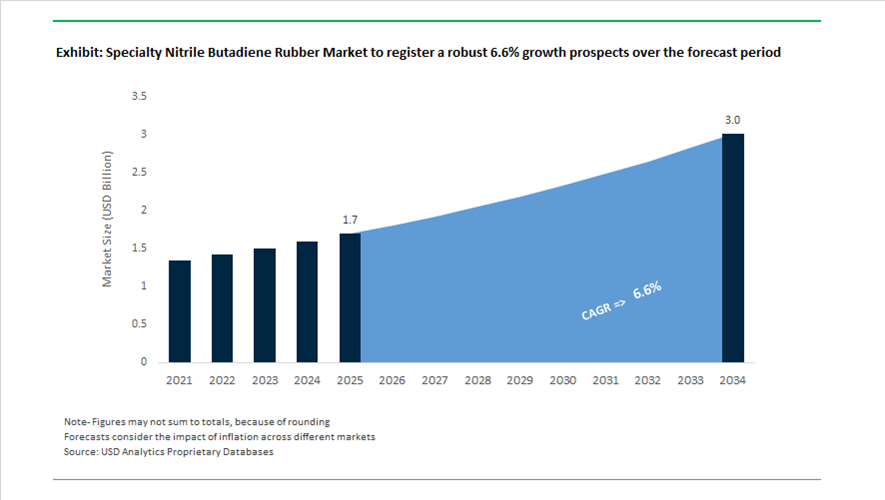

Specialty Nitrile Butadiene Rubber Market Valuation 2025–2034: $1.7 Billion to $3 Billion at 6.6% CAGR Driven by HNBR Expansion, Bio-Based Grades, and Industrial Elastomer Demand

The global specialty nitrile butadiene rubber (NBR) market is valued at $1.7 billion in 2025 and is projected to reach $3 billion by 2034, registering a CAGR of 6.6%. Growth is underpinned by rising demand for hydrogenated nitrile butadiene rubber (HNBR), high-acrylonitrile NBR, fast-cure elastomers, oil-resistant seals, industrial hoses, aerospace gaskets, and medical-grade nitrile latex. Specialty NBR grades are engineered for superior heat resistance, chemical stability, fuel compatibility, and low compression set, making them critical in automotive turbo systems, EV battery enclosures, oil and gas drilling components, aviation seals, and protective gloves. Asia-Pacific remains the primary production hub, supported by feedstock integration and expanding elastomer compounding infrastructure.

Capacity expansion accelerated in 2024. In March 2024, Arlanxeo announced plans to construct a 30,000-ton world-scale HNBR plant in China, targeting high-performance elastomer demand from automotive and energy sectors. In early 2024, Kumho Petrochemical confirmed a strategic NBR expansion in South Korea to strengthen supply to the global industrial and medical glove sectors. Throughout 2024, Sinopec’s Hainan Baling Chemical facility ramped up operations at its 170,000-ton synthetic rubber plant, supplying high-purity emulsion and solution polymerization grades. In 2024, Bridgestone and Kumho Petrochemical formalized a long-term supply agreement securing specialty NBR volumes for high-performance automotive and industrial applications. In October 2024, ADNOC finalized its $12.9 billion acquisition of Covestro, signaling vertical integration across petrochemical and specialty elastomer value chains.

Product innovation and regional footprint expansion intensified in 2025. In May 2025, Arlanxeo and TSRC inaugurated their expanded nitrile rubber joint venture facility in Nantong, Jiangsu, increasing capacity from 30 ktpa to 40 ktpa and introducing Perbunan® fast-cure grades to the Chinese market. These specialty grades are optimized for rapid processing, aviation components, and oil and gas sealing systems. In August 2025, Arlanxeo launched ISCC PLUS-certified bio-based Keltan® eco rubber grades in India, offering mass-balance-certified materials to automotive OEMs pursuing Scope 3 emission reductions. In March 2025, Synthomer reported a 9.2% EBITDA increase driven by operational restructuring, with notable recovery in nitrile latex demand for specialty health and protection products.

