Intelligent Surface Technologies and Sensor-Integrated Materials Driving Exponential Growth

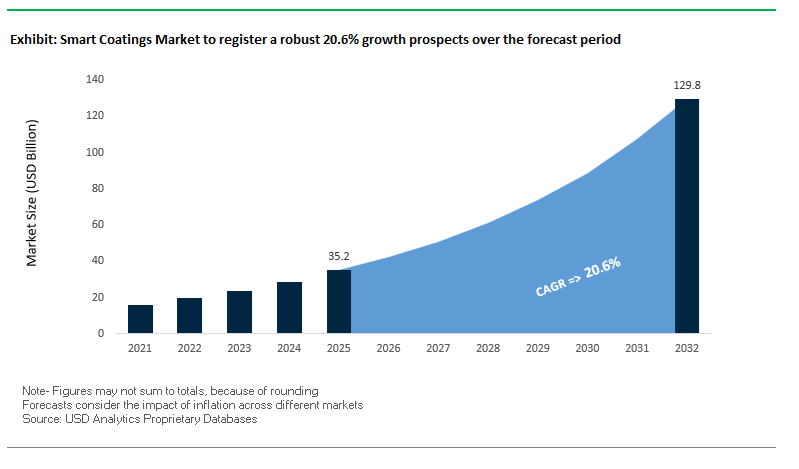

The global Smart Coatings Market is undergoing a rapid transformation, emerging as one of the fastest-growing segments within the advanced materials ecosystem. The market was valued at $35.2 billion in 2025 and is projected to reach $130.6 billion by 2032, expanding at a CAGR of 20.6% during 2025–2032. This exceptional growth is driven by the convergence of material science, IoT integration, and sustainability requirements, enabling coatings to move beyond passive protection toward active, responsive, and data-generating functionalities.

A key structural driver is the increasing demand for self-monitoring and self-responsive surfaces across industries such as energy, infrastructure, automotive, aerospace, and electronics. Smart coatings now incorporate embedded sensors, phase-change materials, and microencapsulation technologies, allowing them to detect corrosion, respond to environmental stimuli, and even repair damage autonomously. These capabilities significantly reduce inspection costs, maintenance cycles, and operational risks, particularly in high-value assets such as offshore platforms, pipelines, and aircraft.

Another major growth catalyst is the integration of energy-efficient and functional coatings in the construction sector. Technologies such as solar-absorbing coatings and thermal-regulating surfaces are enabling buildings to actively contribute to energy management. These solutions align with global decarbonization targets and are increasingly being specified in large-scale commercial and institutional infrastructure projects seeking net-zero energy performance.

The automotive and mobility sectors are also accelerating demand for smart coatings, particularly with the rise of electric and autonomous vehicles. Coatings with LiDAR-reflective properties, thermal management capabilities, and advanced optical effects are becoming essential for sensor accuracy, battery safety, and vehicle aesthetics. Additionally, the push toward low-carbon coating processes and materials, including low-bake and hydrogen-powered application technologies, is reinforcing the role of smart coatings in sustainable manufacturing ecosystems.

Market Analysis: Sensor-Enabled Monitoring, Energy-Harvesting Coatings, and Cross-Industry Collaboration Reshaping Competitive Dynamics

The smart coatings market is being reshaped by breakthrough innovations, cross-industry collaborations, and strategic investments in intelligent material systems, reflecting a shift toward high-value, performance-driven solutions. In March 2026, AkzoNobel introduced a solar-absorbing wall coating technology, positioning itself as the exclusive global supplier. This innovation enables architectural surfaces to capture and store thermal energy, significantly reducing heating and cooling demands in large commercial buildings and reinforcing the role of coatings in energy-efficient infrastructure.

Real-time monitoring capabilities are emerging as a key differentiator. Jotun’s January 2026 launch of smart protective coatings with integrated sensors allows for continuous condition monitoring and early failure detection, particularly in offshore and petrochemical environments where manual inspections are costly and hazardous. These coatings represent a major advancement in predictive maintenance and asset integrity management.

