Decorative Depth, Thermal Insulation, and Design-Led Innovation Driving Steady Expansion

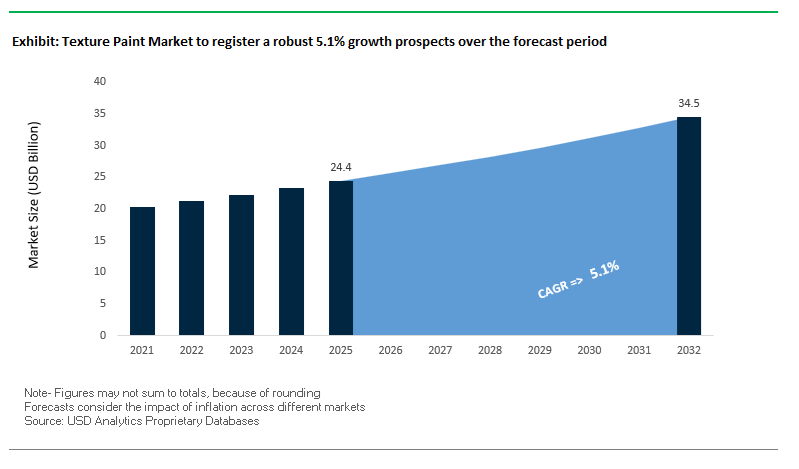

The global Texture Paint Market is expanding steadily, supported by increasing demand for aesthetic surface finishes, architectural customization, and performance-enhancing wall coatings across residential, commercial, and industrial applications. The market was valued at $24.4 billion in 2025 and is projected to reach $34.6 billion by 2032, growing at a CAGR of 5.1% during 2025–2032. This growth is driven by the rising importance of design differentiation, durability, and multi-functional wall systems in modern construction and renovation projects.

A primary structural driver is the growing adoption of decorative textured coatings that combine visual depth with functional benefits, including crack-bridging, moisture resistance, and thermal insulation. These coatings are widely used in facades, interior walls, and exterior insulation systems, particularly in regions with harsh climatic conditions where durability and insulation are critical. The increasing focus on energy-efficient buildings is further accelerating demand for textured coatings integrated with external wall insulation systems (EWIS).

Another key trend is the shift toward premium and customized finishes, where texture paints are used to replicate materials such as natural stone, marble, concrete, and silk. This trend is particularly prominent in luxury residential and commercial spaces, where coatings serve as a design statement rather than just a protective layer. Additionally, advancements in mineral-based and eco-friendly formulations are aligning the market with sustainability goals, offering low-VOC and breathable solutions for modern construction.

The market is also witnessing the integration of digital tools and application technologies, enabling precise texture replication and customization. This is particularly relevant in automotive and industrial segments, where texture coatings are used to restore or replicate original surface finishes. Overall, the market is evolving toward design-driven, high-performance, and technologically enabled coating systems.

Market Analysis: Digital Texture Matching, Architectural Insulation Systems, and Premium Design Collaborations Reshaping Market Dynamics

The texture paint market is being reshaped by technological innovation, strategic consolidation, and design-centric product development, reflecting the growing convergence of functionality and aesthetics. In January 2026, PPG, through its SEM® Products division, launched a next-generation texture refinishing system in collaboration with 4PLASTIC. This system enables automotive repair professionals to replicate OEM textures on plastic components using a mobile app for precise texture matching, reducing replacement costs and supporting sustainability by minimizing plastic waste.

Industry consolidation is also influencing competitive dynamics. The March 2026 merger of equals between AkzoNobel and Axalta creates a global coatings powerhouse with a strengthened portfolio in textured finishes across mobility, industrial, and decorative segments, enabling enhanced R&D capabilities for next-generation tactile coatings.

In the construction sector, Sto SE’s recognition as the global leader in External Wall Insulation Systems (January 2026) highlights the growing importance of textured facade coatings integrated with thermal insulation technologies. The company’s focus on “intelligent” textured renders demonstrates the increasing demand for coatings that deliver both aesthetic appeal and energy efficiency.