Sustainability and portfolio realignment are shaping 2026 supply dynamics. In February 2026, Punia Metox commenced production at its Tirupati facility using tire pyrolysis oil under an ISCC PLUS mass-balance approach to generate circular carbon materials for specialty rubber compounding. Zeon Corporation’s 2024–2025 portfolio restructuring emphasized concentration of elastomer production assets in high-efficiency hubs to enhance capital productivity in specialty rubber manufacturing. These expansions in HNBR capacity, fast-cure Perbunan grades, bio-based elastomers, circular feedstock integration, and long-term automotive supply contracts are reinforcing specialty nitrile butadiene rubber as a critical material platform for high-temperature, oil-resistant, and high-performance elastomer applications through 2034.

Key Trends and High-Impact Opportunities in the Specialty Nitrile Butadiene Rubber (NBR) Market

Automotive EV Thermal Management Accelerates Adoption of Dielectric-Ready HNBR and High-ACN NBR

The transition toward 800V electric vehicle architectures and ultra-fast charging systems has fundamentally altered elastomer performance requirements across powertrain and battery systems. Conventional NBR grades are increasingly unable to withstand prolonged exposure to elevated temperatures, aggressive dielectric coolants, and extended service intervals demanded by next-generation EV platforms. As a result, automotive OEMs and Tier-1 suppliers are rapidly shifting toward hydrogenated nitrile butadiene rubber (HNBR) and high-acrylonitrile NBR formulations that deliver superior heat resistance, chemical stability, and compression set retention.

This shift is directly reflected in strategic capacity expansions across the value chain. In January 2025, Zeon Corporation commissioned its expanded Zetpol HNBR production line in Pasadena, Texas, increasing global capacity by approximately 25%. The expansion was explicitly aligned with rising demand for EV battery coolant seals and high-temperature oil seals that must retain functional integrity for more than 15 years in operating environments exceeding 150°C. These materials are increasingly specified as standard rather than premium options in electric drivetrain architectures.

At the system level, water-glycol coolants continue to dominate EV thermal management, holding a 58.0% share as of late 2025 due to their superior heat transfer efficiency. However, glycol-induced elastomer degradation has emerged as a critical failure risk. To mitigate this, Tier-1 suppliers such as Dana Incorporated are mandating HNBR for critical sealing interfaces to ensure compliance with ISO 21448 Safety of the Intended Functionality requirements. This effectively locks specialty NBR grades into long-term platform specifications, creating durable demand visibility for high-performance elastomer suppliers.

HPHT and Sour Field Development Drives Non-Discretionary Demand for RGD-Resistant NBR

In the oil and gas sector, the maturation of conventional reserves has accelerated investment in high-pressure, high-temperature and sour field developments characterized by elevated hydrogen sulfide concentrations and extreme mechanical stress. These environments impose stringent requirements on elastomers, particularly resistance to rapid gas decompression, chemical attack, and abrasion. Specialty NBR and HNBR formulations have become indispensable in these applications, as failure can result in catastrophic downtime and safety risks.

At Rubber Tech China 2025, ARLANXEO highlighted its Therban HNBR portfolio designed for fully saturated polymer chains, which significantly improve resistance to rapid gas decompression. These materials are now widely adopted in blow-out preventers, packers, and drill-pipe protectors used in offshore and deepwater operations, where unplanned downtime can exceed one million dollars per day. This has shifted procurement decisions away from price-based selection toward performance-guaranteed elastomer systems.

Simultaneously, the growing use of synthetic-based drilling muds in regions such as the Permian Basin has increased chemical exposure for downhole components. These muds contain aromatic hydrocarbons that accelerate swelling and wear in standard elastomers. As a result, oilfield service providers are increasingly deploying carboxylated NBR (XNBR) in stator and rotor applications. Internal industry assessments in 2025 indicate a more than 35% increase in XNBR usage due to its superior abrasion resistance and dimensional stability under chemically aggressive conditions.

High-Barrier NBR Tie-Layers Enable Growth in Modified Atmosphere Packaging

The global shift toward preservative-free food systems and extended cold-chain logistics has accelerated adoption of Modified Atmosphere Packaging across fresh protein, dairy, and pharmaceutical segments. This trend is opening a high-margin niche for specialty NBR grades engineered as ultra-low moisture vapor and gas barrier tie-layers within multilayer packaging structures.

Industry case studies conducted during 2024 and 2025 demonstrate that incorporating NBR-based tie-layers into co-extruded films can extend product shelf life by up to 40% by maintaining precise nitrogen and carbon dioxide ratios. Unlike traditional polyolefin-based barriers, specialty NBR offers superior resistance to oils and fats while delivering low gas permeability, making it particularly suitable for high-value, lipid-rich food products and active pharmaceutical packaging.

