Market Overview: Stainless Steel Wire Rods Market Anchored By High-Corrosion-Resistance Alloys, Cold-Heading Precision & Decarbonized Melt Routes

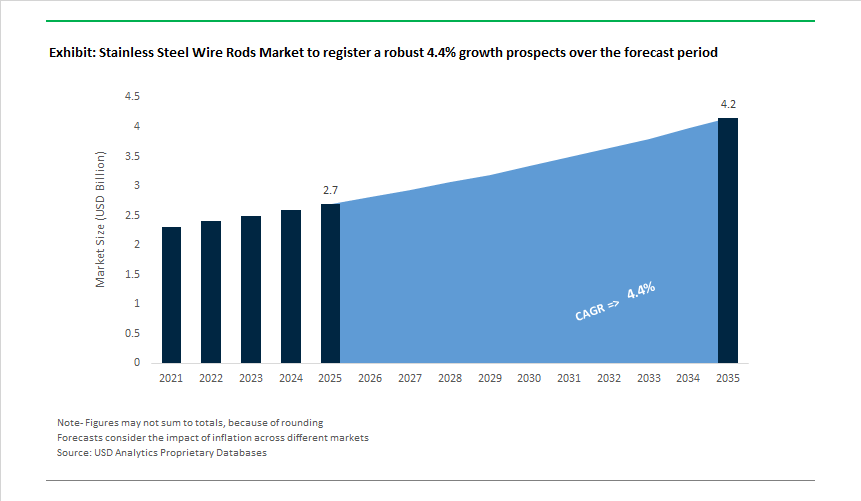

The Stainless Steel Wire Rods Market is valued at USD 2.7 billion in 2025 and is expected to reach USD 4.2 billion by 2035, growing at a CAGR of 4.4%, supported by surging requirements across automotive fasteners, construction anchors, aerospace components, medical instrumentation, marine hardware, and oil & gas infrastructure. As end-use applications demand higher mechanical reliability and corrosion resistance, manufacturers are transitioning rapidly toward super duplex, high-strength austenitic, and precipitation-hardened stainless grades, each requiring extremely tight control of chemistry, inclusion morphology, and surface integrity at the wire rod stage.

Further, procurement teams increasingly require low-carbon and traceable stainless steel, accelerating adoption of Electric Arc Furnace (EAF) production routes with >90% recycled content. This transition forces manufacturers to balance sustainability targets with metallurgical consistency, particularly for grades where sulfur, nitrogen, and residual elements must be precisely managed to maintain toughness, polishability, and pitting resistance. As automotive OEMs, construction material suppliers, and energy-sector operators tighten specifications around LCA/Scope 3 emissions, PREN thresholds, and cold-formability windows, wire rod suppliers must now deliver predictable microstructure, certified sustainability metrics, and application-ready mechanical profiles rather than commodity-grade output.

Market Analysis: Global Expansion, Policy Impacts & Low-Carbon Innovation

The industry is witnessing accelerated capacity expansion and technology adoption across Asia, Europe, and the Americas, driven by regional policy interventions and the sustained shift toward low-carbon stainless steel. In November 2023, Synergy Steels completed a new 0.15 MTPA stainless steel wire rod facility in Rajasthan, enhancing India’s domestic supply and reducing import dependence-an important development ahead of India’s infrastructure and automotive expansion cycles. By November 2024, major players including Walsin Lihwa and Marcegaglia Fagersta Stainless committed substantial capital investments across Indonesia and Europe, adding 300,000 TPA of Southeast Asian production and doubling stainless steel output at the Fagersta plant, respectively. Simultaneously, the EU extended anti-dumping and countervailing duties (up to 24% ad valorem) to protect domestic manufacturers from low-cost imports, reshaping supply chain decisions across European markets.

