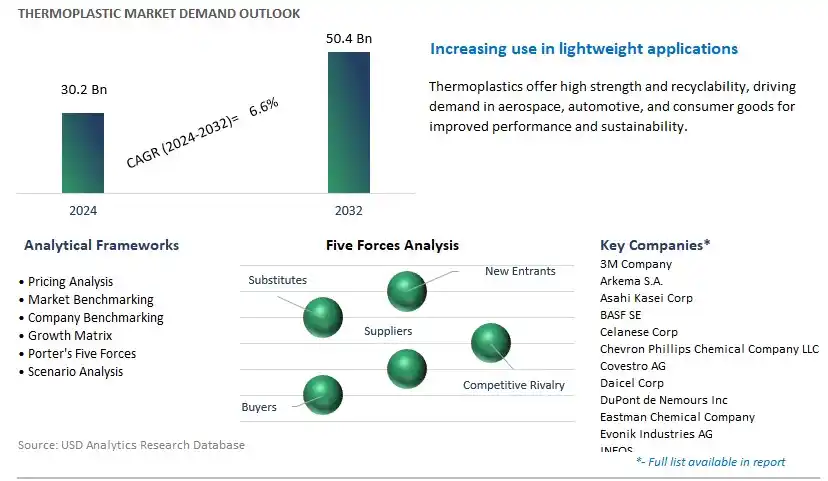

Global Thermoplastic Market Size is valued at $30.2 Billion in 2024 and is forecast to register a growth rate (CAGR) of 6.6% to reach $50.4 Billion by 2032.

The global Thermoplastic Market Study analyzes and forecasts the market size across 6 regions and 24 countries for diverse segments -By Product (Commodity Thermoplastics, Engineering Thermoplastics, High-performance Engineering Thermoplastics, Others), By End-User (Packaging, Building and Construction, Automotive and Transportation, Electrical and Electronics, Sports and Leisure, Medical, Others).

An Introduction to Thermoplastic Market in 2024

Thermoplastics constitute a versatile class of polymers characterized by their ability to soften and mold upon heating, solidifying upon cooling without undergoing chemical change. This unique property enables thermoplastics to be reshaped and recycled multiple times, making them indispensable in various industries, including automotive, packaging, and construction. From lightweight components in automobiles to durable packaging materials and flexible piping systems, thermoplastics offer a wide array of applications, driven by their exceptional mechanical properties, chemical resistance, and ease of processing. With growing emphasis on sustainability and circular economy principles, the demand for recyclable thermoplastics s to soar, prompting innovations in material development, processing technologies, and end-of-life solutions.

Thermoplastic Market Competitive Landscape

The market report analyses the leading companies in the industry including 3M Company, Arkema S.A., Asahi Kasei Corp, BASF SE, Celanese Corp, Chevron Phillips Chemical Company LLC, Covestro AG, Daicel Corp, DuPont de Nemours Inc, Eastman Chemical Company, Evonik Industries AG, INEOS, Lanxess AG, LG Chem Ltd, LyondellBasell Industries Holdings BV, Mitsubishi Engineering-Plastics Corp, Polyplastics Co. Ltd, Royal DSM N.V., SABIC, Solvay SA, Teijin Ltd, and others.

Thermoplastic Market Dynamics

Market Trend: Increasing Adoption of Thermoplastics in 3D Printing and Additive Manufacturing

A significant trend in the thermoplastic market is the growing adoption of these materials in 3D printing and additive manufacturing processes. Thermoplastics offer versatility, ease of processing, and recyclability, making them ideal for additive manufacturing applications where complex geometries, customization, and rapid prototyping are required. With advancements in 3D printing technology and material formulations, thermoplastics are being used to produce a wide range of end-use parts, components, and products across industries such as automotive, aerospace, healthcare, and consumer goods. The ability to manufacture lightweight, durable, and high-performance parts on-demand using thermoplastics is driving their increasing utilization in additive manufacturing, shaping the future of the market.

Market Driver: Demand for Lightweight, Sustainable, and High-Performance Materials

The primary driver behind the growth of the thermoplastic market is the increasing demand for lightweight, sustainable, and high-performance materials across various industries. Thermoplastics offer several advantages over traditional materials such as metals, including reduced weight, corrosion resistance, design flexibility, and recyclability. In industries such as automotive and aerospace, where fuel efficiency, emissions reduction, and environmental sustainability are paramount, thermoplastics are being increasingly adopted to replace heavier materials and optimize component performance. Moreover, the demand for thermoplastics is driven by their versatility and suitability for a wide range of applications, including packaging, construction, medical devices, electronics, and consumer goods. As industries continue to prioritize material innovation and sustainability, the demand for thermoplastics as preferred materials for lightweight, sustainable, and high-performance applications is expected to drive market growth.

