Advanced Optical Performance, Smart Lenses, and Premium Durability Driving Strong Growth

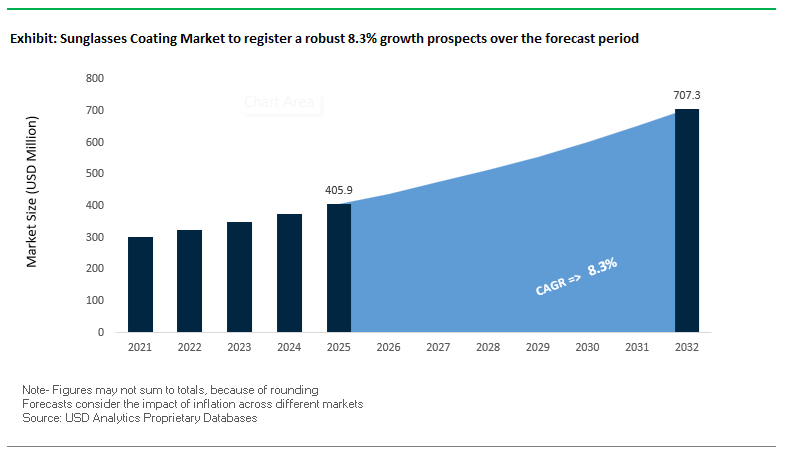

The global Sunglasses Coating Market is experiencing robust expansion, fueled by rising demand for high-performance optical solutions, premium eyewear, and multifunctional lens technologies. The market was valued at $405.9 million in 2025 and is projected to reach $709.3 million by 2032, growing at a CAGR of 8.3% during 2025–2032. This growth is driven by increasing consumer awareness of eye protection, visual clarity, and aesthetic performance, alongside rapid innovation in coating technologies that enhance both functionality and durability.

A key structural driver is the rising adoption of multi-layer coatings that combine anti-reflective (AR), anti-smudge, hydrophobic, oleophobic, scratch-resistant, and UV-protective properties. Consumers are increasingly seeking lenses that offer superior clarity, easy maintenance, and long-term durability, particularly in high-exposure environments such as sports, outdoor recreation, and driving. Additionally, the demand for blue light filtering and high-energy visible (HEV) protection is accelerating, driven by increased screen exposure and awareness of eye health.

Another major trend is the integration of smart and adaptive coatings, including photochromic and color-enhancing technologies. These coatings dynamically adjust to changing light conditions, improving user comfort and visual performance. The convergence of optics, materials science, and wearable technology is also reshaping the market, with smart glasses and AI-enabled eyewear creating new demand for specialized coatings that support sensors, displays, and enhanced user interaction.

Premiumization remains a significant growth factor, particularly in developed markets, where consumers are willing to invest in high-end coatings that offer both performance and aesthetic benefits, such as reduced lens visibility, vibrant color enhancement, and mirror durability. At the same time, expanding distribution networks in emerging markets are increasing accessibility to advanced coating technologies, further supporting market growth.

Market Analysis: CleanGuard Breakthroughs, AI-Integrated Eyewear, and Durable Mirror Technologies Reshaping Competitive Landscape

The sunglasses coating market is being transformed by innovation in surface chemistry, smart eyewear integration, and strategic distribution expansion, reflecting a shift toward high-performance and consumer-centric solutions. In January 2026, ZEISS Vision Care launched its DuraVision Plus portfolio, featuring CleanGuard technology that reduces surface energy at the molecular level. This advancement makes lenses significantly easier to clean while enhancing water repellency and smudge resistance, addressing key consumer pain points in everyday eyewear use.

Smart eyewear is emerging as a major growth frontier. EssilorLuxottica’s Oakley Meta Vanguard (September 2025 / early 2026 rollout) integrates AI capabilities with high-performance athletic coatings, targeting endurance sports and expanding into EMEA and Asian markets. These products require coatings that not only enhance vision but also support sensor integration and durability under extreme conditions.

