Japanese advances in thermal treatment chemicals. Water stewardship is also a differentiator. Kurita Water Industries has emphasized CSV-driven chemical solutions that reduce greenhouse gas emissions by lowering sludge water content. Standardization efforts include pioneering tin-free curing systems for sludge-derived construction materials, aligned with Japan’s strict toxicity and material safety standards.

Comparative Snapshot: Country-Level Sludge Treatment Chemicals Dynamics

Sludge Treatment Chemicals Market County Level Snapshot

|

Country

|

Primary Policy Drivers

|

Strategic Chemical Focus

|

Structural Impact

|

|

China

|

14th Five-Year Plan, low-carbon treatment

|

High-performance dewatering polymers, bio-based flocculants

|

Rapid capacity expansion and municipal compliance

|

|

Germany

|

Phosphorus recovery law, EU REACH

|

Ash-based precipitants, renewable flocculants

|

Closed-loop nutrient recovery and import substitution

|

|

United States

|

PFAS risk assessment, TSCA reform

|

PFAS-free polymers, AI-driven dosing

|

Reformulation and digital efficiency gains

|

|

Japan

|

CCUS strategy, material cycle policy

|

Zeolite purification, thermal treatment chemicals

|

Energy-positive sludge management

|

Sludge Treatment Chemicals Market Report Scope

Sludge Treatment Chemicals Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$10.5 Billion

|

|

Market Size (2034)

|

$17.3 Billion

|

|

Market Growth Rate

|

5.7%

|

|

Segments

|

By Type (Coagulants, Flocculants, Disinfectants, Conditioners & Stabilizers, Specialty Chemicals), By Treatment Process (Primary Treatment, Secondary Treatment, Tertiary Treatment, Sludge Processing), By End-Use Industry (Municipal, Food & Beverage, Oil & Gas, Pulp & Paper, Chemical & Pharmaceutical, Metal & Mining)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Kemira Oyj, Solenis, BASF SE, Ecolab Inc., Kurita Water Industries Ltd., Veolia Water Technologies, Suez SA, Ashland Inc., SNF Group, Buckman Laboratories International, Avista Technologies, Zhejiang Xinan Chemical Industrial Group, Hubbard-Hall Inc., Accepta Water Treatment, Aries Chemical Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Sludge Treatment Chemicals Market Segmentation

By Type

- Coagulants

- Flocculants

- Disinfectants

- Conditioners & Stabilizers

- Specialty Chemicals

By Treatment Process

- Primary Treatment

- Secondary Treatment

- Tertiary Treatment

- Sludge Processing

By End-Use Industry

- Municipal

- Food & Beverage

- Oil & Gas

- Pulp & Paper

- Chemical & Pharmaceutical

- Metal & Mining

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Sludge Treatment Chemicals Industry

- Kemira Oyj

- Solenis

- BASF SE

- Ecolab Inc.

- Kurita Water Industries Ltd.

- Veolia Water Technologies

- Suez SA

- Ashland Inc.

- SNF Group

- Buckman Laboratories International

- Avista Technologies

- Zhejiang Xinan Chemical Industrial Group

- Hubbard-Hall Inc.

- Accepta Water Treatment

- Aries Chemical Inc.

*- List not Exhaustive