Market Opportunity: Development of Bio-based and Recycled Thermoplastics

An opportunity for the thermoplastic market lies in the development of bio-based and recycled thermoplastics to meet the growing demand for sustainable materials. With increasing environmental concerns and regulations aimed at reducing plastic waste and carbon emissions, there is a rising interest in bio-based polymers derived from renewable sources such as plants, biomass, and waste materials. Manufacturers have the opportunity to invest in research and development initiatives focused on bio-based thermoplastics that offer comparable performance to traditional petroleum-based thermoplastics while reducing reliance on fossil fuels and mitigating environmental impact. Additionally, there is potential to develop recycled thermoplastics from post-consumer and post-industrial waste streams, contributing to a circular economy and addressing plastic pollution challenges. By offering bio-based and recycled thermoplastics as sustainable alternatives to conventional materials, the thermoplastic market can capitalize on opportunities to align with sustainability goals, meet customer demands for eco-friendly solutions, and differentiate its product offerings in the market.

Thermoplastic Market Share Analysis: Commodity Thermoplastics segment generated the highest revenue in 2024

Within thermoplastic market segmented by product, commodity thermoplastics emerge as the largest segment, commanding a significant share due to their widespread use and versatility in various industries. Commodity thermoplastics are widely used in everyday consumer products and packaging due to their low cost, ease of processing, and desirable physical properties. These thermoplastics include polymers such as polyethylene (PE), polypropylene (PP), polyvinyl chloride (PVC), and polystyrene (PS), among others. They find applications in packaging, consumer goods, construction materials, and automotive components, among others. The high demand for commodity thermoplastics is driven by their affordability, availability, and adaptability to a wide range of manufacturing processes, making them indispensable in numerous applications. Additionally, the growing population, urbanization, and industrialization further fuel the demand for commodity thermoplastics, as they are essential materials for meeting the needs of a growing global economy. As industries continue to innovate and expand, the demand for commodity thermoplastics is expected to remain robust, solidifying its position as the largest segment in thermoplastic market.

Thermoplastic Market Share Analysis: Packaging is poised to register the fastest CAGR over the forecast period

Among the segments delineated within thermoplastic market by end-user, the packaging industry is the fastest-growing segment, catalyzing significant advancements in packaging materials and solutions. Thermoplastics are extensively utilized in the packaging sector due to their versatility, lightweight nature, durability, and ability to be molded into various shapes and sizes. The demand for thermoplastics in packaging applications is driven by the increasing consumption of packaged goods, rising e-commerce activities, and the growing emphasis on sustainable packaging solutions. Thermoplastics offer manufacturers and brand owners the flexibility to design innovative and functional packaging solutions that meet consumer preferences while ensuring product protection and shelf appeal. Additionally, the recyclability and recyclable properties of thermoplastics align with the sustainability goals of the packaging industry, further driving their adoption. As the packaging sector continues to evolve to meet the dynamic needs of consumers and regulatory requirements, the demand for thermoplastics is expected to witness rapid growth, positioning packaging as the fastest-growing segment in thermoplastic market.

Thermoplastic Market

By Product

Commodity Thermoplastics

-Polyethylene (PE)

-Polypropylene (PP)

-Polyvinyl chloride (PVC)

-Polystyrene (PS)

Engineering Thermoplastics

-Polyamide (PA)

-Polycarbonates (PC)

-Polymethyl methacrylate (PMMA)

-Polyoxymethylene (POM)

-Polyethylene terephthalate (PET)

-Polybutylene terephthalate (PBT)

-Acrylonitrile Butadiene Styrene (ABS)/Styrene Acrylonitrile (SAN)

High-performance Engineering Thermoplastics

-Polyether Ether Ketone (PEEK)

-Liquid Crystal Polymer (LCP)

-Polytetrafluoroethylene (PTFE)

-Polyimide (PI)

Others

By End-User

Packaging

Building and Construction

Automotive and Transportation

Electrical and Electronics

Sports and Leisure

Medical

Others

Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Thermoplastic Companies Profiled in the Study

3M Company

Arkema S.A.

Asahi Kasei Corp

BASF SE

Celanese Corp

Chevron Phillips Chemical Company LLC

Covestro AG

Daicel Corp

DuPont de Nemours Inc

Eastman Chemical Company

Evonik Industries AG

INEOS

Lanxess AG

LG Chem Ltd

LyondellBasell Industries Holdings BV

Mitsubishi Engineering-Plastics Corp

Polyplastics Co. Ltd

Royal DSM N.V.