Strategic expansion into high-growth markets is strengthening distribution channels. EssilorLuxottica’s April 2026 acquisition of a stake in Top Charoen provides direct access to Southeast Asia’s expanding optical retail market, enabling wider adoption of advanced coatings such as Crizal and Transitions.

Performance-driven innovation continues in sports and lifestyle segments. Oakley’s 2026 Tour De France™ Velo Kato™ release incorporates Prizm Road lens technology and Stealth™ Pro anti-reflective coatings, designed to minimize reflections and enhance contrast for athletes.

Durability advancements are also redefining product standards. HOYA Vision Care’s Lumacore™ Mirrors (August 2025) embed mirror coatings directly into the lens material, significantly improving scratch resistance and long-term color stability compared to traditional surface-applied coatings.

Adaptive lens technologies are gaining traction. Transitions Optical’s Color Touch™ (February 2025) and GEN S™ (late 2024 scaling) introduce next-generation photochromic systems that offer faster response times and continuous color presence, enhancing both functionality and style.

In parallel, HOYA’s Polarized HEV™ lenses (August 2025) provide advanced coatings that filter 97% of solar blue light, improving visual comfort in high-glare environments such as water and snow. Essilor’s Crizal Natural Look (September 2025) further advances anti-reflective technology by minimizing visible lens reflections while maintaining high levels of scratch and smudge resistance.

Collaborations are also shaping specialized applications. Safilo Group’s Carrera | Ducati partnership renewal (November 2024) focuses on developing coatings capable of withstanding high vibration and environmental stress, targeting performance eyewear for motorcycling.

Market Trend: EU REACH 2026 PFAS Restrictions Transform Oleophobic Coating Formulations in Eyewear

The sunglasses coating industry is undergoing a significant reformulation cycle as the European Chemicals Agency advances the phase-out of PFAS-based oleophobic coatings. Following the March 2026 opinions from regulatory committees, enforcement of strict concentration limits becomes effective October 10, 2026, targeting persistent fluorinated compounds such as PFHxA. These regulations impose thresholds as low as 25 parts per billion for specific substances, effectively eliminating traditional fluorocarbon-based “easy-clean” coatings from the European consumer market. This regulatory shift is particularly impactful given that over 70% of premium eyewear products rely on oleophobic coatings to deliver smudge resistance and low surface energy performance. Manufacturers are now accelerating the transition toward fluorine-free alternatives, including siliconized and bio-based hydrophobic coatings, which aim to replicate oil and water repellency without environmental persistence or bioaccumulation risks. This transition is not only compliance-driven but also reshaping product positioning, as brands increasingly market PFAS-free coatings as a sustainability differentiator. The reformulation challenge lies in balancing surface energy reduction, optical clarity, and abrasion resistance, making advanced material engineering a critical competitive factor in the evolving sunglasses coatings market.

Market Trend: ANSI Z80.3-2025 Drives Adoption of Functional Optical Coatings for Safety and Visual Performance

The release of ANSI Z80.3-2025 introduces a new generation of performance requirements for nonprescription eyewear, significantly elevating the role of functional coatings in sunglasses design. The updated standard emphasizes both safety and visual optimization, particularly through stricter requirements for blue-light attenuation and traffic signal recognition. Coatings must now achieve measurable reduction in high-energy visible light within the 380 nm to 500 nm spectrum, with advanced vacuum-deposited systems capable of filtering 40% to 50% of blue light while preserving accurate color perception. This shift is driving the replacement of traditional tinted lenses with precision-engineered multilayer coatings that deliver selective wavelength filtering. In parallel, the standard introduces enhanced criteria for traffic signal transmittance, requiring lenses to maintain a defined Q-factor that ensures clear differentiation of red, yellow, and green signals. This is accelerating the adoption of high-definition contrast coatings that utilize notch-filtering techniques to enhance specific wavelengths while reducing glare. As consumer expectations evolve toward both style and performance, compliance with ANSI Z80.3-2025 is pushing manufacturers to integrate advanced optical coatings that combine safety, clarity, and visual comfort.

