Southeast Asia Water Treatment Chemicals Market Value Analysis and Forecast

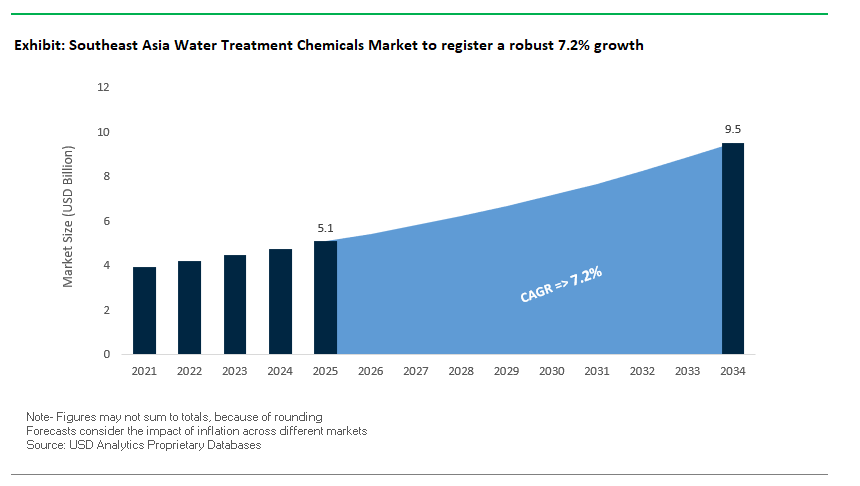

Southeast Asia Water Treatment Chemicals Market Size is estimated at $5.1 Billion in 2025 and is forecast to register an annual growth rate (CAGR) of 7.2% to reach $9.5 Billion by 2034.

The Southeast Asia (SEA) water treatment chemicals market is defined by the region’s tropical climate, monsoon variability, high organic loads, and growing industrialization factors that demand adaptable and cost-effective chemical treatment regimes. Municipal water systems frequently contend with raw water turbidity exceeding 500 NTU during the rainy season, addressed using polyaluminum chloride (PACl) with cationic starch, consistently achieving effluent clarity below 1 NTU in compliance with Vietnam’s TCVN 7221 standards.

Biofilm growth, accelerated by warm conditions and high nutrient loads, is mitigated by DBNPA dosed at 5–20 ppm; its <24-hour degradation profile ensures environmental compatibility, particularly under Thailand’s Pollution Control Department (PCD) regulations. In the industrial segment, palm oil mill effluent (POME) remains a key challenge anaerobic digestion systems coupled with ferric chloride scrubbing are employed to reduce hydrogen sulfide emissions by over 90%, adhering to Malaysian Palm Oil Board (MPOB) standards.

For textile effluents, Fenton’s reagent enables over 95% dye degradation at competitive operational costs as outlined in Indonesia’s Ministry of Environment Regulation 16/2023. The region’s push toward water reuse is evident in brackish water reverse osmosis (RO) systems, where antiscalants dosed at 3–8 ppm effectively manage silica concentrations above 180 ppm, per Singapore PUB’s Code of Practice.

Advanced direct potable reuse is gaining traction, particularly in the Philippines, where integrated MF/RO followed by UV/H₂O₂ advanced oxidation delivers potable-grade water, aligning with DENR Administrative Order 2016-08. As SEA economies urbanize and climate volatility intensifies, demand is rising for robust, scalable water treatment chemistries that blend local compliance, climatic resilience, and industrial specificity.

Market Trend: Rapid Industrialization Spurs Surge in Bio-Based and Smart Water Treatment Solutions Across Southeast Asia

The Southeast Asia water treatment chemicals market is witnessing a structural transformation fueled by accelerating industrial growth and tightening environmental standards. With 50% of the ASEAN population exposed to high water stress (World Bank, 2024), governments are enforcing strict water reuse and pollution control regulations. This has catalyzed the shift toward bio-based and non-toxic chemical solutions, particularly in textiles, municipal water, and manufacturing sectors. In Indonesia, BioFloc™ tamarind seed coagulants backed by Ministry of Environment subsidies have replaced aluminum sulfate in Jakarta’s plants, cutting sludge volumes by 30%. Meanwhile, Vietnam’s Green Chemistry Decree has banned phosphonate-based antiscalants, spurring uptake of lignin-derived formulations like BASF’s Sokalan® Bio. On the digital front, Singapore’s PUB Smart Plants are leveraging AI to optimize chloramine dosing at the Changi NEWater facility, achieving 20% chemical savings. As Thailand rolls out its 2024 Industrial Effluent Standards, and cassava-based flocculants gain momentum due to 40% lower OPEX vs. imports, sustainability and digital precision are becoming the twin pillars of chemical demand in Southeast Asia’s water market.

