LED Materials Market 2025–2034: Micro-LED Epitaxy, UV-C Innovation, and Vertical Integration Driving $88.2 Billion Outlook at 9.9% CAGR

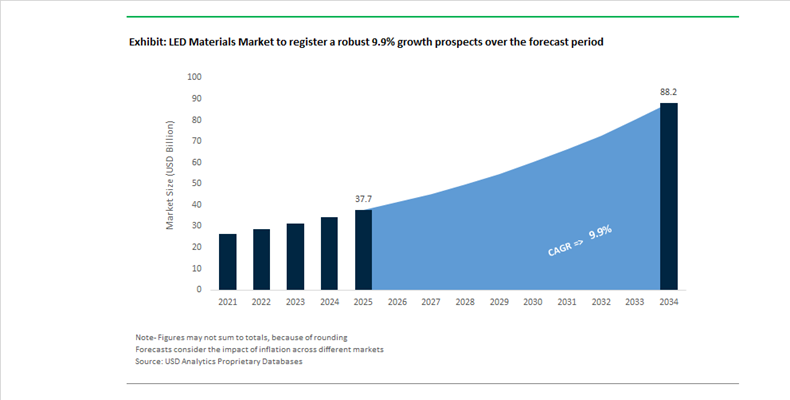

The LED Materials Market is projected to expand from $37.7 billion in 2025 to $88.2 billion by 2034, reflecting a strong CAGR of 9.9%. Growth is anchored in accelerating adoption of Micro-LED epitaxial wafers, advanced phosphor materials, high-efficiency InGaN emitters, UV-C semiconductor packages, and modular LED component systems across display technology, automotive lighting, smart wearables, water sterilization, and architectural illumination. The industry is undergoing structural transformation as chipmakers, packaging specialists, and system integrators realign supply chains to capture value in high-definition displays, adaptive driving beams, and mercury-free UV solutions.

Throughout late 2024 and 2025, Lumileds and research institutes reported breakthroughs in Red Indium Gallium Nitride (InGaN) LED efficiency, addressing a critical bottleneck in Micro-LED development. Traditionally dominated by AlInGaP materials, red emission via InGaN enables improved thermal stability and monolithic integration with blue and green LEDs on a single wafer, significantly simplifying mass transfer and alignment processes for ultra-high-resolution displays. In early 2025, Lumileds and Cree Lighting introduced the “NightScape” 1900K/50CRI low-blue light LED materials engineered to reduce ecological light pollution while maintaining luminous efficacy. In October 2025, Nichia doubled UV-C output density through advanced heat dissipation packaging adapted from laser diode architecture, increasing mercury-free water sterilization capacity from 10 m3/h to 25 m3/h. These advances underscore rising demand for high-power UV-C emitters, specialty phosphors, and thermally optimized substrate materials.

Strategic consolidation and portfolio focus intensified in 2025 and 2026. In August 2025, San’an Optoelectronics and Inari Berhad reached a definitive agreement to acquire Lumileds for $239 million, with completion expected in early 2026. This transaction provides San’an, already the largest global LED chip producer, with vertical integration into premium high-power LED materials and automotive lighting systems. In December 2025, Samsung Electronics announced expanded Micro-RGB TV production for 2026, signaling industrial-scale growth in sub-100µm RGB LED fabrication and advanced mass transfer materials required for precise chip placement. On February 3, 2026, ams OSRAM completed the €570 million divestment of its non-optical sensor business to Infineon, sharpening its Digital Photonics strategy focused on Micro-LED emitters and adaptive driving beam materials. At CES 2026, ams OSRAM introduced VEGALED, an ultra-compact RGGB four-chip package optimized for LCOS micro-displays in AR smart glasses. In February 2026, Cree LED launched OptiLamp with pixel-level active intelligence enabled by advanced multi-layer material stacking. In January 2026, Nichia initiated a full transition to mercury-free LED-based production lines by 2030, reinforcing long-term demand for high-irradiance UV-LED materials. Signify reported in its 2025 year-end results that circular revenues reached 37% of total sales, driven by modular LED luminaire architectures supporting standardized, replaceable LED material components.

