Super Abrasives Market Valuation 2025–2034: $9.2 Billion to $16.6 Billion at 6.8% CAGR Driven by EV Power Electronics, CVD Diamond Coatings, and AI-Enabled Precision Manufacturing

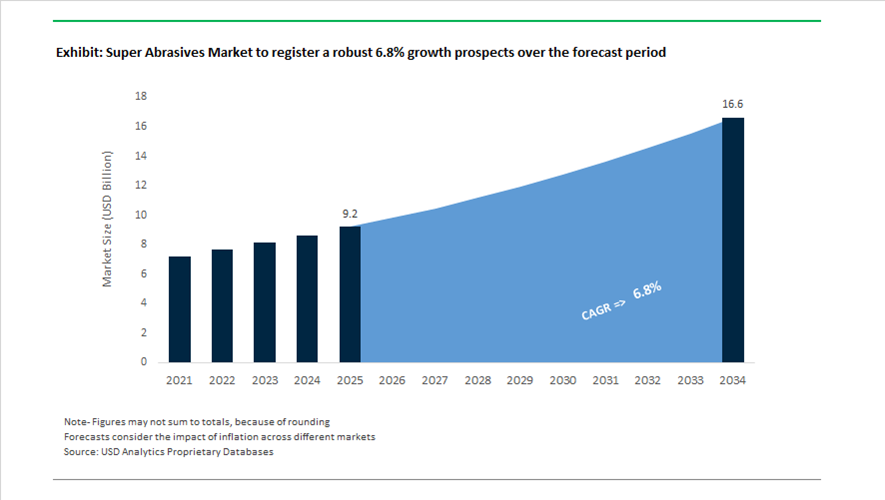

The global super abrasives market is valued at $9.2 billion in 2025 and is projected to reach $16.6 billion by 2034, expanding at a CAGR of 6.8%. Growth is fueled by rising demand for diamond abrasives, cubic boron nitride (CBN) tools, polycrystalline diamond (PCD) inserts, hybrid diamond-CBN grinding wheels, and thermal management composites across EV manufacturing, aerospace machining, semiconductor wafer processing, bearing production, and rail infrastructure. Increasing electrification, silicon carbide wafer adoption, lightweight aluminum machining, and high-performance computing hardware are pushing manufacturers toward ultra-hard materials capable of micron-level precision and superior thermal conductivity. Simultaneously, AI-based quality control and sustainable production technologies are reshaping cost structures and defect tolerance standards in advanced grinding and cutting systems.

Capacity expansion and geographic diversification accelerated in 2024 and early 2025. Following its acquisition of Acme Abrasives, Tyrolit integrated operations through 2024, establishing its sixth U.S. facility to strengthen its super abrasive portfolio for North American steel and rail applications. During 2024 and 2025, Tyrolit also broke ground on a new manufacturing plant in Pune, India, targeting high-performance diamond and CBN tools for the expanding automotive and infrastructure sectors. In 2024, Hyperion Materials & Technologies expanded its R&D and production footprint near Barcelona, focusing on PCD and cemented carbide tooling solutions for aerospace and industrial machining. In January 2025, Element Six introduced a Copper Diamond Composite engineered for thermal management in AI and high-performance computing hardware, delivering thermal conductivity levels of approximately 800 W/mK to mitigate heat-induced semiconductor degradation. In July 2025, Kyocera launched the MD90 super fine pitch cutter featuring advanced diamond-tipped inserts optimized for precision aluminum machining in electric vehicle platforms.

Strategic integration and technology innovation intensified in late 2025 and early 2026. In September 2025, Kyocera Unimerco integrated Weber Technologies GmbH to scale CVD diamond coating technology across aerospace and automotive tool networks. In October 2025, Mirka finalized the acquisition of URMA Rolls, strengthening its diamond dressing roll capabilities for high-precision bearing and powertrain grinding. In the same month, Mirka announced a €25 million investment in a green technology production line in Finland, enhancing sustainable abrasive manufacturing efficiency. Throughout late 2025 and early 2026, manufacturers including Asahi Diamond and Tyrolit commercialized hybrid diamond-CBN wheels enabling faster dicing of silicon carbide wafers used in EV power electronics. In late 2025, Resonac deployed a deep-learning AI inspection system reducing false detection rates in super abrasive particle inspection to 3.2%, ensuring compliance with semiconductor-grade zero-defect standards. In September 2025, 3M committed $3.5 billion to R&D through 2027, targeting accelerated product launches in automotive electrification and industrial automation where super abrasive tools are mission-critical. These acquisitions, hybrid tool innovations, AI-driven quality upgrades, and EV-driven demand expansions are reinforcing sustained growth in the super abrasives market through 2034.