In March 2025, U.S. domestic steel policy reasserted itself with reinstated tariffs under Section 232, raising import duties to 50% effective June 2025, injecting volatility into supply contracts-particularly for automotive fasteners and industrial fabrication segments reliant on overseas stainless grades. On the other hand, April 2025 saw India’s Bansal Wire Industries inaugurate a major stainless steel wire facility (360,000 MTPA), significantly strengthening India’s wire rod capability and positioning the country as a rising export hub. During the same month, Fagersta Stainless and Danieli formalized a partnership to install a 70,000-ton blooming mill by late 2026, improving product range flexibility and billet quality for specialty stainless applications.

By December 2025, sustainability moved into sharper focus with Acerinox launching EcoACX®, a stainless steel line leveraging recycled content and low-carbon melting to support green manufacturing objectives. This follows a broader trend of global stainless steel producers adopting Electric Arc Furnaces and recycled scrap-intensive processes to achieve 75% lower CO₂ footprints compared to conventional routes.

Stainless Steel Wire Rods Market: Trends and Opportunities

High-Strength, Thermally Stable Wire Rod Grades Gain Traction in EV Safety Architectures

Automotive electrification is reshaping material selection for safety-critical components, accelerating a shift from conventional austenitic 304/316 wire rods toward high-strength duplex and ferritic–austenitic stainless grades. The driver is not only lightweighting, but thermal survivability during battery failure scenarios. In 2025, disclosures from Aperam highlighted that stainless steel retains ~70% of its original strength at 800°C, compared with ~15% for carbon steel, while aluminum approaches its melting point near 660°C. This performance gap is making stainless wire rods the default choice for EV battery enclosures, safety cages, springs, and structural fasteners that must withstand thermal runaway without catastrophic loss of integrity.

Formability improvements are reinforcing adoption. New EV-oriented austenitic chemistries now exceed 50% elongation, enabling deep-drawn battery module casings and complex brackets to be formed from a single rod-feed, reducing weld count and assembly complexity. Corrosion performance adds a second-order advantage: 2025 road-salt exposure trials showed zero measurable corrosion after 24 months for stainless wire rod–based under-chassis components, allowing OEMs to eliminate secondary coatings. The result is a simplified logistics chain, lower component mass for small-diameter fasteners, and improved lifecycle durability—positioning advanced stainless wire rods as a system-level enabler of EV safety and manufacturability.

Precision-Grade Stainless Rods Enable the Scaling of Robotic-Assisted Surgery

The rapid expansion of robotic-assisted surgery (RAS) is creating demand for ultra-clean, precision stainless steel wire rods that can be drawn into fine wires—often between 0.003” and 0.180”—for motion-control cables, actuation systems, and end-effectors. Surgical robotics requires a rare combination of tensile strength, flexibility, and fatigue resistance, driving preference for high-purity 304 and 316L feedstock with tightly controlled surface quality. By 2025, engineering benchmarks favored 1×19 and 7×19 cable constructions, derived from precision wire rods, for robotic arms that must transmit force reliably through tortuous anatomical pathways.

Platform scaling is amplifying volume pull. The June 2024 launch of the SS Innovations Mantra 3—featuring up to five modular robotic arms—significantly increased per-system consumption of medical-grade stainless wire. With more than 5,000 procedures completed by late 2025, OEMs and device developers are shifting toward “FastLane” sourcing programs that guarantee rapid access to certified fine wire for accelerated tool iteration. In parallel, martensitic stainless wire rods are being optimized for endoscopic instruments subjected to millions of micro flex-cycles in pulley-driven systems, maintaining fatigue resistance without work-hardening into brittleness—an uncompromisable requirement for telesurgery safety and regulatory approval.

Low-Cobalt, Corrosion-Resistant Fasteners Create a Structural SMR Opportunity

The move toward Small Modular Reactors (SMRs) is creating a distinct, high-margin opportunity for stainless steel wire rods engineered to nuclear specifications. Unlike large, bespoke reactors, SMRs adopt factory-based serial production, generating predictable, repeat demand for fasteners, tendons, and threaded components. The World Nuclear Association emphasized in late 2025 that this modularization fundamentally changes procurement patterns—favoring long-term supplier qualification over episodic project sourcing.

