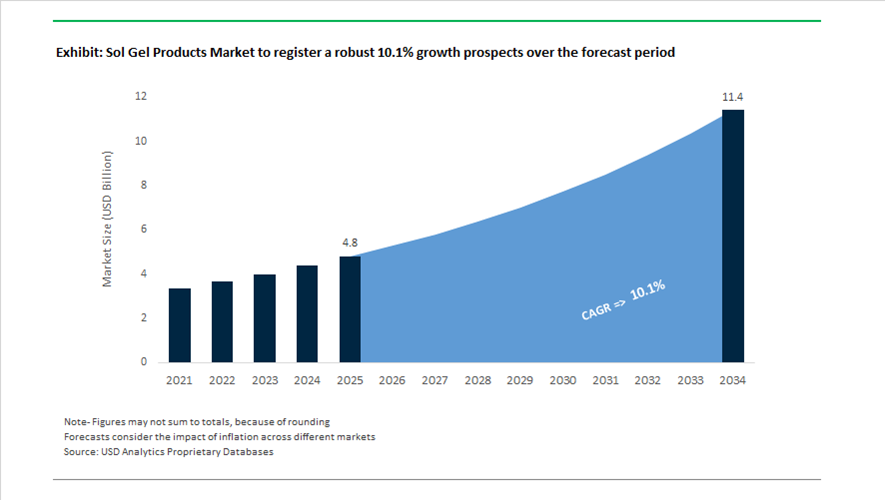

Sol Gel Products Market Valuation 2025–2034: $4.8 Billion to $11.4 Billion at 10.1% CAGR Accelerated by PFAS-Free Coatings, AR Optics, and Aerospace Innovation

The global sol gel products market is valued at $4.8 billion in 2025 and is projected to reach $11.4 billion by 2034, expanding at a robust CAGR of 10.1%. Growth is fueled by increasing adoption of sol-gel coatings, ceramic thin films, optical layers, biomedical formulations, and corrosion-resistant surface treatments across aerospace, automotive, marine, semiconductor, cookware, and medical dermatology sectors. Sol-gel technology enables precise nanostructured coatings with superior hardness, thermal stability, optical transparency, and chemical resistance while supporting PFAS-free and low-VOC formulations. Regulatory pressure against persistent fluorinated compounds and the shift toward lightweight, high-durability materials in EVs, AR devices, and aircraft are accelerating commercialization of advanced sol-gel chemistries.

In July 2024, Sol-Gel Technologies signed six licensing agreements across Europe and South Africa to commercialize its proprietary sol-gel-based dermatology drugs TWYNEO® and EPSOLAY® outside the United States, expanding pharmaceutical applications of controlled-release sol-gel systems. In September 2024, East Midland Coatings introduced Fusion Sol-Gel technology as a PFAS-free alternative to traditional PTFE coatings, aligned with EU environmental directives on persistent chemicals. In December 2024, Topciment® launched the EU-funded ZENEX project to upcycle industrial waste-derived silica into sustainable sol-gel protective coatings for construction. During late 2024, PPG introduced FUSION® Pro II, a next-generation ceramic sol-gel non-stick cookware coating delivering a 70% improvement in performance without intentionally added PFAS.

Industrial scale-up and optical innovation accelerated through 2025. In early 2025, SCHOTT completed integration of QSIL GmbH, strengthening quartz glass and sol-gel precursor capabilities critical for semiconductor wafer fabrication. The same period saw SCHOTT ramp up production at its Malaysia facility for geometric reflective waveguides manufactured using advanced sol-gel processing, targeting mass-market augmented reality smart glasses. In May 2025, POLYRISE introduced custom optical sol-gel coatings in collaboration with SAINT-GOBAIN, optimized for aerospace and automotive head-up display systems requiring enhanced optical clarity and mechanical durability. In November 2025, AkzoNobel and Axalta announced an all-stock merger of equals, creating a major global coatings entity with expanded R&D resources to advance next-generation sol-gel coatings for aerospace and automotive OEM applications.