Strategic alignment with sustainability goals is also driving innovation. The September 2025 consortium between AkzoNobel, Arkema, and BASF focuses on developing low-carbon, low-bake powder coatings, reducing curing energy consumption by up to 20%. Complementing this, Evonik’s March 2025 launch of mass-balanced eCO additives introduces smart additive technologies that lower the carbon footprint of coatings while maintaining high-performance characteristics, particularly in digital and industrial applications.

In the automotive sector, Axalta’s 2026 “A Plan” execution highlights the growing importance of smart mobility coatings, including LiDAR-reflective and heat-management technologies essential for autonomous and electric vehicles. BASF’s 2025–2026 automotive color innovations, such as “Tesseract Blue,” further demonstrate the convergence of functional performance and digital aesthetics, creating coatings that interact with light and perception in advanced ways.

Infrastructure investments are also supporting market expansion. RPM International’s January 2025 establishment of a manufacturing plant in Malaysia strengthens supply capabilities for smart specialty coatings in Southeast Asia, addressing rising demand from infrastructure and construction projects. Meanwhile, AkzoNobel’s hydrogen-powered spray booth (November 2024) introduces a zero-emission application process, aligning coating deployment with broader decarbonization initiatives.

Material innovation continues to evolve toward self-healing and adaptive barrier technologies. Jotun’s Next Generation Barrier series (November 2024) incorporates zinc-rich smart coatings that act as sacrificial anodes, providing autonomous protection against corrosion in highly saline environments. Similarly, Hempel’s “Accelerate to Win” strategy (January 2026) emphasizes the deployment of smart, life-extending coating technologies, targeting significant emission reductions while enhancing asset durability.

Market Trend: ASTM D8267-25 Establishes Quantifiable Benchmark for Self-Healing Coating Performance

The ratification of ASTM D8267-25 marks a pivotal advancement in the smart coatings industry by introducing a standardized methodology for evaluating self-healing performance. Historically, the absence of harmonized testing protocols limited the credibility and scalability of self-healing coatings across high-reliability sectors such as aerospace, marine, and energy infrastructure. The new standard formalizes the measurement of Healing Efficiency (HE) using Electrochemical Impedance Spectroscopy, requiring coatings to recover at least 80% of their original barrier resistance within 24 hours of mechanical damage to qualify as high-performance systems. This quantifiable benchmark is enabling procurement teams and engineering stakeholders to directly compare product efficacy, accelerating qualification cycles and reducing reliance on manufacturer-claimed data. The impact is already evident, with Tier-1 aerospace suppliers reporting a 35% increase in certification requests for self-healing primers following the 2025–2026 guideline release. Furthermore, the ability to model coating degradation and recovery behavior using standardized HE data is allowing asset owners to optimize inspection intervals and predictive maintenance strategies. This development is positioning smart coatings as a credible alternative to conventional corrosion protection systems in mission-critical applications.

Market Trend: EU REACH Microplastics Restriction Reshaping Self-Healing Coating Chemistry

The European Union’s REACH regulation targeting intentionally added microplastics, under Annex XVII Entry 78, is entering a critical compliance phase in May 2026, significantly impacting smart coatings that rely on microencapsulation technologies. These coatings typically incorporate polymer-based microcapsules containing isocyanate or other reactive healing agents, which are released upon mechanical damage to initiate repair. Under the new regulation, manufacturers must disclose detailed emission profiles and chemical compositions for microencapsulated substances, with stringent concentration limits of 0.01% by weight for many microparticles. This regulatory burden is driving a pronounced shift in material innovation strategies, with approximately 45% of European smart coating producers transitioning toward intrinsic self-healing systems. These systems leverage reversible chemical reactions, such as Diels-Alder mechanisms or shape-memory polymer networks, eliminating the need for microcapsules and thereby bypassing regulatory reporting requirements. This transition is not only compliance-driven but is also influencing long-term R&D investment, as intrinsic systems offer improved durability and repeatable healing cycles compared to single-use extrinsic systems. The regulatory landscape is therefore accelerating a fundamental redesign of smart coating architectures, prioritizing sustainability, regulatory alignment, and lifecycle performance.

