Advanced Surface Protection and Aesthetic Durability Driving Consistent Growth

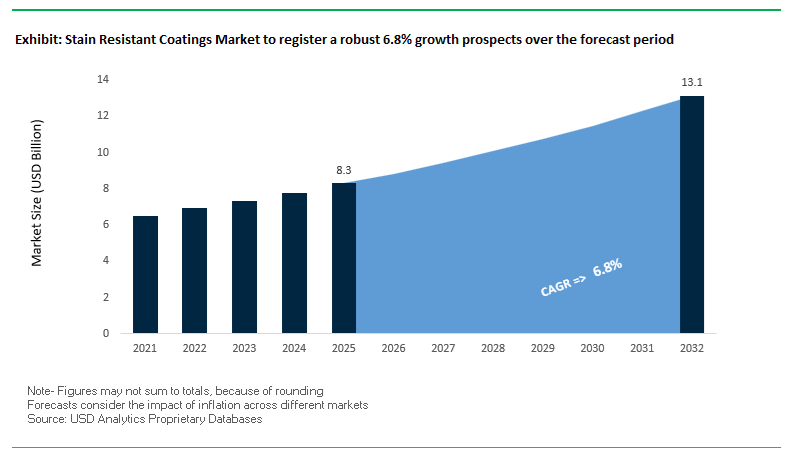

The global Stain Resistant Coatings Market is expanding steadily, supported by rising demand for high-performance decorative finishes, protective coatings, and easy-to-maintain surfaces across residential, commercial, automotive, and industrial applications. The market was valued at $8.3 billion in 2025 and is projected to reach $13.2 billion by 2032, growing at a CAGR of 6.8% during 2025–2032. This growth reflects increasing consumer and industrial preference for coatings that combine aesthetic longevity with functional resistance to stains, chemicals, and environmental contaminants.

A key structural driver is the growing demand for low-maintenance, high-durability coatings in high-traffic environments, such as commercial buildings, healthcare facilities, hospitality spaces, and transportation infrastructure. These coatings are engineered to resist oil, grease, dirt, water spotting, and chemical exposure, significantly reducing cleaning costs and extending repaint cycles. Additionally, the rise of premium interior finishes is pushing manufacturers to develop coatings that maintain matte or flat aesthetics without compromising stain resistance, a historically challenging balance.

Another important growth factor is the increasing adoption of multi-functional coatings that integrate stain resistance with additional properties such as antimicrobial protection, UV resistance, and self-cleaning capabilities. These innovations are particularly relevant in sectors such as healthcare, food processing, and marine applications, where hygiene and surface cleanliness are critical.

The market is also benefiting from advancements in nanotechnology, fluoropolymer chemistry, and hybrid coating systems, enabling the development of surfaces that actively repel contaminants or prevent their adhesion. At the same time, sustainability trends are influencing formulation strategies, with manufacturers focusing on low-VOC, PFAS-free, and environmentally compliant stain-resistant technologies that align with global regulatory frameworks.

Market Analysis: Flat-Finish Innovation, Marine Anti-Fouling Technologies, and Strategic Consolidation Reshaping Market Dynamics

The stain-resistant coatings market is being shaped by product innovation, strategic mergers, and cross-sector application expansion, reflecting a shift toward high-performance and multifunctional surface technologies. The March 2026 proposed merger between AkzoNobel and Axalta represents a major consolidation move, combining extensive portfolios in decorative, automotive refinish, and industrial stain-resistant coatings. This merger is expected to create a global leader with enhanced R&D capabilities and scale advantages across multiple end-use sectors.

Product innovation is increasingly focused on addressing performance gaps in aesthetic coatings. PPG’s Master’s Mark Ballard™ Flat Interior coating (January 2026) introduces a flat-finish system with enhanced scrub and stain resistance, overcoming traditional limitations where matte coatings were more prone to staining. This development is particularly relevant for high-traffic interior spaces requiring both durability and design appeal.