Design-driven innovation is accelerating in premium segments. Asian Paints’ ColourNext 2026 forecast (March 2026) introduces trends such as “Solarpunk” and “Moonlit Silk”, emphasizing the use of advanced mineral and silk-effect textures to reflect evolving consumer preferences. Similarly, Jotun’s “Soulful Spaces” 2026 collection showcases hand-crafted, natural-looking textures that mimic stone and plaster finishes, catering to the growing demand for bespoke interior designs.

Regional expansion is strengthening market penetration. Sto SE’s July 2025 expansion into Australia localizes production of textured facade systems, supporting demand in the Australasian construction sector. Meanwhile, Nippon Paint’s 2024–2026 strategic roadmap focuses on developing tropical climate-resistant textured coatings, addressing durability challenges in high-humidity regions.

Advanced pigment technologies are also redefining surface aesthetics. BASF’s 2025–2026 “Driving the Proxy” collection introduces coatings that create a perceived depth and texture on smooth surfaces, bridging the gap between visual and tactile experiences.

Collaborations are further elevating the role of texture in design. Asian Paints’ partnership with designer Manish Malhotra (November 2024) positions textured coatings as a core element of luxury architecture, moving beyond traditional applications into high-end design narratives. Additionally, Sherwin-Williams’ 2026 Color of the Year initiative integrates texture trends such as matte finishes and structured wall treatments, reinforcing the synergy between color and texture in contemporary design.

Market Trend: U.S. GSA Buy Clean Mandates Drive Low-Carbon Texture Paint Adoption in Federal Projects

The expansion of the U.S. General Services Administration’s Buy Clean initiative under the 2025/2026 P100 Facilities Standards is significantly influencing the specification of texture paints in public-sector construction. Federal procurement is increasingly prioritizing materials with reduced embodied carbon, extending beyond structural components to include high-volume finishing materials such as architectural coatings. As of January 2026, contractors involved in federal modernization projects exceeding $5 million are required to submit product-specific Type III Environmental Product Declarations, demonstrating at least a 20% reduction in Global Warming Potential compared to industry benchmarks. This requirement is reshaping formulation strategies, with manufacturers integrating bio-based binders, recycled mineral fillers, and low-energy processing techniques to meet carbon reduction targets. Additionally, the allocation of $2.15 billion in Inflation Reduction Act funding toward low-embodied carbon materials is accelerating the adoption of sustainable texture paints in federal buildings, including courthouses and administrative offices. The growing emphasis on carbon transparency and lifecycle assessment is positioning low-carbon texture coatings as a key competitive differentiator in large-scale institutional projects.

Market Trend: China GB/T 41651-2024 Redefines Texture Paint Performance for High-Rise Urban Applications

China’s GB/T 41651-2024 standard, fully implemented by late 2025, is introducing a new level of technical rigor to the texture paint market by shifting from aesthetic classification to performance-based evaluation. The standard establishes minimum thresholds for adhesion, durability, and crack resistance, particularly for exterior applications in high-density urban environments. Texture paints must now achieve a tensile bond strength of at least 0.7 MPa after water immersion, ensuring that thick-film coatings remain securely bonded under conditions of high humidity and thermal cycling typical of coastal megacities. In parallel, the standard mandates dynamic crack resistance of at least 0.30 mm, addressing a critical failure mode associated with heavy-bodied coatings applied to masonry substrates. These requirements are driving the adoption of advanced polymer systems and fiber-reinforced formulations that provide enhanced flexibility and crack-bridging capabilities. As urban infrastructure projects continue to scale across Asia, compliance with GB/T 41651-2024 is becoming essential for manufacturers seeking to participate in high-rise construction and façade renovation projects.

Market Opportunity: Antimicrobial Texture Paints Gain Traction in Healthcare and Educational Infrastructure

The increasing emphasis on indoor environmental quality and occupant health is creating strong demand for antimicrobial texture paints in high-traffic facilities such as hospitals, schools, and public institutions. Driven by building certification frameworks such as WELL v2 and Fitwel, antimicrobial functionality is transitioning from a niche feature to a baseline requirement in interior coatings. Advanced formulations developed in 2026 are capable of achieving greater than 99.9% reduction in common pathogens, including Staphylococcus aureus and Escherichia coli, within 24 hours of contact, as validated by ISO 22196 testing protocols. These coatings utilize non-leaching antimicrobial agents, such as silver-ion and quaternary ammonium compounds, ensuring long-term efficacy without compromising environmental safety. In addition to antimicrobial performance, innovations in surface engineering are reducing the inherent porosity of textured finishes. Nanostructured fillers are being incorporated to minimize micro-voids that can harbor contaminants, resulting in an estimated 40% reduction in bio-load retention compared to conventional sand-textured coatings. As public health considerations continue to influence building design and material selection, antimicrobial texture paints are emerging as a critical solution for maintaining hygienic indoor environments.

Market Opportunity: Ultra-Low VOC Waterborne Texture Paints Enable Compliance with LEED v4.1 and Global Green Building Standards

The global shift toward green building certifications is driving rapid innovation in low-VOC waterborne texture paint systems. Under LEED v4.1 and updated BREEAM standards, the acceptable VOC threshold for interior coatings has effectively been reduced to 50 g/L, presenting a technical challenge for texture paints that traditionally rely on high-solids formulations. In response, manufacturers are developing advanced waterborne resin systems capable of delivering VOC levels below 30 g/L while maintaining high performance characteristics. These coatings are designed to meet stringent indoor air quality requirements, including compliance with the CDPH Standard Method v1.2, which limits total VOC emissions to 0.5 mg/m³ after a 14-day curing period. At the same time, innovations in polymer chemistry are enabling these low-VOC systems to achieve Class 1 scrub resistance under EN 13300, ensuring durability in high-traffic interior environments. Another emerging trend is the incorporation of bio-based carbon content, measured using ASTM D6866, as architects and developers increasingly prioritize materials with reduced carbon footprints. With more than 60% of leading architectural firms actively specifying bio-based content in 2026, ultra-low VOC waterborne texture paints are positioned as a key enabler of sustainable interior design and certification compliance.

Texture Paint Market Share and Segmentation Insights: Product Segment Dominance and Growth Drivers

Sand Texture Paint Leads the Global Texture Coatings Market with 25.9% Share

The sand texture paint segment dominates the global texture paint market in 2025, capturing 25.9% market share, making it the most widely adopted product type across both residential and commercial applications. This leadership is driven by its cost-effective pricing, versatility, and superior ability to conceal wall imperfections, positioning it as a preferred alternative to more expensive finishes such as stucco, Venetian plaster, and knockdown textures. In the broader decorative coatings and textured wall finishes market, sand texture paints are extensively used for interior walls, exterior facades, and renovation projects, benefiting from strong demand in both developed and emerging markets. Additionally, the segment gains traction due to its easy application methods—roller, spray, or trowel—making it highly DIY-friendly, a key trend in the home improvement and remodeling sector. The availability of pre-mixed formulations further boosts adoption among homeowners and contractors, reinforcing its leadership within the architectural coatings and wall texture solutions market.

Home Improvement Centers Capture 40.9% Share as Primary Texture Paint Sales Channel

In the texture paint market by sales channel, home improvement centers hold the largest share at 40.9% in 2025, driven by strong consumer preference for DIY home renovation and convenient retail access. These large-format retailers dominate distribution within the decorative paint and coatings market, as homeowners increasingly purchase texture paints for accent walls, ceiling repairs, and small-scale remodeling projects. The segment benefits from high product visibility, competitive pricing, and extensive in-store inventory, including popular finishes such as sand texture, orange peel, and popcorn coatings. Furthermore, home improvement centers offer extended operating hours, bundled product solutions, and expert guidance, enhancing customer experience and boosting repeat purchases. The rise of weekend DIY projects and home décor trends continues to fuel foot traffic, making this channel a critical revenue driver in the global texture paint distribution landscape. Its dominance also reflects shifting consumer behavior toward one-stop retail destinations for paints, tools, and surface finishing solutions.

Competitive Landscape Analysis of the Texture Paint Market

Sherwin-Williams Strengthening Contractor-Driven Texture Paint Demand in North America

The Sherwin-Williams Company continues to dominate the texture paint market through strong performance in its Paint Stores Group, reporting a 6.8% increase in net sales during 2025–2026. This growth is largely driven by professional contractors seeking high-performance architectural coatings and textured finishes. The company leads the North American residential MRO coatings segment, offering “imperfection-masking” texture paints that can reduce structural labor costs by up to 15%. Its expanded Emerald® and Duration® product lines now feature advanced texture additives that enhance crack resistance and hide surface defects. With over 4,800 company-operated stores, Sherwin-Williams ensures rapid delivery of customized decorative texture paint solutions, reinforcing its distribution advantage.

AkzoNobel Innovating Thermo-Sensitive and Energy-Efficient Texture Coatings

AkzoNobel N.V. is advancing the texture paint market through cutting-edge innovations in thermo-sensitive coatings and sustainable decorative paints. In 2026, the company introduced its “Rhythm of Blues” Color of the Year collection, featuring texture technologies like Mellow Flow™, Slow Swing™, and Free Groove™ that dynamically adjust visual depth based on ambient lighting. Its partnership with IPG Photonics has enabled laser-curing technology for powder-based textures, reducing energy consumption by 30% in industrial applications. Financially, AkzoNobel achieved a 14.2% adjusted EBITDA margin in 2025, reflecting its focus on high-margin decorative coatings. Additionally, its role in Calosol heat-absorbing façade technology positions it as a leader in energy-efficient textured surfaces.

Asian Paints Dominating Asia-Pacific Decorative Texture Paint Segment

Asian Paints Limited holds a commanding 46.1% share of the Asia-Pacific texture paint market, driven by rapid urbanization and rising demand for premium interior finishes. Its Royale Play series remains the benchmark for luxury decorative texture coatings, offering effects like Marmorino, Dune, and Archi-Concrete for the global high-end residential segment. In 2026, the company introduced “Moonlit Silk,” aligning with quiet luxury and biophilic design trends in modern interiors. Asian Paints is also investing heavily in Solar Punk ecological coatings, focusing on carbon-neutral and green building solutions. This strategic direction strengthens its leadership in sustainable decorative paints and advanced textured finishes across emerging markets.

Nippon Paint Expanding Specialty Texture Coatings Through Strategic Acquisitions

Nippon Paint Holdings Co., Ltd. is strengthening its position in the global texture paint market through a disciplined M&A strategy focused on specialty chemicals. Adopting a “Holistic ROIC-conscious framework,” the company is enhancing the durability of its Stone Paint and exterior texture coatings portfolios. Despite raw material volatility, Nippon Paint targets mid-single-digit revenue growth and high-single-digit EPS growth for 2025–2026. It is also expanding into automotive and industrial texture coatings, particularly EV-related applications with a 15% market share goal in thermal management components. Its decentralized “Partner Company” model enables rapid, localized innovation in key regions like China and Oceania, boosting its competitiveness.

Kansai Paint Driving Sustainable Expansion in Emerging Texture Paint Markets

Kansai Paint Co., Ltd. is accelerating growth in the texture paint market through strategic investments and sustainability initiatives. The company has allocated JPY 100 billion for mergers and acquisitions between 2025 and 2027, targeting high-growth regions in Africa and the Middle East. In 2025, Kansai Paint introduced bio-based resins that reduce the carbon footprint of decorative texture coatings by 40%, aligning with global sustainability trends. Its expansion of the Plascon brand distribution network by 20% in Africa by 2026 positions the company to capitalize on infrastructure development. These efforts reinforce Kansai Paint’s role in delivering eco-friendly textured coatings and scalable decorative paint solutions in emerging markets.

China’s Transition Toward Smart Façade Texture Paints and Sustainable Urban Coatings

China is rapidly evolving within the texture paint market by shifting from conventional sand-finish coatings to multi-functional architectural texture paints aligned with its sustainable urbanization goals. A key technological breakthrough in 2026 includes the localization of self-cleaning photocatalytic texture coatings, which leverage ambient UV light to break down organic pollutants on building exteriors—significantly improving air quality and reducing maintenance.

Government-backed initiatives such as the National Green Building Label System (2025–2026) are accelerating the adoption of thermal-insulating texture paints, contributing to reduced cooling loads in high-rise structures. Strategic investments, including AkzoNobel’s expansion of water-based texture paint production in Shanghai, highlight the growing demand for low-VOC decorative coatings. Infrastructure developments across Beijing and Shenzhen metro systems have driven widespread use of anti-graffiti texture coatings, enhancing durability in high-traffic public spaces. Additionally, thick-film elastic texture paints are being deployed on prefabricated housing units to improve crack resistance and weatherproofing. Regulatory enforcement of low-toxicity coating formulations is further pushing the industry toward sustainable solutions.

India’s Premiumization Trend and Climate-Resilient Texture Coatings Growth

India’s texture paint market is undergoing a significant transformation driven by premium decorative coatings demand and climate-resilient innovations. Consumers are increasingly shifting toward textured wall finishes that provide aesthetic appeal along with durability, particularly in urban residential and hospitality sectors.

Industry expansion is supported by major developments such as JSW Paints’ strategic acquisition to strengthen its supply chain for high-performance coatings. Leading companies like Asian Paints and Berger Paints are scaling production of quartz-based texture coatings and additives, enabling advanced finishes tailored for local conditions. Product innovation is focused on hydrophobic “lotus-effect” texture paints, designed to withstand monsoon climates by preventing water penetration and algae formation.

Government housing initiatives under Pradhan Mantri Awas Yojana are boosting demand for exterior texture coatings in large-scale residential projects. Technological advancements include the integration of fire-retardant additives into interior texture coatings, ensuring compliance with updated fire safety standards. High adoption of sand-textured and metallic finish coatings in luxury hotels and resorts is further strengthening India’s position as a growing hub for premium texture paints.

United States Driving Innovation in Application Systems and Eco-Friendly Texture Paints

The United States is shaping the texture paint market through advancements in application technologies, sustainability, and renovation-driven demand. The introduction of adjustable aerosol nozzle systems in 2026 allows users to achieve professional-grade finishes such as “orange peel” and “knockdown” textures, enhancing DIY and contractor efficiency.

Regulatory pressure from the EPA’s Clean Air Act updates is accelerating the transition to bio-renewable and zero-VOC texture coatings, especially in colder regions where oil-based formulations were traditionally dominant. Government-led infrastructure retrofitting programs are promoting the use of recycled-content texture coatings to improve building insulation and acoustic performance.

Significant investments, including Sherwin-Williams’ advanced R&D facility, are enabling the development of smart texture coatings that can visually indicate moisture intrusion behind walls. Product innovations such as quick-dry water-based texture aerosols are supporting the booming residential renovation market. Additionally, the adoption of anti-slip texture coatings for commercial walkways and healthcare facilities highlights the functional diversification of texture paints across industries.

Saudi Arabia’s High-Performance Texture Coatings for Extreme Climate Infrastructure

Saudi Arabia is emerging as a critical market for high-durability texture coatings, driven by large-scale infrastructure projects under Vision 2030. The country’s extreme climate conditions are fueling demand for UV-resistant and heat-reflective texture paints capable of withstanding high surface temperatures and desert environments.

Major infrastructure developments, including the NEOM “The Line” project, are utilizing polysiloxane-based texture coatings for superior thermal resistance and long-term durability. Government mandates requiring high Solar Reflectance Index (SRI) coatings are addressing urban heat island effects, further boosting adoption of advanced texture paints.

Product innovation in sand-abrasion resistant coatings is addressing challenges posed by sandstorms, while local production expansions by Jotun and Al-Jazeera Paints are strengthening supply chain capabilities. Applications such as texture-coated aluminum panels in airport expansions highlight the importance of non-glare, safety-enhancing coatings in aviation infrastructure. Regulatory standards like the SASO “Durability Grade” are ensuring long-lasting, maintenance-free coating solutions for public projects.

Germany’s Focus on Acoustic and Sustainable Texture Paint Technologies

Germany is leading innovation in functional texture coatings, particularly in acoustic performance and sustainable construction. The development of micro-porous acoustic texture paints capable of improving sound absorption is gaining traction in commercial and residential applications, especially in urban environments.

Product innovation includes invisible mineral-based texture repair coatings, enabling seamless restoration of historic structures without altering their original appearance. Regulatory frameworks under the EU’s Ecodesign standards are promoting transparency through digital product passports, ensuring sustainability and recyclability of coating materials.

Investments by BASF in advanced production facilities are enhancing the development of low-carbon texture resins, aligning with Europe’s environmental goals. Germany also dominates in hygienic and chemical-resistant texture coatings for pharmaceutical and laboratory settings. Additionally, companies like Sto SE are advancing bio-inspired texture coatings, reflecting cutting-edge research in functional surface engineering.

Japan’s Nano-Functional Texture Paints for Smart Living Environments

Japan is pioneering nano-functional texture paint technologies, focusing on enhancing indoor air quality and supporting aging populations. Innovations such as nano-silica infused texture coatings are capable of absorbing indoor pollutants like formaldehyde and neutralizing odors, contributing to healthier living environments.

Technological advancements include ultra-thin texture films designed for prefabricated housing, enabling precise and efficient application of decorative patterns in controlled manufacturing environments. Product innovations such as “safe-touch” texture coatings are being widely adopted in elderly care facilities, improving safety through non-slip, tactile surfaces.

Industrial expansion includes specialized clean-room production facilities catering to demand for anti-static and dust-resistant texture coatings, particularly in semiconductor environments. Updated Japanese Industrial Standards (JIS) are reinforcing quality by mandating performance metrics such as moisture vapor transmission, ensuring long-term durability and mold prevention. Japan’s luxury retail sector is also driving demand for metallic and silk-effect texture coatings, emphasizing aesthetic refinement and premium finishes.

Texture Paint Market Report Scope

Texture Paint Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$24.4 Billion

|

|

Market Size (2032)

|

$34.6 Billion

|

|

Market Growth Rate

|

5.1%

|

|

Segments

|

By Product (Sand Texture, Smooth Texture, Orange Peel and Knockdown, Popcorn, Stucco and Venetian Plaster, Roll-on and Self-Mixing Textures), By Technology (Water-Based Technology, Solvent-Based Technology, Additive-based), By Application Area (Interior Texture Paints, Exterior Texture Paints, Ceiling-specific Textures), By Substrate (Drywall and Plaster, Concrete and Masonry, Wood Surfaces, Metal Surfaces), By End-User Industry (Residential, Commercial, Institutional, Industrial), By Sales Channel (Direct Sales, Specialty Paint and Decor Stores, Home Improvement Centers, E-commerce)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

The Sherwin-Williams Company, PPG Industries, Inc., Akzo Nobel N.V., Nippon Paint Holdings Co., Ltd., Asian Paints Limited, Jotun A/S, RPM International Inc., Kansai Paint Co., Ltd., Berger Paints India Limited, Hempel A/S, Sika AG, Mapei S.p.A., Behr Process Corporation, Benjamin Moore and Co., Kelly-Moore Paints

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Texture Paint Market Segmentation

By Product

- Sand Texture

- Smooth Texture

- Orange Peel and Knockdown

- Popcorn

- Stucco and Venetian Plaster

- Roll-on and Self-Mixing Textures

By Technology

- Water-Based Technology

- Solvent-Based Technology

- Additive-based

By Application Area

- Interior Texture Paints

- Exterior Texture Paints

- Ceiling-specific Textures

By Substrate

- Drywall and Plaster

- Concrete and Masonry

- Wood Surfaces

- Metal Surfaces

By End-User Industry

- Residential

- Commercial

- Institutional

- Industrial

By Sales Channel

- Direct Sales

- Specialty Paint and Decor Stores

- Home Improvement Centers

- E-commerce

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Texture Paint Industry

- The Sherwin-Williams Company

- PPG Industries, Inc.

- Akzo Nobel N.V.

- Nippon Paint Holdings Co., Ltd.

- Asian Paints Limited

- Jotun A/S

- RPM International Inc.

- Kansai Paint Co., Ltd.

- Berger Paints India Limited

- Hempel A/S

- Sika AG

- Mapei S.p.A.

- Behr Process Corporation

- Benjamin Moore & Co.

- Kelly-Moore Paints

*- List not Exhaustive