Strategic Trends and High-Impact Opportunities Shaping the LED Materials Market

Trend: Industry-Wide Transition to 200mm Silicon Carbide Substrates for Power and Automotive LEDs

The LED materials market is experiencing a structural realignment driven by the rapid scale-up of 200mm silicon carbide substrates, which are becoming essential for cost-efficient, high-voltage power electronics and advanced automotive LED systems. The shift from 150mm to 200mm SiC wafers is not a simple diameter expansion but a material science upgrade aimed at reducing basal plane dislocations, improving epitaxial uniformity, and maximizing usable die count per wafer. These improvements are critical for lowering cost per kilowatt in electric vehicle inverters, onboard chargers, and high-reliability LED driver modules used in next-generation mobility platforms.

In August 2024, Infineon Technologies inaugurated the first phase of its Kulim 3 facility in Malaysia, positioned as the world’s largest 200mm SiC power semiconductor fab. To secure long-term leadership in wide-bandgap materials, Infineon committed an additional €5 billion for Phase 2 expansion, bringing total site investment close to €7 billion and backed by €6 billion in forward supply commitments from automotive OEMs including Ford, SAIC, and Chery. Parallel capacity scaling is underway in North America. In late 2024, Wolfspeed secured a combined $1.5 billion financing package under the U.S. CHIPS and Science Act and private capital markets to accelerate ramp-up at its Mohawk Valley Fab, the first fully automated 200mm SiC facility globally, while strategically shutting down older 150mm lines. Yield improvements from trench-based architectures on 200mm wafers now enable roughly 30% more chips per wafer, materially improving LED power module economics.

Trend: Advanced Mass-Transfer and Bonding Materials Enable MicroLED Commercialization

MicroLED commercialization remains constrained by mass-transfer yield and bonding precision, placing advanced materials at the center of the technology roadmap. The LED materials market is responding with rapid innovation in eutectic bonding alloys and anisotropic conductive films that enable simultaneous placement of tens of thousands of micron-scale emitters with near-perfect yield. As pixel pitches fall below 50 microns, bonding materials must deliver mechanical stability, thermal conductivity, and electrical isolation at unprecedented tolerances.

By March 2025, two divergent but material-intensive approaches had gained traction. ams OSRAM advanced its GaN-on-silicon EVIYOS 2.0 architecture, integrating 25,600 pixels on a single die to minimize transfer steps. In contrast, Nichia commercialized its µPLS platform, which relies on the precise mass transfer of 16,384 discrete micro-LEDs onto an ASIC backplane. Late-2025 patent filings such as WO/2025/255661 highlight automated quality control modules that monitor Van der Waals forces and photothermal reactions during bonding, underscoring the growing importance of materials-level precision. High-end display R&D is increasingly adopting gold indium and tin copper eutectic systems, which outperform polymer adhesives in thermal dissipation and mechanical reliability, a prerequisite for high-brightness automotive HUDs and AR VR displays.

Opportunity: High-Stability Phosphor Materials for Adaptive Driving Beam Headlights

Regulatory approval of Adaptive Driving Beam technology has unlocked a premium growth segment for wavelength conversion materials capable of operating under extreme optical and thermal loads. In the LED materials market, phosphors designed for pixelated headlamp matrices are becoming mission-critical components as automakers deploy software-defined lighting for safety and differentiation.

In July 2025, ams OSRAM partnered with NIO to integrate the EVIYOS HD25 microLED platform into the NIO ET9, deploying a 25,600-pixel matrix that enables real-time beam shaping and on-road symbol projection. These systems require ultra-stable phosphors with narrow emission bandwidths and high thermal resilience. Performance benchmarks indicate that advanced phosphor formulations have extended headlight projection distances from 350 meters to 500 meters while boosting low-beam ground illumination by 50% in dense urban settings. Material requirements are intensifying further. In November 2025, Koito Manufacturing introduced a compact laser-based ADB system for electric vehicles, accelerating demand for laser-pumped phosphors with superior thermal conductivity to prevent quenching at elevated power densities.

