High-Speed Metal Coating Demand and Architectural Performance Driving Stable Expansion

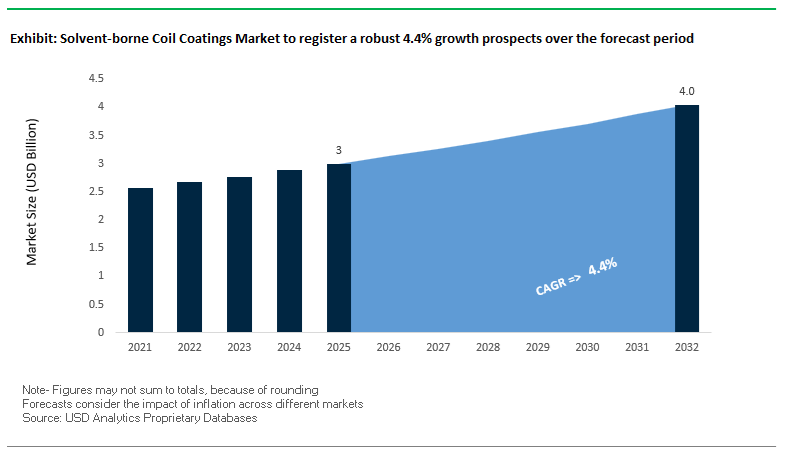

The global Solvent-Borne Coil Coatings Market continues to demonstrate steady growth, supported by strong demand from construction, appliance manufacturing, automotive components, and industrial metal processing sectors. The market was valued at $3 billion in 2025 and is projected to reach $4.1 billion by 2032, expanding at a CAGR of 4.4% during 2025–2032. This growth is closely tied to the increasing use of pre-painted metal (PPM) in building envelopes, roofing systems, facades, and white goods, where coil coatings provide uniform finish quality, corrosion resistance, and long-term durability.

A key structural driver is the reliance on high-speed coil coating lines, which demand coatings capable of rapid curing, excellent adhesion, and consistent film formation under continuous processing conditions. Solvent-borne systems remain highly preferred in these environments due to their process reliability, superior wetting behavior, and ability to perform across diverse substrates such as steel and aluminum. These characteristics make them critical for large-scale industrial production where downtime and defects must be minimized.

Another important growth factor is the increasing demand for architectural-grade finishes and functional coatings, including UV-resistant, color-stable, and weatherproof systems for exterior applications. As urban construction intensifies and design aesthetics become more sophisticated, coil coatings are evolving to deliver enhanced visual appeal alongside structural protection. Additionally, the rise of energy-efficient building materials and “cool roof” systems is influencing formulation innovation within the solvent-borne segment.

The market is also witnessing gradual transformation toward lower-VOC, high-solids, and bio-attributed solvent systems, as manufacturers seek to align with environmental regulations without compromising performance. This balance between regulatory compliance and industrial efficiency remains central to the long-term relevance of solvent-borne coil coatings in global manufacturing ecosystems.

Market Analysis: Advanced Coil Systems, and Sustainable Resin Innovation Reshaping Industry Dynamics

The competitive landscape of the solvent-borne coil coatings market is being significantly reshaped by large-scale consolidation, targeted product innovation, and sustainability-driven R&D investments. The March 2026 merger of equals between AkzoNobel and Axalta represents a transformative industry event, creating a $17 billion “super-company” with 173 manufacturing sites globally. This consolidation combines two of the largest portfolios in solvent-borne coil and industrial coatings, strengthening their position across construction, automotive, and appliance segments while enabling global supply chain optimization and innovation scale.

Product innovation remains a key competitive lever. AkzoNobel’s March 2026 launch of FIDURA™ coil coating systems introduces high-performance solvent-borne formulations designed for extreme outdoor durability and flexibility, particularly in architectural applications. The integration of a 3D digital visualization tool for architects further enhances customer engagement and project customization, reflecting the increasing importance of design-driven coating solutions.