Marine and digital material innovation shaped the 2025–2026 outlook. In December 2025, AkzoNobel extended its partnership with Winning Shipping to deploy Intersleek® 1100SR, a biocide-free sol-gel fouling control coating, across six vessels scheduled for 2026 implementation to improve fuel efficiency and reduce emissions. In January 2026, 3M unveiled an AI-driven material innovation platform at CES, enabling engineers to simulate and design sol-gel-based films and display coatings for lighter vehicles and high-reliability data center components. These developments highlight how PFAS-free compliance, AR optics manufacturing, marine efficiency mandates, semiconductor precursor integration, and AI-assisted material design are driving double-digit growth in the sol gel products market toward $11.4 billion by 2034.

Technology-Driven Trends and High-Value Opportunities in the Sol Gel Products Market

Industrial Scale-up of Sol-Gel Coatings for Aerospace and High-Temperature Infrastructure

The sol gel products market is entering a phase of industrial-scale adoption as aerospace, defense, and energy sectors actively replace legacy surface treatments with sol-gel based ceramic and hybrid coatings. This transition is not incremental. It is driven by the dual pressure of regulatory compliance and the need for higher performance on lightweight aluminum and titanium alloys used in next-generation aircraft and energy infrastructure. Sol-gel pre-treatments and coatings are increasingly specified for their ability to deliver superior adhesion, corrosion resistance, and thermal stability while eliminating hexavalent chromium and fluorinated chemistries.

In September 2025, Socomore confirmed that its SOCOGEL sol-gel coating series successfully cleared extended fatigue-life testing on aluminum alloy frames, achieving qualification with both Airbus and Boeing. These approvals represent a major inflection point, as sol-gel coatings are now validated for structural aerospace components rather than limited secondary applications. The shift is further accelerated by the 2024 EU PFAS restrictions, which are forcing aerospace OEMs and Tier 1 suppliers to adopt fluorine-free alternatives capable of operating above 400 degrees Celsius without compromising mechanical integrity.

Corrosion economics reinforce this trend. Data from the U.S. Department of Defense indicates that corrosion-related degradation costs the department approximately $20 billion annually. To reduce lifecycle costs, the DoD has prioritized water-based, chrome-free sol-gel pre-treatments such as Jet Prep systems from Sherwin-Williams. These solutions reduce application time by roughly 30% compared with multi-step conversion coatings while maintaining critical adhesion performance for advanced aerospace topcoats, directly supporting fleet readiness and maintenance efficiency.

Sol-Gel Encapsulation as the Stability Backbone for Perovskite Quantum Dot Displays

A second high-impact trend is emerging in the display industry, where sol-gel chemistry is becoming the enabling platform for stabilizing perovskite quantum dots under commercial operating conditions. As panel manufacturers push toward BT.2020 color gamut compliance and higher brightness targets for Micro-LED and QD-OLED displays, the intrinsic instability of PQDs under heat and humidity has become a critical bottleneck. Sol-gel encapsulation using silica and titania matrices is now the benchmark approach to overcome this limitation.

Peer-reviewed studies published in August 2025 demonstrate that PQDs encapsulated using sol-gel silane coupling agents can achieve photoluminescence quantum yields of up to 78% when embedded into polymer-compatible matrices. This performance threshold is essential for integrating high-purity red and green emitters into mass-produced display films that must withstand panel lamination and thermal processing. Stability data reported in late 2025 further confirms the robustness of sol-gel encapsulation. Silica-encapsulated PQDs synthesized via the Stöber sol-gel method retained more than 90% of their initial luminance after 1,000 hours under 85% relative humidity at elevated temperature. This level of durability aligns with consumer electronics lifetime requirements and positions sol-gel chemistry as a foundational material technology for next-generation 8K and large-area display platforms.

Scalable Sol-Gel Processing Routes for Solid-State Battery Electrolytes

The race to achieve electric vehicle battery energy densities approaching 500 Wh per kilogram is driving unprecedented interest in solid-state battery architectures. Within this context, sol-gel processing is emerging as a preferred manufacturing route for thin-film solid electrolytes, particularly lithium lanthanum zirconate systems. Compared with conventional solid-state sintering, sol-gel methods enable lower processing temperatures, tighter stoichiometry control, and improved microstructural uniformity, all of which are critical for ionic transport performance.