Market Opportunity: $500M+ Opportunity Emerges in Industrial Water Reuse and Circular Economy Applications

Southeast Asia is rapidly becoming a global hotspot for industrial water reuse, driven by green manufacturing mandates, international compliance standards, and rising pressure on freshwater resources. Electronics giants like Samsung are leading the charge: its Vietnam facilities operate PFAS-free UPW systems with <0.1 ppb TOC levels, meeting stringent semiconductor purity benchmarks. This trend is poised to unlock a $500M+ market by 2030, as chip fabs expand across Vietnam and Thailand. The textile and dyeing sector presents another major opportunity H&M’s supplier program in Cambodia uses enzyme-based decolorizers to achieve 80% water reuse, while Adidas’ Indonesian partners pay 15% price premiums for ZDHC-compliant green chemicals. In the resource sector, Freeport Indonesia’s tailings facilities have adopted chitosan coagulants to simultaneously recover copper and meet 0.2 mg/L heavy metal discharge limits, aligning with rising environmental scrutiny. With Malaysia’s MSPO 2025 standards mandating P-free antifoams in palm oil processing and the Philippines offering 50% tax incentives for bio-chemical adoption, the race is on to supply ESG-aligned, closed-loop chemical solutions. Add to this the monetization of carbon credits ($5–10/ton CO₂) from wastewater reuse, and it’s clear that first-mover suppliers are poised to dominate Southeast Asia’s water circularity boom.

Competitive Landscape: Southeast Asia Water Treatment Chemicals Market

The Southeast Asia water treatment chemicals market features a mix of players that includes multinational corporations, regional leaders, and many local formulators. Large companies such as Ecolab, Solenis, BASF, and Kemira hold about 40% of the market share. They use their global expertise in digital water technologies, sustainable chemistries, and integrated service models. These companies are particularly strong in export-driven sectors like pulp and paper, electronics, and pharmaceuticals.

Regional leaders, including Indonesia’s PT Lautan Luas, Vietnam’s Vinachem, and Thai Polychemicals, make up around 35% of the market. They focus on high-volume commodity chemicals and specific applications like palm oil wastewater and electrocoagulation. Local formulators, over 500 in total across the region, serve the remaining 25% of the market with cost-sensitive, lower-spec products aimed at domestic needs.

The market can be divided into four competitive groups. Global integrators like Ecolab and Solenis offer complete water management solutions. Commodity specialists like Vinachem and Thai Polychemicals operate at scale and maintain a cost advantage. Niche experts such as PT Lautan and Ion Exchange target specific sectors like mining and pharmaceuticals. Emerging tech disruptors, including WateROAM and Hydroflux, introduce portable and digital solutions for underserved or remote areas.

Ecolab leads the market with a 15% share thanks to its strong local presence through joint ventures, such as with Malaysia’s HUME Chemicals, and its solid digital infrastructure, including the 3D TRASAR platform. Solenis stands out in pulp and paper by providing high-performance polymers and specializes in palm oil wastewater. BASF sets itself apart with bio-based inhibitors designed for tropical climates and supports these efforts with an R&D center in Indonesia. Kemira, a leader in coagulation and flocculation, has tailored its offerings to ASEAN needs through a regional production center in Thailand and sourcing starch-based raw materials.

Regional players like PT Lautan are growing by acquiring local blenders, while Vinachem benefits from state support, which helps it stay competitive in government contracts. Ion Exchange is strengthening its presence in ASEAN by investing in infrastructure, including a manufacturing plant in Indonesia. Startups like WateROAM, which focuses on portable systems for disaster-prone areas, and Hydroflux, which aims to provide compact zero liquid discharge systems to SMEs, are also making progress through partnerships with NGOs and tech-transfer programs.

Competitive dynamics vary by country. In Indonesia, treating palm oil effluent is a major focus, where Solenis and PT Lautan are the leaders, but new regulations regarding biological oxygen demand are changing formulation strategies. In Vietnam, rising foreign investment in electronics is increasing the demand for high-purity water treatment, making BASF and Vinachem key players, although concerns about PFAS contamination are leading to changes in product formulations. In Thailand, Kemira and Thai Polychemicals are active in the tourism-driven market, especially as marine discharge rules become stricter. The Philippines, which faces frequent typhoons, is seeing more interest in decentralized mobile systems like those offered by WateROAM.

