Spirotetramat Packaging Market Size, Overview, and Growth Outlook (2025–2034)

Spirotetramat Packaging Market Projected to Reach $354.3 Million by 2034 Amid Growing Adoption of Precision Agriculture

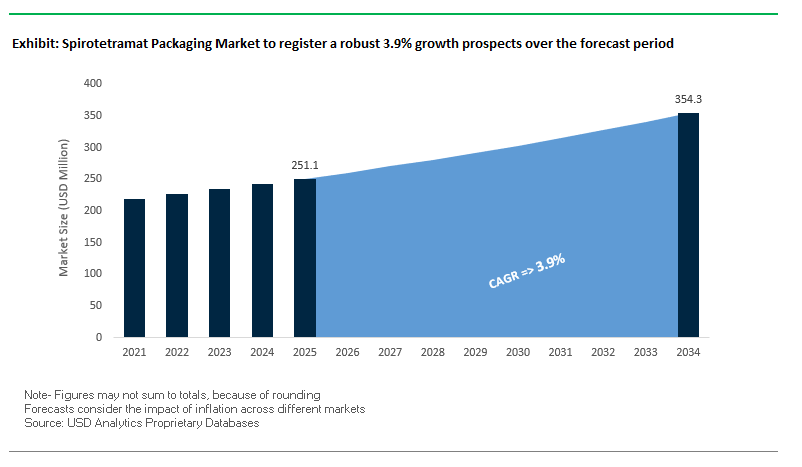

The global spirotetramat packaging market is estimated at $251.1 million in 2025 and is expected to reach $354.3 million by 2034, growing at a CAGR of 3.9%. This specialized sector focuses on packaging for spirotetramat-based systemic insecticides, essential for effective pest control in modern agriculture. Packaging ensures product stability, safety, and precision in application, which are critical for maximizing agricultural output while minimizing environmental impact.

Key Insights for Industry Professionals:

- Integrated Pest Management (IPM) adoption drives demand for spirotetramat packaging due to its safe mode of action for beneficial insects.

- Advanced liquid formulations (OD, SC) require durable packaging with secure seals and controlled dispensing mechanisms.

- Tamper-evident and secure closures are increasingly vital to prevent counterfeiting and ensure product integrity.

- Sustainable packaging trends: Bio-based polymers and recyclable materials are gaining traction amid rising environmental regulations.

- Market innovation focus: Packaging solutions are aligning with new application technologies and concentrated formulations to meet farmer and regulatory needs.

Market Analysis: Strategic Innovations and Sustainable Packaging Trends Are Reshaping the Spirotetramat Industry

The spirotetramat packaging market is undergoing dynamic changes driven by sustainability initiatives and application technology advancements. In September 2025, Bayer CropScience showcased innovations in its Movento insecticide portfolio, emphasizing safe and efficient systemic insecticide application. August 2025 saw a U.S. university study highlight the effectiveness of controlled-release formulations, prompting packaging designs that prolong product efficacy.

The trend toward eco-friendly materials is gaining momentum. In May 2025, an academic review focused on “green” polymers for agricultural use, influencing packaging materials for spirotetramat. User experience remains crucial: In February 2025, feedback from Indian retailers highlighted the importance of ergonomic and easy-to-open caps, ensuring farmers can apply products efficiently without spillage.

Regulatory compliance continues to drive demand. September 2024 saw spirotetramat included on the approved list for use in Great Britain, reinforcing the need for compliant and region-specific packaging. Meanwhile, companies are offering customized solutions, as exemplified by Nanjing Essence Fine-Chemical in December 2024, reflecting a shift toward tailored packaging for specific crops and regional markets.