Market Opportunity: Electrochromic Smart Coatings Driving Energy Optimization in Net-Zero Commercial Buildings

Electrochromic coatings are emerging as a transformative solution within the smart coatings market, particularly in the context of stringent Net-Zero building regulations across Europe and North America. These coatings dynamically modulate light transmission and solar heat gain in response to low-voltage electrical signals, enabling real-time control of indoor environmental conditions. Advanced electrochromic window systems are capable of reducing total building energy consumption for heating and cooling by up to 27%, while simultaneously decreasing occupant glare by approximately 32%. This dual benefit enhances both energy efficiency and occupant comfort, aligning with modern building performance standards. Moreover, the integration of electrochromic coatings into the “Building-as-a-Battery” concept is enabling more efficient load management by reducing peak energy demand. One of the most significant economic advantages lies in HVAC system optimization, where controlled solar heat gain allows for downsizing of heating and cooling infrastructure, resulting in capital expenditure reductions of 10% to 15% for new commercial developments. As urban construction increasingly prioritizes energy efficiency, digital control, and sustainability, electrochromic smart coatings are positioned as a high-growth segment within the architectural coatings landscape.

Market Opportunity: Corrosion-Sensing Smart Coatings Enabling Predictive Maintenance in Critical Infrastructure

Corrosion-sensing or “self-reporting” coatings represent a high-value opportunity in infrastructure monitoring, particularly for sectors such as hydrogen transport, carbon capture pipelines, and offshore energy systems. These advanced coatings incorporate functional additives such as pH-sensitive dyes or fluorescent markers that respond to early-stage corrosion processes occurring beneath the coating layer. By detecting subtle chemical changes, such as pH variations as low as 0.5 units, these systems can identify sub-film corrosion significantly earlier than conventional inspection techniques, including ultrasonic testing or manual visual assessment. This early detection capability enables operators to intervene before structural degradation becomes critical, improving asset reliability and safety. In quantitative terms, smart sensing coatings can accelerate corrosion detection timelines by a factor of three to five, providing a substantial advantage in high-risk environments. Additionally, the deployment of these coatings supports a transition from time-based maintenance schedules to condition-based maintenance strategies, which are more efficient and cost-effective. Industry projections indicate that this shift can reduce long-term maintenance expenditures by approximately 20%, particularly in large-scale infrastructure networks. As asset owners increasingly adopt digital and data-driven maintenance frameworks, corrosion-sensing smart coatings are becoming an integral component of next-generation asset integrity management systems.

Smart Coatings Market Share and Segmentation Insights: Single-Layer Innovation and Direct Sales Channel Expansion

By Layer Type: Single-Layer Smart Coatings Lead with Cost Efficiency and Functional Integration

The single-layer smart coatings segment dominated the market with a 63.5% share in 2025, driven by its cost-effectiveness, ease of application, and rapid technological advancement. These coatings integrate advanced functionalities such as self-cleaning coatings (TiO₂-based photocatalytic), antimicrobial coatings (silver-ion technology), anti-fog coatings, and thermochromic coatings directly into a single layer, eliminating the need for complex multi-layer systems. This simplification reduces application time, labor costs, and material usage, making single-layer coatings highly attractive for both consumer applications (glass, textiles, electronics) and industrial sectors (automotive, construction, healthcare). Additionally, ongoing innovation in nanotechnology and functional additives has enabled improved performance within a single coating layer, accelerating adoption across diverse end-use industries. The combination of high-performance functionality, lower cost, and scalability continues to position single-layer smart coatings as the dominant segment in the global smart coatings market.