Material requirements are stringent. Low-cobalt stainless grades are essential to minimize radiation-induced activation in primary coolant systems, while corrosion resistance must be sustained over decades. For emerging molten salt reactor (MSR) designs, compatibility with aggressive salts at >600°C is critical. Outokumpu is actively developing high-ductility alternatives to 347H for SMR tanks and internals, targeting resistance to potassium nitrate and molten salt chemistries. Additional niche demand arises in start-up neutron source assemblies, where stainless wire rods encapsulate Californium-252 sources and must meet NRC and ISO 2919 standards—requiring near-zero surface defects to ensure flawless TIG welding and long-term containment integrity.

High-Surface-Area Wire Mesh Positions Stainless Rods at the Core of Green Hydrogen Plants

Green hydrogen production is opening a fast-growing application for stainless steel wire rods in the form of woven wire mesh electrodes, gas diffusion layers (GDLs), and porous transport layers (PTLs) used in alkaline and PEM electrolyzers. These meshes must combine electrical conductivity, corrosion resistance, and mechanical stability under continuous pressure cycling. In October 2025, peer-reviewed research demonstrated that magnetically modified mesh electrodes can deliver >35% energy savings in alkaline electrolysis by accelerating bubble detachment—directly linking mesh geometry and surface area to system efficiency.

PEM systems are pushing innovation further. Manufacturers such as Haver & Boecker are supplying 3D-woven stainless meshes that serve as PTLs and can be subsequently coated with titanium or iridium to enhance corrosion resistance in ultra-pure water environments. Longevity is the decisive metric at scale: adoption of nickel-alloyed austenitic wire rods is enabling mesh components to achieve 20+ year service life under chemical attack and pressure fluctuation. This durability is critical for lowering hydrogen production costs over time, positioning stainless steel wire rods not as commodity inputs, but as performance-critical materials in gigawatt-scale electrolyzer infrastructure.

Market Share Analysis: Stainless Steel Wire Rods Market

Market Share by Grade: 300 Series Austenitic Wire Rods Define Industrial Versatility and Longevity

The 300 Series (austenitic) stainless steel wire rods command approximately 65% of the global market, underscoring their position as the universal standard for downstream wire processing and high-reliability applications. This dominance is structurally driven by the high nickel content of 300 Series grades, which delivers an optimal combination of ductility, corrosion resistance, and thermal stability unmatched by ferritic or martensitic alternatives. Type 304, often referred to as the 18/8 benchmark, remains the most widely specified grade because it can be cold-drawn into ultra-fine diameters without fracture, enabling high-speed production of springs, fasteners, meshes, and precision wires with minimal yield loss. From a lifecycle economics perspective, higher-alloy grades such as 316L offer superior resistance to chloride-induced corrosion, significantly extending service life in coastal, chemical, and infrastructure environments where lower-alloy steels fail prematurely. The non-magnetic behavior of 300 Series wire rods further expands their addressable market, particularly in electronics, medical equipment, and imaging environments where electromagnetic neutrality is mandatory. High-temperature strength adds another layer of strategic value, as selected 300 Series grades maintain mechanical integrity in furnace components and exhaust systems exposed to extreme heat. Collectively, these performance attributes explain why 300 Series stainless steel wire rods remain the default material choice across industrial value chains, securing their dominant share in the global market.

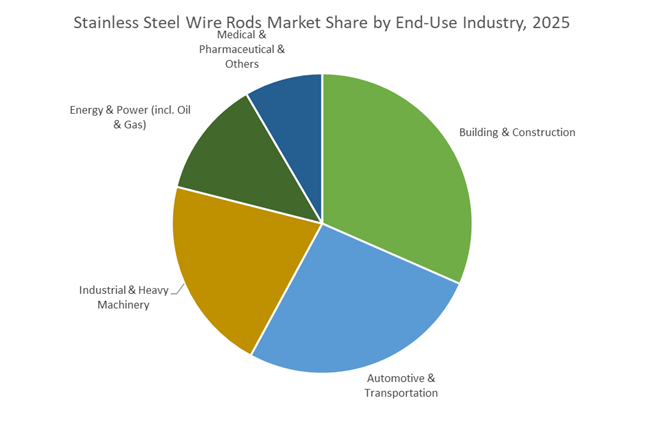

Market Share by Application: Building and Construction Anchor Long-Term Wire Rod Demand