Supply chain efficiency and additive optimization are also evolving. Evonik’s February 2026 distribution consolidation in North America improves the availability of specialized additives for high-solids solvent-borne systems, ensuring consistent performance in high-speed coil operations.

Strategic partnerships are accelerating sustainability initiatives. The November 2025 collaboration between Nippon Paint and Allnex focuses on developing bio-based and lower-carbon solvent-borne resins, particularly targeting China’s industrial coating sector. Similarly, Beckers Group’s June 2025 partnership with Anodyne Chemistries aims to introduce renewable chemical feedstocks into coil coating formulations, reducing dependence on fossil-derived materials while maintaining performance standards.

Regional innovation hubs are also playing a critical role. Beckers Group’s October 2025 R&D center launch in Shanghai is dedicated to developing localized solvent-borne and sustainable coating solutions for Asia’s rapidly expanding construction and appliance markets.

In parallel, Axalta’s 2026 “A Plan” execution highlights strong operational performance, with a focus on optimizing mobility and industrial coating segments, including specialized coil coatings for appliances and automotive components.

Advanced aesthetic and functional coatings are also gaining traction. PPG’s April 2025 launch of polychromatic metal coatings, including updates to the DURANAR® VARI-Cool® system, leverages solvent-borne carriers to deliver color-shifting metallic effects for premium architectural applications. Meanwhile, Jotun’s November 2024 next-generation barrier primers provide high-solids zinc-rich protection for coil-coated metals exposed to harsh coastal and industrial environments.

Additionally, Sherwin-Williams’ Jet Prep™ pretreatment expansion (October 2024) offers a transitional solution for existing solvent-borne coil lines, enabling manufacturers to meet evolving environmental regulations without requiring full-scale equipment replacement, thereby preserving capital efficiency.

Market Trend: EPA 40 CFR Part 63 Subpart SSSS Eliminates SSM Exemptions and Enforces Continuous HAP Compliance

The 2026 residual risk and technology review of the U.S. EPA NESHAP for surface coating of metal coil is fundamentally tightening operational compliance for solvent borne coil coating lines. The removal of startup, shutdown, and malfunction exemptions establishes a zero-tolerance compliance environment, requiring emission limits to be maintained continuously across all production phases. Facilities classified as major sources must now adhere to a strict organic hazardous air pollutant emission cap of 0.046 kg HAP per liter of solids applied, calculated on a rolling 12-month average. This requirement is compelling manufacturers to re-evaluate formulation strategies, solvent selection, and process efficiencies to remain within regulatory thresholds. Additionally, facilities relying on capture and control technologies must demonstrate a minimum of 98% overall HAP control efficiency, effectively mandating the deployment of advanced regenerative thermal oxidizers on legacy solvent-based lines. The rule also introduces mandatory digital compliance through the Compliance and Emissions Data Reporting Interface, requiring real-time monitoring and electronic reporting of emissions across coating stations. This shift toward continuous compliance and digital traceability is increasing capital expenditure and operational complexity, while simultaneously accelerating the transition toward lower-emission solvent systems and high-solids formulations in the coil coatings market.

Market Trend: China GB/T 41662-2025 Enforces Lower VOC Thresholds and Restricts Aromatic Solvent Usage

China’s GB/T 41662-2025 standard, fully enforced in early 2026, is consolidating and strengthening VOC regulations for coil coatings used in architectural and appliance applications. The new framework establishes mandatory VOC limits of 420 g/L for topcoats and 480 g/L for primers, representing a significant reduction from historical industrial averages of 550 to 600 g/L. This regulatory tightening is driving a systematic reduction in solvent intensity across the Chinese coil coatings sector, with manufacturers optimizing resin systems and solvent blends to achieve compliance. A critical component of the standard is the restriction on benzene, toluene, and xylene, limiting their combined concentration to less than 10% by weight in liquid formulations. This is forcing a transition away from traditional aromatic solvents toward oxygenated and aliphatic alternatives, which offer lower toxicity profiles but require careful formulation to maintain coating performance characteristics such as flow, leveling, and gloss retention. The standard is also influencing upstream supply chains, as raw material producers adjust solvent and resin offerings to align with compliance requirements. As China remains a dominant producer and consumer of coil-coated metals, GB/T 41662-2025 is expected to have a global ripple effect, shaping formulation standards and export competitiveness across the solvent borne coil coatings industry.