By Sales Channel: Direct Sales Channel Leads with Technology Protection and Technical Support

The direct sales segment accounted for a leading 46.7% share of the smart coatings market in 2025, reflecting the importance of intellectual property protection and specialized technical collaboration. Smart coatings often involve proprietary, patented formulations, prompting manufacturers to engage directly with end-users or licensed applicators to maintain strict control over product quality and prevent unauthorized replication. This direct engagement also ensures proper handling of application parameters such as UV activation, curing conditions, and film thickness, which are critical for achieving desired functionalities like self-healing, anti-microbial performance, or temperature responsiveness. Additionally, direct supplier relationships enable customized coating solutions, real-time technical support, and performance validation, which are essential for high-value applications in sectors such as healthcare, electronics, and aerospace. As demand rises for advanced functional coatings and smart material technologies, the direct sales channel continues to drive innovation, quality assurance, and market growth.

Competitive Landscape of the Smart Coatings Market

Axalta Leads Innovation with AI-Driven Manufacturing and EV Safety Coatings

Axalta Coating Systems is the “innovation titan” in the smart coatings market, recognized globally for its technological breakthroughs. In 2026, the company won multiple Edison Awards, including Gold for its EcoNextJet™ system, which enables production-scale vehicle color customization through drop-on-demand technology. Its Alesta® e-PRO FG Black coating delivers fire resistance up to 1200°C, enhancing EV battery safety. Axalta’s TintMaster AI platform improves Right-First-Time (RFT) performance by up to 29%, reducing manufacturing inefficiencies. Its strong focus on mobility coatings positions it as a leader in high-growth EV and automotive segments.

AkzoNobel Strengthens Market Position with Smart Powder Coatings and Digital Inspection Tools

AkzoNobel N.V. is a major player in the smart coatings market, combining sustainability with advanced digital technologies. The company reported improved profitability in 2026 and is progressing toward its merger with Axalta. Its innovations include drone-based coating inspection systems that automate maintenance for aircraft and infrastructure, reducing downtime. AkzoNobel has also introduced laser-based curing technologies for powder coatings, enabling faster and more energy-efficient application processes. Its “Rhythm of Blues” smart coating family integrates visible-light responsiveness and thermal management capabilities, reinforcing its leadership in multifunctional coatings.

PPG Drives Market with Digital Ecosystems and Self-Cleaning Smart Coatings

PPG Industries, Inc. remains the technological vanguard in the smart coatings market, leveraging its strong R&D and digital infrastructure. Its PPG LINQ™ platform integrates AI-driven spectrophotometers and automated mixing systems, reducing material waste by up to 30%. The company is also pioneering TiO₂-based self-cleaning coatings that break down pollutants under sunlight, targeting smart city applications. PPG’s focus on anticorrosion smart coatings for marine and offshore sectors positions it strongly in infrastructure and energy markets.

Hempel Leads Sustainability and Marine Applications with Smart Fouling-Release Technologies

Hempel A/S is a key innovator in the smart coatings market, particularly in marine and infrastructure applications. Its Hempaguard smart coatings have contributed to 35.9 million tonnes of CO₂ emission reductions by improving vessel efficiency. The company reported record financial performance in 2026, supported by strong growth in marine coatings. Its Avantguard® technology remains a benchmark for smart corrosion protection, offering long-term durability in extreme environments.

BASF Strengthens Market with Smart Additives and Advanced Material Integration

BASF SE plays a critical enabling role in the smart coatings market, supplying essential additives and materials. Its expansion of HALS and NOR® HALS stabilizers supports the growing demand for UV-resistant smart coatings. BASF is also innovating in smart materials, including TPU-based solutions for sports and textiles, and electrospun nano-membranes for smart fabrics. Its vertical integration ensures consistent supply of advanced materials for next-generation coatings.