Trends and Opportunities Transforming the Spirotetramat Packaging Market

Strategic Down-gauging and Lightweighting of HDPE Containers

One of the most prominent trends in the Spirotetramat packaging market is the widespread adoption of lightweighting strategies for HDPE containers. Agrochemical manufacturers and packaging suppliers are leveraging advanced extrusion blow-molding processes to achieve up to 15% resin reduction per container without compromising chemical resistance or mechanical strength. This development is being driven by dual motivations: lowering production costs and achieving sustainability targets outlined in corporate ESG frameworks. For example, lightweight HDPE containers reduce overall resin consumption, translating directly into cost savings, while also cutting greenhouse gas emissions associated with resin manufacturing and downstream logistics. Furthermore, a lighter container footprint reduces fuel consumption in transportation, allowing agrochemical companies to demonstrate measurable progress toward their plastic reduction and carbon neutrality goals. This trend is shaping procurement decisions as agricultural distributors increasingly prioritize suppliers that can provide environmentally responsible yet durable container solutions.

Adoption of Integrated RFID Tagging for Supply Chain Security

Another major trend reshaping the market is the use of RFID-enabled Spirotetramat packaging to combat counterfeiting and strengthen supply chain visibility. Counterfeit agrochemicals represent a significant risk to farmers, undermining crop yields and potentially violating regulatory safety requirements. To address this, agrochemical packaging suppliers are embedding RFID tags directly into HDPE containers, allowing every unit to carry a unique digital identity. This track-and-trace system provides authentication from production to end-user, creating an effective safeguard against illicit trade. Beyond anti-counterfeiting, RFID technology offers enhanced operational efficiencies, including real-time visibility into inventory levels and automated reconciliation at distribution points. Compared to traditional barcodes, RFID enables container-level accuracy without line-of-sight scanning, reducing labor time while ensuring that inventory movements are tracked with higher precision. The integration of RFID into agrochemical packaging is expected to expand rapidly as governments tighten regulations on crop protection products and companies seek to build trust with farmers through secure and transparent distribution channels.

Development of “Recyclable-by-Design” HDPE Containers with Barrier Layers

A major innovation opportunity lies in addressing the recyclability challenges of multi-layer agrochemical packaging. Many Spirotetramat containers incorporate barrier layers, such as EVOH, to prevent chemical permeation and maintain product integrity. However, these materials are incompatible with the HDPE recycling stream and are identified by the Association of Plastic Recyclers (APR) as contaminants, significantly reducing the recyclability and market value of used containers. This challenge is opening the door for “recyclable-by-design” solutions that employ compatible barrier technologies. Emerging co-extrusion methods and novel tie-layer adhesives are being engineered to bond barrier materials with HDPE while remaining fully recyclable within existing infrastructures. The development of such barrier systems not only ensures compliance with increasingly strict recycling regulations but also enhances circularity by allowing used agrochemical containers to be collected, processed, and reintroduced as high-quality post-consumer recycled (PCR) content. For packaging suppliers, this represents a critical innovation pathway to align with sustainability demands while safeguarding product performance.

Implementation of Returnable and Reusable Container Systems

The second opportunity lies in scaling closed-loop, reusable packaging systems for Spirotetramat and other agrochemicals. Major agrochemical companies, including Syngenta and BASF, are investing in deposit-return models where bulk containers are returned, inspected, cleaned, and refilled under strict quality control. These systems address both waste reduction and on-farm safety concerns, providing farmers with a reliable means of handling empty containers without contributing to landfill or incineration. By reusing bulk totes, companies significantly cut down on plastic waste while also lowering lifecycle emissions associated with container production. From a customer relationship standpoint, these programs offer added value through reduced disposal costs and assurance of container safety, fostering loyalty among distributors and end-users. As regulators increasingly favor extended producer responsibility (EPR) frameworks, returnable and reusable container programs are expected to gain further traction, positioning them as a cornerstone of sustainable packaging strategies in the agrochemical industry.

Competitive Landscape: Leading Agrochemical Companies Are Innovating Packaging Solutions to Enhance Spirotetramat Efficiency and Safety

The global spirotetramat packaging market is shaped by key players in agrochemicals who leverage formulation expertise, packaging innovation, and global distribution to provide secure, durable, and user-friendly solutions.