In advanced applications, stain resistance is being integrated into high-performance and specialty coatings. AkzoNobel’s March 2026 aerospace facility upgrade enables the production of coatings with enhanced stain and chemical resistance for aircraft interiors and exteriors, where cleanliness and durability are critical.

Strategic positioning in premium decorative segments is also evident. Hempel’s “Accelerate to Win” strategy (January 2026) emphasizes expansion of luxury “stain-shield” coating lines under brands such as Farrow & Ball and Crown Paints, targeting high-end residential and commercial markets with premium performance and aesthetic appeal.

The automotive and energy sectors are driving demand for chemical-resistant coatings. Jotun’s June 2025 EV battery coating systems provide protection against electrolyte stains and environmental contaminants, while maintaining electrical insulation and fire safety, highlighting the role of stain resistance in next-generation mobility solutions.

Cross-sector innovation is further expanding the definition of stain resistance. AkzoNobel’s Calosol partnership (December 2025) integrates self-cleaning and stain-resistant properties into solar-absorbing architectural coatings, ensuring long-term performance of energy-harvesting surfaces. Similarly, its Intersleek® 1100SR marine coating utilizes fluoropolymer technology to prevent biofouling and organic staining, representing a marine equivalent of stain-resistant functionality.

Strategic acquisitions are also strengthening market reach. RPM International’s June 2025 acquisition of Ready Seal Inc. expands its presence in wood protection and semi-transparent stain-resistant coatings, particularly for outdoor infrastructure.

In automotive coatings, BASF’s 2025–2026 “Driving the Proxy” collection introduces advanced finishes with intrinsic resistance to water spotting and environmental staining, combining aesthetic innovation with functional performance. Meanwhile, foundational technologies such as Dalton Enterprises’ QuickPatch H2O (November 2024) enhance surface preparation by creating non-porous substrates, improving the effectiveness of subsequent stain-resistant coatings.

Market Trend: EPA TSCA PFAS Reporting Requirements Reshape Stain-Resistant Textile and Carpet Coatings Market

The implementation of the U.S. EPA’s TSCA Section 8(a)(7) reporting rule in 2026 is significantly restructuring the stain resistant coatings industry, particularly in textile and carpet applications historically dependent on fluorochemical technologies. The rule mandates comprehensive disclosure of PFAS usage across the entire value chain, including imported finished goods containing even trace levels of fluorinated compounds. With regulators evaluating a 0.1% concentration threshold, the scope of compliance expands to thousands of previously unreported applications, creating a substantial data collection and reporting burden for manufacturers, importers, and distributors. Additionally, the enforcement of the Significant New Use Rule under the EPA’s PFAS Strategic Roadmap requires immediate notification for any reintroduction of inactive PFAS substances, effectively closing regulatory loopholes that previously allowed legacy chemistries to re-enter the market. This dual-layer regulatory pressure is accelerating the phase-out of C6 and C8 fluorocarbon-based stain resistant coatings, forcing manufacturers to reassess product formulations, supply chains, and long-term compliance strategies. The textile coatings segment is therefore transitioning toward non-fluorinated alternatives, with regulatory compliance emerging as a primary driver of innovation and market differentiation.

Market Trend: EU PPWR 2026 Mandates Complete PFAS Elimination in Food-Contact Packaging Coatings

The European Union’s Packaging and Packaging Waste Regulation, effective August 12, 2026, introduces one of the most stringent regulatory frameworks for PFAS elimination in food-contact materials. The regulation enforces a complete ban on intentionally added PFAS in paper and board packaging, with strict concentration thresholds set at 25 parts per billion for individual PFAS, 250 parts per billion for cumulative PFAS, and 50 parts per million for total fluorinated substances including polymeric variants. Unlike previous regulatory approaches, the PPWR includes no grandfathering provisions, meaning all packaging products entering the EU market after the enforcement date must comply regardless of production timeline. This creates immediate inventory risk for manufacturers holding non-compliant stock and is driving rapid reformulation efforts across the paperboard coatings sector. The regulation is also influencing global supply chains, as exporters targeting the European market must align with these stringent requirements. As a result, the industry is witnessing a decisive shift away from fluorinated stain-resistant coatings toward alternative chemistries that can deliver barrier performance without regulatory exposure. This regulatory inflection point is redefining competitive dynamics and accelerating the commercialization of PFAS-free coating technologies.

