Performance-Critical Applications and Industrial Durability Sustaining Stable Growth

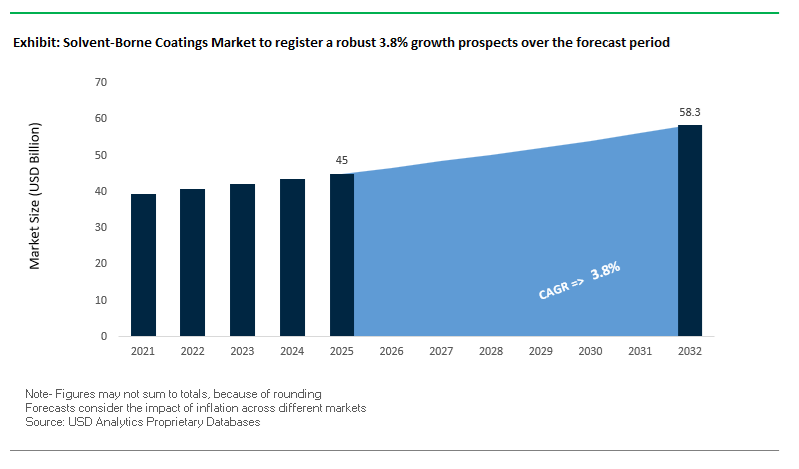

The global Solvent-Borne Coatings Market continues to hold a critical position within the broader coatings industry, driven by its superior performance characteristics in demanding environments. The market was valued at $45 billion in 2025 and is projected to reach $58.4 billion by 2032, expanding at a CAGR of 3.8% during 2025–2032. Despite regulatory pressure favoring waterborne alternatives, solvent-borne coatings remain indispensable in applications requiring high durability, rapid curing, strong adhesion, and resistance to extreme chemical and environmental conditions.

A key structural driver is the sustained demand from automotive refinish, aerospace, marine, oil & gas, and heavy industrial sectors, where performance requirements often exceed the capabilities of water-based systems. Solvent-borne coatings provide enhanced film formation under variable environmental conditions, making them suitable for outdoor and high-humidity applications. Their ability to deliver fast drying times and superior finish quality also supports productivity in industrial operations, particularly in large-scale infrastructure and manufacturing projects.

Another major growth factor is the evolution of low-VOC and high-solids solvent formulations, which aim to balance regulatory compliance with performance advantages. Manufacturers are increasingly developing advanced solvent-borne chemistries that reduce emissions while maintaining the core benefits of solvent systems. This includes innovations in polyaspartics, epoxies, and acrylic technologies, which are being optimized for faster curing, extended durability, and improved environmental profiles.

Additionally, solvent-borne coatings remain central to specialty applications, including fire protection, corrosion under insulation (CUI) prevention, and pharmaceutical-grade cleanroom environments. These niche but high-value segments ensure the continued relevance of solvent-based systems, particularly where regulatory approvals, technical performance, and reliability are non-negotiable.

Market Analysis: Industry Consolidation, Aerospace Expansion, and High-Performance Product Innovation Reshaping Competitive Landscape

The solvent-borne coatings market is undergoing significant transformation driven by large-scale consolidation, portfolio restructuring, and continuous product innovation, reinforcing its importance in high-performance industrial applications. The proposed merger of equals between AkzoNobel and Axalta (2025–2026) represents one of the most significant consolidation moves in the coatings industry. This transaction combines Axalta’s strength in automotive and mobility coatings with AkzoNobel’s industrial scale, creating a dominant global entity in solvent-borne refinish and industrial coatings.

Strategic investments in manufacturing capacity are also strengthening market positioning. In March 2026, AkzoNobel completed a €50 million upgrade to its Waukegan, Illinois aerospace coatings facility, scaling production of advanced solvent-borne pretreatments and topcoats required for high-durability aviation applications. This highlights the continued reliance on solvent-based systems in safety-critical and performance-intensive sectors.