Bayer AG (Bayer CropScience): Driving Sustainable and User-Friendly Packaging for Movento

Bayer CropScience leads with its flagship Movento spirotetramat product, offering durable, ergonomically designed bottles with secure dosing mechanisms. The company emphasizes two-way systemic action on packaging to highlight efficacy against hidden pests. Bayer’s focus on sustainable farming initiatives ensures environmentally friendly packaging aligned with global regulatory standards. Its extensive R&D capabilities and global distribution network strengthen its leadership in agrochemical packaging.

Syngenta AG: Integrating Sustainable Packaging Across a Comprehensive Pest Management Portfolio

Syngenta provides secure and easy-to-handle packaging for its spirotetramat products as part of a broader crop protection strategy. Through its Good Growth Plan, the company emphasizes recyclable materials and reduced plastic usage, reflecting sustainability trends. Syngenta’s strong R&D pipeline, global farmer relationships, and integrated solutions position it as a key driver in sustainable packaging innovation.

ADAMA Agricultural Solutions Ltd.: Combining Durability and Cost-Effectiveness for Off-Patent and Proprietary Formulations

ADAMA focuses on packaging solutions for liquid and granular formulations, ensuring durability, safety, and cost-efficiency. Its strategic expansions and tailored regional solutions enable rapid market adaptation. The company’s ability to bring new products to market efficiently and provide versatile packaging options underscores its focus on practical and scalable solutions for global farmers.

Nanjing Essence Fine-Chemical Co., Ltd.: Customizing Packaging Solutions for Global Agrochemical Clients

Nanjing Essence Fine-Chemical offers customized packaging for OD and SC spirotetramat formulations, ranging from 10 mL to 200 L. Its focus on secure transport, product stability, and tailored solutions positions it as a key supplier for international clients. The company is expanding global presence and manufacturing capabilities to meet growing demand, emphasizing flexibility and quality in packaging design.

Spirotetramat Packaging Market Share Insights, 2025-2034

Bottles & Cans Lead Market Share by Product Type in Spirotetramat Packaging

Bottles and cans represent 40% of the spirotetramat packaging market, positioning them as the primary format for agrochemical formulators and distributors. HDPE bottles and cans offer excellent chemical resistance, durability, and cost-effectiveness, making them the preferred choice for concentrated formulations that require safe storage and transport before dilution in the field. Their mid-range capacity also aligns with the operational needs of agricultural distributors and farm cooperatives, providing manageable units that reduce handling risks. The adoption of standardized bottle and can formats across regions also streamlines logistics and regulatory compliance, reinforcing their position as the cornerstone of this specialized packaging sector.

Agriculture Dominates Market Share by End-Use Industry in Spirotetramat Packaging

Agriculture commands an overwhelming 95% of the spirotetramat packaging market, underscoring the sector’s dependence on this insecticide for crop protection. Packaging solutions in agriculture prioritize safety, durability, and scalability, with HDPE bottles, foil pouches, and bulk drums serving the needs of farms ranging from smallholdings to industrial-scale operations. The dominance of this segment reflects the widespread registration and approval of spirotetramat for fruits, vegetables, and nuts, where sucking pests can devastate yields. Packaging formats are tailored to farming distribution models, enabling efficient bulk transport and safe on-site application. With public health and hygiene applications limited to niche programs, agriculture will continue to dictate both volume and innovation in spirotetramat packaging.

United States: EPA Regulations and Child-Resistant Agrochemical Packaging

The United States spirotetramat packaging market is strongly shaped by regulatory oversight from the U.S. Environmental Protection Agency (EPA), which frequently updates pesticide tolerance levels through federal register notices. These changes directly influence labeling requirements and safety standards for spirotetramat-based products. Manufacturers are increasingly required to adopt clear, compliant labeling and safety data sheets (SDS) that align with EPA guidance, ensuring farmers and distributors are fully informed about handling practices.