Market Opportunity: Bio-Based Non-Fluorinated Coatings Unlock Sustainable Growth in Textile and Apparel Applications

The phase-out of fluorocarbon-based chemistries is creating a significant opportunity for bio-based, non-fluorinated stain resistant coatings in textile and apparel markets. These “C0” technologies leverage hydrocarbon, silicone, and plant-derived wax chemistries to achieve durable water repellency while meeting stringent environmental and regulatory requirements. Recent advancements have enabled bio-based coatings to achieve static water contact angles exceeding 130 degrees, aligning closely with the hydrophobic performance of legacy C6 fluorochemical systems. Moreover, improvements in formulation stability and fiber adhesion have enhanced wash durability, with modern hydrocarbon-based treatments maintaining up to 80% of their repellency after 30 to 50 industrial wash cycles. This represents a substantial improvement over earlier generations of bio-based coatings that exhibited rapid performance degradation. However, a key technical challenge remains in achieving oil repellency, where non-fluorinated systems typically reach only Grade 1 to 2 on the AATCC 118 scale compared to Grade 6 for traditional fluorochemicals. This performance gap is driving ongoing research into hybrid nanocomposite additives and multifunctional coating systems. As sustainability mandates intensify and consumer demand for PFAS-free products increases, bio-based stain resistant coatings are positioned as a critical growth segment within the global coatings market.

Market Opportunity: Easy-Clean Nano-Coatings Expand Adoption in Residential Surfaces and High-Traffic Interiors

The residential coatings segment is experiencing strong growth in easy-clean, stain resistant technologies designed for kitchen and bathroom applications. These coatings utilize advanced nano-ceramic and alkoxysilane chemistries to create surfaces that are both hydrophobic and oleophobic, significantly reducing the adhesion of contaminants such as oils, fingerprints, and mineral deposits. By lowering surface free energy to below 25 mN/m, these coatings enable effortless removal of stains using minimal cleaning agents, reducing chemical cleaner usage by up to 60% to 75%. In terms of durability, nano-ceramic coatings are achieving pencil hardness levels of 9H under ASTM D3363 testing, providing robust protection against abrasion and chemical attack. This makes them particularly suitable for high-use surfaces such as stone countertops, glass panels, and ceramic tiles, where resistance to acidic substances like vinegar and citrus is critical. Additionally, in high-humidity environments, superhydrophobic sol-gel coatings have demonstrated up to 90% reduction in limescale buildup over a 12-month period, enhancing both aesthetic appeal and maintenance efficiency. As consumers increasingly prioritize convenience, hygiene, and long-term durability, easy-clean coatings are emerging as a high-value application segment within the stain resistant coatings industry.

Stain Resistant Coatings Market Share and Segmentation Insights: Fluoropolymer Leadership and Direct Industrial Supply Trends

By Chemistry: Fluoropolymer Coatings Lead with Ultra-Low Surface Energy and High Durability

The fluoropolymers segment (PTFE, PVDF) dominated the stain resistant coatings market with a 36.5% share in 2025, driven by its unmatched low surface energy and superior stain repellency performance. Fluoropolymer coatings exhibit extremely low surface tension levels of 18–20 dynes/cm, enabling liquids such as oil, wine, coffee, and ink to bead and roll off surfaces, effectively preventing staining. This makes them the preferred choice for automotive interiors, performance textiles, carpets, and high-end upholstery applications. In addition to stain resistance, fluoropolymers provide excellent chemical resistance and thermal stability, allowing them to withstand harsh cleaning agents and elevated temperatures without degradation. These properties are critical in both industrial and consumer-facing applications, where durability and long-term performance are essential. The combination of advanced surface protection, easy-clean functionality, and high durability coatings continues to position fluoropolymers as the leading chemistry in the global stain resistant coatings market.

