Thin-Film Precision, Energy-Active Surfaces, and PFAS-Free Chemistry Accelerating Double-Digit Growth

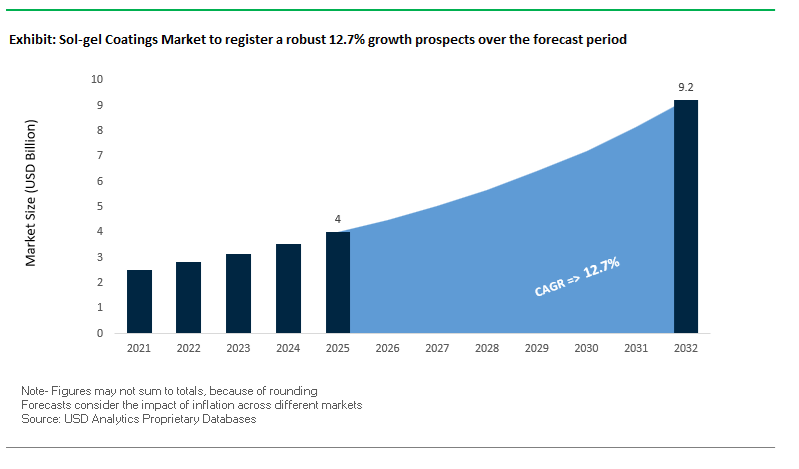

The global Sol-Gel Coatings Market is advancing rapidly as industries shift toward ultra-thin, high-performance inorganic coatings capable of delivering multifunctional protection with minimal material usage. The market was valued at $4 billion in 2025 and is projected to reach $9.2 billion by 2032, expanding at a CAGR of 12.7% during 2025–2032. Growth is driven by the unique ability of sol-gel technologies to form nanostructured, chemically bonded films that offer superior adhesion, corrosion resistance, optical clarity, and thermal functionality across aerospace, construction, electronics, and automotive applications.

A primary structural driver is the increasing demand for lightweight, high-efficiency coating systems, particularly in aerospace and electric mobility. Sol-gel coatings provide thin-film protection with minimal added weight, making them ideal for aircraft components and EV battery systems where performance and energy efficiency are tightly coupled. Additionally, their compatibility with chromium-free and low-VOC formulations positions sol-gel coatings as a preferred alternative to legacy pretreatment systems, aligning with stringent environmental and occupational safety regulations.

Another major growth catalyst is the emergence of energy-active and functional architectural coatings. Sol-gel technologies are enabling surfaces to perform beyond protection, incorporating capabilities such as heat absorption, anti-graffiti resistance, and self-cleaning properties. These innovations are particularly relevant in urban infrastructure, where coatings contribute to energy efficiency, reduced maintenance costs, and enhanced building longevity.

The market is also benefiting from increasing adoption in electronics and semiconductor manufacturing, where sol-gel processes enable the precise deposition of high-purity, defect-free coatings required for advanced components. As industries prioritize durability, sustainability, and performance optimization, sol-gel coatings are emerging as a critical platform technology bridging material science, nanotechnology, and green chemistry.

Market Analysis: Aerospace-Grade Pretreatments, Anti-Graffiti Breakthroughs, and EV Battery Applications Driving Commercial Expansion

The competitive landscape of the sol-gel coatings market is defined by advanced R&D investments, strategic acquisitions, and rapid commercialization of specialty formulations, reflecting the transition of sol-gel technology from niche applications to scalable industrial solutions. In March 2026, AkzoNobel became the exclusive supplier of Calosol, a sol-gel-based heat-absorbing coating technology that transforms building facades into energy-generating surfaces. This innovation underscores the growing role of sol-gel systems in sustainable architecture and energy-efficient infrastructure.

Environmental compliance and durability are key innovation themes. Evonik’s March 2026 launch of Protectosil® ECO-TRETE® introduces a PFAS-free, water-based anti-graffiti coating that chemically bonds to mineral substrates, delivering long-term protection without the environmental risks associated with fluorinated compounds. This development aligns with the broader industry shift toward non-toxic, high-performance coating chemistries.