The building and construction sector accounts for approximately 30% of total demand in the Stainless Steel Wire Rods Market, making it the largest application segment and a stable anchor for long-term consumption. This leadership is driven by the global pivot toward durable, low-maintenance infrastructure, where stainless steel wire rods offer lifecycle advantages that align with public spending priorities and sustainability goals. In bridges, façades, and reinforced concrete systems, austenitic wire rods provide exceptional corrosion resistance and tensile durability, extending structural service life by decades compared to carbon steel alternatives and significantly reducing repair and rehabilitation costs. Market share is further reinforced by the material’s seismic performance, as high elongation and energy absorption allow structures to deform under stress without brittle failure—an increasingly critical requirement in earthquake-prone regions. Sustainability considerations also play a decisive role, as stainless steel wire rods are fully recyclable and increasingly produced from high recycled content, supporting green building certifications and circular economy objectives. Within urban construction, growing use of high-strength architectural safety meshes and tension systems highlights the material’s ability to combine structural safety with aesthetic transparency. Together, these durability, safety, and sustainability drivers position building and construction as the primary demand engine for stainless steel wire rods, sustaining its leading share in the global market.

Competitive Landscape: Global Leaders in Sustainable, High-Performance Stainless Steel Wire Rods

Competition in the stainless steel wire rods market is shaped by companies with advanced metallurgy capabilities, extensive alloy portfolios, global manufacturing footprints, and strong sustainability credentials. Leading producers differentiate through specialty duplex/super-duplex grades, cold-heading optimized rod quality, ultra-low-carbon Cr-Ni alloys, and integrated scrap-based EAF production. Their ability to deliver high-PREN wires, controlled yield-strength profiles, and custom temper-rolled conditions positions them strongly in fasteners, oil & gas, marine, aerospace, and industrial manufacturing segments.

Outokumpu Oyj - Global Benchmark in Low-Carbon Stainless Steel Production

Outokumpu remains the industry leader in decarbonized stainless steel wire rod production, utilizing over 90% recycled content and achieving a 75% lower CO₂ emission rate versus the global industry average. The company’s product portfolio includes its Ultra Range, with alloys such as Ultra 254 SMO offering PREN >27, suitable for aggressive corrosive conditions. Outokumpu also produces temper-rolled austenitic and duplex wire rod variants (e.g., Core 304L/4307) essential for high-strength fasteners and spring applications. Its strategic emphasis on low-carbon Cr-Ni grades attracts industries seeking Scope 3 emission reductions, especially in construction, marine engineering, and sustainable equipment manufacturing.

Aperam S.A. - Integrated Low-Carbon Stainless Steel Producer With Bio-Coke Advantage

Aperam differentiates itself through its integrated Brazilian operations that utilize eucalypt-based bio-coke, significantly lowering its carbon footprint and supporting its circular economic production model. With €24.3 million invested in R&D in 2024, Aperam focuses on co-developing solutions for hydrogen production infrastructure and automotive battery materials, directly contributing to energy transition markets. Its specialty alloy portfolio includes INVAR® SFD, a controlled thermal expansion alloy critical for OLED fabrication tooling. Aperam also maintains strong credentials in supplying cryogenic stainless steel for LNG storage systems, reinforcing its role in clean energy infrastructure.

Valbruna Stainless Steel - High-Capacity Producer Of Specialty Stainless and Nickel Alloy Wire Rods

Valbruna operates four major production sites across Italy, the U.S., and Canada, collectively producing approximately 200,000 tonnes of specialty steels annually. It supplies hot-rolled stainless wire rods in sizes from 5 mm to 38 mm, covering demanding applications such as aerospace fasteners, surgical instruments, and naval propulsion components. With a catalog of over 700 stainless and nickel alloy grades, including duplex, super duplex, and martensitic steels, Valbruna is equipped to serve markets requiring extreme heat resistance, high corrosion resistance, and precision alloy performance.