Opportunity: AlGaN-Based UV-C LED Materials for Mercury-Free Disinfection

The global phase-down of mercury vapor lamps under the Minamata Convention is creating a long-term growth opportunity for aluminum gallium nitride epitaxial materials used in UV-C LEDs. These materials form the backbone of solid-state disinfection systems operating in the 200 to 280 nanometer range for air, surface, and water sterilization. Regulatory enforcement is accelerating adoption as agencies including the United States Environmental Protection Agency tighten compliance under frameworks such as FIFRA, favoring mercury-free technologies.

As of 2025, mercury lamps still account for approximately 46% of installed disinfection capacity, but UV-C LEDs represent the fastest-growing segment due to their compact form factor, instant-on performance, and system-level integration flexibility. However, a material efficiency gap remains. UV-C LEDs lag visible LEDs in wall-plug efficiency, creating high-value opportunities for advanced AlGaN epitaxy, specialty quartz encapsulation, and high-reflectivity p-side materials that improve deep-UV photon extraction. Suppliers that can close this efficiency gap stand to capture outsized value as UV-C LEDs scale across healthcare, municipal water treatment, and industrial hygiene applications.

LED Materials Market Share and Segmentation Insights

Substrate Materials Lead LED Materials Demand Through Critical Role in Epitaxial Growth and Device Performance

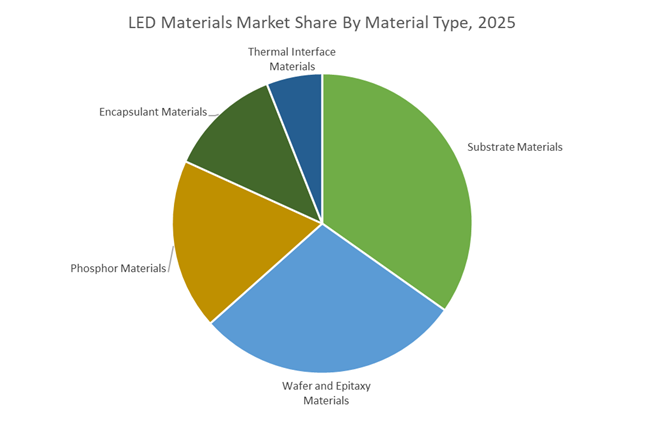

Substrate materials held 34.80% of the LED Materials Market share in 2025, making them the most significant material category in LED manufacturing. Substrates such as sapphire, silicon carbide (SiC), silicon, and gallium nitride on silicon platforms serve as the structural base for epitaxial layer growth used in LED chips. The quality and composition of the substrate directly influence crystal structure, defect density, thermal conductivity, and overall luminous efficiency, making substrate selection one of the most critical factors in LED device performance and production cost. Sapphire substrates remain widely used in high-brightness LED manufacturing, while silicon-based platforms are gaining attention for certain applications due to their compatibility with existing semiconductor manufacturing infrastructure. In 2025, LED manufacturers continue transitioning toward large-diameter wafer substrates, including 6-inch and 8-inch wafers, enabling improved production yields and reduced per-unit costs. Advances in substrate engineering and defect control technologies support scalable LED chip manufacturing for high-volume lighting, display, and automotive applications.

General Lighting Drives the Largest Demand for LED Materials

General lighting accounted for 48.60% of the LED Materials Market share in 2025, establishing it as the largest application segment for LED materials. LEDs have become the dominant lighting technology for residential, commercial, and industrial illumination, replacing legacy light sources such as incandescent bulbs, compact fluorescent lamps (CFLs), and high-intensity discharge (HID) lighting. Government energy efficiency regulations and sustainability initiatives across global markets have accelerated the adoption of LED lighting due to its long operational life, reduced energy consumption, and lower maintenance costs. LED materials including substrates, epitaxy wafers, phosphors, encapsulants, and thermal interface materials are essential for manufacturing high-performance LED chips and modules used in lighting systems. In 2025, the evolution of smart lighting ecosystems is reshaping material performance requirements, as LED devices increasingly support dimming capability, tunable white lighting, color control, and connectivity with building automation and smart home systems. These advanced functionalities require LED materials capable of maintaining consistent luminous output, color stability, and thermal reliability under diverse operating conditions.

LED Materials Market Competitive Landscape

The LED materials market in 2026 is shaped by Micro-LED scaling, UV-C LED adoption, and WBG material innovation. Competitive intensity is rising due to IP-driven differentiation, GaN-based material advancements, and strategic pivots toward automotive LED, AR/VR displays, and human-centric lighting applications.

Nichia leads UV-C LED materials innovation and phosphor IP dominance

Nichia Corporation maintains technological leadership in LED materials through its vertically integrated GaN-on-sapphire platform and dominant phosphor IP portfolio. Its Mercury-Free Project is accelerating UV-C LED adoption for water sterilization and industrial disinfection, supported by breakthroughs that increase throughput to 25 m³/h while reducing system footprint. The sustainabLED™ initiative further strengthens its ESG positioning by reducing packaging waste and logistics emissions. Nichia’s control over high-brightness blue LED materials and white LED phosphors continues to create high entry barriers, particularly in high-power UV-LED and mercury-free lighting infrastructure markets.

ams OSRAM scales digital photonics with sensor-integrated LED platforms

ams OSRAM AG is redefining LED materials demand through its digital photonics strategy, integrating emitters with CMOS sensors and ASICs for intelligent lighting systems. Innovations such as the EVIYOS™ HD 25 with 25,000+ pixels and VEGALED™ RGGB chips target automotive adaptive lighting and AR/VR micro-display applications. Its IR:6 technology enhances infrared LED efficiency by 33%, optimizing facial recognition and driver monitoring systems. Expansion of its Shanghai design center reflects strong positioning in the Asia-Pacific LED materials market, particularly in high-growth sensor-driven applications.

Samsung drives Micro-LED material commercialization with AI-integrated displays

Samsung Electronics is accelerating Micro-LED commercialization by combining sub-100 μm LED chip fabrication with AI-driven display ecosystems. Its Micro RGB technology achieves full BT.2020 color gamut, setting benchmarks for wide-bandgap LED materials in ultra-high-definition displays. The expansion of Micro RGB TVs up to 115 inches and integration of Vision AI Companion shift value toward intelligent display systems. Samsung’s deployment of Onyx LED cinema screens and large-scale signage reinforces demand for high-efficiency LED materials in premium visualization and commercial display segments.

Lumileds strengthens automotive LED materials through high-power innovation and M&A

Lumileds Holding B.V. is reinforcing its position in high-power LED materials following its acquisition by San’an Optoelectronics, combining scale manufacturing with advanced IP. Its LUXEON NightScape technology addresses blue-light reduction below 2%, aligning with regulatory and environmental lighting standards. The LUXEON Versat platform supports next-generation EV headlamp design with thermal stability and compact form factors. Dominance in adaptive driving beam (ADB) systems through modular LED architectures positions Lumileds at the forefront of automotive LED materials innovation.

Seoul Semiconductor advances human-centric lighting with Wicop and SunLike technologies

Seoul Semiconductor Co., Ltd. is differentiating through spectrum-engineered LED materials and aggressive IP enforcement. Its SunLike LEDs replicate natural sunlight, driving adoption in human-centric lighting and circadian rhythm optimization applications. The Wicop platform eliminates packaging constraints, enabling compact, high-efficiency LED designs for automotive and mobile displays. Its “No-Patent, No-Product” strategy, reinforced by successful global litigation, protects its LED material innovations and secures market share in high-value segments.

Toyoda Gosei integrates LED materials into automotive safety and hydrogen mobility

Toyoda Gosei Co., Ltd. is focusing on automotive LED materials integration, combining GaN-based semiconductors with advanced vehicle lighting systems. Innovations such as Dynamic Shadowy Illumination enhance in-cabin experience, while In-Mold Coating technology reduces emissions in LED-integrated components. Its transition toward carbon-neutral manufacturing and recycled materials aligns with automotive OEM sustainability mandates. The company’s involvement in hydrogen systems and GaN-on-GaN devices positions it at the intersection of advanced LED materials and next-generation mobility platforms.

United States LED Materials Market: MicroLED Scale-Up, Thermal Performance, and Circularity Mandates

The United States LED materials market is entering a phase defined by MicroLED commercialization, advanced thermal management, and materials circularity requirements. Federal semiconductor incentives are accelerating next-generation display infrastructure, exemplified by the USD 40 million grant supporting VuReal’s MicroLED mass-transfer materials and specialized substrates. This push is complemented by material science breakthroughs such as the University of Texas at Austin’s commercialization of a hybrid liquid-metal and aluminum nitride thermal interface material in October 2025, delivering heat dissipation rates three times higher than conventional silicone greases. These advances directly address thermal bottlenecks in high-brightness LEDs and dense pixel architectures used in MicroLED and AI-driven optical systems.

Industrial deployment is reinforcing this trajectory. Henkel commercialized Loctite TCF 14001 for 800G and 1.6T transceivers in October 2025, linking LED and laser materials to AI data center optics. Domestic demand for advanced, PFAS-free LED encapsulants rose 27% in 2025, driven by smart city retrofits. At the substrate level, Navitas Semiconductor expanded GaN-on-silicon manufacturing partnerships to reduce reliance on sapphire for industrial floodlighting. Regulatory modernization adds momentum, as the U.S. Department of Energy’s updated L-Prize criteria require 90% of LED materials in federal contracts to be recyclable or bio-based by 2027, reshaping procurement and formulation strategies.

India LED Materials Market: Policy-Led Localization and Heat-Resilient Materials

India’s LED materials ecosystem is transitioning from assembly-led growth to localized materials manufacturing, anchored by policy execution and mass adoption. Realized investments under the Production Linked Incentive scheme reached ₹1.76 lakh crore by March 2025, catalyzing domestic production lines for LED chip packaging, drivers, and light management systems. The decade-long UJALA program, which distributed 36.87 crore LED bulbs by January 2025, has created a sizable aftermarket for thermal pads and metal core printed circuit board materials, reinforcing demand for reliable, locally sourced inputs.

Public lighting programs are tightening material performance thresholds. The Street Lighting National Program’s plan to replace an additional 1.62 crore street lights prioritizes materials that withstand extreme tropical conditions, including high-purity alumina coatings and ceramic substrates. Semiconductor cluster designations in Gujarat and Telangana during late 2025 offer 50% capital subsidies for plants producing LED phosphors and precursor chemicals such as high-purity ammonia. Private sector innovation is aligning with these needs, as firms like Havells introduced heat-resistant fixtures in 2025 using domestic ceramic substrates engineered for sustained operation above 50°C.

China LED Materials Market: MicroLED Materials Scale and Substrate Cost Disruption

China remains the global epicenter for LED materials scale, with policy backing accelerating the MicroLED transition. The MIIT’s 2026 work plan targets 4.6 to 5.0% growth in high-tech manufacturing, explicitly incentivizing mass-transfer materials critical to MicroLED adoption. By late 2025, more than half of China’s display industry had shifted toward Mini-LED and MicroLED architectures, driving a 40% surge in demand for high-performance optical encapsulants and advanced resins.

Sustainability and cost reduction are converging. BASF completed the transition of its Nanjing specialty chemical portfolio, including LED-grade intermediates, to 100% renewable electricity in October 2025, lowering the carbon footprint of exported resins by 4%. On the substrate front, San'an Optoelectronics reported successful pilots of 8-inch GaN-on-silicon wafers in December 2025, targeting a 20% cost reduction versus sapphire substrates in 2026. These advances reinforce China’s ability to combine scale economics with incremental sustainability gains.

Japan LED Materials Market: GaN-on-Silicon, Quantum Dots, and Rare Earth Circularity

Japan’s LED materials strategy emphasizes precision engineering, spectral performance, and circular supply chains. Toshiba Electronics Europe announced second-generation LETERAS white LEDs using a 200 mm GaN-on-silicon process during 2024–2025, lowering material costs for high-power applications. Strategic alignment with the United States deepened in September 2025 through a USD 550 million investment framework supporting joint R&D in semiconductor-grade LED materials.

Material innovation continues to target high-value applications. Nichia Corporation and Sony showcased non-cadmium quantum dot films at CEATEC 2025, achieving CRI values above 98 for medical lighting. Complementing performance gains, the Ministry of Economy, Trade and Industry launched a 2026 subsidy for urban mining of LED phosphors, enabling recovery of yttrium and europium from decommissioned street lighting and reducing dependence on primary rare earth supply.

LED Materials Market: Country-Level Strategic Snapshot

LED Materials Market County Level Snapshot

|

Country

|

Primary Growth Lever

|

Core Material Focus

|

Strategic Implication

|

|

United States

|

MicroLED and AI optics

|

TIMs, PFAS-free encapsulants, GaN-on-Si

|

Performance leadership under circularity mandates

|

|

India

|

Policy-driven localization

|

MCPCB, alumina coatings, ceramic substrates

|

Heat-resilient materials for mass deployment

|

|

China

|

Scale and cost optimization

|

Optical encapsulants, GaN-on-Si substrates

|

MicroLED cost disruption with sustainability gains

|

|

Japan

|

Precision and circularity

|

GaN-on-Si LEDs, quantum dots, recycled phosphors

|

High-CRI niches and rare earth recovery

|

LED Materials Market Report Scope

LED Materials Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$37.7 Billion

|

|

Market Size (2034)

|

$88.2 Billion

|

|

Market Growth Rate

|

9.9%

|

|

Segments

|

By Material Type (Substrate Materials, Wafer and Epitaxy Materials, Phosphor Materials, Encapsulant Materials, Thermal Interface Materials), By Technology (Standard LED, High-Brightness LED, UV LED, Mini-LED, Micro-LED), By Application (General Lighting, Automotive Lighting, Display Backlighting, Specialized Lighting)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Nichia Corporation, Cree LED, ams OSRAM, Samsung LED, Seoul Semiconductor, Toyoda Gosei, Lumileds Holding, Toshiba Corporation, Epistar Corporation, Dow, Shin-Etsu Chemical, Henkel, Mitsubishi Chemical Group, H.B. Fuller, Sanan Optoelectronics

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

LED Materials Market Segmentation

By Material Type

- Substrate Materials

- Wafer and Epitaxy Materials

- Phosphor Materials

- Encapsulant Materials

- Thermal Interface Materials

By Technology

- Standard LED

- High-Brightness LED

- UV LED

- Mini-LED

- Micro-LED

By Application

- General Lighting

- Automotive Lighting

- Display Backlighting

- Specialized Lighting

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the LED Materials Market

- Nichia Corporation

- Cree LED

- ams OSRAM

- Samsung LED

- Seoul Semiconductor

- Toyoda Gosei

- Lumileds Holding

- Toshiba Corporation

- Epistar Corporation

- Dow

- Shin-Etsu Chemical

- Henkel

- Mitsubishi Chemical Group

- H.B. Fuller

- Sanan Optoelectronics

*- List not Exhaustive