Portfolio restructuring is further reshaping competitive dynamics. BASF’s planned carve-out and sale of its automotive coatings business (Q2 2026) signals a strategic shift toward focused operations, with the new standalone entity expected to manage a significant share of the global solvent-borne automotive coatings supply chain.

Product innovation remains a central competitive lever. Sherwin-Williams’ August 2025 launch of Acrolon 680, a solvent-based acrylic polyaspartic, delivers fast-drying performance combined with lower VOC levels, addressing regulatory challenges while maintaining performance advantages. Similarly, its Heat-Flex® AEB (March 2025) targets corrosion under insulation (CUI) in high-temperature industrial environments, while the FIRETEX® FX7002 expansion (March 2024) enhances fire protection capabilities for structural steel, providing up to two hours of resistance.

In specialized environments, Sherwin-Williams’ next-generation pharmaceutical cleanroom coatings (March 2025) demonstrate the continued importance of solvent-borne epoxies in highly controlled, chemically aggressive environments requiring repeated sterilization cycles.

Supply chain optimization is also improving market efficiency. Evonik’s February 2026 distribution consolidation in North America enhances the delivery of specialized additives that optimize flow, leveling, and performance in solvent-borne coatings, supporting both automotive and industrial applications.

Meanwhile, Jotun’s November 2024 launch of next-generation barrier technologies introduces high-solids solvent-borne zinc primers designed for rapid curing and reduced recoat times in shipyards and offshore environments, reinforcing the operational advantages of solvent chemistry.

Additionally, AkzoNobel’s involvement in Calosol heat-absorbing technology demonstrates the expanding role of solvent-borne carriers in enabling advanced functional coatings, particularly in architectural applications requiring consistent adhesion and performance across diverse substrates.

Market Trend: CARB SCM and South Coast AQMD Rule 1113 Establish De-Facto 50 g/L VOC Benchmark Across U.S. Architectural Coatings

The solvent borne coatings industry is facing accelerated contraction in the architectural segment as California’s regulatory framework tightens VOC thresholds to near-zero levels. Under the combined enforcement of the California Air Resources Board Suggested Control Measure and South Coast AQMD Rule 1113, a 50 g/L VOC cap is now effectively universal for both interior and exterior coatings as of 2026. This threshold renders the majority of traditional solvent borne alkyd paints and wood stains non-compliant, as these products typically operate in the 250 to 350 g/L VOC range. As a result, approximately 90% of legacy solvent borne architectural formulations have been eliminated from the California retail ecosystem, forcing manufacturers to transition toward water borne acrylics, hybrid resins, and 100% solids technologies. The regulatory influence extends beyond California, with more than 12 U.S. states, including members of the Ozone Transport Commission, formally aligning with the same VOC limits. This convergence is creating a de facto national compliance standard, fundamentally reshaping product portfolios, distribution strategies, and raw material sourcing. The architectural coatings segment is therefore experiencing a structural shift away from solvent-based chemistry, with compliance-driven innovation focusing on ultra-low VOC and zero-VOC alternatives.

Market Trend: EPA NESHAP 2026 Amendments Increase Compliance Costs for Solvent-Based Manufacturing Operations

The U.S. Environmental Protection Agency’s updated National Emission Standards for Hazardous Air Pollutants for miscellaneous coating manufacturing facilities is significantly increasing the regulatory burden on solvent borne coatings production. The 2026 amendments mandate a cumulative annual reduction of approximately 4,900 tons of hazardous air pollutants, including key solvents such as toluene, xylene, and ethylbenzene. These substances are prevalent in solvent-based industrial coatings, making this segment a primary target for emission reduction efforts. Facilities are now required to implement enhanced leak detection and repair protocols and demonstrate a minimum control efficiency of 95% for process vent emissions. Achieving this level of control typically necessitates capital-intensive investments in thermal oxidizers, carbon adsorption systems, or other advanced emission abatement technologies. Consequently, the cost structure of solvent borne coatings manufacturing is increasing, reducing competitiveness relative to water borne and high-solids alternatives. This regulatory pressure is also influencing capacity planning decisions, with some manufacturers consolidating or retrofitting facilities to meet compliance requirements. As emission regulations continue to tighten, the solvent borne coatings industry is undergoing a gradual but decisive transition toward more sustainable production models.