Structural Trends and Monetizable Opportunities in the Super Abrasives Market

Strategic Investment in Diamond Slurries for 200 mm and 300 mm SiC Wafering

The global transition from silicon to Silicon Carbide substrates is fundamentally redefining the super abrasives market, with diamond slurry performance now dictating throughput, yield, and cost economics across the power semiconductor supply chain. SiC wafering and polishing demand abrasives that can withstand extreme hardness while maintaining tight control over material removal rates and surface integrity. As wafer diameters scale from 150 mm to 200 mm and now toward 300 mm, slurry homogeneity and thermal stability have become non negotiable performance criteria.

This shift is closely tied to capacity expansion programs at leading SiC manufacturers. In October 2024, Wolfspeed secured a $2.5 billion funding package, including support from the US CHIPS Act, to accelerate its $6 billion SiC expansion. The John Palmour Manufacturing Center is engineered to deliver a tenfold increase in 200 mm wafer output, forcing abrasive suppliers to scale bulk diamond slurries capable of sustaining material removal rates of 8 to 10 micrometers per hour while preserving sub-nanometer surface roughness.

The technology bar rose further in December 2025 when Coherent Corp. announced the industry’s first 300 mm SiC platform milestone. Larger wafers intensify thermal gradients during polishing and amplify defect risk, pushing demand toward ultra homogeneous diamond slurries that consistently deliver Ra values below 0.2 nanometers. As AI data centers and high voltage power electronics drive SiC adoption, diamond slurry suppliers are increasingly embedded as strategic partners rather than interchangeable consumable vendors.

PCBN Tooling Mandates for EV Powertrain Hard-Part Turning

Electrification is reshaping automotive machining strategies, accelerating the adoption of Polycrystalline Cubic Boron Nitride tooling for hardened steel components in EV motors, gears, and transmissions. PCBN’s superior thermal stability compared with carbide enables hard part turning after heat treatment, eliminating secondary grinding operations and compressing manufacturing cycle times. For OEMs and Tier 1 suppliers, this transition directly supports cost reduction, energy efficiency, and sustainability targets.

At TechDays 2025, Sandvik Coromant demonstrated that PCBN tooling can reduce machining cycle times by 30 to 50% in transmission and drivetrain components. Higher cutting speeds reduce tool changes, scrap rates, and energy consumption, aligning machining efficiency with corporate decarbonization goals.

Product innovation is keeping pace with these demands. In October 2024, Kennametal launched its KCU25B turning inserts, engineered for roughing and medium machining of hardened steels and high temperature alloys. These PCBN tools integrate advanced PVD coatings to enhance flank wear resistance and edge stability, addressing the aggressive wear environments typical of next generation EV and aerospace platforms. As hard machining becomes the default rather than the exception, PCBN tooling is emerging as a structural growth pillar within the super abrasives market.

Automated Post-Processing Systems for Metal Additive Manufacturing

As additive manufacturing transitions from prototyping to serial production, post-processing has emerged as the primary bottleneck limiting scalability. Aerospace, medical, and industrial OEMs now require automated, repeatable finishing solutions capable of removing support structures and refining complex geometries without manual intervention. This creates a high-margin opportunity for super abrasive systems designed specifically for automated AM workflows.

Industry assessments released in early 2025 emphasize that automation is no longer optional in post-processing. Companies such as PostProcess Technologies are deploying software-driven finishing platforms that integrate super abrasive grinding wheels, robotic milling heads, and adaptive control systems. These solutions reduce labor dependency while cutting chemical and energy usage, directly improving the sustainability profile of AM production lines.

Surface integrity is a critical differentiator. A 2024 study on AM components highlighted that mechanical finishing methods, including magnetic abrasive finishing and precision diamond tooling, significantly improve fatigue life by mitigating micro-cracks and surface defects. For abrasive manufacturers, this opens a pathway to develop diamond coated robotic brushes and custom abrasive tools capable of navigating internal channels and lattice structures that are inaccessible to conventional finishing techniques.

Ultra-Fine Diamond Compounds for Compound Semiconductor Polishing

Beyond SiC, rapid growth in GaN on silicon and GaN photonics for 5G infrastructure, satellite communications, and advanced optics is creating demand for atomically smooth surfaces. This niche requires ultra fine diamond compounds with particle sizes ranging from 1 to 100 nanometers, where even minimal surface contamination can compromise device performance.