Regulatory alignment has further strengthened this opportunity. In 2025, ARLANXEO introduced clean-grade Perbunan NBR formulations compliant with FDA 21 CFR Part 177 and EU Regulation 1935/2004. These approvals have enabled direct adoption of NBR in one-way valves, flexible pouches, and active packaging components that require both stringent food-contact compliance and robust barrier performance, positioning specialty NBR as a functional enabler rather than a commodity polymer.

ESD-Controlled NBR Becomes Essential for Sub-3nm Semiconductor Cleanrooms

The global acceleration of semiconductor fabrication capacity under various Chips Act initiatives has triggered a surge in ISO Class 1 to 5 cleanroom construction. These advanced fabs demand elastomeric components that are not only chemically clean but also inherently static-dissipative to protect ultra-sensitive wafers from electrostatic discharge. Specialty NBR formulations engineered for ESD control are emerging as a critical material choice in this environment.

Government-led programs such as the India Semiconductor Mission, which outlined a ₹76,000 crore investment framework at SEMICON India 2025, are driving localized production of cleanroom consumables. Specialty NBR producers are responding with conductive and static-dissipative NBR roll covers, seals, and wiper blades designed to meet ANSI/ESD S20.20 standards. These materials prevent static buildup that can attract nanometer-scale particles and compromise yield in angstrom-era lithography processes.

In parallel, cleanroom operators are tightening requirements around outgassing and particle shedding. New NBR formulations introduced in late 2025 focus on minimizing total mass loss and collected volatile condensable materials to comply with ISO 14644 particle limits. Leading equipment suppliers are increasingly specifying these low-outgassing NBR grades for seals and interfaces used in sub-3nm fabrication, reinforcing specialty NBR’s role as a strategic material in next-generation semiconductor manufacturing infrastructure.

Specialty Nitrile Butadiene Rubber Market Share and Segmentation Insights

High-Acrylonitrile NBR Leads the Specialty Nitrile Butadiene Rubber Market for Fuel and Chemical Resistance

High-acrylonitrile nitrile butadiene rubber accounted for 28.40% of the specialty nitrile butadiene rubber market in 2025, reflecting its strong performance in demanding industrial and automotive environments. With acrylonitrile content typically ranging from 39% to 50%, this grade offers superior oil, fuel, and chemical resistance, making it widely used in automotive fuel systems, oilfield equipment, and industrial sealing components. The higher nitrile content improves barrier properties and mechanical strength, enabling reliable performance under exposure to hydrocarbon fluids. A key 2025 market driver is the growing use of biofuel-blended fuels, where high-acrylonitrile NBR provides enhanced resistance to ethanol-blended gasoline and biodiesel, helping maintain seal integrity and prevent material swelling in modern vehicle fuel systems.

Seals, Gaskets and O-Rings Drive Demand for Specialty Nitrile Butadiene Rubber

Seals, gaskets, and O-rings represent the largest application segment in the specialty nitrile butadiene rubber market, accounting for 32.80% of total demand in 2025 due to the material’s excellent resistance to oils, fuels, and industrial fluids. NBR’s combination of mechanical durability, compression set resistance, and chemical compatibility makes it a preferred material for sealing applications in automotive engines, transmissions, hydraulic systems, and industrial machinery. The reliability of these components is essential for preventing leaks and maintaining system performance. A significant 2025 trend is the increasing demand for high-performance sealing materials, particularly hydrogenated nitrile butadiene rubber (HNBR) grades that offer improved heat resistance, oxidation stability, and long-term durability for equipment operating under higher temperatures and pressures.

Specialty Nitrile Butadiene Rubber Market Competitive Landscape

The global specialty nitrile butadiene rubber market in 2026 is defined by the shift toward high-performance HNBR and XNBR grades for EV batteries, oilfield seals, and extreme environments. Leading players are scaling capacity, integrating low-carbon production, and advancing conductive and high-purity elastomers for next-generation industrial applications.