Market Opportunity: Ultra-High-Solids Solvent Borne Coatings Sustain Relevance in Marine and Offshore Corrosion Protection

Despite regulatory pressures, solvent borne coatings continue to hold a critical position in high-performance industrial applications, particularly in marine and offshore environments where durability requirements exceed the capabilities of many water borne systems. Ultra-high-solids solvent borne coatings, with volume solids content ranging from 80% to 95%, are emerging as a key innovation segment that balances VOC compliance with performance. These formulations can achieve VOC levels below 150 g/L while enabling single-coat, high-build applications exceeding 300 microns of dry film thickness. This capability reduces labor requirements by 30% to 40% compared to multi-coat systems, delivering significant cost advantages in large-scale offshore projects. In terms of corrosion resistance, ultra-high-solids epoxies consistently achieve more than 10,000 hours of neutral salt spray performance under ASTM B117 testing, meeting the stringent demands of C5-M marine environments. Additionally, these coatings exhibit edge retention ratios above 70%, ensuring adequate film build on welds and sharp edges that are most susceptible to corrosion initiation. As offshore wind, oil and gas, and maritime infrastructure investments expand, ultra-high-solids solvent borne coatings remain a technically indispensable solution within the protective coatings market.

Market Opportunity: Low-Temperature Cure Solvent Borne Epoxies Enable Year-Round Infrastructure Development in Cold Regions

Low-temperature cure solvent borne epoxy coatings represent a specialized but high-growth opportunity, particularly in regions with extended cold seasons where water borne technologies are operationally constrained. These advanced formulations are engineered to achieve full mechanical cure at temperatures as low as 5°C within 24 hours, significantly expanding the workable construction window. This capability extends project timelines by approximately 60 to 90 days annually in northern geographies such as Canada and the Northern United States, improving project scheduling flexibility and asset utilization. Unlike water borne coatings, which are susceptible to freezing and flash rusting in high-humidity environments, solvent borne low-temperature systems maintain strong adhesion and film integrity at relative humidity levels up to 85%. This makes them particularly suitable for pipeline construction, bridge repair, and other critical infrastructure applications requiring reliable performance under adverse environmental conditions. Field data from 2026 indicates that these coatings improve cathodic disbondment resistance by approximately 25% in low-temperature soil environments, enhancing long-term pipeline integrity. As infrastructure investment accelerates in cold climate regions, low-temperature cure solvent borne coatings are positioned as an essential enabling technology for durable and efficient construction.

Solvent Borne Coatings Market Share and Segmentation Insights: High-Performance 2K Systems and Direct Industrial Procurement

By Resin Type: Two-Component (2K) Solvent Borne Coatings Lead with High-Build Performance and Durability

The two-component (2K) segment dominated the solvent borne coatings market with a 67.3% share in 2025, driven by its superior chemical resistance, corrosion protection, and long-term durability in demanding industrial environments. Based on advanced chemistries such as epoxy, polyurethane, and acrylic coatings, 2K systems are widely used across marine coatings, automotive coatings, aerospace coatings, and heavy industrial applications where performance requirements exceed the capabilities of waterborne alternatives. A key advantage is their high-build capability, allowing coatings to achieve film thicknesses of 100–500+ microns in a single coat without sagging, which is critical for pipeline coatings, tank linings, and heavy equipment finishing. This enables faster project completion and enhanced protection against harsh environmental conditions. The combination of high-performance protective coatings, thick film application, and industrial reliability continues to drive the dominance of 2K solvent borne coatings in the global market.

