Sterols Market Valuation 2025–2034: $3.4 Billion to $6.7 Billion at 7.8% CAGR Driven by Phytosterol Nutrition, Functional Foods, and Supply Chain Integration

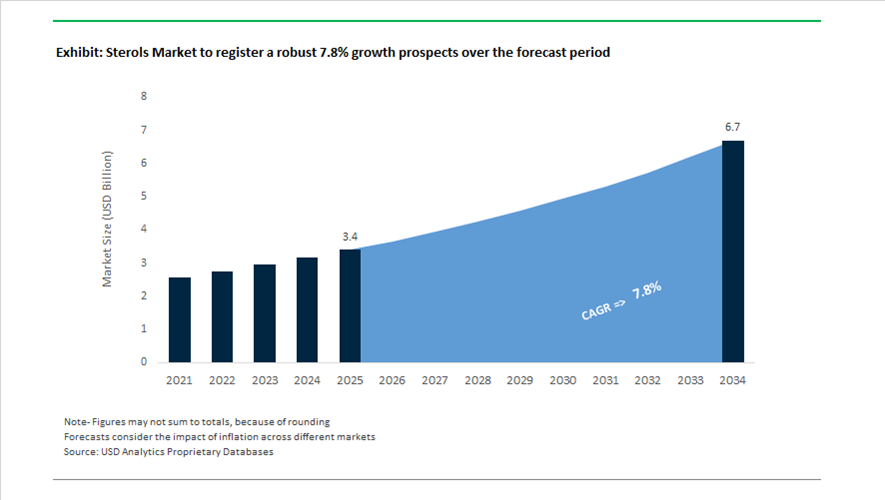

The global sterols market is valued at $3.4 billion in 2025 and is projected to reach $6.7 billion by 2034, expanding at a CAGR of 7.8%. Growth is fueled by rising demand for plant sterols, phytosterols, phytostanols, stigmasterol derivatives, and sterol-based functional ingredients used in cholesterol-lowering foods, dietary supplements, pharmaceutical intermediates, and fortified dairy alternatives. Increasing cardiovascular disease awareness, regulatory endorsement of sterol health claims, and expansion of functional food portfolios across Asia-Pacific and Europe are accelerating adoption. Manufacturers are strengthening vertically integrated oilseed extraction systems to secure phytosterol feedstocks from rapeseed, sunflower, and soybean refining streams while investing in high-purity sterol processing for pharmaceutical and nutraceutical applications.

Strategic portfolio realignment reshaped the market in 2024 and early 2025. In December 2024, BASF signed a binding agreement to divest its Food & Health Performance Ingredients business, including plant sterol production at its Illertissen site in Germany, to Louis Dreyfus Company. The transaction, progressing through 2025, marks BASF’s exit from non-core human nutrition while enabling LDC to diversify into value-added plant-based sterol ingredients. In late 2024, Kensing LLC completed the acquisition of Advanced Organic Materials, strengthening its global phytosterol and natural vitamin E portfolio derived from non-GMO rapeseed and sunflower oils. In February 2025, ADM announced a $500–$750 million cost optimization initiative focused on aligning its Nutrition segment with long-term health and wellness growth, reinforcing sterol-based product development. In May 2024, ProBiotix Health introduced the CholBiome® CH bi-layer cholesterol management tablet combining Lactobacillus plantarum LPLDL with plant sterols and stanols, demonstrating innovation in synbiotic sterol delivery systems.