By late 2025, technical briefings on water-based diamond suspensions highlighted the increasing use of nanodiamonds engineered with self-lubricating characteristics. These formulations improve polishing efficiency while minimizing defect density, particularly in optics and photonics applications where surface precision directly impacts signal integrity.

High volume manufacturing readiness is now the critical success factor. Entegris and Fujimi Incorporated are scaling HVM qualified slurry platforms such as the DM 1000 series, capable of delivering surface finishes below 5 angstroms. These ultra fine abrasive systems are essential for planarizing FinFET and Gate All Around transistor architectures, where any residual surface defect can result in catastrophic yield loss. As compound semiconductors move deeper into mainstream electronics, ultra fine diamond abrasives represent one of the most technically demanding and profitable segments within the super abrasives market.

Super Abrasives Market Share and Segmentation Insights

Diamond Abrasives Lead with Superior Hardness and Semiconductor Wafer Processing Demand

Diamond abrasives accounted for 72.80% of the super abrasives market in 2025, driven by their unmatched hardness and cutting efficiency across high-precision industrial applications. These abrasives are extensively used in semiconductor wafer dicing, automotive component grinding, construction cutting tools, and precision optics, where superior material removal rates and surface finish are critical. The scalability of synthetic diamond production ensures consistent quality and cost efficiency for industrial use. The 2025 growth driver is the rising demand for silicon carbide and advanced semiconductor materials, where diamond abrasives are essential for wafer slicing, grinding, and polishing, supporting precision manufacturing in next-generation power electronics and microelectronic devices.

Semiconductor and Electronics Sector Drives High-Precision Super Abrasives Consumption

Semiconductors and electronics accounted for 34.80% of super abrasives market demand in 2025, making it the leading end-use industry due to its reliance on ultra-precision material processing. Diamond abrasives are critical in wafer thinning, back grinding, dicing, and polishing of silicon, SiC, and compound semiconductors, ensuring minimal surface defects and high yield. Increasing adoption of advanced packaging, MEMS devices, and power semiconductors continues to elevate demand for high-performance abrasive solutions. The 2025 trend centers on wafer thinning and fine-pitch dicing advancements, where ultra-thin blades, fine-grit grinding wheels, and precision polishing systems enable tighter tolerances, reduced chipping, and improved device performance in semiconductor fabrication processes.

Super Abrasives Market Competitive Landscape

The super abrasives market in 2026 is defined by advanced CBN and PCD engineering, AI-driven tool design, and localized manufacturing hubs in Asia. Competition centers on thermal stability, precision grinding of high-nickel alloys, and semiconductor materials, with increasing focus on digital integration and low-emission abrasive systems.

Saint-Gobain Expands Low-Emission Superabrasives with Ceramic Grain Technology and Global Localization

Saint-Gobain is strengthening its leadership in high-performance super abrasives through its "Lead & Grow" strategy and decarbonized manufacturing initiatives. The company reported €46.5 billion in 2025 sales, supported by resilient industrial segments and precision grinding solutions. Its Norton Quantum Prime series utilizes advanced ceramic grain technology to deliver higher metal removal rates and reduced thermal damage in aerospace grinding. Expansion into Indonesia and the Dominican Republic enhances localized production of abrasive bonding agents. The company is integrating recycled materials and low-energy vitrified bonds to align with net-zero targets. Its focus on sustainable abrasive systems supports demand from advanced manufacturing and construction sectors.

3M Accelerates AI-Driven Superabrasive Design and Semiconductor Grinding Applications

3M is transforming its super abrasives portfolio through AI-integrated R&D and high-margin industrial applications. The company committed $3.5 billion to machine learning-driven abrasive design, optimizing diamond grain orientation to extend tool life. In 2025, 3M reported $24.3 billion in sales with a 21.1% operating margin in its Safety and Industrial segment. Its Precision-Shaped Grain technology is widely used in semiconductor wafer back-grinding and dicing for SiC and GaN substrates. The company is reformulating abrasive systems to eliminate PFAS, aligning with regulatory shifts in 2025–2026. Its innovation strategy focuses on precision, durability, and sustainability in next-generation electronics manufacturing.

Sandvik Integrates Digital Manufacturing and Tungsten Supply Chain for Closed-Loop Grinding Systems

Sandvik is advancing super abrasive technologies through digital manufacturing and secure raw material integration. The company achieved 11% organic order growth in 2025, supported by SEK 4.5 billion in R&D investment targeting automation and advanced materials. Its internal tungsten processing capabilities ensure supply chain stability for abrasive bonding systems amid global shortages. Innovations such as the CoroCut® 2 platform enhance wear resistance and tool longevity in high-interruption machining. Sandvik’s acquisition of CAM and metrology firms enables closed-loop grinding systems with real-time tool wear compensation. Its dual focus on machining and intelligent manufacturing strengthens its position in precision engineering markets.