By Sales Channel: Direct Sales Channel Dominates with Technical Support and Bulk Industrial Demand

The direct sales segment accounted for a leading 50.6% share of the solvent borne coatings market in 2025, reflecting the growing importance of direct manufacturer engagement in complex industrial coating applications. Large-scale buyers in sectors such as shipbuilding, coil coating, can coating, and infrastructure protection require custom coating formulations, batch certification, and compliance with stringent regulatory standards including AIM, REACH, and EPA guidelines. Direct procurement enables manufacturers to provide technical consultation, product customization, and quality assurance, ensuring coatings meet precise application and performance specifications. Additionally, high-volume consumption industries benefit from competitive pricing, priority supply allocation, and consistent batch quality through long-term contracts with coating producers. This direct relationship minimizes supply chain disruptions and enhances operational efficiency. As demand for high-performance solvent borne coatings in industrial and marine sectors continues to grow, the direct sales channel remains a critical driver of market expansion and innovation.

Competitive Landscape of the Solvent-Borne Coatings Market

PPG Leads Market with High-Performance Polyurethanes and Digital Ecosystems

PPG Industries, Inc. remains a dominant force in the solvent-borne coatings market, leveraging its strong industrial portfolio and productivity initiatives. Following the divestiture of its North American architectural business, PPG has intensified its focus on high-margin industrial and mobility coatings. The company leads in solvent-borne polyurethane systems for automotive and heavy equipment, offering high-build properties and rapid curing. Its integration of the PPG LINQ™ platform enables AI-driven color matching, reducing paint waste in refinish applications by 15%.

AkzoNobel Strengthens Global Leadership with Aerospace Expansion and Strategic Merger

AkzoNobel N.V. is a major player in the solvent-borne coatings market, focusing on high-performance segments such as aerospace and marine coatings. The company is expanding its global footprint with a new Aerospace Coatings Hub in Dubai, supporting growing demand in the Middle East. Its ongoing merger with Axalta is expected to create a leading force in the global solvent-borne coatings market. AkzoNobel is also advancing sustainability initiatives, targeting a 50% reduction in Scope 1 and 2 emissions by 2030, while maintaining performance standards in solvent-based systems.

Sherwin-Williams Dominates Industrial Wood and Refinish Segments with High-Performance Systems

The Sherwin-Williams Company maintains a strong position in the solvent-borne coatings market, particularly in industrial wood and automotive refinish applications. Its Futura™ and Natura™ clear lacquers are industry benchmarks for fast-drying, high-quality finishes. The company has also introduced the Vindu™ outdoor range, offering 30+ years of durability for extreme exposure conditions. Its extensive distribution network, supported by the Paint Stores Group, ensures strong market penetration and customer accessibility.

Axalta Drives Innovation with AI-Powered Customization and EV-Focused Coatings

Axalta Coating Systems is a leading innovator in the solvent-borne coatings market, particularly in automotive and EV applications. Its EcoNextJet™ system enables production-scale vehicle customization using jettable solvent-borne paints, while its TintMaster AI platform improves color accuracy and reduces production inefficiencies by up to 29%. Axalta is also advancing EV safety coatings, including flame-retardant systems capable of withstanding extreme temperatures. Its strong financial performance supports continued investment in advanced coating technologies.

BASF Strengthens Market Backbone with Integrated Resin Production and Sustainable Feedstocks

BASF SE plays a critical role in the solvent-borne coatings market as a supplier of resins and additives. Its expanded production facilities in South Africa and integrated Verbund sites ensure reliable supply of key raw materials such as MDI and polyurethanes. BASF is also advancing sustainability through bio-circular feedstocks, enabling solvent-based coatings with up to 20% renewable content. Its HALS and NOR® HALS stabilizers enhance UV resistance and durability, reinforcing its position as a key enabler of high-performance coatings.

Kansai Paint Expands APAC Leadership with High-Solids Automotive and Infrastructure Coatings

Kansai Paint Co., Ltd. is a regional powerhouse in the solvent-borne coatings market, particularly in Asia-Pacific. The company is a leader in high-solids automotive coatings, delivering premium finishes while reducing VOC emissions. Its strong presence in Japan, China, and India supports growth in automotive OEM and infrastructure sectors. Kansai’s expertise in anti-corrosive alkyd and epoxy systems makes it a preferred supplier for heavy machinery and construction equipment applications, reinforcing its leadership in high-growth regional markets.