Walsin Lihwa - Strategic Southeast Asian Expansion For 300-Series Stainless Wire Rods

Walsin Lihwa’s USD 9.15 million investment in November 2024 established a major new 300,000-tonne stainless steel wire rod facility in Indonesia, strengthening its influence across Southeast Asia’s fast-growing manufacturing economies. The facility’s production of 300-series austenitic grades (notably 304 and 316) targets welding consumables, food-processing equipment, and general industrial fabrication markets. Leveraging its expanded regional footprint, Walsin Lihwa is positioned to meet rising demand in emerging economies while providing competitive, high-quality supply to local and export markets.

India’s stainless steel wire rods market is being structurally reshaped by the third round of the Production Linked Incentive scheme (PLI 1.2), which elevates stainless long products from commodity status to strategic industrial inputs. By explicitly incentivizing austenitic and coated stainless wire rods with 4–15% benefits on incremental sales, the policy is accelerating capital deployment into energy-efficient melting, precision rolling, and downstream wire drawing. The parallel relaxation for non-BIS imports through December 2025 has temporarily eased MSME input shortages but intensified policy debate around dumping risks and long-term quality enforcement. Capacity additions-such as the new Dadri facility by Bansal Wire Industries-signal a decisive move toward solar-assisted operations and sustainable wire rod production tailored for automotive fasteners, renewable mounts, and industrial springs. Collectively, these measures are pushing India toward self-reliance while improving grade consistency for export-ready stainless wire rods.

China’s Output Stabilization and Precision Regulation Driving Grade Upgradation

China continues to anchor global volumes in stainless steel wire rods while recalibrating toward higher-value metallurgy under “precise regulation.” The 2025–2026 stabilization plan prioritizes the closure of obsolete capacity while safeguarding high-tech stainless production, enabling mills to pivot toward electronic-grade wires and specialty alloys. Despite headline production caps, resilient infrastructure demand and improving mill economics have supported wire rod pricing and profitability. Critically, Chinese producers are aligning output with 800V EV platforms and semiconductor packaging needs, where tighter tolerances and surface integrity command premiums. This dual strategy-controlled volumes with upgraded grades-keeps China competitive amid environmental constraints and trade scrutiny.

United States’ Tariff Volatility and Infrastructure Funding Creating a Demand Floor

The U.S. stainless steel wire rods market in 2025 is defined by tariff-driven price volatility and a construction rebound under federal infrastructure programs. Elevated trade barriers have re-priced imports, enabling domestic mills to prioritize corrosion-resistant wire rods for energy, transport, and industrial infrastructure supported by the Inflation Reduction Act. New capacity from entrants such as Hybar, alongside expansions by Nucor and Commercial Metals Company, is strengthening domestic availability of long products. With a significant portion of IIJA funds already committed, stainless wire components-fasteners, ties, and structural elements-benefit from a multi-year demand floor, favoring producers with flexible order mixes and rapid delivery capabilities.

European Union’s Trade Defense and Green Steel Standards Elevating Premium Grades

The EU’s stainless steel wire rods market is increasingly shaped by anti-dumping enforcement and carbon regulation. Definitive duties on hot-rolled imports protect regional producers while reinforcing investment in low-carbon, high-precision wire rod manufacturing. Strategic capex-such as capacity doubling and new blooming mills-supports tighter dimensional control and higher surface quality for automotive and renewable applications. CBAM’s transition phase is further advantaging producers with high recycled content and verified emissions performance, prompting aggressive marketing of “circular stainless steel.” This regulatory architecture favors premium duplex and austenitic wire rods over commoditized imports.