Aerospace remains a critical application segment. AkzoNobel’s €50 million manufacturing upgrade (January 2026) at its Waukegan facility is specifically designed to scale production of sol-gel pretreatments and advanced thin-film coatings required for next-generation, fuel-efficient aircraft. Complementing this, Sherwin-Williams’ Jet Prep™ Pretreatment (October 2024) offers a chrome-free sol-gel solution that replaces traditional hazardous systems while improving adhesion performance, highlighting the sector’s shift toward safer and more sustainable coating technologies.

In the electric mobility sector, Jotun’s June 2025 launch of hybrid sol-gel powder coatings for EV battery enclosures demonstrates the technology’s ability to deliver high dielectric strength and thermal insulation in ultra-thin layers, enabling lighter and more efficient battery designs. This application underscores the strategic importance of sol-gel coatings in next-generation energy storage systems.

Supply chain optimization and regional expansion are also shaping market dynamics. Wacker Chemie’s September 2025 realignment toward electronic-grade silanes ensures a stable supply of high-purity precursors essential for sol-gel synthesis, particularly in semiconductor and optical coating applications. Meanwhile, Sherwin-Williams’ December 2025 acquisition of Suvinil strengthens its R&D and production capabilities in Latin America, enabling the localization of smart and sol-gel mineral coatings for infrastructure markets.

Strategic expansion into emerging markets is further accelerating adoption. Nippon Paint’s 2025 “Asset Assembler” strategy focuses on acquiring regional specialty coating manufacturers, particularly in India and Southeast Asia, to expand its portfolio in inorganic and mineral-based coatings, including sol-gel systems for renovation and restoration projects.

Additionally, innovations such as Dalton Enterprises’ QuickPatch H2O (November 2024) demonstrate the application of water-activated sol-gel binders for instant structural repair, enabling chemical compatibility with existing substrates and improving long-term durability.

Market Trend: EU REACH 2026 Controls on Metal Alkoxide Precursors Driving Low-Emission Sol-Gel Formulations

The sol-gel coatings industry is undergoing a significant transition as EU REACH regulations intensify oversight of metal alkoxide precursors such as tetraethyl orthosilicate and tetramethyl orthosilicate. The June 2026 implementation of Annex XVII restrictions targets residual monomer content and volatile byproducts, directly impacting traditional sol-gel chemistries that rely on hydrolysis of silane-based compounds. Under the updated framework, formulations must comply with stringent semi-volatile organic compound emission limits of less than 0.1 mg/m³ over a 28-day aging period, effectively mandating the adoption of pre-polymerized or low-monomer precursor systems. This requirement is accelerating innovation in controlled hydrolysis processes and precursor stabilization technologies to minimize emissions without compromising coating performance. In parallel, the EU Green Deal’s Zero Pollution Action Plan is reinforcing the shift away from solvent-heavy systems, with European manufacturers reporting a 35% increase in water-borne sol-gel coating adoption. These water-based systems not only reduce VOC liabilities but also align with broader sustainability targets in architectural and industrial applications. As regulatory scrutiny intensifies, sol-gel coatings are evolving toward ultra-low emission, environmentally compliant formulations that retain their inherent advantages in adhesion, hardness, and chemical resistance.

Market Trend: US DoD Performance Specifications Accelerate Adoption of Non-Chromate Sol-Gel Pretreatments

The transition from prescriptive to performance-based specifications within the U.S. Department of Defense is significantly advancing the adoption of sol-gel coatings in aerospace and defense applications. Under revised standards such as MIL-PRF-32239 and emerging MIL-PRF-2025 guidelines, sol-gel adhesion promoters are becoming a mandatory interface layer between non-chromate surface treatments and protective primers. This shift is driven by the need to eliminate hexavalent chromium while maintaining or exceeding corrosion protection benchmarks. To meet 2026 qualification requirements, sol-gel systems must demonstrate zero corrosion undercutting and no blistering after 2,000 hours of neutral salt spray exposure on high-strength aluminum alloys such as AA7075-T6. Beyond corrosion resistance, sol-gel coatings offer substantial weight reduction advantages, with thin-film pretreatments reducing surface treatment mass by up to 90% compared to traditional chromate conversion coatings. This translates into measurable operational benefits, including an estimated 0.5% improvement in fuel efficiency for long-range aircraft. Additionally, process efficiency gains are notable, as qualified sol-gel systems enable a ready-to-paint window within 30 minutes, reducing production cycle times and increasing throughput in aerospace manufacturing environments. These performance and efficiency gains are positioning sol-gel coatings as a critical enabler of next-generation, environmentally compliant aerospace finishing systems.