Germany Leading High-Solid Solvent Coatings Innovation with Green Solvent Integration

Germany remains a global leader in the solvent-borne coatings market, balancing high-performance requirements with strict environmental regulations. The transition toward ultra-high-solid (UHS) formulations exceeding 80% solids content is significantly reducing solvent emissions while maintaining premium finish quality required in automotive and industrial applications.

Technological advancements include the development of bio-renewable solvent carriers derived from agricultural waste, enabling compliance with green building standards without compromising coating durability. Regulatory updates under the AgBB evaluation scheme (2026) have introduced targeted exemptions for high-performance solvent coatings in critical industries, ensuring continued use in demanding applications. Infrastructure modernization, particularly in railway systems, is driving demand for solvent-borne anti-graffiti coatings known for superior chemical resistance. Additionally, Germany’s dominance in dielectric conformal coatings for semiconductor manufacturing and expansion of silicone resin production for EV battery applications reinforce its leadership in advanced solvent-based technologies.

China Strengthening Solvent-Borne Coatings for Marine, Aerospace, and High-Corrosion Environments

China is strategically reinforcing its position in the solvent-borne coatings industry, focusing on high-performance applications where waterborne alternatives fall short. Large-scale infrastructure projects are driving demand for heavy-duty epoxy solvent coatings, particularly for coastal bridges requiring long-term corrosion protection.

Technological innovation includes the development of graphene-infused solvent-borne primers designed for extreme marine environments (C5-M conditions), enhancing durability and lifespan. Regulatory frameworks are evolving, with new standards promoting low-toxicity solvent profiles while maintaining performance advantages. The aerospace sector is a key growth driver, with the use of fluorocarbon solvent coatings in space launch vehicles for superior adhesion and thermal stability. Additionally, investments in high-solid solvent coating production and innovations such as self-healing solvent-borne clearcoats for automotive applications highlight China’s focus on advanced, high-value coating solutions.

United States Driving Industrial Resurgence with Smart and High-Durability Solvent Coatings

The United States is experiencing a resurgence in the solvent-borne coatings market, driven by infrastructure modernization and industrial demand for high-durability systems. Federal investments are boosting the use of zinc-rich solvent-borne primers for bridge protection, valued for their superior penetration and corrosion resistance compared to water-based alternatives.

Technological advancements include the commercialization of fast-curing solvent-borne polyaspartic coatings, enabling rapid turnaround times in logistics and industrial flooring applications. Regulatory updates under NESHAP are allowing controlled VOC usage for coatings that significantly extend asset lifecycles. Innovation is also evident in the development of smart solvent coatings embedded with fiber-optic sensors for real-time corrosion monitoring in oil and gas pipelines. Additionally, the use of silicone-alkyd hybrid coatings for offshore wind structures and the implementation of closed-loop manufacturing systems are enhancing both performance and environmental sustainability.

India Emerging as a Major Hub for Automotive and Industrial Solvent Coatings

India is witnessing rapid growth in the solvent-borne coatings market, driven by expanding automotive production and industrialization. Significant consolidation in the sector, including major acquisitions, is strengthening domestic control over specialty solvent-based resins.

Government initiatives such as the National Rail Plan 2030 are driving demand for polyurethane solvent-borne coatings in high-speed trains, ensuring long-term UV stability and color retention. Product innovations include low-viscosity solvent coatings for humid environments, addressing regional climatic challenges. Expansion of manufacturing capacity by leading domestic companies is supporting demand from electronics and industrial sectors. Additionally, the widespread adoption of solvent-based epoxy flooring systems in pharmaceutical and clean-room environments highlights the continued importance of solvent coatings in high-performance applications, despite growing environmental regulations.