Research updated in August 2025 shows that sol-gel derived LLZO thin films with thicknesses near 300 nanometers can achieve room-temperature ionic conductivity ranging from 1.67×10−6 to 1.4×10−3 siemens per centimeter when combined with organic-inorganic hybrid modifiers. These conductivity levels are sufficient to meaningfully reduce internal cell resistance, enabling faster charging and higher discharge rates in solid-state designs. Scale-up feasibility is also improving. A landmark 2025 study introduced a solution blowing process using sol-gel precursors that produces ion-conductive ceramic fibers at speeds up to 15 times faster than traditional electrospinning. This innovation provides a credible pathway toward high-volume production of flexible ceramic separators, supporting the projected multibillion-dollar solid-state battery market expected by the end of the decade.

Bioactive Sol-Gel Coatings for Precision Medical Implant Systems

The medical device sector represents another high-value opportunity where sol-gel products are evolving from passive coatings into active, multifunctional interfaces. Implant manufacturers are increasingly adopting sol-gel coatings to create porous, drug-eluting surfaces on titanium and nitinol alloys that promote osseointegration while reducing post-surgical complications.

In May 2025, researchers demonstrated a sol-gel based drug delivery platform for porous nitinol cardiovascular implants that combined ceramic coatings with thermosensitive hydrogels. This hybrid architecture achieved a threefold increase in drug-loading capacity and sustained the release of antiproliferative agents such as rapamycin for up to 17 days, significantly lowering the risk of vascular tissue hyperplasia. Complementary bio-integration studies highlight the material advantages of advanced sol-gel compositions. Strontium- and titanium-modified silica sol-gel coatings have been shown to reduce nickel ion leaching by more than 60% while simultaneously enhancing osteoblast cell proliferation. For orthopedic and dental implant markets, these performance gains translate into an estimated 20% reduction in implant rejection risk, creating a compelling value proposition for premium, bioactive implant systems based on sol-gel surface engineering.

Sol-Gel Products Market Share and Segmentation Insights

Sol-Gel Coatings Lead the Market Through Multifunctional Surface Protection Technologies

Coatings accounted for 48.60% of the sol-gel products market in 2025, making them the dominant product category across advanced materials applications. Sol-gel coatings provide unique performance advantages including high purity, uniform composition, low-temperature processing, and strong substrate adhesion, enabling their use in corrosion protection, anti-reflective coatings, optical layers, and advanced surface treatments. These coatings are widely adopted in industries such as automotive, aerospace, and electronics, where durable and functional surfaces are critical. A major 2025 technology trend is the development of multifunctional sol-gel coatings capable of delivering multiple surface properties simultaneously, including corrosion resistance combined with anti-icing performance, anti-reflective coatings with self-cleaning capability, and antimicrobial barrier layers, supporting high-value performance in demanding industrial applications.

Electronics & Optoelectronics Sector Drives Demand for Sol-Gel Materials in Advanced Devices

Electronics and optoelectronics represent the largest end-use segment in the sol-gel products market, accounting for 32.80% of total demand in 2025 due to the need for high-purity functional materials in advanced electronic device manufacturing. Sol-gel derived materials are widely used in dielectric layers, optical coatings, semiconductor processing materials, and sensor components, where precise composition control and nanoscale structure are required. The sol-gel process enables production of highly uniform thin films and coatings suitable for sensitive electronic applications. A key 2025 innovation trend is the rapid development of flexible electronics and wearable devices, where sol-gel derived hybrid materials provide low-temperature processable dielectric coatings, barrier layers, and conductive films compatible with flexible polymer substrates used in next-generation electronic systems.

Sol-Gel Products Market Competitive Landscape

The global sol-gel products market in 2026 is driven by PFAS-free nano-ceramic coatings, low-temperature curing technologies, and high-performance hybrid sol-gel matrices. Leading players are advancing precision surface engineering, semiconductor-grade coatings, and integrated barrier solutions for automotive, aerospace, and electronics applications.

PPG Industries Expands Aerospace Sol-Gel Coatings and EV Clearcoat Innovations Through High-Capacity Manufacturing

PPG Industries is strengthening its leadership in sol-gel coatings through its $380 million North Carolina facility, designed for high-performance aerospace primers and chrome-free adhesion systems. Its sol-gel based coatings enhance corrosion resistance and bonding on aircraft aluminum substrates, aligning with stringent regulatory requirements. The company’s automotive portfolio includes advanced sol-gel clearcoats engineered for EVs, offering superior UV resistance and self-healing surface properties. PPG’s transition toward PFAS-free ceramic coatings is evident across industrial and consumer applications, including non-stick cookware systems. Its “Total Finish Solutions” strategy integrates sol-gel coatings into automated manufacturing lines, improving throughput and surface durability. The company’s focus on nano-ceramic coatings and scalable production strengthens its competitive positioning.