Market Opportunity: Hydrophilic Anti-Fog Coatings Enhance Performance Eyewear for Sports and Active Lifestyles

The convergence of performance sports and lifestyle fashion is driving strong demand for advanced anti-fog coatings in the sunglasses market. Hydrophilic anti-fog technologies, which function by absorbing and dispersing moisture across the lens surface, are emerging as a key differentiator in high-performance eyewear. Unlike temporary surfactant-based treatments, these coatings are permanently integrated into the lens substrate, providing consistent fog resistance under dynamic environmental conditions. In 2026, leading formulations are capable of restoring full optical clarity within 0.5 seconds following rapid temperature transitions, such as those experienced during intense physical activity. This performance is particularly critical for cycling, running, and outdoor sports, where visibility directly impacts safety and user experience. Additionally, durability benchmarks have improved significantly, with advanced coatings capable of withstanding more than 500 simulated steam cycles and repeated cleaning without degradation in performance. This extended lifespan enhances product value and reduces the need for reapplication or replacement. As the “utility luxe” trend continues to merge technical functionality with premium design, hydrophilic anti-fog coatings are positioned as a high-growth opportunity in the performance eyewear segment.

Market Opportunity: Multilayer Dielectric Mirror Coatings Enable Thermal Management and Premium Aesthetic Customization

Dielectric multilayer mirror coatings are redefining the role of reflective finishes in sunglasses, evolving from purely aesthetic enhancements to multifunctional performance systems. These coatings, constructed from alternating layers of materials such as silicon dioxide and titanium dioxide, are engineered to selectively reflect specific wavelengths of light, including near-infrared radiation. Modern designs incorporating up to 12 layers can reflect up to 60% of near-infrared energy, significantly reducing heat buildup around the eyes and improving wearer comfort in high-intensity environments such as mountain and desert conditions. This thermal management capability is becoming a key selling point in premium and performance-oriented eyewear. At the same time, precise control over layer thickness enables advanced chromatic effects, allowing lenses to exhibit dynamic color shifts depending on the angle of light incidence. This feature supports the growing demand for visually distinctive products in the fashion segment while maintaining compliance with Category 3 and Category 4 UV protection standards. By combining functional benefits with aesthetic versatility, dielectric multilayer mirror coatings are emerging as a strategic innovation area within the sunglasses coatings industry.

Sunglasses Coating Market Share and Segmentation Insights: UV Protection Dominance and OEM Manufacturing Leadership

By Coating Functionality: UV Blocking Coatings Lead as a Mandatory Health and Safety Standard

The ultraviolet (UV) blocking coatings segment dominated the sunglasses coating market with a 27.4% share in 2025, driven by its essential role in eye protection and regulatory compliance. Global standards such as ANSI Z80.3, ISO 12312-1, and FDA regulations mandate that sunglasses must block 99–100% of harmful UVA and UVB radiation, making UV coatings a non-negotiable feature across all eyewear products, including prescription and non-prescription lenses. This requirement ensures that UV protection coatings are applied to virtually every pair of sunglasses manufactured globally, exceeding 1.2 billion units annually, making it the highest-volume coating segment. While not always premium-priced, its universal application across fashion sunglasses, sports eyewear, and safety glasses drives significant market share. The growing awareness of eye health, UV radiation risks, and preventive care continues to reinforce UV blocking coatings as the foundational technology in the global sunglasses coatings market.

By Sales Channel: OEM Manufacturers Dominate with Integrated Coating Technologies and Cost Efficiency

The OEM (lens and frame manufacturers) segment accounted for a leading 54.6% share of the sunglasses coating market in 2025, reflecting the strong integration of coating processes within large-scale eyewear manufacturing operations. Major players such as EssilorLuxottica, Safilo, and Carl Zeiss operate advanced in-house vacuum coating and dip coating lines, enabling the application of anti-reflective (AR), mirror, hydrophobic, oleophobic, and UV coatings directly during lens production. This integration allows OEMs to achieve high production efficiency, consistent coating quality, and the lowest per-unit cost, as coatings are applied alongside lens casting, edging, and assembly processes. In contrast, optical laboratories and retail channels typically apply coatings as secondary operations, resulting in higher costs and limited scalability. With increasing demand for multi-functional, high-performance eyewear coatings, OEM-led production continues to dominate, ensuring innovation, cost optimization, and mass-market accessibility in the global sunglasses coating market.