Innovation in formulation science and regional expansion accelerated through 2025 and 2026. In April 2025, Cargill inaugurated its transformed Innovation Center in Singapore to advance sterol-fortified dairy alternatives and functional snack applications tailored for Asian health profiles. In December 2025, peer-reviewed research confirmed that incorporating resveratrol into liposomal systems significantly enhances the thermal stability of stigmasterol, enabling broader use of sterols in high-temperature food processing environments. In late 2025, the Raisio Research Foundation funded a heart-health professorship at the University of Helsinki to strengthen clinical evidence supporting plant stanol efficacy. In January 2026, Cargill announced expansion of its Beijing manufacturing site to meet rising demand for high-purity nutritional ingredients, including sterol-enriched functional fats. In the same month, Cargill received the 2026 BIG Innovation Award recognizing advancements in functional fats incorporating heart-healthy sterol technologies. Following consolidation of PZ Wilmar shares in 2025, Wilmar International intensified integration of phytosterol extraction within its global oilseed crushing operations, reinforcing supply chain stability for pharmaceutical and nutraceutical sectors. These divestitures, acquisitions, clinical research milestones, and manufacturing expansions are redefining competitive dynamics in the sterols market through 2034.

Structural Demand Shifts and High-Value Opportunities in the Sterols Market

Mainstream Fortification Enabled by Heart-Health Regulatory Validation

The Sterols Market has moved decisively from niche nutraceutical positioning into mass-market food and beverage fortification, driven by regulatory clarity and standardized health claims. Scientific validation by the European Food Safety Authority and the U.S. Food and Drug Administration confirming that daily intake levels of 1.5 g to 3.0 g of plant sterols can reduce LDL cholesterol by 7% to 12.5% has transformed sterols into a strategic functional ingredient for everyday consumption categories. This regulatory leverage allows Consumer Packaged Goods manufacturers to embed sterols into high-frequency consumption products such as milk, yogurt, drinkable dairy, and functional beverages rather than relying on episodic supplement usage.

Commercial execution accelerated in late 2024 when Kensing introduced Sunvasterol®, an upcycled sunflower-derived phytosterol platform, at Food Ingredients Europe. The product followed a landmark EFSA novel food approval, granting Kensing commercial exclusivity in Europe for this non-GMO and allergen-free sterol source. This approval has materially lowered formulation risk for dairy and plant-based beverage manufacturers seeking clean-label cholesterol-lowering claims. Parallel clinical developments have further reinforced demand. Research published in 2025 on the Dietary Portfolio Approach demonstrated that combining plant sterols with fiber-rich, low-fat diets can achieve LDL reductions approaching 30%, comparable to entry-level statin therapy. This evidence has catalyzed the adoption of the Cholesterol-Lowering Capacity Index as a standardized benchmarking tool, enabling food brands, healthcare professionals, and regulators to quantify the clinical relevance of sterol-fortified products in preventive nutrition strategies.

Shift Toward Sustainable, Non-GMO, and Upcycled Sterol Feedstocks

Sustainability disclosure requirements are now directly influencing sterol sourcing strategies. Under the EU Corporate Sustainability Reporting Directive, sterol producers and downstream CPG brands are under pressure to demonstrate traceable, low-impact supply chains, accelerating the move away from genetically modified soy toward identity-preserved sunflower oil, pine tree tall oil, and other upcycled lipid streams. This transition is no longer optional, as sterols increasingly contribute to Scope 3 emissions profiles for large food and personal care companies.

Supply chain realignment is evident in the strategic disclosures of major agribusiness players. Cargill, in its 2025 Impact Report, outlined commitments to eliminate deforestation across agricultural inputs by 2030, a policy that directly affects sterol extraction from vegetable oils. As a result, branded food manufacturers are demanding full traceability and non-GMO certification for phytosterols used in functional products. At the same time, portfolio rationalization is reshaping competitive dynamics. In September 2025, BASF completed the divestment of its Food and Health Performance Ingredients business to Louis Dreyfus Company, enabling LDC to vertically integrate sterol esters into its global oilseed value chain. This shift reflects a broader industry trend toward fewer, larger suppliers capable of delivering high-purity sterols with verifiable sustainability credentials at global scale.