Regulatory conditions also influence strategy. Indonesia provides tax breaks for green chemistry, Vietnam encourages investment in special economic zones, and Thailand is advancing its Bio-Circular-Green economy framework. Looking ahead, localization and flexibility will be crucial. Companies are establishing regional formulation centers, such as BASF’s facility in Surabaya, localizing raw materials like Kemira’s starch inputs, and building extensive distributor networks, such as Ecolab’s network of over 200 partners.

Innovations tailored to local needs include tropicalized formulations with high-temperature stability, mobile dosing trucks for island regions, and easy-to-use systems for low-literacy environments. Future trends may see regional players gaining an estimated 15% more market share by 2030. Chinese firms may enter the market through Belt and Road Initiative projects, and digital water systems are likely to reach 25% penetration in industrial segments. To thrive, companies will need to personalize their products for different market segments, collaborate with ASEAN governments on regulatory matters, and adopt climate-resilient chemistries along with circular economy practices that use local agricultural waste in water treatment.

Southeast Asia Water Treatment Chemicals Market – Segmentation Insights (2025–2034)

By Type of Chemical: Coagulants Lead, Membrane Cleaners and Corrosion Inhibitors Accelerate

In Southeast Asia, coagulants and flocculants are expected to remain the dominant chemical category with a 2025 market share of around 29.6%, largely due to widespread use in treating high-turbidity surface water and industrial effluents. Nations like Indonesia, the Philippines, and Vietnam continue to rely heavily on coagulants such as alum, PAC, and polyDADMAC for sediment and organic load removal in both drinking water and wastewater streams. The increasing incidence of industrial runoff into rivers and aging municipal water systems further sustains demand for coagulation-based clarification.

However, membrane cleaning chemicals are projected to grow the fastest at a CAGR of 8.3%, driven by the rapid adoption of RO/NF technologies in water-scarce and high-tech regions like Singapore and Malaysia. Industrial zones and urban desalination plants are deploying membrane systems for both potable water and industrial reuse, necessitating chemical solutions for biofouling and scale control. Meanwhile, corrosion and scale inhibitors are gaining momentum (CAGR 11%) due to growing investment in offshore oil and gas, thermal power generation, and industrial cooling infrastructure along coastal areas. These inhibitors are crucial for protecting pipelines, boilers, and heat exchangers in humid and saline environments.

.png)

By Application: Industrial Sector Dominates, Municipal Demand Strengthens with Urbanization

The industrial segment is projected to dominate the Southeast Asia water treatment chemicals market with a 2025 share of approximately 49.2%, fueled by rising water usage in sectors such as electronics manufacturing in Vietnam, textile processing in Indonesia, and refining/petrochemicals in Thailand. These industries demand robust treatment programs for process water, boiler feedwater, and cooling circuits boosting the need for biocides, corrosion inhibitors, and pH stabilizers. Environmental compliance pressures and growing exports also push firms toward more advanced water management practices.

The municipal sector accounts for about 38.1% of the market, with consistent growth supported by urban expansion and government-backed water security initiatives. Projects like Metro Manila’s water infrastructure upgrades and smart city rollouts in Malaysia and Indonesia are increasing investments in disinfection, coagulation, and membrane treatment technologies. Additionally, the commercial segment, covering hospitality and healthcare, benefits from rising tourist footfall in Thailand, Bali, and the Philippines, driving demand for clean water and Legionella control chemicals across hotels and resort facilities.

Southeast Asia Water Treatment Chemicals Report Scope

Southeast Asia Water Treatment Chemicals Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$5.1 Billion

|

|

Market Size (2034)

|

$9.5 Billion

|

|

Market Growth Rate

|

7.2%

|

|

Segments

|

By Type of Chemical (Coagulants and Flocculants, Biocides and Disinfectants, Corrosion and Scale Inhibitors, pH Adjusters and Neutralizers, Membrane Cleaning Chemicals, Defoamers and Antifoaming Agents, Oxygen Scavengers, Other Specialty Chemicals), By Application (Industrial Water Treatment, Municipal Water Treatment, Commercial Water Treatment), By End-User Industry (Industrial, Municipal), By Form of Chemical (Liquid, Powder/Solid