Market Opportunity: Anti-Reflective Sol-Gel Coatings Enhancing Energy Yield in High-Efficiency Solar Photovoltaic Systems

The rapid expansion of the global solar energy sector is creating strong demand for advanced surface engineering solutions, with sol-gel-based anti-reflective coatings emerging as a standard specification for high-performance photovoltaic modules. These coatings, typically based on nanostructured silicon dioxide matrices, are engineered to minimize optical losses and maximize light transmission across a broad spectral range. Field data from 2026 indicates that anti-reflective sol-gel coatings can increase annual electricity generation by approximately 5.5%, while simultaneously reducing the levelized cost of energy by 2.7% in utility-scale installations. This performance improvement is achieved through the reduction of front-surface reflection from approximately 4% to below 1% across wavelengths ranging from 400 nm to 1100 nm, significantly enhancing photon capture in advanced N-type and bifacial solar cells. Additionally, biomimetic “moth-eye” nanostructures are improving angular light acceptance by around 15%, enabling higher energy yield during low-angle sunlight conditions such as early morning and late afternoon. As solar developers prioritize efficiency gains and cost optimization, anti-reflective sol-gel coatings are becoming a critical component in next-generation photovoltaic module design.

Market Opportunity: Superhydrophobic and Photocatalytic Sol-Gel Coatings Transforming Low-Maintenance Building Facades

Superhydrophobic sol-gel coatings incorporating titanium dioxide and silica nanostructures are unlocking new opportunities in sustainable architecture and green building design. These coatings deliver dual functionality by combining photocatalytic activity with ultra-low surface energy, enabling self-cleaning surfaces that significantly reduce maintenance requirements. Performance testing in 2026 demonstrates that sol-gel coatings containing anatase titanium dioxide achieve up to 96.7% degradation efficiency for organic pollutants under UV exposure, effectively breaking down contaminants on building facades. Simultaneously, these coatings maintain water contact angles exceeding 140 degrees even after prolonged exposure to acidic and alkaline environments, meeting stringent durability requirements for long-term exterior applications. The reduction of surface energy to below 20 mN/m allows water to form a continuous sheeting effect, removing up to 90% of accumulated particulate matter during rainfall events. This functionality is particularly valuable in urban environments where pollution and particulate deposition are significant challenges. In addition to reducing maintenance costs, these coatings contribute to mitigating urban heat island effects by maintaining cleaner, more reflective building surfaces. As green certification frameworks such as LEED and BREEAM increasingly emphasize lifecycle performance and maintenance efficiency, superhydrophobic sol-gel coatings are gaining traction as a high-value solution in modern building envelope systems.

Sol-Gel Coatings Market Share and Segmentation Insights: Hybrid Technology Leadership and Automotive Sector Demand

By Product Type: Hybrid Sol-Gel Coatings Dominate with Balanced Performance and Low-Temperature Processing

The hybrid sol-gel coatings (organic-inorganic) segment led the market with a 52.8% share in 2025, driven by its unique ability to deliver a balanced combination of mechanical strength, flexibility, and multifunctional performance. By integrating inorganic components for hardness and thermal stability with organic networks for flexibility and adhesion, hybrid sol-gel coatings enable advanced functionalities such as anti-scratch, anti-corrosion, anti-reflective, and hydrophobic properties across plastics, metals, and glass substrates. A key advantage is their low-temperature curing capability (80–150°C), making them ideal for heat-sensitive materials such as polycarbonate, acrylic, and composite substrates, where traditional ceramic coatings require significantly higher temperatures (>400°C). This versatility supports growing adoption in automotive, electronics, and optical applications, positioning hybrid sol-gel coatings as a leading solution in next-generation functional coating technologies.