High-Purity Sterol Intermediates for Bio-Based Pharmaceutical Steroids

A structurally attractive opportunity is emerging at the intersection of sterols and pharmaceutical manufacturing. Sterols such as stigmasterol and diosgenin form the molecular backbone for corticosteroids, hormone therapies, and vitamin D analogs, positioning them as critical intermediates in API synthesis. As the pharmaceutical industry increasingly adopts green chemistry principles, demand is rising for sterol intermediates that can support enzyme-catalyzed biotransformation routes. These processes can reduce solvent usage and energy consumption by up to 40% compared with traditional multi-step chemical synthesis, making sterols strategically relevant beyond nutrition.

With the pharmaceutical intermediates market valued at approximately $29.2 billion in 2025, sterol suppliers are investing in advanced extraction, purification, and crystallization technologies to achieve pharmaceutical-grade purity exceeding 99%. Companies such as ADM and Arboris are expanding capacity to serve biopharma customers developing next-generation anti-inflammatory and hormone-regulating therapies. This segment offers structurally higher margins than food-grade sterols, supported by long qualification cycles, regulatory lock-in, and multi-year supply agreements with API manufacturers.

Sterol-Based Emulsifiers for Texture Engineering in Plant-Based Foods

The evolution toward Plant-Based 2.0 formulations has exposed limitations in texture, mouthfeel, and emulsion stability across meat and dairy alternatives. Sterols are emerging as a multifunctional solution due to their amphiphilic structure, enabling them to act as crystallization modifiers and emulsion stabilizers within plant-derived fat systems. This functionality directly addresses one of the most cited consumer complaints in plant-based milk alternatives and meat analogs, namely phase separation, oil-out, and inconsistent sensory performance.

Academic and industry research published in early 2025 highlighted that emulsion instability remains a primary technical bottleneck for plant-based beverages. Sterols are now being evaluated as lipid-structuring agents that stabilize vegetable oil emulsions while extending shelf life without synthetic emulsifiers. At the 2025 Bridge2Food Summit, formulators presented application data showing that sterol esters can precisely tune the melting behavior of coconut and sunflower oil blends in plant-based burgers. By controlling fat crystallization kinetics, these systems prevent premature oil leakage during cooking and deliver improved juiciness, bite, and mouth-coating perception. As plant-based brands shift focus from simple substitution toward sensory parity with animal products, sterol-based emulsifiers represent a high-value growth avenue within the Sterols Market.

Sterols Market Share and Segmentation Insights

Phytosterols Dominate the Sterols Market Driven by Cholesterol-Lowering Functional Ingredient Demand

Phytosterols accounted for 58.60% of the sterols market in 2025, positioning plant sterols as the most commercially significant sterol category in functional nutrition and nutraceutical formulations. Their dominance is linked to strong clinical evidence supporting cholesterol reduction and cardiovascular health benefits, combined with regulatory health claim approvals across major markets including the US, EU, and Asia. Phytosterols are widely produced from vegetable oil deodorizer distillates, ensuring scalable supply for food and supplement applications. The 2025 growth catalyst is the regulatory health claim expansion, which has enabled manufacturers to incorporate phytosterols into functional foods such as yogurts, spreads, fortified juices, and dietary capsules, increasing consumer adoption in cholesterol management products.

Dietary Supplements Lead Sterols Market Consumption Through Heart Health Formulations

Dietary supplements accounted for 42.80% of the sterols market in 2025, making them the largest application segment due to strong consumer demand for natural cholesterol management solutions. Phytosterol-based supplements provide targeted dosing convenience, allowing consumers to achieve clinically recommended intake levels of approximately 2 grams per day without significant dietary changes. The supplement format also supports high-concentration delivery through capsules, tablets, and softgels, which are widely used in preventive health products. The 2025 market trend is the rapid growth of multi-ingredient cardiovascular health supplements, where phytosterols are increasingly combined with omega-3 fatty acids, CoQ10, and red yeast rice, enabling premium heart health formulations with broader therapeutic positioning.