By Distribution Channel: Direct Sales Channel Dominates with Industrial Integration and Custom Formulation Demand

The direct sales segment accounted for a leading 54.2% share of the stain resistant coatings market in 2025, reflecting the strong demand from industrial manufacturers and OEM production environments. Large-scale producers in sectors such as automotive seating, furniture manufacturing, footwear, and technical textiles procure stain-resistant fluorochemicals directly from suppliers for integration during manufacturing processes, rather than through retail channels. This direct engagement enables custom formulation development tailored to specific substrates, including suede, leather, nylon, and polyester, ensuring optimal stain resistance performance and durability. Additionally, brands require rigorous performance testing and validation, including resistance to oils, liquids, and repeated cleaning cycles, which is best achieved through close collaboration with coating manufacturers. By offering technical expertise, proprietary formulations, and consistent quality assurance, the direct sales channel continues to drive innovation and maintain its leadership in the global stain resistant coatings market.

Competitive Landscape of the Stain-Resistant Coatings Market

PPG Leads Market with High-Performance Interior Coatings and Sustainable Formulations

PPG Industries, Inc. is a frontrunner in the stain-resistant coatings market, leveraging its global leadership in architectural and protective coatings. In 2026, the company introduced the MASTER’S MARK BALLARD™ Flat Interior Paint, offering superior hiding power along with enhanced scrub and stain resistance for premium residential applications. Under its “Refresh & Sustain” strategy, PPG is prioritizing health-conscious and long-lasting coatings, aligning with consumer demand for durability and sustainability. Its global presence across 70+ countries ensures strong supply chain resilience and market reach.

AkzoNobel Strengthens Market Position with Aesthetic Innovation and Easy-to-Clean Technologies

AkzoNobel N.V. is a major player in the stain-resistant coatings market, combining color innovation with surface performance. Its Rhythm of Blues™ collection introduces stain-resistant coatings for construction and appliance metals, integrating aesthetic appeal with functionality. The company is also expanding its portfolio with “Easy-to-Clean” topcoats such as TRINAR and CERAM-A-STAR, designed for low-maintenance commercial and industrial applications. Its ongoing merger with Axalta is expected to further consolidate its leadership in this segment.

Axalta Drives Innovation with AI-Powered Customization and High-Durability Coatings

Axalta Coating Systems is a key innovator in the stain-resistant coatings market, supported by strong financial performance and advanced R&D capabilities. Its EcoNextJet™ system enables drop-on-demand customization for stain-resistant automotive exteriors using advanced polymers. The company’s Industrial segment is also expanding into stain-resistant coatings for fabrics and upholstery, offering superior chemical and abrasion resistance. Its strong EBITDA margin and cash flow support ongoing investment in nanoparticle-based stain-blocking technologies.

BASF Strengthens Market Backbone with Sustainable Resins and UV-Stable Additives

BASF SE plays a critical role in the stain-resistant coatings market, focusing on sustainability and advanced material supply. The company has expanded production of HALS and NOR® HALS stabilizers, which maintain clarity and durability of stain-resistant coatings under UV exposure. Its transition to renewable electricity across European operations significantly reduces the carbon footprint of its products. BASF’s vertically integrated production ensures consistent supply of bio-based and waterborne binders, reinforcing its position as a key supplier in this segment.

Sherwin-Williams Expands Market Leadership with Smart Surface and Low-VOC Technologies

The Sherwin-Williams Company is strengthening its position in the stain-resistant coatings market, particularly in North America. Its SHIFT 2026 color trend initiative supports the development of coatings that emphasize longevity, durability, and ease of maintenance. The company’s General Industrial Coatings division is rolling out low-VOC stain-blocking finishes for cabinetry and furniture, targeting high-traffic applications. Its Loxon® and ConFlex® systems provide heavy-duty stain and weather resistance for building exteriors, reinforcing its leadership in construction markets.