Competitive Landscape of the Sunglasses Coating Market

EssilorLuxottica Leads Market with Smart Lens Integration and Premium Coating Technologies

EssilorLuxottica SA is the undisputed leader in the sunglasses coating market, leveraging its vertically integrated model across brands like Ray-Ban and Oakley. The company controls 35% of global market revenue, driven by strong demand for premium polarized lenses. Its Crizal® Sun X Protect coating combines full-spectrum UV protection with advanced oleophobic properties, reducing smudging by 45%. EssilorLuxottica is also advancing electrochromic smart coatings, enabling app-controlled tint adjustment for next-generation eyewear.

ZEISS Sets Technical Benchmark with Advanced Anti-Static and Easy-Clean Coatings

Carl Zeiss Vision Care (ZEISS) is the technical standard in the sunglasses coating market, focusing on durability and hygiene. Its DuraVision Plus portfolio introduces CleanGuard technology, allowing lenses to be cleaned up to three times faster. ZEISS also integrates anti-static layers that repel up to 93% of dust and fingerprints, enhancing user experience. Its universal UVProtect technology ensures full UV coverage across all lens types, strengthening its leadership in the premium optical segment.

Safilo Expands Market with Sustainable Multi-Layer Mirror Coatings and Digital Channels

Safilo Group S.p.A. is a key innovator in the sunglasses coating market, focusing on luxury and sustainable eyewear. Its multi-layer mirror coatings, produced via energy-efficient vacuum deposition, reduce energy consumption by 20% per batch. Safilo’s expansion of direct-to-consumer (DTC) platforms enables rapid deployment of customized and limited-edition eyewear. Its commitment to sustainability is reflected in the transition of 33% of its collections to renewable or recycled materials, paired with eco-friendly coatings.

Hoya Leads APAC Market with High-Durability and Photochromic Coating Technologies

Hoya Corporation is a dominant player in the sunglasses coating market, particularly in Asia-Pacific. Its Hi-Vision LongLife (HVLL) coating offers 50% greater durability than standard hardcoats, setting industry benchmarks for scratch resistance. Hoya is also a leader in the photochromic segment, delivering faster transition speeds between tinted and clear states. Its investment in high-speed spin-coating technologies supports mass production of advanced coatings for digital-native consumers.

Mitsui Chemicals Strengthens Market with Advanced Optical Materials and UV-Blocking Technologies

Mitsui Chemicals plays a critical role in the sunglasses coating market as a supplier of high-index materials and coating resins. Its MR™ lens series, combined with UV420™ coatings, provides protection against high-energy visible (HEV) light. The company is also advancing bio-based optical monomers to reduce carbon footprint. Its innovations in super-hydrophobic sol-gel coatings enhance performance in humid and marine environments, reinforcing its position in high-performance optical materials.

PPG Expands Market Presence with High-Performance Optical Coatings and Impact-Resistant Materials

PPG Industries, Inc. is a major player in the sunglasses coating market, particularly in high-performance and safety eyewear. Its Trivex® and polycarbonate-based coatings dominate the impact-resistant segment, which accounts for over 50% of lens material share. PPG is also advancing multifunctional thin-film coatings, combining anti-fog, anti-scratch, and mirror properties. Its Hi-Transmittance AR coatings improve light transmission to 99.5%, supporting emerging trends in indoor-outdoor eyewear.

Germany Leading Precision Optical Coatings with Clean-Tech Multi-Layer Systems

Germany remains the global benchmark in the sunglasses coating market, driven by its expertise in high-durability thin-film optical coatings and precision engineering. Innovations such as advanced molecular low-surface-energy coatings (e.g., CleanGuard technology) are significantly improving lens cleanability and longevity, making lenses up to three times easier to maintain.