AkzoNobel Advances Circular Sol-Gel Smart Surfaces and Lightweight EV Coating Technologies

AkzoNobel is accelerating innovation in sustainable sol-gel coatings through its “Paint the Future” initiative, supported by €1.1 billion in funding raised in 2026. Its development of “coatings on command” leverages sol-gel chemistry to enable reversible and adaptive surface functionalities, supporting circular design principles. The company’s sol-gel primers for EV battery enclosures achieve 80–90% thinner coatings, delivering up to 25% weight reduction for improved vehicle efficiency. Demonstrations at Expo 2025 Osaka highlight large-scale applications of sol-gel and PU hybrid coatings in sustainable infrastructure. AkzoNobel’s global footprint across 150 countries enables rapid commercialization of eco-friendly coating technologies. Its focus on PFAS-free, lightweight, and high-performance coatings positions it strongly in advanced materials markets.

Arkema Strengthens Battery Materials Integration with Sol-Gel Precursors and PVDF Expansion

Arkema is leveraging its specialty materials expertise to integrate sol-gel chemistry into next-generation battery technologies and energy storage systems. Its collaboration with Senior focuses on advanced electrode coating processes using silane-based sol-gel precursors, improving adhesion and durability. The expansion of Kynar® PVDF production in China supports increased demand for high-performance battery separators and chemical-resistant coatings. Arkema’s Incellion™ solutions showcased at Interbattery 2026 demonstrate hybrid sol-gel integration capabilities for enhanced safety in large-scale energy storage. The company is reallocating R&D toward semi-solid battery technologies, where sol-gel derived electrolytes are expected to improve energy density. Its alignment with the global battery value chain strengthens its strategic position in advanced coatings.

Evonik Industries Optimizes Sol-Gel Additives and Alkoxy Silane Production Through Advanced Technologies Strategy

Evonik Industries is reinforcing its position in the sol-gel products market through its Advanced Technologies segment, generating €5.97 billion in revenue and focusing on high-value inorganic precursors. The company is scaling production of alkoxy silanes, essential for gradient coatings, antimicrobial films, and optical applications. Its streamlined North American distribution model enhances technical support and market penetration for sol-gel additives and coating systems. The “Evonik Tailor Made” program accelerates commercialization of crosslinkers and hybrid material components used in nano-ceramic coatings. Evonik’s innovation in materials informatics supports the development of high-performance sol-gel films for tissue engineering and optics. Its focus on customized additives and advanced inorganics strengthens its role in specialty coating solutions.

Merck Group Strengthens Semiconductor-Grade Sol-Gel Precursors and Thin Film Innovations for Advanced Electronics

Merck Group is a critical supplier of high-purity sol-gel precursors for semiconductor and photovoltaic applications, supported by €21.1 billion in 2025 net sales and a strong 28.9% EBITDA margin. Its “for synthesis” product line enables precise chemical mechanical planarization and conductive paste formulation for advanced chip manufacturing. The integration of Intermolecular® accelerates commercialization of nano-coatings for display, sensor, and semiconductor technologies. Merck’s focus on sol-gel derived thin films enhances control over refractive index and nano-scale surface properties, critical for optronics and data storage systems. Its materials play a key role in enabling next-generation electronics and AR/VR sensor technologies. The company’s emphasis on ultra-high-purity chemicals positions it at the forefront of semiconductor-grade sol-gel innovation.

United States Sol Gel Products Market Anchored by Aerospace Qualification and Semiconductor Purity

The United States sol gel products industry is advancing through aerospace-grade qualification, semiconductor-driven purity standards, and pharmaceutical microencapsulation leadership. In late 2024 and throughout 2025, Sherwin-Williams Aerospace Coatings scaled deployment of its Jet Prep Pretreatment CM0220P01, a water-based, chrome-free sol-gel conversion coating engineered to enhance adhesion of high-performance aircraft topcoats. Adoption across commercial and defense aviation platforms reflects a structural shift away from chromates while preserving corrosion resistance and long-term coating integrity. In parallel, the CHIPS Act has accelerated investments in ultra-high purity silica and titania sol production for Chemical Mechanical Planarization applications supporting sub-5 nm semiconductor nodes, reinforcing sol-gel chemistry as a critical enabler of advanced wafer fabrication.