Saudi Arabia Driving Demand for High-Heat and Abrasion-Resistant Solvent Coatings

Saudi Arabia is a key growth market for solvent-borne coatings, particularly in extreme environmental conditions. Mega infrastructure projects under Vision 2030 are driving demand for polysiloxane solvent coatings capable of withstanding temperatures exceeding 80°C and resisting sand abrasion.

The energy sector remains a major application area, with mandatory adoption of corrosion-under-insulation (CUI) solvent coatings in refinery expansions to prevent costly failures. Technological innovations include sand-shedding coatings that protect solar infrastructure and architectural surfaces. Investments in domestic manufacturing capacity, including siloxane precursor facilities, are strengthening local supply chains. Additionally, regulatory frameworks emphasizing durability are reinforcing the necessity of solvent-based coatings in high-capital infrastructure projects, where long-term performance is critical.

Japan Leading Nano-Functional Solvent Coatings for Electronics and Automotive Applications

Japan is a global leader in high-purity solvent-borne coatings, focusing on nano-functionalized systems for electronics and automotive industries. Innovations such as nano-silica reinforced solvent clearcoats are delivering superior scratch resistance for automotive surfaces and touch interfaces.

Technological advancements include the development of high-reflectance cool roof coatings designed for industrial environments, enhancing energy efficiency. The country is also expanding production capacity for liquid silicone rubber (LSR) solvent coatings to support medical device manufacturing. In the automotive sector, acoustic damping solvent coatings are improving cabin comfort in electric vehicles. Regulatory updates are ensuring stricter testing for chemical leaching, enhancing product safety. Additionally, Japan’s leadership in precision conformal coatings for 5G and 6G technologies highlights its role in high-performance, electronics-focused applications.

Solvent-Borne Coatings Market Report Scope

Solvent-Borne Coatings Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$45 Billion

|

|

Market Size (2032)

|

$58.4 Billion

|

|

Market Growth Rate

|

3.8%

|

|

Segments

|

By Resin Type (One-Component, Two-Component), By Technology (High-Solids Solvent-Borne, Conventional Solvent-Borne, Radiation-Cured Solvent-Borne, Nonaqueous Dispersion), By End-User Industry (Transportation and Automotive, Oil and Gas, Manufacturing and Machinery, Infrastructure and Construction, Aerospace and Defense, Marine, Utilities and Power Generation), By Sales Channel (Direct Sales, Industrial Distributors and Wholesalers, Specialized Retail)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

The Sherwin-Williams Company, PPG Industries, Inc., Akzo Nobel N.V., BASF SE, Axalta Coating Systems Ltd., Nippon Paint Holdings Co., Ltd., Kansai Paint Co., Ltd., Jotun Group, RPM International Inc., Asian Paints Limited, Hempel A/S, KCC Corporation, Berger Paints India Limited, Tikkurila, Beckers Group

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Solvent Borne Coatings Market Segmentation

By Resin Type

- Alkyd Coatings

- Acrylic Coatings

- Epoxy Coatings

- Polyester Coatings

- Polyurethane Coatings

- Vinyl

- Epoxy-Polyamine

- Epoxy-Polyamide

- Polyurethane

- Polyurea

By Technology

- High-Solids Solvent-Borne

- Conventional Solvent-Borne

- Radiation-Cured Solvent-Borne

- Nonaqueous Dispersion

By End-User Industry

- Transportation and Automotive

- Oil and Gas

- Manufacturing and Machinery

- Infrastructure and Construction

- Aerospace and Defense

- Marine

- Utilities and Power Generation

By Sales Channel

- Direct Sales

- Industrial Distributors and Wholesalers

- Specialized Retail

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Solvent Borne Coatings Industry

- The Sherwin-Williams Company

- PPG Industries, Inc.

- Akzo Nobel N.V.

- BASF SE

- Axalta Coating Systems Ltd.

- Nippon Paint Holdings Co., Ltd.

- Kansai Paint Co., Ltd.

- Jotun Group

- RPM International Inc.

- Asian Paints Limited

- Hempel A/S

- KCC Corporation

- Berger Paints India Limited

- Tikkurila

- Beckers Group

*- List not Exhaustive