Indonesia’s Nickel-Backed Emergence as a Bypass Manufacturing Hub

Indonesia is rapidly positioning itself as a stainless wire rod production base for global manufacturers seeking tariff-efficient access to Asian and emerging markets. Inbound investments-such as new facilities approved by Walsin Lihwa-capitalize on Indonesia’s nickel advantage to produce competitive 300-series wire rods. Integrated mine-to-metal models reduce cost volatility and support exports of industrial springs, ropes, and fasteners. As trade barriers persist in the U.S. and EU, Indonesia’s role as a regional hub is strengthening.

Japan’s Materials DX and High-Purity Wire Leadership

Japan maintains a technology-led edge through Materials DX and ultra-fine stainless wire innovation. AI-enabled simulation of crystal growth is improving defect control in large-diameter and ultra-fine wire rods for aerospace and precision machinery. Producers are pairing DX with EAF modernization and carbon-neutral pathways to sustain margins in high-purity segments. Nippon Steel Corporation’s multi-track strategy emphasizes sophisticated order mixes and equipment upgrades, reinforcing Japan’s position as a premium exporter of stainless steel long products.

National Strategic Development Matrix: Stainless Steel Wire Rods Market (2025)

Stainless Steel Wire Rods Market Development Matrix by Country

|

Country / Region

|

Primary Policy or Driver

|

Key 2025 Development

|

Strategic Focus

|

|

India

|

PLI 1.2 & quality controls

|

Incentives for stainless long products; capacity expansion

|

Import substitution, sustainable wire rods

|

|

China

|

Precise regulation

|

Output stabilization with grade upgradation

|

Electronic-grade & EV-ready wires

|

|

United States

|

Tariffs & infrastructure

|

New mills and IIJA demand commitments

|

Corrosion-resistant infrastructure wires

|

|

European Union

|

Anti-dumping & CBAM

|

Duties and green steel investments

|

Low-carbon premium wire rods

|

|

Indonesia

|

Nickel integration

|

New wire rod facilities for exports

|

Cost-competitive 300-series rods

|

|

Japan

|

Materials DX

|

AI-driven defect reduction & EAF upgrades

|

High-purity, ultra-fine wires

|

Stainless Steel Wire Rods Market Report Scope

Stainless Steel Wire Rods Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$2.7 Billion

|

|

Market Size (2035)

|

$4.2 Billion

|

|

Market Growth Rate

|

4.4%

|

|

Segments

|

By Grade (200 Series, 300 Series, 400 Series, Duplex Series), By Size (Small, Medium, Large), By Application (Fasteners, Wire Ropes, Welding Consumables, Springs, Electrodes), By End-Use Industry (Automotive & Transportation, Building & Construction, Medical & Pharmaceutical, Energy & Power)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

ArcelorMittal, Tsingshan Holding Group, Jindal Stainless Limited, Marcegaglia, Aperam S.A., Nippon Steel Corporation, POSCO Holdings Inc, Acerinox S.A, Walsin Lihwa Corporation, Bansal Wire Industries Ltd, Fagersta Stainless AB, Shagang Group, Evraz PLC, Gerdau S.A, Venus Wire Industries Pvt Ltd

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Stainless Steel Wire Rods Market Segmentation

By Grade

- 200 Series

- 300 Series

- 400 Series

- Duplex Series

By Size

By Application

- Fasteners

- Wire Ropes

- Welding Consumables

- Springs

- Electrodes

By End-Use Industry

- Automotive & Transportation

- Building & Construction

- Medical & Pharmaceutical

- Energy & Power

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Stainless Steel Wire Rod Market

- ArcelorMittal

- Tsingshan Holding Group

- Jindal Stainless Limited

- Marcegaglia

- Aperam S.A.

- Nippon Steel Corporation

- POSCO Holdings Inc

- Acerinox S.A

- Walsin Lihwa Corporation

- Bansal Wire Industries Ltd

- Fagersta Stainless AB

- Shagang Group

- Evraz PLC

- Gerdau S.A

- Venus Wire Industries Pvt Ltd

*- List not Exhaustive