Tyrolit Expands Local Manufacturing in India with Digital Monitoring and High-Precision Grinding Solutions

Tyrolit is scaling its global footprint through localized production and advanced monitoring systems for super abrasives. The company’s Pune facility, launched in 2025, enables regional retipping and finishing of CBN and diamond wheels, reducing lead times and logistics costs. Its SKYTEC XD-2 and ALPHA series deliver improved self-sharpening and higher removal rates for stainless steel and industrial applications. The integration of ToolScope provides real-time grinding force data, minimizing thermal damage and improving process control. Tyrolit specializes in custom-engineered, non-standard tools including large-diameter and ultra-thin precision wheels. Its strategy targets double-digit market share growth in Asia by 2030.

Asahi Diamond Strengthens Semiconductor-Focused Superabrasives Amid Supply Chain Diversification

Asahi Diamond is reinforcing its position in high-precision super abrasives with a strong focus on semiconductor and electronics applications. The company is actively diversifying its synthetic diamond sourcing to mitigate export restrictions from China. Its Mid-term Management Plan prioritizes semiconductor wafer processing, with new tools showcased at SEMICON China 2026. Investments in R&D facilities and headquarters modernization support faster development of electroplated diamond wire for solar and EV applications. The company continues to optimize capital efficiency through shareholder-focused financial strategies. Its advanced diamond technologies address the precision requirements of power modules and next-generation chip manufacturing.

China Super Abrasives Market Shaped by Export Controls and Industrial Localization

China’s super abrasives industry has entered a phase of strategic tightening and domestic prioritization following the implementation of export controls on artificial diamond abrasive grains and related superhard materials in November 2024. The requirement for dual-use export licenses has materially altered global supply dynamics for the 2025–2026 cycle, reinforcing China’s intent to retain domestic access to critical super-abrasive inputs. This policy shift is closely aligned with the Non-Ferrous Metals Action Plan (2025–2026), led by the Ministry of Industry and Information Technology, which targets a 5% average annual growth in value-added output by emphasizing ultra-purity metals and advanced rare earth materials that require diamond and CBN-based precision grinding.

Demand-side momentum is increasingly driven by China’s semiconductor localization agenda. Under the 2025–2026 industrial framework, domestic production of high-purity grinding wheels and CMP pads has been prioritized to support 2nm and 5nm chip fabrication goals. Parallel targets to scale secondary metal production to 20 million tonnes have boosted the use of high-durability CBN tools for recycled high-strength alloys, where conventional abrasives underperform. At the operational level, the “AI + Manufacturing” roadmap has accelerated deployment of smart abrasive monitoring systems, cutting precision grinding waste by an estimated 18%. Regionally, Henan province continues to anchor the sector, accounting for more than 70% of global synthetic diamond output and increasingly focusing on large-particle lab-grown diamonds for heavy-duty industrial cutting tools.

United States Super Abrasives Market Anchored in Innovation and Environmental Applications

The U.S. super abrasives market is defined less by volume expansion and more by technology-driven differentiation across advanced manufacturing, semiconductors, and environmental solutions. Strategic consolidation has continued, exemplified by Saint-Gobain Abrasives entering a partnership with Dedeco Abrasive Products in 2024 to strengthen its position in specialized jewelry and dental super-abrasives through 2026. This reflects a broader trend toward niche, high-margin applications rather than commoditized grinding products.

Innovation investment has intensified. In late 2025, 3M unveiled re-engineered Cubitron and Trizact micro-replicated technologies, delivering substantial reductions in operator vibration and step-change improvements in cut rates. Federal CHIPS Act funding has also flowed into Diamond-on-Silicon technologies, increasing domestic demand for ultra-fine diamond abrasives used in thermal management for next-generation data centers. Beyond manufacturing, environmental use cases are emerging as a strategic growth vector. Element Six received global recognition in 2025 for its Diamox technology, which deploys boron-doped diamond electrodes to destroy PFAS in industrial wastewater, highlighting the expanding role of synthetic diamonds beyond mechanical abrasion.

Japan Super Abrasives Market Driven by Semiconductor and EV Precision Standards

Japan’s super abrasives industry continues to be anchored in ultra-precision manufacturing for semiconductors, electric vehicles, and advanced materials. In December 2025, Resonac was recognized with a top-tier supplier award for its contributions to advanced semiconductor packaging ecosystems, which rely heavily on super-abrasive precision for component preparation and finishing. This recognition underscores Japan’s strength in coupling materials science with process control.