Technological advancements include the integration of anti-static coating layers that actively repel dust and airborne particles, particularly beneficial for sports and industrial eyewear. Investments in automated Ion-Assisted Deposition (IAD) manufacturing lines are enhancing production efficiency and consistency for multi-layer anti-reflective stacks. Regulatory pressure around environmental performance is accelerating the shift toward solvent-free and UV-curable coating technologies, while expanded production of silica-based precursors is supporting demand for scratch-resistant coatings. Additionally, Germany is witnessing strong adoption of hydrophilic anti-fog coatings in high-performance sports applications, reinforcing its leadership in premium optical coatings.

United States Driving Smart Eyewear Integration and PFAS-Free Coating Innovation

The United States is transforming the sunglasses coatings market through the integration of smart eyewear technologies and regulatory-driven innovation. The transition toward PFAS-free oleophobic and hydrophobic coatings is accelerating due to stricter environmental mandates, promoting safer and more sustainable lens chemistry.

Technological breakthroughs include fast-transition photochromic coatings capable of adapting from clear to sun-protective states within seconds, improving user convenience. The rise of smart sunglasses with integrated electronics and voice interfaces is creating demand for specialized durable coatings that protect embedded components. Product innovations such as infrared (IR) blocking coatings are enhancing ocular comfort in high-sun regions, while expansion of mass-production facilities is supporting the growth of anti-reflective coatings for athletic eyewear. These developments position the U.S. as a leader in combining functionality, sustainability, and digital integration in eyewear coatings.

China Scaling High-Performance Lens Coatings with Material Innovation and Mass Production

China has emerged as a dominant force in the sunglasses coatings market, leveraging its large-scale manufacturing capabilities and control over key raw materials. The country’s leadership in titanium dioxide (TiO₂) production is supporting the growth of reflective and UV-protective coatings for mass-market applications.

Technological advancements include the commercialization of gradient mirror coatings using advanced PVD techniques, enabling rapid product customization for fashion-driven markets. Government initiatives are supporting the development of photocatalytic self-cleaning coatings, enhancing functionality and durability. Product innovations such as graphene-reinforced hard coatings are improving scratch resistance, while the integration of blue-light filtering coatings is addressing increasing digital screen exposure. Expanded production of high-purity silica is further strengthening China’s position in anti-reflective and anti-scratch coating technologies.

Italy Leading Luxury Sunglasses Coatings with Aesthetic Innovation and Premium Materials

Italy remains the global hub for luxury sunglasses coatings, combining craftsmanship with advanced coating technologies. The use of precious metal vapor deposition is enabling unique aesthetic finishes, while innovations in gradient and mirror coatings are driving premium product differentiation.

Technological advancements include the use of sol-gel-based coating systems for in-store customization and refurbishment, supporting circular economy practices. Large-scale expansion of global retail networks is increasing the reach of high-end proprietary coatings. Additionally, the adoption of AI-driven spectral mapping technologies is ensuring precise color consistency across luxury product lines. Italy’s dominance in double-gradient mirror coatings highlights its focus on combining visual appeal with high optical performance in the premium segment.

Japan Advancing Nano-Precision Coatings for Optical Clarity and Anti-Fog Performance

Japan is a global leader in nano-scale sunglasses coatings, focusing on achieving superior optical clarity and durability. Innovations such as multi-layer interference filters with near-total anti-reflective efficiency are setting new benchmarks in lens performance, particularly for professional photography and high-end eyewear.

Technological advancements include nano-porous silica coatings that provide permanent anti-fog properties by absorbing moisture at the molecular level. Regulatory updates are enforcing stricter durability standards, encouraging the use of high-performance coating systems. Investments in clean-room manufacturing and expansion of super-lipophobic coatings are supporting applications in smart eyewear and electronics-integrated lenses, ensuring protection against sweat, oils, and environmental exposure. Japan’s focus on precision and quality continues to drive innovation in advanced optical coatings.