By End-User Industry: Automotive and Transportation Segment Leads with Lightweight Protection and Regulatory Compliance

The automotive and transportation segment accounted for the largest 27.4% share of the sol-gel coatings market in 2025, fueled by increasing demand for lightweight, high-performance protective coatings. Hybrid sol-gel coatings are widely used for anti-scratch and anti-fingerprint clearcoats in automotive interiors, including touchscreens, dashboards, and trim components, as well as exterior plastic parts such as headlight lenses and decorative trims. These coatings enhance durability without adding significant weight, supporting vehicle efficiency and design innovation. Additionally, sol-gel-based primers provide chrome-free corrosion protection for aluminum, magnesium, and zinc alloys, aligning with stringent environmental regulations such as REACH and ELV directives. This makes them highly attractive for both automotive and aerospace component manufacturing. With rising focus on sustainable coatings, lightweight materials, and advanced surface protection, the automotive sector continues to drive growth in the global sol-gel coatings market.

Competitive Landscape of the Sol-Gel Coatings Market

PPG Leads Market with Advanced Sol-Gel Ceramics and Data Center Applications

PPG Industries, Inc. remains the technological vanguard in the sol-gel coatings market, leveraging its innovation leadership and strong R&D capabilities. The company has introduced PFOA-free sol-gel ceramic coatings for cookware, delivering up to 40% higher abrasion resistance compared to traditional PTFE systems. PPG is also expanding into data center infrastructure, using sol-gel thermal barrier coatings to reduce cooling energy consumption by up to 15%. Its integration of sol-gel chemistry into marine coatings further enhances sustainability through biocide-free, low-friction solutions.

AkzoNobel Strengthens Market Position with Low-Cure Sol-Gel Coatings and Aerospace Expansion

AkzoNobel N.V. is a major player in the sol-gel coatings market, focusing on sustainability and high-performance applications. The company has introduced low-cure sol-gel powder coatings and expanded its aerospace coatings capacity through a €50 million facility upgrade in the U.S. Its innovations include sol-gel pigments for enhanced UV stability and laser-curing technologies that reduce curing time by up to 60%. AkzoNobel’s strategic merger with Axalta is expected to further strengthen its global coatings leadership.

Sherwin-Williams Dominates Aerospace Segment with Chromate-Free Sol-Gel Technologies

The Sherwin-Williams Company is a leader in the sol-gel coatings market, particularly in aerospace and specialty coatings. Its sol-gel aircraft pre-treatment systems eliminate the need for chromate-based primers, reducing environmental impact while improving adhesion performance. The company’s sol-gel clearcoats provide superior gloss retention and high UV reflectivity, making them ideal for aircraft and infrastructure applications. Its strong financial performance supports continued innovation and market expansion.

Nippon Paint Drives APAC Growth with AI-Driven and Antiviral Sol-Gel Coatings

Nippon Paint Holdings Co., Ltd. is a key growth leader in the sol-gel coatings market, leveraging strong regional presence and innovation partnerships. The company is utilizing generative AI to accelerate sol-gel formulation development, targeting carbon-neutral urban applications. Its antiviral sol-gel coatings achieve 99.9% pathogen neutralization, making them suitable for high-touch surfaces in healthcare and public infrastructure. Nippon Paint’s expansion into Central Asia further strengthens its position in emerging markets.

3M Leads Deep-Tech Applications with Nano-Ceramic and Semiconductor Coatings

3M is a major innovator in the sol-gel coatings market, focusing on advanced nano-ceramic solutions. Its coatings are widely used in semiconductor cleanrooms, offering low-friction and hydrophobic properties that improve production efficiency. The company is transitioning away from fluoropolymers toward sol-gel systems, aligning with global PFAS-free mandates. Its expertise in hybrid silica structures enables development of coatings for quantum computing and high-performance electronics, reinforcing its leadership in deep-tech applications.