In addition to compliance, the U.S. market emphasizes safety and durability in agrochemical packaging. Companies are investing in child-resistant closures and tamper-proof containers to prevent accidental spills and poisoning, particularly in domestic and small-scale farming contexts. Key industry players like Bayer CropScience, with its Movento brand, are leading innovation in container design, using durable plastics and multilayer packaging that meet both safety and sustainability standards. These advancements highlight the balance between stringent safety mandates and sustainability-driven innovation in the U.S. agrochemical sector.

European Union: PPWR and Stricter Hazardous Packaging Standards

The European Union spirotetramat packaging market is undergoing structural change under the Packaging and Packaging Waste Regulation (PPWR), enforced since February 2025. This regulation requires agrochemical packaging to include minimum percentages of recycled content by 2030, compelling manufacturers to re-engineer plastic bottles, containers, and bulk drums. At the same time, the Ecodesign for Sustainable Products Regulation (ESPR) introduces Digital Product Passports, ensuring transparency on material composition, recyclability, and compliance.

Another crucial driver is the EU’s ban on per- and polyfluoroalkyl substances (PFAS) in food-contact packaging effective August 2026, which indirectly impacts agrochemical packaging by stimulating innovation in barrier coatings and advanced resins. Regulatory bodies are also tightening rules on hazardous waste handling and disposal, pushing companies to adopt robust, puncture-resistant, and recyclable container formats. Mergers and partnerships within the European packaging industry are accelerating investment in circular economy solutions tailored to agrochemical packaging.

China: Traceability and Advanced Agrochemical Packaging Solutions

The China spirotetramat packaging market is being driven by a dual focus on plastic pollution control and anti-counterfeiting measures. Under the “14th Five-Year” plan, strict environmental regulations came into effect on June 1, 2025, mandating companies across logistics and agriculture to adopt eco-friendly and reusable packaging systems. This regulatory push is transforming the supply chain for large-volume agrochemical packaging, such as bulk containers and transport drums.

To combat counterfeit agrochemicals, companies are increasingly adopting digital traceability tools such as QR codes, holographic printing, and blockchain-based authentication. At the same time, there is a rising demand for premium, technologically advanced packaging solutions that combine durability, advanced printing, and enhanced security features. Local manufacturers are scaling up investments in R&D and facility upgrades to meet demand for packaging that not only preserves spirotetramat quality but also aligns with China’s sustainability and traceability objectives.

India: EPR Obligations and Diverse Agrochemical Packaging Formats

The India spirotetramat packaging market is shaped by the Plastic Waste Management (Amendment) Rules, 2024, which came into effect in April 2025. These rules emphasize Extended Producer Responsibility (EPR), making agrochemical packaging producers accountable for collection, recycling, and safe disposal. From July 1, 2025, all agrochemical packaging in India must carry barcodes or QR codes for full traceability, significantly increasing packaging compliance and accountability.

India’s rapidly expanding agricultural sector continues to boost demand for effective pest control solutions, driving the adoption of robust and versatile packaging formats. Manufacturers are catering to diverse farmer needs by offering small sachets and bottles for individual farmers and large-capacity drums and cans for commercial farming operations. This market is also influenced by India’s rising emphasis on pesticide safety and eco-friendly material use, pushing companies toward cost-effective, recyclable, and tamper-resistant packaging formats.

Japan: Plastic Reduction Laws and Compostable Agrochemical Packaging

The Japan spirotetramat packaging market is transitioning under the Plastic Resource Circulation Strategy, which requires all plastic packaging to be reusable or recyclable by 2025. This regulation is reinforced by the Plastic Resource Circulation Promotion Law, effective in 2025, mandating the reduction or redesign of 12 categories of single-use plastics. These measures are accelerating the shift from plastic agrochemical containers to compostable and paper-based alternatives.