Sterols Market Competitive Landscape

The sterols market in 2026 is defined by high-purity phytosterol extraction, PCF transparency, and microencapsulation technologies. Industry leaders are shifting toward pharmaceutical-grade sterols, functional food fortification, and bio-based feedstock optimization to meet clean label and regulatory requirements across EU and North American markets.

ADM Expands High-Purity Plant Sterols Portfolio Through Nutrition Segment Growth and Global Supply Chain Integration

ADM is strengthening its sterols market position by prioritizing its Nutrition segment as a high-margin growth engine. Despite total revenues declining to $80.3 billion in 2025, the Nutrition division delivered an 8% increase in operating profit to $417 million, driven by specialty ingredients like phytosterols. The CardioAid® portfolio continues to expand into functional beverages and microbiome-enhancing formulations. ADM is optimizing its production network to focus on Health & Wellness ingredients, targeting $500–$750 million in cost savings by 2028. Its vertically integrated oilseed processing ensures consistent Non-GMO sterol feedstock supply. Strong traceability and scale support pharmaceutical-grade sterol production and global nutraceutical demand.

BASF Advances Pharmaceutical-Grade Sterols and Nanostructured Delivery Systems for Functional Nutrition Applications

BASF maintains leadership in high-purity sterols through advanced formulation technologies and integrated production systems. The company is scaling its Vegapure® phytosterol line with innovations in nanostructured lipid carriers and emulsion systems for low-fat and transparent beverage applications. Its Nutrition & Care segment is expected to deliver strong earnings growth in 2026, supported by recovery in health and personal care markets. BASF is targeting the pharmaceutical steroid intermediate segment, supplying high-purity sitosterol and stigmasterol for hormone synthesis. The "Winning Ways" strategy is driving €2.3 billion in cost optimization, with reinvestment into bio-based production at its Zhanjiang Verbund site. Its focus on high-value sterol applications strengthens its competitive positioning.

Bunge Leverages Viterra Integration to Scale Sterol Extraction and Specialty Ingredients Portfolio

Bunge is expanding its sterols footprint through large-scale integration of oilseed processing assets following the Viterra acquisition. The company captured $190 million in synergies by early 2026, optimizing sterol and tocopherol extraction from rapeseed and sunflower oils. Its Refining and Specialty Ingredients segment is a key driver of its strategy to achieve a $15 EPS baseline by 2030. The acquisition of IFF’s soy protein and lecithin business enhances its distribution channels for sterol-enriched plant-based ingredients. Bunge is prioritizing phytosterol esters for both functional foods and industrial applications such as green tire formulations. Its global logistics network supports rapid expansion across Asia-Pacific markets.

Cargill Strengthens Functional Sterol Systems with AI-Driven Extraction and Asia-Focused Expansion

Cargill is reinforcing its leadership in plant sterols through innovation and regional investment strategies. The RMB 45 million expansion of its Beijing facility enhances its ability to integrate sterols into functional food systems, including beverages and coatings. Its CoroWise® brand continues to dominate the North American heart health segment, with ongoing improvements in sterol fraction extraction using biotechnology. Recognition in the 2026 BIG Innovation Awards highlights its use of AI and predictive analytics in optimizing ingredient production. The company’s $240 million investment plan in India supports development of high-value agricultural supply chains for sterol extraction. Its global expertise combined with localized production strengthens its competitive edge.

Matrix Life Science Expands High-Purity Phytosterol Solutions with Customized Formulations and Global Distribution

Matrix Life Science is emerging as a key pure-play supplier in the sterols market, focusing on high-purity and customized phytosterol formulations. The company expanded its global presence with the establishment of Matrix Fine Sciences USA, enabling stronger North American distribution of its PhytoLite™ portfolio. The launch of PhytoLite™ Granules improves flowability for direct compression in nutraceutical tablet manufacturing. Matrix utilizes multi-source Non-GMO feedstocks, including soy, sunflower, and rapeseed, ensuring supply stability. Advanced chromatographic profiling allows the company to deliver customized sterol compositions for pharmaceutical and cosmetic applications. Its focus on precision formulation supports high-growth nutraceutical and clean label markets.