ARLANXEO Scales Therban® HNBR Capacity in China to Capture EV Battery Binder and High-Performance Sealing Demand

ARLANXEO is reinforcing its leadership in specialty nitrile butadiene rubber through the expansion of Therban® HNBR production in Changzhou, China, with a total capacity of 5,000 tons per year. The first 2,500-ton phase became operational in late 2025, targeting the high-growth Asia-Pacific EV market. The facility integrates advanced thermal oxidation systems, reducing carbon emissions by approximately 80% compared to conventional processes. ARLANXEO is positioning HNBR as a critical cathode binder for lithium-ion batteries, ensuring stability under high-voltage conditions. Its co-located EPDM plant and Regional Technology Center enable a closed-loop innovation ecosystem. This integration enhances product development speed and application-specific customization for high-performance elastomers.

Zeon Advances Ultra-Low Temperature HNBR and Conductive Elastomers Through STAGE30 Specialty Focus Strategy

Zeon Corporation continues to lead in HNBR technology with its Zetpol® product line, widely used in automotive timing belts and oil-resistant seals. Under its STAGE30 Phase 3 strategy, the company is reallocating capital toward specialty elastomers and battery materials. Recent R&D focuses on ultra-low temperature HNBR grades capable of maintaining elasticity at -40°C, addressing extreme climate applications. Zeon is integrating NBR with single-walled carbon nanotubes to develop conductive elastomers for sensors and advanced battery systems. Operational restructuring at its Tokuyama plant aims to reduce product development timelines by 20% by 2027. This specialization strengthens its position in high-performance and electronics-integrated elastomer markets.

Kumho Petrochemical Expands High-Value NBR Portfolio with EV-Specific Elastomers and 92,000 MT Capacity Scale

Kumho Petrochemical is transitioning toward high-value specialty NBR products, supported by a production capacity of 92,000 MT per year and a leading nitrile latex capacity of 946,000 MT. The company is focusing on EV-specific elastomers designed for enhanced chemical resistance in coolant systems and improved rolling resistance in tires. Strategic investments through Kumho Mitsui Chemicals are expanding MDI capacity by 100,000 tons, enabling integrated polyurethane and elastomer solutions. Kumho’s dominance in nitrile latex supports over 30% of the global glove market, reinforcing its scale advantage. Advanced emulsion polymerization ensures cost efficiency and consistent product quality. Its shift toward specialty elastomers aligns with evolving automotive and industrial performance requirements.

LG Chem Strengthens Low-Carbon Nitrile Latex Leadership with LETZero Platform and Semiconductor-Grade Elastomer Applications

LG Chem is advancing its specialty NBR portfolio through organizational restructuring and sustainability-driven innovation. Its nitrile latex business now operates under the High Performance Materials division, aligning with its global leadership in glove materials. The company maintains large-scale production capacities in South Korea and China, exceeding 490,000 tons combined. Its LETZero platform focuses on bio-balanced, low-carbon nitrile latex production to meet ESG mandates. Specialty NBR grades are increasingly used in semiconductor cleanroom gloves and high-purity engineering applications. Recent innovations include high-nitrile content rubbers with superior permeation resistance for aerospace and SAF compatibility. This positions LG Chem at the intersection of sustainability and advanced material performance.

Synthos Accelerates Functionalized NBR Innovation with European Production Optimization and Bio-Based Feedstock Development

Synthos is strengthening its specialty rubber portfolio through strategic optimization of its Schkopau plant in Germany, focusing on high-margin functionalized NBR and SBR products. The company anticipates EBITDA recovery in 2026 driven by increased demand from European automotive OEMs. Its acquisition of Trinseo’s synthetic rubber business has expanded its capabilities in specialty elastomers. Synthos is gaining recognition for sustainability innovation, including its inclusion in the UN Global Compact Yearbook 2025. The company is piloting bio-based butadiene feedstocks to develop carbon-neutral specialty NBR grades by 2027. Its focus on circular economy technologies and low-emission production enhances competitiveness in the evolving elastomer market.

China Specialty Nitrile Butadiene Rubber Market Accelerated by HNBR Scale-Up and EV Localization

China has emerged as the most dynamic capacity expansion hub for specialty nitrile butadiene rubber, driven by hydrogenated grades and environmental compliance. In March 2024, ARLANXEO announced the construction of a world-scale HNBR facility in Changzhou under its Therban brand, with commercial operations scheduled for Q3 2025. Although the initial 2,500 tons per annum phase appears modest, the strategic intent lies in establishing localized HNBR supply for high-temperature, oil-resistant applications in automotive powertrains and industrial machinery. This investment directly addresses Asia’s long-standing dependence on imported hydrogenated elastomers.