Cross-sector innovation remains a defining feature. A strategic collaboration announced in July 2024 between 3M and DuPont focuses on nanostructured sol-gel coatings for renewable energy glass and electronic displays, with emphasis on anti-reflective performance and durability. In healthcare, Sol-Gel Technologies Ltd. secured multiple FDA approvals during 2024–2025 for TWYNEO and EPSOLAY, leveraging proprietary silica-based sol-gel microencapsulation to stabilize active ingredients and improve controlled delivery. Federal defense funding is also supporting sol-gel derived ceramic fibers for next-generation turbine engines capable of sustained operation above 1200°C, while pilot lines for transparent conductive sol-gel coatings are emerging in flexible smart window applications.

Germany Sol Gel Products Market Defined by Industrial Scale-Up and Regulatory Leadership

Germany represents a mature and regulation-led sol gel ecosystem, characterized by industrial-scale coating production, advanced surface engineering, and early compliance with environmental mandates. In 2024, BASF SE expanded sol-gel coating capacity at its Schwarzheide site to meet rising demand from automotive and energy customers seeking high-durability, low-emission surface solutions. Regulatory preparedness is a competitive advantage, as German manufacturers have completed the transition to VOC-free sol-gel systems ahead of the 2026 EU REACH requirements, positioning domestically produced coatings as preferred materials for eco-certified construction and infrastructure projects.

Product-level differentiation continues to deepen. In September 2025, SCHOTT commenced serial production of its CERAN matte cooktop surfaces, using a specialized sol-gel process to achieve fingerprint resistance and enhanced scratch durability. Beyond consumer applications, Germany remains a center for biomedical and heritage protection research. German-affiliated research hubs such as Materia Nova introduced tunable, biocompatible sol-gel scaffolds for bone tissue engineering in 2025, while Fraunhofer-linked institutes accelerated development of organic-inorganic hybrid ORMOCER coatings designed to protect cultural monuments from acid rain and environmental degradation.

China Sol Gel Products Market Scaled by EV Safety, Solar Efficiency, and Infrastructure Mandates

China has emerged as the global volume leader in sol-gel-derived functional materials, driven by electric vehicle safety requirements, photovoltaic efficiency gains, and policy-backed infrastructure upgrades. In 2025, new production facilities in Jiangsu significantly expanded output of sol-gel derived silica aerogel blankets, supplying domestic EV manufacturers with lightweight thermal insulation materials engineered to mitigate thermal runaway in high-density battery packs. The photovoltaic sector has also integrated sol-gel chemistry at scale. By late 2024, major solar glass producers adopted dual-layer sol-gel anti-reflective coatings that increase light transmission by more than 3%, directly enhancing performance of PERC and TopCon cell architectures.

Government policy is reinforcing deployment. The Ministry of Industry and Information Technology’s 2025 New Material guidelines prioritize subsidies for sol-gel technologies enabling self-cleaning and photocatalytic glass in urban construction. Semiconductor localization strategies are also progressing, as domestic firms have synthesized sol-gel based photoresists for mid-range lithography, reducing reliance on imported chemical precursors. In infrastructure, new coastal projects initiated in 2025 mandate sol-gel anti-corrosion primers for steel and rebar to extend asset life in high-salinity environments, embedding sol-gel coatings into national durability standards.

India Sol Gel Products Market Accelerated by Deep-Tech Funding and Biomedical Localization

India’s sol gel products market is transitioning from academic research toward commercialization, supported by large-scale public funding and targeted acquisitions. In July 2025, the Union Cabinet approved the Research Development and Innovation Scheme with an outlay of ₹1.0 lakh crore, allocating significant capital to sunrise sectors such as nanomaterials and sol-gel based clean energy technologies. This funding environment is catalyzing pilot-scale manufacturing and translational research across energy storage, coatings, and advanced ceramics.

Private investment is reinforcing domestic capability. In August 2025, Lionstead Ventures acquired Ceramat, strengthening India’s production of sol-gel derived hydroxyapatite for dental and orthopedic implants. Public-sector innovation is also visible in water treatment, where the Department of Science and Technology showcased a hybrid adsorbent utilizing a sol-gel-like porous carbonization process capable of removing up to 90% of heavy metals from industrial wastewater. In textiles, sol-gel based antimicrobial finishes are being deployed for heritage fabrics, supported by the Centre for Sustainable Textile Heritage at IIT Delhi, linking material science with cultural preservation.