3M Leads Nanotechnology Segment with PFAS-Free Repellent Coatings

3M is a specialist leader in the stain-resistant coatings market, particularly in nanotechnology-driven solutions. The company is transitioning toward fluorine-free liquid repellency systems, aligning with global regulatory mandates. Its coatings are widely used in textiles, healthcare, and consumer electronics, providing oleophobic and hydrophobic properties for enhanced stain resistance. 3M’s dominance in the healthcare sector highlights its expertise in coatings that combine fluid resistance with antimicrobial performance, strengthening its position in high-growth applications.

Germany Leading PFAS-Free Innovation with Bio-Based Nanochemistry and Functional Surfaces

Germany remains a global benchmark in the stain-resistant coatings market, driven by its leadership in PFAS-free, bio-based coating technologies. The development of polyurethane-siloxane hybrid coatings derived from renewable feedstocks is enabling high-performance stain resistance without reliance on fluorocarbons, achieving top-tier resistance against both acidic and alkaline contaminants.

Regulatory frameworks such as the DGNB sustainable building standards are accelerating the adoption of ultra-low VOC coatings, supported by tax incentives for environmentally compliant materials. Infrastructure investments in healthcare facilities are boosting demand for antimicrobial and stain-resistant coatings capable of withstanding aggressive cleaning cycles. Product innovations such as photocatalytic self-cleaning coatings are enhancing urban façade performance, while applications in high-speed rail interiors are reducing maintenance frequency through advanced nanostructured ceramic stain barriers.

China Strengthening High-Safety Stain-Resistant Coatings for Food, Electronics, and Construction

China is rapidly advancing in the stain-resistant coatings market, transitioning toward high-safety, specialty applications. Regulatory updates such as GB 4806.10-2025 are enforcing stringent safety standards for food-contact coatings, including strict limits on harmful chemical migration.

Technological advancements include the localization of ultra-thin ETFE coatings for solar panels, providing superior anti-soiling and stain resistance in high-dust environments. The electronics sector is a major driver, with widespread adoption of oleophobic coatings for foldable devices, preventing fingerprint and oil contamination. Infrastructure standards are also evolving, with updated waterproofing regulations ensuring that stain-resistant coatings meet fire safety and durability requirements. Additionally, investments in graphene-enhanced coatings and expanded manufacturing capacity are strengthening China’s role in high-performance industrial applications.

India Emerging as a High-Growth Market Driven by Green Building Regulations and Urban Infrastructure

India is witnessing rapid growth in the stain-resistant coatings market, driven by government mandates and urbanization. Proposed regulations requiring low-VOC certified materials in construction projects are accelerating the adoption of environmentally friendly coating solutions across residential and commercial sectors.

Infrastructure development under Smart Cities initiatives is boosting demand for anti-graffiti and easy-clean coatings in public transit systems. Technological innovations include the development of waterborne ceramic-polyester hybrid coatings designed for tropical climates, offering resistance to fungal growth and humidity-related staining. Local manufacturing expansion and innovations such as bio-based coatings derived from cashew nutshell liquid (CNSL) are further strengthening domestic capabilities. Additionally, applications in high-speed rail interiors and textiles highlight the growing importance of stain-resistant coatings in both infrastructure and consumer markets.

United States Driving PFAS-Free Transition and High-Performance Stain-Resistant Coatings

The United States is a key innovator in the stain-resistant coatings industry, driven by regulatory changes and demand for high-performance applications. The EPA’s updated regulations are accelerating the shift toward fluorine-free, water-based stain-resistant coatings, particularly in textiles and consumer goods.

Technological advancements include the development of ceramic-based automotive clearcoats with high hardness and resistance to environmental contaminants, as well as self-healing stain-resistant polymers for enhanced durability. The adoption of silicone-based cool roof coatings with dirt pick-up resistance (DPUR) is improving long-term reflectivity and energy efficiency. High-value applications include optical-grade coatings for AR/VR devices and medical equipment, where smudge resistance is critical. Additionally, defense applications are driving innovation in omniphobic coatings designed to repel chemical contaminants, highlighting the strategic importance of advanced stain-resistant technologies.