Market Opportunity: High-Solids Polyester Coil Coatings Enable Emission Reduction Without Sacrificing Line Speed or Durability

High-solids polyester coil coatings are emerging as a key solution to balance regulatory compliance with performance and productivity requirements in the architectural metal sector. By increasing solids content from conventional levels of approximately 45% to 70% or higher, these formulations significantly reduce the volume of solvent required per unit of coated substrate. This translates into an approximate 55% reduction in solvent emissions per square meter, enabling many facilities to meet stringent 2026 emission limits without extensive investment in emission control infrastructure such as regenerative thermal oxidizers. From a performance standpoint, high-solids polyesters are achieving AAMA 2604 compliance, delivering over 3,000 hours of salt spray resistance and hardness values in the 2H to 3H range. These properties position them as a cost-effective alternative to traditional polyvinylidene fluoride systems for mid- to high-performance applications. In addition, advances in rheology control have enabled these coatings to be applied at line speeds of up to 200 meters per minute without issues such as slinging or uneven edge build, maximizing throughput on continuous coil coating lines. As manufacturers seek to optimize both environmental compliance and operational efficiency, high-solids polyester systems represent a critical growth segment within the solvent borne coil coatings market.

Market Opportunity: Low-Bake PVDF Coil Coatings Reduce Energy Consumption While Expanding Substrate Compatibility

The development of low-bake polyvinylidene fluoride coil coatings is creating new opportunities in energy-efficient manufacturing and expanded substrate utilization. Traditional PVDF coatings require peak metal temperatures in the range of 232°C to 250°C to achieve full resin fusion and optimal performance. However, newly engineered low-bake systems introduced in 2026 can achieve equivalent performance at temperatures as low as 150°C to 155°C. This reduction in curing temperature delivers a direct energy savings of 25% to 30% in coil coating ovens, providing a significant operational advantage in regions subject to carbon pricing and energy cost pressures. Beyond energy efficiency, low-bake PVDF coatings enable the processing of heat-sensitive substrates, including heavy-gauge aluminum and specialty clad metals that are prone to warping or thermal distortion at higher temperatures. This expands the application range of PVDF coatings into previously inaccessible segments of the architectural and industrial metals market. Importantly, these systems maintain a high PVDF resin content of approximately 70%, ensuring long-term weatherability, UV resistance, and chalk resistance consistent with 30-year performance warranties. As sustainability and performance requirements converge, low-bake PVDF technologies are positioned as a strategic innovation within the solvent borne coil coatings industry.

Solvent Borne Coil Coatings Market Share and Segmentation Insights: Steel Substrate Dominance and Direct Supply Chain Integration

By Substrate: Steel Leads with Construction and Appliance Industry Demand

The steel segment dominated the solvent borne coil coatings market with a 66.7% share in 2025, driven by its extensive use across construction, infrastructure, and home appliance applications. Pre-painted steel coils are widely utilized in building cladding, roofing systems, garage doors, HVAC units, and white goods, where durability, corrosion resistance, and aesthetic performance are essential. Solvent borne coatings such as polyester and PVDF coatings remain the industry standard for exterior applications due to their superior weatherability, UV resistance, and long-term performance. A key factor supporting this dominance is the widespread use of hot-dip galvanized (HDG) and Galvalume (aluminum-zinc coated) steel substrates, which require specially formulated solvent borne primers and topcoats for optimal adhesion and protection. This combination of high-performance coating systems and versatile steel substrates continues to reinforce steel’s leadership in the global solvent borne coil coatings market.