In addition, Japan’s long-term sustainability target of doubling renewable material usage by 2030 is shaping R&D in smart plastics and bio-based packaging. Companies are responding with eco-innovations in container design, including barrier-coated paper canisters and biopolymer-based bottles. The combination of strict environmental regulations and cutting-edge material innovation is positioning Japan as a leader in next-generation agrochemical packaging solutions.

Brazil: Reverse Logistics and Agrochemical Waste Management Reforms

The Brazil spirotetramat packaging market is heavily influenced by the National Solid Waste Policy (PNRS), which prioritizes responsible waste disposal, reuse, and recycling. With Law No. 15,088 taking effect in January 2025, banning the import of plastic waste, domestic producers are compelled to build sustainable internal recycling ecosystems.

A major development in Brazil is the government’s promotion of a reverse logistics system, which places responsibility on agrochemical producers to manage the post-consumer collection and recycling of containers. For spirotetramat packaging, this means manufacturers must ensure durable, recyclable, and compliant packaging formats that can withstand Brazil’s tropical climate while also meeting environmental mandates. These policies are reshaping the competitive landscape, with local and multinational agrochemical companies aligning packaging design with Brazil’s circular economy framework.

Spirotetramat Packaging Market Report Scope

Spirotetramat Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$251.1 Million

|

|

Market Size (2034)

|

$354.3 Million

|

|

Market Growth Rate

|

3.9%

|

|

Segments

|

By Material (Plastic, Metal, Glass, Composite Materials), By Product Type (Bottles & Cans, Drums, Pouches & Bags, Boxes & Cartons), By End-Use Industry (Agriculture, Public Health & Hygiene, Others), By Formulation (Suspension Concentrate, Water-Dispersible Granules, Soluble Granules, Oil Dispersion, Others)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Bayer AG, DuPont de Nemours, Inc., Syngenta AG, BASF SE, Nufarm Limited, Amcor plc, Mondi Group, Sonoco Products Company, Huhtamaki Oyj, Silgan Holdings Inc., WestRock Company, Greif, Inc., Mauser Packaging Solutions, LC Packaging, United Caps

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Spirotetramat Packaging Market Segmentation

By Material

- Plastic

- Metal

- Glass

- Composite Materials

By Product Type

- Bottles & Cans

- Drums

- Pouches & Bags

- Boxes & Cartons

By End-Use Industry

- Agriculture

- Public Health & Hygiene

- Others

By Formulation

- Suspension Concentrate

- Water-Dispersible Granules

- Soluble Granules

- Oil Dispersion

- Others

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Spirotetramat Packaging Market

- Bayer AG

- DuPont de Nemours, Inc.

- Syngenta AG

- BASF SE

- Nufarm Limited

- Amcor plc

- Mondi Group

- Sonoco Products Company

- Huhtamaki Oyj

- Silgan Holdings Inc.

- WestRock Company

- Greif, Inc.

- Mauser Packaging Solutions

- LC Packaging

- United Caps

* List Not Exhaustive

Methodology

The research methodology for the Spirotetramat Packaging Market combines rigorous primary and secondary research to deliver actionable, industry-focused insights. USDAnalytics conducted in-depth interviews with packaging engineers, agrochemical formulators, supply chain managers, and regulatory specialists across key regions including North America, Europe, Asia-Pacific, India, Japan, and Brazil. Secondary research included analysis of corporate sustainability reports, regulatory filings, technical journals, and verified industry publications to understand trends in material innovation, lightweighting, RFID integration, and recyclable-by-design container technologies. Market sizing and growth projections were derived using both top-down and bottom-up approaches, incorporating regional regulatory frameworks such as EPR, PPWR, Plastic Waste Management Rules, and Japan’s Plastic Resource Circulation Strategy. Data triangulation ensured accuracy across materials, product types, formulations, and end-use industries, while competitive intelligence from leading players like Bayer, Syngenta, and ADAMA informed strategic market insights. This methodology ensures the report provides reliable intelligence for professionals seeking to optimize packaging solutions, enhance sustainability, and comply with evolving agrochemical regulations globally.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.