Germany Sterols Market Reconfigured by Asset Divestment and Regulatory Yield Expansion

Germany remains a pivotal hub for high-purity sterols in Europe, although its market structure shifted materially in 2025. In October 2025, BASF completed the divestment of its Food and Health Performance Ingredients business to Louis Dreyfus Company. The transaction transferred the Illertissen production site and associated plant sterol ester lines to LDC, effectively integrating European sterol capacity into a vertically aligned, plant-based ingredients platform. This move has reshaped competitive dynamics by aligning sterol extraction more closely with upstream oilseed origination and downstream nutrition markets.

Regulatory evolution has reinforced this transition. Following a scientific reassessment by the European Food Safety Authority, Regulation (EU) 2025/1509 amended phytosterol specifications for sunflower-derived inputs, increasing the allowable content of “other sterols and stanols” to below 7.0%. This change materially improves extraction economics for German processors sourcing from sunflower oil streams. In parallel, chemical hubs in the Rhine-Ruhr corridor have expanded the supply of pharmaceutical-grade beta-sitosterol for corticosteroid and progesterone intermediates, while adopting supercritical CO2 extraction to reduce VOC emissions by an estimated 35% versus hexane-based processes.

United States Sterols Market Driven by Clean-Label Nutrition and Process Innovation

The United States sterols market is increasingly shaped by functional nutrition and formulation science rather than bulk commodity extraction. In 2025, Cargill and ADM reported a 17% rise in new phytosterol-enriched product launches, particularly within heart-health positioned spreads, beverages, and fortified juices. This expansion reflects sustained consumer demand for clean-label cholesterol management solutions and effective utilization of existing FDA-authorized health claims linking phytosterols to reduced coronary heart disease risk.

Technological differentiation is emerging as a key competitive lever. ADM introduced a proprietary microencapsulation platform in late 2024 that preserves sterol bioactivity at baking temperatures approaching 200°C, enabling penetration into bakery and snack matrices previously unsuitable for sterol fortification. On the supply side, U.S. refiners have diversified away from imported soy-derived sterols, increasing reliance on tall oil fractions and corn-based feedstocks to mitigate trade volatility and strengthen domestic sourcing resilience.

China Sterols Market Anchored in Steroid Intermediates and Export Reform

China continues to dominate the global sterols value chain through its role as a primary supplier of steroid intermediates. Domestic producers consume more than 1,500 tons of crude phytosterols annually via microbial biotransformation routes to produce androstenedione and related hormone precursors, reinforcing China’s strategic position in pharmaceutical APIs. Regulatory reform has further sharpened export orientation. In November 2025, the Ministry of Agriculture and Rural Affairs introduced draft rules streamlining approvals for products registered exclusively for overseas markets, reducing administrative friction for technical-grade sterol exports.

At the same time, compliance requirements have intensified. New export control measures introduced by Ministry of Commerce of China in October 2025, while focused on sensitive materials, extended scrutiny to overseas subsidiaries under the “50% rule.” Domestically, the National Health China 2030 initiative has driven incorporation of phytosterols into blended edible oils, positioning sterols as affordable preventive nutrition inputs for urban populations facing rising hyperlipidemia rates.

India Sterols Market Supported by Fortification Policy and API Localization

India’s sterols industry is transitioning from import dependence toward integrated nutraceutical and pharmaceutical supply. Updated “Eat Right” guidelines issued by the Food Safety and Standards Authority of India in late 2025 explicitly encourage the use of plant sterols in edible oils and dairy alternatives to address cardiovascular risk. This policy endorsement has accelerated adoption across mass-market oil brands and fortified food categories.