Structural demand is also being reinforced by EV and lightweighting initiatives. Government-backed programs have accelerated the machining of silicon carbide wafers and carbon fiber composites, both of which require diamond and CBN abrasives to maintain dimensional accuracy and surface integrity. Asahi Diamond Industrial has responded by restructuring its global operations and reallocating capital toward semiconductor-grade grinding wheel R&D for the 2026–2030 cycle. Concurrently, Japan’s hydrogen co-firing and hard-to-abate industry projects have begun integrating super-abrasive material production into low-carbon power frameworks, while automated CNC abrasive dressing has become the standard for aerospace-grade components.

Germany Super Abrasives Market Aligned with Green Steel and Strategic Expansion

Germany’s super abrasives market is closely linked to industrial modernization and sustainability-led materials transitions. In October 2025, Saint-Gobain outlined its “Lead & Grow” roadmap, committing to a multi-year investment and acquisition strategy aimed at infrastructure-heavy regions and applications that demand super-abrasive precision. This strategic direction reinforces Germany’s role as a technology and application development hub rather than a low-cost producer.

At the research and materials level, collaboration with institutions such as the Fraunhofer network has supported the recovery of Germany’s domestic materials market, particularly in low-carbon grinding solutions. The national Green Steel initiative has emerged as a structural demand driver, as hydrogen-reduced iron and tougher DRI-based alloys require CBN wheels with superior thermal and mechanical resilience. These shifts position super abrasives as an enabling technology within Germany’s broader decarbonization and industrial efficiency agenda.

Comparative Snapshot: Super Abrasives Industry by Country

Super Abrasives Market County Level Snapshot

|

Country

|

Core Demand Driver

|

Strategic Focus

|

Competitive Differentiator

|

|

China

|

Semiconductors and recycled metals

|

Export control and localization

|

Scale in synthetic diamond and AI-enabled manufacturing

|

|

United States

|

Advanced manufacturing and environment

|

Innovation and niche applications

|

Diamond-on-silicon and PFAS destruction technologies

|

|

Japan

|

Semiconductors and EV materials

|

Ultra-precision engineering

|

Automated standards and high-purity processing

|

|

Germany

|

Green steel and infrastructure

|

Sustainable materials transition

|

CBN tools for hydrogen-reduced alloys

|

Super Abrasives Market Report Scope

Super Abrasives Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$9.2 Billion

|

|

Market Size (2034)

|

$16.6 Billion

|

|

Market Growth Rate

|

6.8%

|

|

Segments

|

By Material Type (Diamond Abrasives, Cubic Boron Nitride Abrasives, Hybrid Super Abrasives), By Bond Type (Vitrified Bond, Resin Bond, Metal Bond, Electroplated), By End-Use Industry (Semiconductors and Electronics, Automotive, Aerospace and Defense, Healthcare and Medical, Construction and Infrastructure)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Saint-Gobain Abrasives, 3M Company, Element Six, Asahi Diamond Industrial Co., Ltd., Resonac Holdings Corporation, Tyrolit Group, Sandvik AB, Mitsubishi Materials Corporation, Noritake Co., Ltd., Zhengzhou Zhongnan Jihua Superhard Material Co., Ltd., Henan Huanghe Whirlwind Co., Ltd., Fujimi Incorporated, Vardhaman Abrasives, Sino-Crystal Diamond Co., Ltd., Hilti Group

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Super Abrasives Market Segmentation

By Material Type

- Diamond Abrasives

- Cubic Boron Nitride Abrasives

- Hybrid Super Abrasives

By Bond Type

- Vitrified Bond

- Resin Bond

- Metal Bond

- Electroplated

By End-Use Industry

- Semiconductors and Electronics

- Automotive

- Aerospace and Defense

- Healthcare and Medical

- Construction and Infrastructure

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Super Abrasives Industry

- Saint-Gobain Abrasives

- 3M Company

- Element Six

- Asahi Diamond Industrial Co., Ltd.

- Resonac Holdings Corporation

- Tyrolit Group

- Sandvik AB

- Mitsubishi Materials Corporation

- Noritake Co., Ltd.

- Zhengzhou Zhongnan Jihua Superhard Material Co., Ltd.

- Henan Huanghe Whirlwind Co., Ltd.

- Fujimi Incorporated

- Vardhaman Abrasives

- Sino-Crystal Diamond Co., Ltd.

- Hilti Group

*- List not Exhaustive