Japan Sol Gel Products Market Driven by Miniaturization and Optical Precision

Japan’s sol gel industry is distinguished by precision engineering, electronic miniaturization, and advanced optical materials. In 2025, Shin-Etsu Chemical and Kyocera expanded production of sol-gel derived ceramic capacitors offering superior capacitance-to-volume ratios, addressing the stringent size and performance requirements of emerging 6G hardware. This capability underscores Japan’s leadership in translating sol-gel chemistry into mass-produced electronic components.

Optical applications remain a core strength. Japanese firms have pioneered fluorine-doped sol-gel silica for ultra-low-loss optical fibers, positioning domestic suppliers for large-scale data center and telecom infrastructure upgrades planned for 2026. Automotive coatings are another area of commercialization, with premium brands adopting sol-gel based self-healing clearcoats that repair micro-scratches at ambient conditions, extending vehicle aesthetics and reducing lifecycle maintenance intensity.

Comparative Snapshot: Country-Level Sol Gel Products Industry Dynamics

Sol Gel Products Market County Level Snapshot

|

Country

|

Core Demand Drivers

|

Strategic Focus Areas

|

Structural Impact

|

|

United States

|

Aerospace, semiconductors, dermatology

|

Chrome-free pretreatments, UHP sols, microencapsulation

|

Qualification-led adoption and federal backing

|

|

Germany

|

Automotive, construction, heritage

|

VOC-free sol-gel, ORMOCER hybrids

|

Regulatory leadership and industrial scaling

|

|

China

|

EV batteries, solar PV, infrastructure

|

Aerogels, AR coatings, anti-corrosion primers

|

Volume leadership and policy-driven deployment

|

|

India

|

Clean energy, biomaterials, water treatment

|

Public RDI funding, biomedical localization

|

Transition from research to commercialization

|

|

Japan

|

Electronics, optics, automotive finishes

|

Miniaturized ceramics, optical sol-gels

|

Precision manufacturing and premium applications

|

Sol Gel Products Market Report Scope

Sol Gel Products Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$4.8 Billion

|

|

Market Size (2034)

|

$11.4 Billion

|

|

Market Growth Rate

|

10.1%

|

|

Segments

|

By Product Type (Coatings, Ceramics & Glass, Powders & Granules, Thin Films, Gels & Monoliths), By Material Type (Silica-Based, Titania-Based, Alumina-Based, Zirconia-Based, Hybrid Materials), By Synthesis Process (Alkoxide Route, Aqueous Route, Non-Hydrolytic Sol-Gel), By End-Use Industry (Automotive, Aerospace & Defense, Electronics & Optoelectronics, Healthcare & Biomedical, Energy, Building & Construction)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF SE, PPG Industries Inc., Akzo Nobel NV, SCHOTT AG, 3M Company, Corning Incorporated, Shin-Etsu Chemical Co. Ltd., Dow Inc., Evonik Industries AG, Sol-Gel Technologies Ltd., Henkel AG & Co. KGaA, Mitsubishi Chemical Group, Saint-Gobain SA, Kyocera Corporation, Heraeus Holding

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Sol-Gel Products Market Segmentation

By Product Type

- Coatings

- Ceramics & Glass

- Powders & Granules

- Thin Films

- Gels & Monoliths

By Material Type

- Silica-Based

- Titania-Based

- Alumina-Based

- Zirconia-Based

- Hybrid Materials

By Synthesis Process

- Alkoxide Route

- Aqueous Route

- Non-Hydrolytic Sol-Gel

By End-Use Industry

- Automotive

- Aerospace & Defense

- Electronics & Optoelectronics

- Healthcare & Biomedical

- Energy

- Building & Construction

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Sol-Gel Products Industry

- BASF SE

- PPG Industries Inc.

- Akzo Nobel NV

- SCHOTT AG

- 3M Company

- Corning Incorporated

- Shin-Etsu Chemical Co. Ltd.

- Dow Inc.

- Evonik Industries AG

- Sol-Gel Technologies Ltd.

- Henkel AG & Co. KGaA

- Mitsubishi Chemical Group

- Saint-Gobain SA

- Kyocera Corporation

- Heraeus Holding

*- List not Exhaustive