Environmental regulation has also reshaped China’s NBR manufacturing footprint. In May 2025, the ARLANXEO–TSRC joint venture inaugurated its relocated NBR plant in Nantong, expanding nameplate capacity to 40,000 tons per year. The new site is fully aligned with Yangtze River environmental controls and produces Perbunan and Krynac grades designed for low-emission processing. At the application level, Chinese producers are increasingly developing electronic-grade NBR for new energy vehicles, particularly for cell-to-pack battery gaskets and coolant sealing systems. Implementation of the GB 4806.16-2025 national safety standard has further forced upgrades toward high-purity NBR with reduced extractables, opening premium segments in food-contact and pharmaceutical elastomers.

United States Specialty Nitrile Butadiene Rubber Market Defined by Supply Assurance and Advanced Mobility

The United States specialty NBR market is shaped by supply security concerns, hydrogenated elastomer shortages, and advanced mobility requirements. Zeon Chemicals, a subsidiary of Zeon Corporation, is executing a 25% capacity expansion at its Pasadena, Texas HNBR facility, with completion expected by late 2025. This expansion targets critical demand from automotive OEMs and oilfield service providers that require elastomers capable of sustained operation under extreme heat and aggressive chemical exposure.

Feedstock volatility has reinforced long-term contracting behavior. During Q2 2025, scheduled maintenance at domestic acrylonitrile and butadiene units drove NBR prices sharply higher, prompting OEMs to shift toward multi-year supply assurance agreements with specialty rubber suppliers. Policy-driven reshoring is also evident in medical applications. Post-pandemic healthcare reviews have incentivized domestic NBR latex production for surgical gloves, reducing reliance on Southeast Asian imports. In parallel, Lubrizol and Zeon published data in late 2025 confirming the compatibility of advanced NBR grades with dielectric fluids used in immersion-cooled EV battery systems, positioning U.S. elastomer suppliers at the forefront of next-generation electric mobility materials.

South Korea Specialty Nitrile Butadiene Rubber Market Supported by Industrial Policy and Electronics Integration

South Korea’s specialty NBR industry is closely integrated with national industrial policy and the country’s electronics export ecosystem. In December 2024, the government launched a combined W50 billion High-Value Specialty Fund and a W1 trillion petrochemical restructuring fund administered by the Korea Development Bank. These mechanisms are explicitly designed to shift producers such as Kumho Petrochemical away from commoditized rubbers toward high-margin specialty elastomers, including advanced NBR and HNBR grades.

Export orientation remains a defining feature. With electronics exports exceeding $200 billion, Korean manufacturers are developing ultra-thin NBR gaskets and vibration-damping components for next-generation smart devices and precision electronics. Technology partnerships are reinforcing this trajectory. LG Chem and Synthos operationalized a joint venture during 2024–2025 focused on high-performance NBR for industrial hoses, leveraging proprietary polymerization know-how. Sustainability considerations are increasingly embedded, as Yeosu-based facilities integrated recycling and energy-efficiency upgrades in 2025 to lower greenhouse gas intensity per ton of specialty elastomer produced.

Japan Specialty Nitrile Butadiene Rubber Market Anchored by Precision Engineering and Medical Applications

Japan’s specialty NBR market remains centered on precision engineering, heat resistance, and medical-grade purity. In late 2024, Zeon Corporation introduced a new high-performance NBR grade capable of maintaining chemical stability above 150°C, addressing the needs of downsized turbocharged engines and high-load industrial sealing systems. Such innovations reflect Japan’s emphasis on performance differentiation rather than volume expansion.

Advanced synthesis techniques further distinguish Japanese output. Producers are utilizing high-purity rare gases in specialized NBR and NBR/PVC blends to improve ozone and weather resistance, critical for outdoor power equipment and infrastructure components. Demographic pressures are also influencing demand. Japan’s aging population has driven increased R&D investment into nitrile-based medical tubing, stoppers, and closures. JSR Corporation is focusing on low-protein-binding NBR grades to meet stringent biocompatibility requirements in injectable and implantable medical devices.