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Ecolab Inc. (U.S.), Solenis LLC (U.S.), Kemira Oyj (Finland), SNF Floerger (France), BASF SE (Germany), Kurita Water Industries Ltd. (Japan), Veolia Water Technologies (France), SUEZ S.A. (France), The Dow Chemical Company (U.S.), Nouryon (The Netherlands), Buckman (U.S.), Ion Exchange (India)

|

|

Countries

|

Indonesia, Vietnam, Thailand, Malaysia, Singapore, Philippines

|

Southeast Asia Water Treatment Chemicals Market Segmentation

By Type of Chemical

- Coagulants and Flocculants

- Biocides and Disinfectants

- Corrosion and Scale Inhibitors

- pH Adjusters and Neutralizers

- Membrane Cleaning Chemicals

- Defoamers and Antifoaming Agents

- Oxygen Scavengers

- Other Specialty Chemicals

By Application

- Industrial Water Treatment

- Cooling Water Treatment

- Boiler Water Treatment

- Process Water Treatment

- Industrial Wastewater Treatment

- Water Reuse and Recycling

- Water Desalination

- Sludge Treatment

- Municipal Water Treatment

- Drinking Water Treatment

- Municipal Wastewater Treatment

- Commercial Water Treatment

By End-User Industry

- Industrial

- Power Generation

- Chemical and Petrochemical

- Food and Beverage

- Pulp and Paper

- Electronics and Semiconductors

- Textile and Dyeing

- Mining and Metallurgy

- Pharmaceutical

- Oil and Gas

- Other Manufacturing Industries

- Municipal

By Form of Chemical

By Country

- Indonesia

- Vietnam

- Thailand

- Malaysia

- Singapore

- Philippines

- Rest of Southeast Asia

Top Companies in Southeast Asia Water Treatment Chemicals Market

- Ecolab Inc. (U.S.)

- Solenis LLC (U.S.)

- Kemira Oyj (Finland)

- SNF Floerger (France)

- BASF SE (Germany)

- Kurita Water Industries Ltd. (Japan)

- Veolia Water Technologies (France)

- SUEZ S.A. (France)

- The Dow Chemical Company (U.S.)

- Nouryon (The Netherlands)

- Buckman (U.S.)

- Ion Exchange (India)

* List Not Exhaustive

Research Coverage

This USDAnalytics report provides an in-depth analysis of the Southeast Asia Water Treatment Chemicals Market, offering insights into market size, key growth drivers, emerging opportunities, and strategic developments across the ASEAN region. It covers a detailed breakdown of chemical categories, including coagulants and flocculants, corrosion and scale inhibitors, membrane cleaning agents, biocides, and specialty formulations designed for advanced water reuse and compliance with green manufacturing initiatives. The study emphasizes trends like bio-based formulations, AI-enabled dosing optimization, and sustainable chemistry adoption, all within the context of stringent regulatory environments, rapid industrialization, and climate-resilient water strategies.

Scope Includes:

- Segmentation

- By Type of Chemical: Coagulants & Flocculants, Biocides & Disinfectants, Corrosion & Scale Inhibitors, Membrane Cleaners, pH Adjusters, Oxygen Scavengers, Specialty Chemicals.

- By Application: Industrial Water Treatment (cooling, boiler, process, wastewater), Municipal Water Treatment (drinking, wastewater), and Commercial Water Treatment.

- By End-User: Power Generation, Petrochemical, Food & Beverage, Electronics, Textile & Dyeing, Pharmaceutical, Mining, and Others.

- By Form: Liquid and Powder/Solid.

- Geographic Coverage: Indonesia, Vietnam, Thailand, Malaysia, Singapore, Philippines, and Rest of Southeast Asia.

- Study Period: Historic data from 2021–2024 and forecast data from 2025–2034.

- Key Companies Covered: Ecolab Inc., Solenis LLC, Kemira Oyj, SNF Floerger, BASF SE, Kurita Water Industries, Veolia Water Technologies, SUEZ S.A., The Dow Chemical Company, Nouryon, Buckman, Ion Exchange.

Methodology

The research methodology combines primary and secondary data collection for accurate market insights:

- Primary Research: Interviews with water utility managers, industrial water specialists, chemical suppliers, and regulatory authorities across Southeast Asia.

- Secondary Research: Review of government regulations (e.g., DENR, PUB Singapore, Vietnam TCVN standards), trade journals, company reports, and technical publications.

- Market Size Estimation: A bottom-up approach based on chemical dosage norms, installed treatment capacities, and application-specific chemical intensity in municipal and industrial sectors.

- Forecasting Framework: Advanced time-series modeling integrating macroeconomic indicators, infrastructure investments, regulatory changes, and ESG compliance mandates.

- Validation: Triangulation with on-ground interviews and financial reports from leading players ensures reliability.

- Scenario Analysis: Evaluates high-growth opportunities in industrial water reuse, bio-based formulations, and AI-integrated dosing systems, factoring in regulatory tightening and digital adoption rates.

Deliverables

- Complete Market Research Report (PDF, Excel): data tables, market charts, and visual insights.

- Country-Level Forecasts & Analysis

- Segment-wise Revenue Projections (2025–2034)

- Competitive Benchmarking & SWOT Analysis

- Recent Developments & News Tracker

- Executive summary and key takeaway slides for boardroom presentations

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements