Market Overview: Advanced Flat-Rolled Steel Shifts Toward Ahss Metallurgy, Zn-Al-Mg Coatings & Low-Carbon Eaf/H₂ Steelmaking

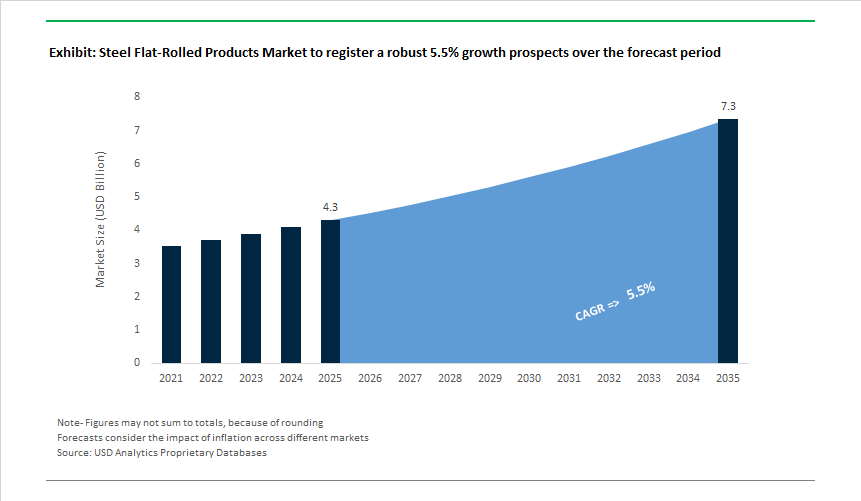

The Steel Flat-Rolled Products Market, valued at USD 4.3 billion in 2025, is expected to reach USD 7.3 billion by 2035 (CAGR 5.5%) as major global mills shift toward automotive-grade AHSS, Zn-Al-Mg corrosion-resistant coated sheet, and low-carbon flat steel produced through EAF and hydrogen-assisted reduction routes. Demand is being shaped by OEM requirements for steels with high strength-ductility combinations (25-45 GPa·%), ultra-stable yield strengths across large coil widths, and bake-hardening increments (BH20-BH40 MPa) that remain consistent after forming, painting, and curing-capabilities actively promoted by manufacturers such as ArcelorMittal (Usibor®, Fortiform®), Nippon Steel (NEXSTEEL™, ZAM®), POSCO (Giga Steel), SSAB (Docol®) and Voestalpine (phs-ultraform®).

In coated flat steel, manufacturers are commercializing Zn-Al-Mg alloys (ZAM®, MagiZinc®, PosMAC) delivering 10-20× higher corrosion resistance than conventional zinc galvanizing, particularly in C5 marine and industrial atmospheres. Automotive and construction buyers increasingly specify these coatings for undercarriage parts, battery enclosures, guard rails, solar structures, and prefabricated buildings, where extended service life and reduced maintenance are quantifiable ROI metrics. Parallel advances in continuous annealing and galvanizing lines (CGLs) allow mills to run dual-phase, TRIP, complex-phase and martensitic steels with precision thermal profiles, enabling thinner gauges (<0.8 mm) with tight flatness control required for BIW (body-in-white) assemblies, EV motors, and stamped structural parts.

Decarbonization is now a core competitive differentiator. Producers such as SSAB (HYBRIT hydrogen-reduced iron), ArcelorMittal (DRI-EAF transition), Nucor (scrap-EAF with renewable power), Tata Steel (HISarna pilot) and Salzgitter (SALCOS hydrogen program) are reshaping the supply landscape by offering low-CO₂ coil products, some achieving <0.6 tCO₂/t crude steel. OEM procurement teams increasingly treat CO₂ intensity as a purchasing criterion, creating clear market advantages for mills that can certify EAF-based flat-rolled products with >75-95% scrap input.

Market Analysis: Capacity Moves, Decarbonisation Projects and Consolidation Shape the Long-Term Market Outlook

The flat-rolled market experienced a flurry of strategic activity reflecting capacity expansion, decarbonization milestones and industry consolidation. In September 2024, Baosteel (China Baowu) announced an aggressive export expansion strategy aiming to grow annual exports to 10 million tonnes by 2028, signaling intensified competition in Southeast Asia and the Middle East for high-end flat sheets. Following that, November 2024 saw major investments including Walsin Lihwa’s approval of a new stainless wire-rod plant in Indonesia and Marcegaglia Fagersta’s €116.77 million program to double stainless output, underscoring supply-side scaling in both stainless and carbon flat products.

During 2025 the market pivoted further toward low-carbon steelmaking and vertical integration. February 2025 marked POSCO Holdings’ inauguration of its Hydrogen Reduction Steelmaking Development Center, formalizing a strategic commitment to the HyREX route for near-zero CO₂ steel-a development that directly impacts long-term availability of green flat rolled coils. May 2025, Tata Steel’s board approved funds to design a 2.5 MTPA thin slab caster and rolling facility in Meramandali, scaling thin-gauge flat product capacity for automotive and appliance markets. July 2025 was notable for Algoma Steel achieving “First Arc and First Steel” from a new EAF Unit One, demonstrating the industry’s practical shift from BF-BOF to EAF routes for hot-rolled product decarbonization. Consolidation trends also accelerated in 2025: October 2025 saw the Ryerson-Olympic Steel merger announced to secure distribution efficiencies and flat-coil inventory optimisation, while December 2025 recorded Steel Dynamics’ acquisition of the remaining stake in New Process Steel, expanding value-added service center reach.

Steel Flat-Rolled Products Market: Trends and Opportunities

Ultra-High-Strength Flat-Rolled Steels Become the Backbone of EV Structural Safety

Automotive electrification has shifted flat-rolled steel from a cost-optimized commodity to a safety-critical engineering material, particularly for battery enclosures, crash rails, and underbody structures. As global EV volumes scale in 2025, OEMs are standardizing Advanced High-Strength Steel (AHSS) and Press-Hardened Steel (PHS) grades that deliver exceptional strength-to-weight ratios while preserving formability. High-temperature performance is a decisive differentiator: 2025 product disclosures from Outokumpu (Forta H-Series) show that high-performance austenitic flat products retain structural integrity at ~1250°C for over 10 minutes—a critical threshold during thermal runaway events where aluminum fails within minutes at ~600°C.

Mechanical benchmarks are tightening in parallel. OEM specifications increasingly require ≥1000 MPa yield strength (Rp0.2) for flat-rolled components. Engineering data from SSAB (Docol® AHSS) demonstrate that upgrading truck frames from ~827 MPa to 1100 MPa martensitic steel can cut ~90 kg per vehicle—directly translating into higher payloads for electrified heavy transport. Formability has kept pace: WorldAutoSteel reports that commercially available AHSS grades nearly doubled from 2017 to 2025, enabling complex deep-drawn battery floor shells with fewer welds, lower clean-room costs, and improved dimensional consistency.

Low-CO₂, EAF-Centric Flat-Rolled Production Accelerates Under Carbon Regulation

Decarbonization has become a balance-sheet imperative as carbon pricing and border measures reshape competitiveness in flat-rolled steel. The EU’s CBAM and China’s ETS are catalyzing a structural pivot from blast furnaces to Electric Arc Furnaces (EAFs) paired with hydrogen-ready Direct Reduced Iron (DRI). In July 2025, Tata Steel UK broke ground on a new EAF at Port Talbot—a £1.25 billion transformation supported by a £500 million UK government grant—targeting a ~90% emissions reduction (≈5 Mt CO₂ annually) by 2027.

China’s inclusion of steel in its national ETS in April 2025 has similarly unlocked DRI investments totaling ~6 Mtpa in the first wave, structurally linking emissions intensity to operating costs. Energy sourcing is reinforcing the shift: industrial gas and power agreements indicate that ~61% of electricity feeding low-carbon flat-rolled production in 2025 comes from renewables (hydro, biomass, wind), exemplified by collaborations such as Linde with Salzgitter. The result is a widening competitive moat for producers that can deliver certified low-CO₂ coils and plate at scale.

Thick-Gauge Plate and Coil Demand Surges with Offshore Wind “Gigantification”

Government-mandated offshore wind targets are creating a durable, high-volume pull for thick-gauge flat-rolled plate used in monopiles and transition pieces. As turbine ratings climb to 12–15 MW, foundations are scaling to >70 m lengths and ~10 m diameters, demanding plates with stringent through-thickness (Z-direction) properties to prevent lamellar tearing under cyclic marine loads. Near-term volume is concentrated in shallow waters (0–30 m), where standardized monopile designs remain the most cost-effective—representing a rapid uptake opportunity for domestic plate producers.

Policy visibility underpins demand. India’s Ministry of New and Renewable Energy has identified 16 offshore zones off Gujarat and Tamil Nadu with ~71 GW potential, setting up multi-decade requirements for high-weldability structural plate. Across Europe, expanded Green Deal targets are reinforcing similar procurement pipelines, favoring mills that can consistently supply ultra-thick plate with marine-grade toughness and fatigue performance.

High-Strength Flat-Rolled Steel Reclaims Ground in Electrified Heavy Transport

Freight electrification is triggering a reassessment of trailer and chassis materials. While aluminum once dominated weight-reduction strategies, AHSS flat-rolled products are regaining share due to superior stiffness, durability, and lower lifecycle emissions—especially when produced via EAF routes. Manufacturers report that AHSS components can be formed on existing cold-forming lines with minor tooling upgrades, making them 20–30% more cost-effective than aluminum or CFRP while meeting legal axle limits.

Design innovation is amplifying value. Complex Phase (CP) and Martensitic (M) grades are being deployed in dual-wall shell architectures that integrate thermal management directly into battery enclosure skins, improving torsional stiffness and fatigue life. Market signaling is also evolving: in 2025, Asian buyers began recognizing “green premiums” for flat-rolled steel below 1.6 t CO₂/t steel (often labeled “5-star”), enabling producers of sustainable coils and plate to command higher margins in automotive and heavy transport supply chains.

Market Share Analysis: Steel Flat-Rolled Products Market

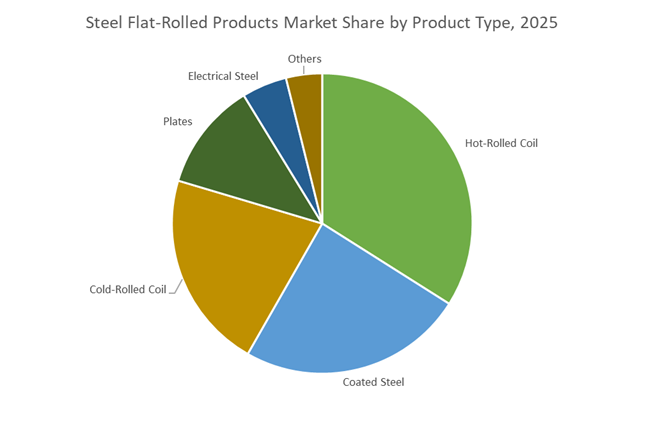

Market Share by Product Type: Hot-Rolled Coil (HRC) Remains the Structural Backbone of Flat Steel Demand

Hot-Rolled Coil (HRC) accounts for approximately 35% of the global Steel Flat-Rolled Products Market, reflecting its role as the foundational input for structurally intensive and cost-sensitive steel applications. HRC dominates because it delivers the most compelling cost-to-strength equation among flat-rolled products, driven by a streamlined production route that avoids the additional processing, annealing, and surface finishing steps required for cold-rolled or coated steels. Produced above the recrystallization temperature, HRC offers superior ductility and formability, enabling fabricators to bend, weld, and shape large sections with minimal risk of cracking or distortion. Modern HRC grades now achieve tensile strengths in the 450–550 MPa range, allowing their use in load-bearing beams, heavy equipment frames, and automotive chassis where structural resilience outweighs surface aesthetics. Thickness versatility further reinforces market share, as HRC is available across a wide gauge spectrum, with thicker coils dominating demand due to their unmatched load-bearing capacity in heavy fabrication. Lower residual stress compared to cold-worked steel improves dimensional stability during cutting and welding, reducing rework and fabrication losses. Collectively, these economic and mechanical advantages position HRC as the default flat-rolled steel choice for volume-driven, structurally critical applications, anchoring its leading share in the global market.

Market Share by End-User Industry: Building and Infrastructure Drive Sustained Consumption of Flat-Rolled Steel

The building and infrastructure sector represents roughly 35–40% of total demand in the Steel Flat-Rolled Products Market, making it the largest and most stable end-user segment. This dominance is driven by accelerating urbanization, high-rise construction, and large-scale infrastructure investments that prioritize structural efficiency, durability, and lifecycle cost control. Hot-rolled flat products are integral to pre-engineered buildings, bridges, transit systems, and modular construction, where high-strength steels enable material weight reductions without compromising safety margins—lowering foundation loads and speeding up on-site assembly. Market share is further reinforced by the sector’s growing focus on sustainable construction, as flat-rolled steel is fully recyclable and increasingly produced with higher recycled content, supporting green building certifications and public-sector procurement standards. In long-life infrastructure assets, weathering flat-rolled steels are gaining traction for their ability to minimize maintenance over multi-decade service periods, improving total cost of ownership. Seismic performance also plays a decisive role, as the high elongation characteristics of quality flat-rolled steel allow structures to absorb and dissipate energy during earthquakes rather than failing abruptly. Together, these structural, economic, and sustainability drivers make building and infrastructure the primary demand engine for steel flat-rolled products, sustaining its dominant market share globally.

Competitive Landscape: Strategic Product Lines, Hyrex R&D and EAF Scaling

Global competition in flat-rolled steel centers on companies that combine high-performance metallurgy (AHSS, ultra-high strength grades), advanced coating and finishing (CGL, Zn-Al-Mg, ZAM®), and credible decarbonization roadmaps (EAF, hydrogen reduction). Buyers prioritize suppliers that guarantee tight tensile/yield tolerances, proven corrosion protection, and validated low-carbon credentials. The following company deep dives highlight product focus, decarbonisation initiatives, capacity plays and market positioning relevant to OEM procurement teams and material engineers.

Arcelormittal - Expanding Xcarb® and HSS Capability While Scaling European EAF Output

ArcelorMittal is accelerating its low-carbon flat-rolled offering through XCarb® branded green-steel and investments to raise European EAF share from 19% to 28% via projects in Gijón and Dunkirk. Its Usibor® hot-stamped product family remains a core offering for automotive safety cages, while the company’s integrated approach delivers cost control (EBITDA/tonne of ~$125 H1 2025) and scale for premium coated and hot-rolled coils. ArcelorMittal’s emphasis on EAF and XCarb® positions it to serve automakers and infrastructure clients seeking verifiable low-carbon flat products and high-strength stamped sheet solutions.

POSCO Holdings - Giga Steel Leadership and Hydrogen Reduction R&D For Green Flat Products

POSCO operates large-scale capacity for its Giga Steel ultra-high-strength product (≈1 Mtpa capability) and markets PosMAC coated steel (Zn-Al-Mg) for superior corrosion resistance. Its Feb 2025 Hydrogen Reduction Steelmaking Development Center underpins HyREX R&D to commercialize hydrogen-reduced flat products. POSCO’s combination of patented high-strength alloys and coating technology targets EV structural applications and long-life infrastructure components that demand both strength-to-weight performance and low lifecycle carbon.

China Baowu (Baosteel) - Volume Leadership With Export Push and EAF Transition Goals

China Baowu remains volume-dominant and has signaled a strategic pivot toward global market share growth by targeting 10 Mtpa exports by 2028 while committing to increase EAF production share to 50% by 2030. Baosteel’s capacity and export strategy affect regional pricing and supply availability of hot-rolled and coated flat products, especially in Asia-Pacific and MENA. For procurement teams, Baosteel’s scale offers supply security but also introduces trade policy sensitivity given regional anti-dumping measures.

Tata Steel - India Growth Engine With Thin-Slab and HRPGL Investments For Domestic Auto Supply

Tata Steel is prioritizing value-added flat production with significant capital allocations (~USD 2.04B FY24/25), including a 0.7 MTPA HRPGL and planning a 2.5 MTPA thin slab caster and rolling facility at Meramandali to serve domestic automotive and appliance markets. Its Kalinganagar expansion and cold-rolling capacity build align with India’s import-substitution and electrification roadmaps, making Tata a strategic supplier for OEMs targeting localized, high-quality flat-rolled coils. Tata’s repeated recognition as a Steel Sustainability Champion highlights its ESG and low-carbon positioning for regional buyers.

Nippon Steel - Coating Innovation and Ultra-High Tensile Flat Products For Advanced Applications

Nippon Steel combines specialized coatings (ZAM® zinc-aluminum-magnesium self-repairing layers) with ultra-high-strength flat sheet grades up to 1,470 MPa for advanced automotive and industrial uses. The company’s low Ceq alloy designs and HTUFF™ weldability technologies enable heavy-duty, weldable plates and high-tensile sheets with superior HAZ toughness-attributes critical for demanding welded structures and safety components. Nippon Steel’s focus on high-performance, coated flat products makes it a preferred partner for customers requiring extreme corrosion resistance and formability at high tensile levels.

The United States steel flat-rolled products market is in a decisive recapitalization phase, driven by IRA-linked incentives and corporate balance-sheet strength aimed at high-value automotive and energy applications. By 2025, domestic producers are prioritizing advanced high-strength steels (AHSS), premium hot-rolled coil (HRC), and coated flat products to support EV platforms and infrastructure rebuilds. U.S. Steel has committed a long-cycle $14 billion growth plan, including capacity restarts and targeted efficiency investments that restore domestic supply optionality. The Granite City blast furnace restart reflects confidence in multi-year HRC demand, while plant-level upgrades sharpen cost competitiveness. Parallel capital markets activity by Steel Dynamics underpins the ramp-up of its Sinton flat-roll division, reinforcing the U.S. strategy of pairing re-shoring with low-carbon process modernization. Together, these moves create a protected pricing environment supported by tariffs and “Buy Clean” procurement, elevating margins for domestic flat-rolled producers.

China: Quality-and-Efficiency Pivot Ahead of the 15th Five-Year Plan

China’s flat-rolled strategy is transitioning from scale to specification. Under the tail end of the 14th Five-Year Plan, output is being redirected toward silicon steel, non-oriented electrical steel, and premium cold-rolled grades for EV motors and high-efficiency appliances. A two-year MIIT action plan (2025–2026) restricts new capacity while incentivizing hydrogen metallurgy and specialty steel, signaling a durable capex discipline. The result is a rising share of manufacturing-grade steel within total output and rapid gains in high-end flat products. This policy mix-capacity restraint plus technology upgrading-positions China to defend margins domestically while preparing export offerings aligned to tighter environmental thresholds.

India: PLI 1.2 Accelerating Atmanirbhar Flat-Rolled Capabilities

India’s flat-rolled market is being reshaped by Production Linked Incentive (PLI 1.2) mechanics that reward incremental output in CRGO, coated sheets, and AHSS. With a ₹6,322 crore outlay and cumulative investments exceeding ₹43,874 crore across earlier tranches, the program is converting policy intent into operating capacity. Deployed capital is translating into cold-rolling, galvanizing, and specialty coating lines that reduce import dependence and improve quality compliance for automotive and electrical steel. The emphasis on CRGO aligns with grid modernization and EV charging, while incentive bands of 4–15% catalyze faster scale-up. India’s trajectory is toward integrated flat-rolled ecosystems that balance cost, quality, and localization.

European Union: CBAM-Backed Green Flat Steel and Scrap Circularity

The EU’s flat-rolled market is governed by carbon discipline. CBAM’s transition phase and the 2025 Steel Dialogue Action Plan combine trade defense with decarbonization funding-€150 million from RFCS and a €1 billion pilot auction to electrify processes. Anti-dumping duties on hot-rolled imports reinforce price stability as producers pivot toward EAF-based, near-zero-carbon sheets. A growing pool of high-quality scrap (20–40 Mt annually) accelerates the shift from blast furnaces, favoring coated and advanced grades with verified low embedded emissions. Europe’s approach elevates compliance-led differentiation over volume growth.

South Korea: Financial Restructuring and High-Grade Share Expansion

South Korea is stabilizing its flat-rolled sector through targeted liquidity and technology programs. A KRW 400 billion support package-coordinated with POSCO and policy banks-lowers financing costs while a KRW 200 billion roadmap funds ten new specialized carbon steel grades by 2030. The objective is to lift high-grade steel to 20% of national output and cut lifecycle emissions by ~30%. This twin focus on solvency and specialization protects export competitiveness amid import pressure.

Brazil: Import Surge Forcing Defensive Realignment

Brazil’s flat-rolled market is confronting record import penetration, with 2025 inflows projected at 5.7 Mt (≈21% of consumption). Price premiums for domestic HRC peaked mid-year, compressing margins and triggering production pullbacks. With crude steel output expected to decline through 2026, mills are reassessing pricing discipline and lobbying for trade remedies. Brazil’s near-term outlook hinges on balancing affordability with capacity utilization as global oversupply tests domestic resilience.

Strategic National Development Matrix: Steel Flat-Rolled Products (2025)

Steel Flat-Rolled Products Development Matrix by Country

|

Country/Region

|

Primary Strategic Driver

|

2025 Anchor Actions

|

Flat-Rolled Focus

|

|

United States

|

Re-shoring & IRA incentives

|

$14B modernization; furnace restart; Sinton ramp

|

AHSS, HRC, coated sheets

|

|

China

|

Quality & efficiency pivot

|

Capacity restraint; hydrogen metallurgy

|

Electrical steel, premium CR

|

|

India

|

PLI 1.2 localization

|

₹6,322 cr incentives; CRGO priority

|

CRGO, coated flats

|

|

European Union

|

CBAM & green steel

|

RFCS funding; anti-dumping

|

Low-carbon EAF flats

|

|

South Korea

|

Financial stabilization

|

KRW 400 bn support; grade roadmap

|

High-grade carbon steels

|

|

Brazil

|

Trade defense under pressure

|

Import surge response; output cuts

|

HRC pricing discipline

|

Steel Flat-Rolled Products Market Report Scope

Steel Flat-Rolled Products Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$4.3 Billion

|

|

Market Size (2035)

|

$7.3 Billion

|

|

Market Growth Rate

|

5.5%

|

|

Segments

|

By Product Type (Hot-Rolled Coils & Sheets, Cold-Rolled Coils & Sheets, Coated Steel, Plates, Strips, Electrical Steel Sheets), By Material Grade (Carbon Steel, Alloy Steel, Stainless Steel, Tool Steel), By Production Process (BF-BOF, EAF, DRI-EAF), By End-User Industry (Automotive & Transportation, Building & Infrastructure, Industrial Machinery & Equipment, Home Appliances, Energy, Packaging, Defense & Aerospace)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

China Baowu Steel Group Corporation, ArcelorMittal S.A., Ansteel Group Corporation, Nippon Steel Corporation, POSCO Holdings Inc., HBIS Group Co., Ltd., Tata Steel Limited, JSW Steel Limited, Jiangsu Shagang Group Co., Ltd., JFE Steel Corporation, United States Steel Corporation, Nucor Corporation, Steel Authority of India Limited, Jindal Steel & Power Limited, Cleveland-Cliffs Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Steel Flat-Rolled Products Market Segmentation

By Product Type

- Hot-Rolled Coil and Sheets

- Cold-Rolled Coil and Sheets

- Coated Steel

- Plates

- Strips

- Electrical Steel Sheets

By Material Grade

- Carbon Steel

- Alloy Steel

- Stainless Steel

- Tool Steel

By Production Process

- Blast Furnace–Basic Oxygen Furnace

- Electric Arc Furnace

- Direct Reduced Iron–Electric Arc Furnace

By End-User Industry

- Automotive and Transportation

- Building and Infrastructure

- Industrial Machinery and Equipment

- Home Appliances

- Energy

- Packaging

- Defense and Aerospace

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Steel Flat-Rolled Products Market

- China Baowu Steel Group Corporation

- ArcelorMittal S.A.

- Ansteel Group Corporation

- Nippon Steel Corporation

- POSCO Holdings Inc.

- HBIS Group Co., Ltd.

- Tata Steel Limited

- JSW Steel Limited

- Jiangsu Shagang Group Co., Ltd.

- JFE Steel Corporation

- United States Steel Corporation

- Nucor Corporation

- Steel Authority of India Limited

- Jindal Steel & Power Limited

- Cleveland-Cliffs Inc.

*- List not Exhaustive