NEI Advances Niche Market Leadership with Nanostructured and Self-Healing Sol-Gel Coatings

NEI Corporation is a specialist leader in the sol-gel coatings market, focusing on nanotechnology-driven solutions. Its NANOMYTE® coatings provide self-healing, transparent hardcoats for plastic substrates, widely used in autonomous vehicle sensors and optical systems. The company has developed sol-gel primers with over 2,000 hours of salt spray resistance, meeting stringent environmental standards. NEI’s focus on custom formulations for biomedical and industrial applications strengthens its position in high-value niche markets.

Germany Leading Sol-Gel Hybrid Coatings Innovation with Low-Temperature Processing and Hydrogen Economy Applications

Germany remains a global leader in the sol-gel coatings market, driven by its expertise in hybrid organic-inorganic coating technologies and precision engineering. The commercialization of low-temperature sol-gel processes is enabling the application of ultra-hard coatings on heat-sensitive polymer substrates, opening new opportunities in lightweight automotive and industrial components.

Innovation is strongly aligned with sustainability and next-generation energy systems, with the development of nanostructured sol-gel barriers for hydrogen storage tanks to prevent embrittlement in hydrogen infrastructure. Government-backed R&D investments are accelerating the creation of smart sol-gel coatings with embedded corrosion indicators, enhancing predictive maintenance. Infrastructure modernization programs, including railway upgrades, are driving the adoption of anti-graffiti and easy-clean sol-gel coatings, while regulatory transitions toward REACH-compliant, chromium-free formulations are reinforcing Germany’s leadership in environmentally sustainable coating technologies.

China Scaling Advanced Sol-Gel Coatings for Renewable Energy and Semiconductor Manufacturing

China is rapidly advancing in the global sol-gel coatings industry, transitioning from conventional protective layers to high-performance functional thin films. Government initiatives under the New Material Industry Development Plan (2025–2026) are supporting domestic production of critical sol-gel materials, particularly for semiconductor and renewable energy applications.

Technological innovation includes the large-scale deployment of photocatalytic titania-based sol-gel coatings on urban buildings to reduce air pollution, as well as the integration of graphene oxide into sol-gel matrices for transparent conductive films in electronic displays. Expansion of manufacturing capacity, including new silica facilities, is supporting demand for anti-reflective coatings in solar modules, improving energy efficiency. Additionally, sol-gel coatings are being widely adopted in aerospace applications, particularly in thermal protection systems for space launch vehicles, highlighting China’s growing influence in high-performance coating technologies.

United States Driving Aerospace-Grade and PFAS-Free Sol-Gel Coatings Innovation

The United States is a major innovator in the sol-gel coatings market, particularly in aerospace, defense, and infrastructure sectors. Regulatory shifts, including the phase-out of PFAS chemicals, are accelerating the adoption of fluorine-free sol-gel coatings as sustainable alternatives for water and oil repellency.

Technological advancements include the development of self-healing sol-gel coatings that repair micro-cracks in aircraft structures, enhancing durability and reducing maintenance costs. Infrastructure investments are driving the use of sol-gel concrete densifiers for bridges, improving structural longevity through chemical strengthening. The expansion of dry-sol manufacturing technologies is reducing the carbon footprint associated with coating production and transport. Additionally, innovations such as radiation-resistant sol-gel coatings for nuclear reactors and strong demand for anti-reflective coatings in military optics are reinforcing the United States’ leadership in advanced material applications.

Japan Leading Nano-Scale Sol-Gel Coatings for Electronics, Medical Devices, and Automotive Applications

Japan is a global leader in nano-scale sol-gel coatings, focusing on precision applications in electronics, healthcare, and automotive industries. Breakthroughs in ultra-thin dielectric sol-gel layers are enabling advancements in high-density electronic components such as multilayer ceramic capacitors.

The automotive sector is adopting glass-ceramic sol-gel coatings for EV battery protection, providing superior fire resistance and electrical insulation. Government initiatives are supporting the development of biocompatible sol-gel coatings for medical implants, improving patient outcomes. Product innovations such as anti-fogging sol-gel coatings for medical devices and expansion of clean-room manufacturing facilities for semiconductor applications are further strengthening Japan’s position. High demand for scratch-resistant coatings in premium consumer appliances highlights the versatility of sol-gel technologies across multiple industries.