By Distribution Channel: Direct Sales Channel Leads with Integrated Production and Custom Formulation Control

The direct sales segment accounted for a leading 56.4% share of the solvent borne coil coatings market in 2025, reflecting the strong integration between steel producers, coil coaters, and coating manufacturers. Major steel companies such as ArcelorMittal, Nippon Steel, POSCO, and Baowu operate fully integrated coil coating lines, sourcing coatings directly from suppliers to enable just-in-time production and consistent product quality. This direct engagement supports the development of customized coating formulations, including specific colors, gloss levels, and performance properties required by architectural and appliance customers. Additionally, end users demand long-term warranties ranging from 20 to 40 years, particularly for PVDF-based coatings, necessitating full traceability, quality certification, and formulation control. Direct sales relationships ensure seamless coordination across the supply chain, enhancing efficiency and reliability. As demand grows for high-performance pre-painted metal coatings, the direct sales channel remains central to innovation and market expansion.

Competitive Landscape of the Solvent-Borne Coil Coatings Market

AkzoNobel Leads Market with Innovation Scale and Strategic Consolidation

AkzoNobel N.V. is the dominant force in the solvent-borne coil coatings market, leveraging its global R&D capabilities and strategic merger with Axalta. The combined entity is expected to generate $600 million in synergies, reinforcing its leadership in high-performance coil coatings. The company reported strong financial performance with a 14.2% EBITDA margin, supported by cost optimization initiatives. Its latest innovations include low-VOC solvent-borne systems with enhanced UV resistance and solar-reflective pigments, addressing urban heat island challenges.

PPG Drives Market with Digital Integration and High-Solids Industrial Coatings

PPG Industries, Inc. is a key player in the solvent-borne coil coatings market, leveraging its scale and digital capabilities. The company reported $3.93 billion in Q1 2026 net sales, with strong margins driven by industrial coatings demand. Its PPG LINQ™ platform enables AI-driven color matching, improving production efficiency and reducing tinting waste by up to 15%. PPG is focusing on high-solids solvent-borne coatings for HVAC and refrigeration systems, delivering superior corrosion resistance and durability.

Sherwin-Williams Expands Market Presence with PVDF Coil Coatings and Global Acquisitions

The Sherwin-Williams Company is strengthening its position in the solvent-borne coil coatings market through expansion and innovation. Its acquisition of a European coil coatings specialist enhances its manufacturing capabilities across key regions. The company’s Fluropon® PVDF coatings are widely used in commercial construction, offering advanced “cool roof” properties that meet evolving ESG standards. Sherwin-Williams’ strong distribution network enables rapid delivery of customized solutions for architectural and industrial applications.

Beckers Leads Sustainability with Renewable Coil Coatings and Advanced R&D Infrastructure

Beckers Group is a sustainability pioneer in the solvent-borne coil coatings market, particularly in Europe and Asia. Its new R&D center in Shanghai focuses on developing renewable chemical-based coatings, supporting the transition to low-carbon materials. Beckers’ FutureLab initiative has successfully piloted chromate-free and sustainable solvent-borne systems, while its recognition as a “Climate Leader” highlights its commitment to net-zero goals. The company dominates specialized segments such as vehicle and heavy machinery coatings, requiring high durability under extreme conditions.

Nippon Paint Drives APAC Growth with Advanced Resin Integration and Functional Coatings

Nippon Paint Holdings Co., Ltd. is a major player in the solvent-borne coil coatings market, particularly in Asia-Pacific. The company reported strong financial growth, with operating profit rising by over 38% in 2026. Its integration of specialty resin technologies enhances the performance of high-durability coil coatings for appliances and infrastructure. Nippon Paint has also developed antimicrobial and antiviral coil coatings using sol-gel hybrid technologies, targeting healthcare and food-processing industries.