Jotun Expands Smart Coatings Leadership with Sensor-Enabled and Anti-Biofouling Technologies

Jotun A/S is a dominant player in the smart coatings market, particularly in marine and energy sectors. Its smart anti-biofouling coatings reduce fuel consumption by 10–15% by preventing marine growth. The company is also developing sensor-embedded coatings for structural health monitoring in oil and gas infrastructure, enabling real-time detection of damage. Its expansion into antimicrobial and self-cleaning coatings supports growth in urban residential applications. Jotun’s strong presence in Asia-Pacific further reinforces its competitive position.

Germany Leading Stimuli-Responsive Smart Coatings Innovation for Automotive and Energy Efficiency

Germany stands at the forefront of the global smart coatings market, driven by its leadership in stimuli-responsive materials and functional nanotechnology. The commercialization of thermochromic window coatings that dynamically adjust transparency based on solar intensity is revolutionizing energy-efficient buildings by significantly reducing HVAC loads.

Government-backed initiatives such as the “Research for Sustainability” (FONA) program are accelerating the development of self-healing infrastructure coatings, aimed at reducing maintenance-related carbon emissions. Strategic investments, including large-scale production expansions for functional e-coat primers, are strengthening Germany’s industrial capabilities. Innovations such as piezoelectric coatings capable of generating micro-currents for structural health monitoring and increasing adoption of ice-phobic coatings for wind turbines highlight the country’s leadership in integrating smart materials into critical infrastructure and renewable energy applications.

China Scaling Smart Coatings for Infrastructure, EV Networks, and Smart City Development

China is rapidly advancing in the smart coatings industry, leveraging large-scale infrastructure projects and its strong manufacturing ecosystem. The deployment of graphene-enhanced anti-corrosion coatings across extensive high-speed rail networks is improving durability in coastal environments, while innovations in AI-driven sensing coatings enable real-time detection of structural fatigue and chemical leaks.

Government initiatives are promoting the adoption of smart greenhouse coatings that optimize light transmission for agricultural productivity, while urban development projects are incorporating phase-change material (PCM) coatings to enhance thermal energy management in buildings. Significant investments in high-purity silicone-based smart additives are supporting the electronics sector, particularly smartphone displays. Additionally, the widespread use of photocatalytic self-cleaning coatings in urban environments is improving air quality by neutralizing pollutants, reinforcing China’s leadership in smart infrastructure and environmental innovation.

United States Driving Smart Coatings Innovation in Aerospace, Defense, and Intelligent Infrastructure

The United States is a major innovation hub in the smart coatings market, driven by advancements in aerospace, defense, and infrastructure modernization. Regulatory changes, including PFAS-free mandates, are accelerating the development of fluorine-free superhydrophobic coatings for consumer and industrial applications.

Technological breakthroughs in self-healing polymer coatings for aircraft surfaces are enhancing aerodynamic performance by repairing micro-damage during operation. Infrastructure investments under federal programs are supporting the deployment of sensor-embedded coatings for bridges, enabling predictive maintenance. The commercialization of RF-transparent coatings is supporting the expansion of 5G and 6G networks, while innovations in anti-fouling coatings for naval applications are improving operational efficiency. Investments in fire-retardant smart coatings for EV battery safety further demonstrate the United States’ leadership in high-performance coating technologies.

Japan Advancing Nano-Functional Smart Coatings for Electronics and Renewable Energy

Japan is a global leader in nano-functional smart coatings, particularly in electronics, semiconductors, and renewable energy applications. The development of nanolayered interference coatings for passive radiative cooling is enhancing thermal management in outdoor electronic systems.

Government support under the Green Growth Strategy is accelerating the adoption of anti-reflective coatings for solar cells, improving energy efficiency in next-generation photovoltaic technologies. Product innovations include flexible conductive coatings for wearable medical devices, enabling high durability and signal integrity. Japan is also advancing antimicrobial smart coatings activated by visible light, addressing hygiene requirements in public spaces. The widespread use of super-lipophobic coatings for LiDAR systems in autonomous vehicles highlights Japan’s role in enabling next-generation mobility technologies.