India Emerging as a High-Growth Market for Sol-Gel Coatings in Infrastructure and Sustainable Technologies

India is witnessing rapid growth in the sol-gel coatings market, driven by infrastructure expansion and increasing focus on sustainable materials. Government initiatives, including the Production Linked Incentive (PLI) scheme, are encouraging investment in specialty coatings R&D, boosting domestic capabilities.

Infrastructure projects are driving demand for solar-reflective sol-gel coatings to reduce urban heat, while the expansion of silica production is supporting the manufacturing of high-performance materials such as green tires. Key applications include zinc-rich sol-gel primers for railway infrastructure and innovations such as low-cost sol-gel water purification systems for rural communities. Technological advancements, including automated production processes, are improving efficiency and reducing waste in coating applications, positioning India as a key growth market in the global sol-gel coatings industry.

South Korea Driving Optoelectronic and Semiconductor Applications of Sol-Gel Coatings

South Korea is a global leader in optoelectronic sol-gel coatings, driven by its strong presence in the semiconductor and display industries. Innovations such as moisture barrier sol-gel coatings for OLED displays are significantly improving device durability and lifespan.

Technological advancements include the development of high-refractive index sol-gel materials that enhance light extraction efficiency in advanced display technologies. Strategic investments in electronic-grade silane production are ensuring a stable supply chain for high-performance coatings. Regulatory updates are promoting the adoption of water-based sol-gel systems, aligning with sustainability goals. Additionally, the use of anti-static sol-gel coatings in semiconductor manufacturing environments highlights South Korea’s leadership in precision coating applications critical for high-tech industries.

Sol-gel Coatings Market Report Scope

Sol-gel Coatings Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$4 Billion

|

|

Market Size (2032)

|

$9.2 Billion

|

|

Market Growth Rate

|

12.7%

|

|

Segments

|

By Product (Inorganic Sol-Gel Coatings, Organic Sol-Gel Coatings, Hybrid Sol-Gel Coatings, Nanocomposite Coatings), By Coating Approach (Sol-Gel Layering, Microencapsulation, UV-Curable Sol-Gel, Self-Crosslinking Systems, Thermal Spray Sol-Gel), By Function (Protective Coatings, Functional, Energy and Thermal Coatings), By End-User Industry (Automotive and Transportation, Aerospace and Defense, Electronics and Semiconductors, Building and Construction, Healthcare and Biomedical, Energy, Consumer Goods)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

3M Company, PPG Industries, Inc., Akzo Nobel N.V., The Sherwin-Williams Company, BASF SE, Evonik Industries AG, Henkel AG and Co. KGaA, SCHOTT AG, SOCOMORE SASU, Arkema S.A., Mitsubishi Materials Corporation, Saint-Gobain, Vibrantz Technologies, Kansai Paint Co., Ltd., Nanovations Pty Ltd

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Sol gel Coatings Market Segmentation

By Product

- Inorganic Sol-Gel Coatings

- Organic Sol-Gel Coatings

- Hybrid Sol-Gel Coatings

- Nanocomposite Coatings

By Coating Approach

- Sol-Gel Layering

- Microencapsulation

- UV-Curable Sol-Gel

- Self-Crosslinking Systems

- Thermal Spray Sol-Gel

By Function

- Protective Coatings

- Functional

- Energy and Thermal Coatings

By End-User Industry

- Automotive and Transportation

- Aerospace and Defense

- Electronics and Semiconductors

- Building and Construction

- Healthcare and Biomedical

- Energy

- Consumer Goods

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Sol gel Coatings Industry

- 3M Company

- PPG Industries, Inc.

- Akzo Nobel N.V.

- The Sherwin-Williams Company

- BASF SE

- Evonik Industries AG

- Henkel AG & Co. KGaA

- SCHOTT AG

- SOCOMORE SASU

- Arkema S.A.

- Mitsubishi Materials Corporation

- Saint-Gobain

- Vibrantz Technologies

- Kansai Paint Co., Ltd.

- Nanovations Pty Ltd

*- List not Exhaustive