India Specialty Nitrile Butadiene Rubber Market Protected by Trade Policy and Bio-Based Innovation

India’s specialty NBR market is transitioning under the dual influence of trade protection and sustainability policy. In October 2024, the Directorate General of Trade Remedies initiated an anti-dumping investigation into NBR imports from multiple regions, aiming to protect domestic producers such as Apcotex Industries. This action has improved pricing visibility for local manufacturers and encouraged incremental capacity utilization in specialty grades.

Longer-term differentiation is emerging through bio-based pathways. The BioE3 Policy introduced in August 2024 provides capital subsidies for bio-foundries, enabling R&D into bio-butadiene and renewable intermediates for nitrile rubber synthesis. Beyond automotive and industrial uses, India’s rapid solar infrastructure build-out has created new demand for durable NBR seals in high-exposure tracking systems, where resistance to heat, UV radiation, and mechanical fatigue is critical. These applications are expanding the addressable market for specialty NBR beyond traditional automotive and glove segments.

Comparative Snapshot: Specialty Nitrile Butadiene Rubber Industry by Country

Specialty Nitrile Butadiene Rubber Market County Level Snapshot

|

Country

|

Strategic Focus

|

Key Drivers

|

Market Positioning

|

|

China

|

HNBR capacity and EV localization

|

Environmental relocation, NEV demand

|

Scale with rising specialty depth

|

|

United States

|

Supply assurance and advanced mobility

|

HNBR shortages, EV cooling systems

|

High-margin, technology-led

|

|

South Korea

|

Electronics-driven specialization

|

Government funds, JV technology

|

Export-oriented precision

|

|

Japan

|

Heat resistance and medical purity

|

Precision synthesis, aging population

|

Performance differentiation

|

|

India

|

Trade protection and bio-based R&D

|

Anti-dumping, BioE3 policy

|

Emerging specialty supplier

|

Specialty Nitrile Butadiene Rubber Market Report Scope

Specialty Nitrile Butadiene Rubber Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1.7 Billion

|

|

Market Size (2034)

|

$3 Billion

|

|

Market Growth Rate

|

6.6%

|

|

Segments

|

By Product Grade (Standard Nitrile Butadiene Rubber, High-Acrylonitrile Nitrile Butadiene Rubber, Low-Acrylonitrile Nitrile Butadiene Rubber, Hydrogenated Nitrile Butadiene Rubber, Carboxylated Nitrile Butadiene Rubber, Nitrile Butadiene Rubber PVC Blends, Nitrile Butadiene Rubber Latex), By Application (Hoses, Belts and Cables, Seals, Gaskets and O-Rings, Medical and Industrial Gloves, Adhesives and Sealants, Molded and Extruded Parts, PVC Modification, Footwear and Consumer Goods)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Zeon Corporation, ARLANXEO, Kumho Petrochemical Co., Ltd., LG Chem Ltd., JSR Corporation, Sibur, Synthos S.A., Nantong Jiangshan Chemical, Apcotex Industries Limited, TSRC Corporation, Sinopec, Versalis S.p.A., Dynasol Group, PetroChina Company Limited, Emerald Performance Materials

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Specialty Nitrile Butadiene Rubber Market Segmentation

By Product Grade

- Standard Nitrile Butadiene Rubber

- High-Acrylonitrile Nitrile Butadiene Rubber

- Low-Acrylonitrile Nitrile Butadiene Rubber

- Hydrogenated Nitrile Butadiene Rubber

- Carboxylated Nitrile Butadiene Rubber

- Nitrile Butadiene Rubber PVC Blends

- Nitrile Butadiene Rubber Latex

By Application

- Hoses, Belts and Cables

- Seals, Gaskets and O-Rings

- Medical and Industrial Gloves

- Adhesives and Sealants

- Molded and Extruded Parts

- PVC Modification

- Footwear and Consumer Goods

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Specialty Nitrile Butadiene Rubber Industry

- Zeon Corporation

- ARLANXEO

- Kumho Petrochemical Co., Ltd.

- LG Chem Ltd.

- JSR Corporation

- Sibur

- Synthos S.A.

- Nantong Jiangshan Chemical

- Apcotex Industries Limited

- TSRC Corporation

- Sinopec

- Versalis S.p.A.

- Dynasol Group

- PetroChina Company Limited

- Emerald Performance Materials

*- List not Exhaustive