Axalta Strengthens Market Position with High-Efficiency and Low-Energy Curing Technologies

Axalta Coating Systems is a key innovator in the solvent-borne coil coatings market, focusing on operational efficiency and high-performance solutions. The company achieved a 22.0% EBITDA margin, reflecting strong profitability and cost management. Its latest developments include low-temperature curing solvent-borne coatings, reducing energy consumption by up to 20% in coil coating lines. Axalta’s Alesta® and Nap-Gard® brands continue to set industry benchmarks, integrating infrared-reflective technologies to meet global sustainability targets.

China Driving High-Performance Fluoropolymer Coil Coatings for BIPV and Rail Infrastructure

China is aggressively advancing the solvent-borne coil coatings market, focusing on high-value applications such as Building-Integrated Photovoltaics (BIPV) and high-speed rail systems. The commercialization of nano-dispersed PVDF coatings with 30-year durability is significantly enhancing performance in coastal and solar applications.

Government mandates under the 14th Five-Year Plan for Building Energy Efficiency are accelerating the use of coil-coated aluminum and steel in public infrastructure. Technological innovations include anti-static topcoats for semiconductor clean-room panels, while large-scale investments in coil coating lines are supporting the production of cool-roof materials with high solar reflectance. Additionally, the use of fluorocarbon coatings in Maglev rail systems highlights China’s leadership in combining durability, UV resistance, and aerodynamic performance.

United States Strengthening Coil Coatings Demand Through Logistics Expansion and Fire-Safe Infrastructure

The United States is experiencing strong growth in the coil coatings market, driven by the rapid expansion of logistics infrastructure and pre-engineered buildings. The surge in warehouse construction is boosting demand for polyester and silicone-modified polyester coil coatings, which offer durability and weather resistance.

Technological advancements include the development of fire-retardant coil coating systems that meet stringent safety standards for insulated metal panels. Regulatory updates are promoting the use of closed-loop solvent recovery systems, enabling compliance with VOC regulations while maintaining high-performance solvent chemistry. Investments in domestic production are supporting applications such as EV battery enclosures and antimicrobial-coated panels for healthcare and food processing industries. Additionally, strong demand in the transportation sector, particularly for prepainted aluminum coils in truck and trailer manufacturing, is reinforcing the U.S. market’s growth trajectory.

Saudi Arabia Driving Demand for Heat-Resistant Coil Coatings in Mega Infrastructure Projects

Saudi Arabia is emerging as a major market for solvent-borne coil coatings, driven by large-scale infrastructure projects under Vision 2030. Developments such as NEOM’s “The Line” are generating significant demand for high-performance polysiloxane coatings capable of withstanding temperatures exceeding 80°C and resisting sand abrasion.

Technological innovations include the development of sand-resistant coil coatings, essential for maintaining structural integrity in desert environments. Government regulations, including climate-adaptive standards for roofing materials, are favoring high-durability fluoropolymer coatings. Large-scale infrastructure projects, such as airport expansions, are driving the use of coil-coated aluminum for roofing systems, while investments in local manufacturing are strengthening supply chain resilience and supporting long-term market growth.

India Emerging as a High-Growth Market for Coil Coatings in Housing and Cold Chain Infrastructure

India is witnessing rapid expansion in the solvent-borne coil coatings market, driven by urbanization, rural housing initiatives, and logistics infrastructure development. Government programs such as Pradhan Mantri Awas Yojana and the National Logistics Policy are significantly increasing demand for pre-painted galvanized steel (PPGI) used in roofing and cold-storage facilities.

Technological advancements include the development of cool-roof coil coatings with high solar reflectance (SRI > 85), helping reduce indoor temperatures in tropical climates. Investments in manufacturing capacity and R&D are supporting innovations such as bio-based solvent carriers and active-barrier anti-corrosive primers for coastal industries. Additionally, the adoption of coil-coated panels in railway projects, including Vande Bharat trains, highlights the growing importance of high-performance coatings in transportation infrastructure.

Japan Leading Nano-Functional Coil Coatings for Electronics and High-Precision Applications

Japan is a global leader in nano-functionalized solvent-borne coil coatings, particularly for electronics, appliances, and high-precision industries. Innovations such as nano-silica reinforced coatings are delivering superior fingerprint resistance and surface durability, making them ideal for premium consumer products.

Technological advancements include the development of ultra-thin coil films for 5G and 6G hardware shielding, enabling compact and high-performance electronic devices. Expansion in specialty material production is supporting the growth of advanced coating systems, while regulatory updates are ensuring higher standards for chemical safety and durability. Additionally, the introduction of photo-curable coil coatings is improving energy efficiency in manufacturing processes, reinforcing Japan’s leadership in sustainable and high-performance coating technologies.

Germany Advancing High-Solid Sustainable Coil Coatings with Digital Formulation Technologies

Germany continues to lead the European coil coatings market by integrating sustainability with high-performance solvent technologies. The development of ultra-high-solid (UHS) coil coatings with up to 85% solids content is significantly reducing VOC emissions while maintaining superior durability.

Government-supported research initiatives are driving the use of AI-based formulation tools to predict long-term performance and UV degradation, improving product reliability. Regulatory alignment with EU sustainability directives is promoting innovations such as bio-based solvent feedstocks and digital product passports for coated materials. Product advancements include multi-functional primers combining corrosion resistance and acoustic damping, particularly for urban construction applications. Germany’s strong presence in HVAC and industrial sectors further reinforces its leadership in advanced coil coating solutions.

Solvent-borne Coil Coatings Market Report Scope

Solvent-borne Coil Coatings Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$3 Billion

|

|

Market Size (2032)

|

$4.1 Billion

|

|

Market Growth Rate

|

4.4%

|

|

Segments

|

By Resin Type (Polyester, Siliconized Polyester, Fluoropolymers, Polyurethane, Plastisols, Epoxy, Acrylic), By Substrate (Steel, Aluminum, Other Metal Alloys), By Technology (Topcoats, Primers, Backing Coats, High-Solids Solvent-Borne), By End-User Industry (Building and Construction, Automotive and Transportation, Consumer Appliances, Industrial and Domestic Equipment, Packaging), By Distribution Channel (Direct Sales, Coil Coating Service Providers, Industrial Distributors)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Akzo Nobel N.V., PPG Industries, Inc., The Sherwin-Williams Company, Beckers Group, Axalta Coating Systems Ltd., Nippon Paint Holdings Co., Ltd., Kansai Paint Co., Ltd., Jotun Group, BASF SE, Hempel A/S, KCC Corporation, JSW Paints, Teknos Group, Henkel AG and Co. KGaA, Titan Coatings Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Solvent borne Coil Coatings Market Segmentation

By Resin Type

- Polyester

- Siliconized Polyester

- Fluoropolymers

- Polyurethane

- Plastisols

- Epoxy

- Acrylic

By Substrate

- Steel

- Aluminum

- Other Metal Alloys

By Technology

- Topcoats

- Primers

- Backing Coats

- High-Solids Solvent-Borne

By End-User Industry

- Building and Construction

- Automotive and Transportation

- Consumer Appliances

- Industrial and Domestic Equipment

- Packaging

By Distribution Channel

- Direct Sales

- Coil Coating Service Providers

- Industrial Distributors

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Solvent borne Coil Coatings Industry

- Akzo Nobel N.V.

- PPG Industries, Inc.

- The Sherwin-Williams Company

- Beckers Group

- Axalta Coating Systems Ltd.

- Nippon Paint Holdings Co., Ltd.

- Kansai Paint Co., Ltd.

- Jotun Group

- BASF SE

- Hempel A/S

- KCC Corporation

- JSW Paints

- Teknos Group

- Henkel AG & Co. KGaA

- Titan Coatings Inc.

*- List not Exhaustive