India Emerging as a High-Growth Market for Smart Coatings in Infrastructure and Industrial Applications

India is witnessing rapid growth in the smart coatings market, driven by infrastructure expansion and government initiatives supporting advanced materials. Policies under Make in India 2.0 are encouraging domestic production of nano-enabled smart coatings, particularly anti-corrosive primers for industrial applications.

Infrastructure investments are driving the adoption of CO₂-absorbing smart pavement coatings and high-reflectivity solutions for improved road safety. Innovations such as humidity-responsive coatings in the textile industry and the deployment of corrosion-sensing smart wraps for pipelines are expanding application areas. The growing logistics sector is also increasing demand for smart concrete densifiers, enhancing durability and reducing maintenance costs. Strategic investments by global players in local production facilities are further strengthening India’s position as a high-growth market.

South Korea Leading Consumer Electronics and Optical Smart Coatings Innovation

South Korea is a global leader in smart coatings for consumer electronics, driven by advancements in display technology and automotive innovation. The development of self-healing coatings for foldable smartphones is enhancing product durability by repairing surface damage at room temperature.

Technological advancements include the commercialization of quantum-dot smart coatings capable of switching between transparency and energy generation modes, representing a breakthrough in multifunctional materials. Investments in hydrophobic coatings for autonomous vehicle sensors are ensuring reliability in challenging weather conditions. Government initiatives under the K-Green New Deal are promoting bio-based smart coatings, while regulatory updates for battery safety are driving the adoption of smart shutdown coatings in lithium-ion batteries. The widespread use of anti-fingerprint coatings in premium appliances further highlights South Korea’s leadership in high-performance consumer applications.

Smart Coatings Market Report Scope

Smart Coatings Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$35.2 Billion

|

|

Market Size (2032)

|

$130.6 Billion

|

|

Market Growth Rate

|

20.6%

|

|

Segments

|

By Function (Anti-Corrosion, Self-Healing, Anti-Microbial, Self-Cleaning, Anti-Icing, Anti-Fouling, Other Functional Types), By Layer Type (Single-Layer Coatings, Multi-Layer Coatings), By Technology (Nano-Coatings, Stimuli-Responsive Coatings, Microencapsulation, Shape Memory Polymers), By End-User Industry (Automotive and Transportation, Aerospace and Defense, Building and Construction, Marine, Healthcare and Medical Devices, Consumer Electronics, Energy), By Sales Channel (Direct Sales, Industrial Distributors, Specialized Service Providers)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

3M Company, PPG Industries, Inc., Akzo Nobel N.V., BASF SE, The Sherwin-Williams Company, Axalta Coating Systems Ltd., Hempel A/S, Jotun A/S, RPM International Inc., Kansai Paint Co., Ltd., Nippon Paint Holdings Co., Ltd., Covestro AG, Evonik Industries AG, DuPont de Nemours, Inc., NEI Corporation

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Smart Coatings Market Segmentation

By Function

- Anti-Corrosion

- Self-Healing

- Anti-Microbial

- Self-Cleaning

- Anti-Icing

- Anti-Fouling

- Other Functional Types

By Layer Type

- Single-Layer Coatings

- Multi-Layer Coatings

By Technology

- Nano-Coatings

- Stimuli-Responsive Coatings

- Microencapsulation

- Shape Memory Polymers

By End-User Industry

- Automotive and Transportation

- Aerospace and Defense

- Building and Construction

- Marine

- Healthcare and Medical Devices

- Consumer Electronics

- Energy

By Sales Channel

- Direct Sales

- Industrial Distributors

- Specialized Service Providers

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Smart Coatings Industry

- 3M Company

- PPG Industries, Inc.

- Akzo Nobel N.V.

- BASF SE

- The Sherwin-Williams Company

- Axalta Coating Systems Ltd.

- Hempel A/S

- Jotun A/S

- RPM International Inc.

- Kansai Paint Co., Ltd.

- Nippon Paint Holdings Co., Ltd.

- Covestro AG

- Evonik Industries AG

- DuPont de Nemours, Inc.

- NEI Corporation

*- List not Exhaustive