Pharmaceutical strategy provides an additional growth axis. Under the Production Linked Incentive framework, Indian manufacturers have expanded capacity for ergosterol and stigmasterol, targeting a reduction in the country’s historical reliance on imported steroid precursors. Public health initiatives such as the “Swasth Nari, Sashakt Parivar” campaign launched in September 2025 have further stimulated demand for sterol-based preventive supplements. Feedstock localization is improving, with refiners increasingly extracting oryzanol and phytosterols from rice bran oil byproducts, enhancing cost efficiency and circularity.

Argentina Sterols Market Leveraging Sunflower Strength and Sustainability Credentials

Argentina occupies a differentiated niche in the sterols landscape through sunflower-based phytosterols. Capitalizing on its oilseed advantage, Advanced Organic Materials secured EU data protection in 2025 for proprietary sunflower sterol extraction technologies, granting five years of exclusivity and strengthening its competitive moat in Europe. Sustainability positioning reinforces this advantage. Argentine producers achieved ISCC PLUS certification in 2025 for low-carbon sterol esters, aligning exports with premium European demand for non-GMO, traceable ingredients.

Comparative Snapshot: Sterols Industry by Country

Sterols Market County Level Snapshot

|

Country

|

Structural Driver

|

Primary Sterol Focus

|

Strategic Advantage

|

|

Germany

|

Asset divestment and EU regulatory updates

|

Phytosterol esters, beta-sitosterol

|

High-purity extraction and pharma integration

|

|

United States

|

Clean-label nutrition demand

|

Phytosterols for functional foods

|

Formulation and encapsulation innovation

|

|

China

|

Steroid intermediate dominance

|

Crude phytosterols for APIs

|

Scale and biotransformation expertise

|

|

India

|

Fortification policy and PLI

|

Ergosterol, stigmasterol

|

API localization and feedstock circularity

|

|

Argentina

|

Sunflower oil leadership

|

Sunflower-derived phytosterols

|

EU data protection and sustainability certification

|

Sterols Market Report Scope

Sterols Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$3.4 Billion

|

|

Market Size (2034)

|

$6.7 Billion

|

|

Market Growth Rate

|

7.8%

|

|

Segments

|

By Product Type (Phytosterols, Phytostanols, Sterol Esters, Zoosterols, Mycosterols), By Source (Vegetable Oil Sources, Tree-Based Sources, Other Plant Sources, Microbial and Algal Sources), By Application (Food and Beverages, Dietary Supplements, Pharmaceuticals, Cosmetics and Personal Care, Animal Feed)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Archer Daniels Midland Company, Cargill, Incorporated, Louis Dreyfus Company, BASF SE, Raisio Oyj, Bunge Limited, Arboris, LLC, Kao Corporation, Matrix Life Science, Advanced Organic Materials, Xi'an Healthful Biotechnology Co., Ltd., Vitae Caps S.A., Zhejiang Garden Biochemical High-Tech Co., Ltd., Pharma Nord, Lipofoods

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Sterols Market Segmentation

By Product Type

- Phytosterols

- Phytostanols

- Sterol Esters

- Zoosterols

- Mycosterols

By Source

- Vegetable Oil Sources

- Tree-Based Sources

- Other Plant Sources

- Microbial and Algal Sources

By Application

- Food and Beverages

- Dietary Supplements

- Pharmaceuticals

- Cosmetics and Personal Care

- Animal Feed

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Sterols Industry

- Archer Daniels Midland Company

- Cargill, Incorporated

- Louis Dreyfus Company

- BASF SE

- Raisio Oyj

- Bunge Limited

- Arboris, LLC

- Kao Corporation

- Matrix Life Science

- Advanced Organic Materials

- Xi'an Healthful Biotechnology Co., Ltd.

- Vitae Caps S.A.

- Zhejiang Garden Biochemical High-Tech Co., Ltd.

- Pharma Nord

- Lipofoods

*- List not Exhaustive