South Korea Driving Smart and Fashion-Tech Coatings for Next-Generation Eyewear

South Korea is emerging as a leader in smart and fashion-driven sunglasses coatings, leveraging its expertise in optoelectronics and consumer trends. Breakthroughs in piezochromic coatings are enabling lenses that change tint based on pressure or electronic input, supporting the growth of connected eyewear.

Product innovations such as invisible anti-fingerprint coatings are enhancing user experience by minimizing visible smudges, while investments in automated coating technologies are improving manufacturing efficiency. Government initiatives are promoting the development of bio-based coating materials, aligning with sustainability goals. Additionally, the rapid adoption of dual-tone mirror coatings in fashion markets is driving global trends in reflective aesthetics, reinforcing South Korea’s influence in the evolving eyewear industry.

Sunglasses Coating Market Report Scope

Sunglasses Coating Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$405.9 Million

|

|

Market Size (2032)

|

$709.3 Million

|

|

Market Growth Rate

|

8.3%

|

|

Segments

|

By Coating Functionality (Anti-Reflective, Ultraviolet, Scratch-Resistant, Mirror and Flash Coatings, Hydrophobic and Oleophobic Coatings, Anti-Fog Coatings, Photochromic Coatings, Polarized Coatings, Blue Light Filtering Coatings), By Coating Material (Titanium Dioxide, Silicon Dioxide, Magnesium Fluoride, Zirconium Dioxide, Fluoropolymers, Polyvinyl Alcohol, Indium Tin Oxide), By Technology (Vacuum Deposition, Spin Coating, Dip Coating, Sputtering, In-Mold Coating), By Lens Substrate (Polycarbonate, CR-39, High-Index Polymers, Trivex, Glass), By End-User (Fashion and Lifestyle, Sports and Performance, Tactical and Military, Industrial Safety, Healthcare), By Sales Channel (OEM, Optical Laboratories, Retail Eyewear Chains, Online Platforms)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

EssilorLuxottica, ZEISS Group, Hoya Corporation, Mitsui Chemicals, Inc., PPG Industries, Inc., Nippon Sheet Glass Co., Ltd., Schneider Optical Machines GmbH, Satisloh, Leybold Optics, Tokuyama Corporation, OptoSigma Corporation, Evonik Industries AG, Dow Inc., COTEC GmbH, Quantum Design, Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Sunglasses Coating Market Segmentation

By Coating Functionality

- Anti-Reflective

- Ultraviolet

- Scratch-Resistant

- Mirror and Flash Coatings

- Hydrophobic and Oleophobic Coatings

- Anti-Fog Coatings

- Photochromic Coatings

- Polarized Coatings

- Blue Light Filtering Coatings

By Coating Material

- Titanium Dioxide

- Silicon Dioxide

- Magnesium Fluoride

- Zirconium Dioxide

- Fluoropolymers

- Polyvinyl Alcohol

- Indium Tin Oxide

By Technology

- Vacuum Deposition

- Spin Coating

- Dip Coating

- Sputtering

- In-Mold Coating

By Lens Substrate

- Polycarbonate

- CR-39

- High-Index Polymers

- Trivex

- Glass

By End-User

- Fashion and Lifestyle

- Sports and Performance

- Tactical and Military

- Industrial Safety

- Healthcare

By Sales Channel

- OEM

- Optical Laboratories

- Retail Eyewear Chains

- Online Platforms

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Sunglasses Coating Industry

- EssilorLuxottica

- ZEISS Group

- Hoya Corporation

- Mitsui Chemicals, Inc.

- PPG Industries, Inc.

- Nippon Sheet Glass Co., Ltd.

- Schneider Optical Machines GmbH

- Satisloh

- Leybold Optics

- Tokuyama Corporation

- OptoSigma Corporation

- Evonik Industries AG

- Dow Inc.

- COTEC GmbH

- Quantum Design, Inc.

*- List not Exhaustive