Japan Leading Nano-Precision Stain-Resistant Coatings for Consumer and Healthcare Applications

Japan is a global leader in nano-scale stain-resistant coatings, focusing on high-end consumer goods and healthcare applications. Innovations such as nano-silica infused coatings for kitchen surfaces are preventing deep penetration of oils and stains, enhancing durability and ease of cleaning.

Technological breakthroughs include the development of liquid-like solid surfaces (SLIPS) that allow viscous substances to slide off without residue. Government initiatives are supporting the development of biocompatible coatings for medical equipment, ensuring hygiene and safety. Product innovations such as invisible anti-fingerprint coatings are improving aesthetics in automotive interiors, while expanding applications in semiconductor packaging and senior living infrastructure highlight Japan’s leadership in precision coating technologies.

South Korea Driving Advanced Stain-Resistant Coatings for Electronics and Appliances

South Korea is a global leader in stain-resistant coatings for electronics and appliances, driven by its strong presence in the consumer electronics industry. Innovations such as multi-layer hard-coat films for foldable devices are delivering high durability and permanent oleophobic properties, ensuring long-term performance.

Technological advancements include the development of anti-stain metallic-effect coatings for premium appliances, combining aesthetics with functionality. Investments in specialty resin production are supporting the growth of UV-cured stain-resistant coatings, while regulatory updates are accelerating the shift toward eco-friendly formulations. Key applications include conformal coatings for wearable electronics, providing resistance to sweat and oils, and easy-clean coatings for airport infrastructure, ensuring hygiene and clarity in high-traffic environments.

Stain Resistant Coatings Market Report Scope

Stain Resistant Coatings Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$8.3 Billion

|

|

Market Size (2032)

|

$13.2 Billion

|

|

Market Growth Rate

|

6.8%

|

|

Segments

|

By Chemistry (Siloxane Copolymers, Fluoropolymers, Polyurethane, Acrylics, Epoxy, Bio-based), By Technology (Water-borne, Solvent-borne, Powder Coatings, UV-cured Coatings, Nanocoatings), By Application (Architectural Coatings, Textile Softeners and Repellents, Cookware and Bakeware, Floor and Wall Protection, Industrial and Protective), By End-User Industry (Building and Construction, Automotive and Transportation, Electrical and Electronics, Textiles and Leather, Healthcare and Hospitality, Packaging), By Distribution Channel (Direct Sales, Specialized Industrial Distributors, Retail)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

PPG Industries, Inc., Akzo Nobel N.V., The Sherwin-Williams Company, 3M Company, BASF SE, Axalta Coating Systems Ltd., DuPont de Nemours, Inc., Nippon Paint Holdings Co., Ltd., Kansai Paint Co., Ltd., Jotun Group, Hempel A/S, The Chemours Company, Arkema S.A., Asian Paints Limited, Berger Paints India Limited

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Stain Resistant Coatings Market Segmentation

By Chemistry

- Siloxane Copolymers

- Fluoropolymers

- Polyurethane

- Acrylics

- Epoxy

- Bio-based

By Technology

- Water-borne

- Solvent-borne

- Powder Coatings

- UV-cured Coatings

- Nanocoatings

By Application

- Architectural Coatings

- Textile Softeners and Repellents

- Cookware and Bakeware

- Floor and Wall Protection

- Industrial and Protective

By End-User Industry

- Building and Construction

- Automotive and Transportation

- Electrical and Electronics

- Textiles and Leather

- Healthcare and Hospitality

- Packaging

By Distribution Channel

- Direct Sales

- Specialized Industrial Distributors

- Retail

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Stain Resistant Coatings Industry

- PPG Industries, Inc.

- Akzo Nobel N.V.

- The Sherwin-Williams Company

- 3M Company

- BASF SE

- Axalta Coating Systems Ltd.

- DuPont de Nemours, Inc.

- Nippon Paint Holdings Co., Ltd.

- Kansai Paint Co., Ltd.

- Jotun Group

- Hempel A/S

- The Chemours Company

- Arkema S.A.

- Asian Paints Limited

- Berger Paints India Limited

*- List not Exhaustive