SABIC

Solvay SA

Teijin Ltd

*- List Not Exhaustive

TABLE OF CONTENTS

1 Introduction to 2024 Thermoplastic Market

1.1 Market Overview

1.2 Quick Facts

1.3 Scope/Objective of the Study

1.4 Market Definition

1.5 Countries and Regions Covered

1.6 Units, Currency, and Conversions

1.7 Industry Value Chain

2 Research Methodology

2.1 Market Size Estimation

2.2 Sources and Research Methodology

2.3 Data Triangulation

2.4 Assumptions and Limitations

3 Executive Summary

3.1 Global Thermoplastic Market Size Outlook, $ Million, 2021 to 2032

3.2 Thermoplastic Market Outlook by Type, $ Million, 2021 to 2032

3.3 Thermoplastic Market Outlook by Product, $ Million, 2021 to 2032

3.4 Thermoplastic Market Outlook by Application, $ Million, 2021 to 2032

3.5 Thermoplastic Market Outlook by Key Countries, $ Million, 2021 to 2032

4 Market Dynamics

4.1 Key Driving Forces of Thermoplastic Industry

4.2 Key Market Trends in Thermoplastic Industry

4.3 Potential Opportunities in Thermoplastic Industry

4.4 Key Challenges in Thermoplastic Industry

5 Market Factor Analysis

5.1 Value Chain Analysis

5.2 Competitive Landscape

5.2.1 Global Thermoplastic Market Share by Company (%), 2023

5.2.2 Product Offerings by Company

5.3 Porter’s Five Forces Analysis

5.4 Pricing Analysis and Outlook

6 Growth Outlook Across Scenarios

6.1 Growth Analysis-Case Scenario Definitions

6.2 Low Growth Scenario Forecasts

6.3 Reference Growth Scenario Forecasts

6.4 High Growth Scenario Forecasts

7 Global Thermoplastic Market Outlook by Segments

7.1 Thermoplastic Market Outlook by Segments, $ Million, 2021- 2032

By Product

Commodity Thermoplastics

-Polyethylene (PE)

-Polypropylene (PP)

-Polyvinyl chloride (PVC)

-Polystyrene (PS)

Engineering Thermoplastics

-Polyamide (PA)

-Polycarbonates (PC)

-Polymethyl methacrylate (PMMA)

-Polyoxymethylene (POM)

-Polyethylene terephthalate (PET)

-Polybutylene terephthalate (PBT)

-Acrylonitrile Butadiene Styrene (ABS)/Styrene Acrylonitrile (SAN)

High-performance Engineering Thermoplastics

-Polyether Ether Ketone (PEEK)

-Liquid Crystal Polymer (LCP)

-Polytetrafluoroethylene (PTFE)

-Polyimide (PI)

Others

By End-User

Packaging

Building and Construction

Automotive and Transportation

Electrical and Electronics

Sports and Leisure

Medical

Others

8 North America Thermoplastic Market Analysis and Outlook To 2032

8.1 Introduction to North America Thermoplastic Markets in 2024

8.2 North America Thermoplastic Market Size Outlook by Country, 2021-2032

8.2.1 United States

8.2.2 Canada

8.2.3 Mexico

8.3 North America Thermoplastic Market size Outlook by Segments, 2021-2032

By Product

Commodity Thermoplastics

-Polyethylene (PE)

-Polypropylene (PP)

-Polyvinyl chloride (PVC)

-Polystyrene (PS)

Engineering Thermoplastics

-Polyamide (PA)

-Polycarbonates (PC)

-Polymethyl methacrylate (PMMA)

-Polyoxymethylene (POM)

-Polyethylene terephthalate (PET)

-Polybutylene terephthalate (PBT)

-Acrylonitrile Butadiene Styrene (ABS)/Styrene Acrylonitrile (SAN)

High-performance Engineering Thermoplastics

-Polyether Ether Ketone (PEEK)

-Liquid Crystal Polymer (LCP)

-Polytetrafluoroethylene (PTFE)

-Polyimide (PI)

Others

By End-User

Packaging

Building and Construction

Automotive and Transportation

Electrical and Electronics

Sports and Leisure

Medical

Others

9 Europe Thermoplastic Market Analysis and Outlook To 2032

9.1 Introduction to Europe Thermoplastic Markets in 2024

9.2 Europe Thermoplastic Market Size Outlook by Country, 2021-2032

9.2.1 Germany

9.2.2 France

9.2.3 Spain

9.2.4 United Kingdom

9.2.4 Italy

9.2.5 Russia

9.2.6 Norway

9.2.7 Rest of Europe

9.3 Europe Thermoplastic Market Size Outlook by Segments, 2021-2032

By Product

Commodity Thermoplastics

-Polyethylene (PE)

-Polypropylene (PP)

-Polyvinyl chloride (PVC)

-Polystyrene (PS)

Engineering Thermoplastics

-Polyamide (PA)

-Polycarbonates (PC)

-Polymethyl methacrylate (PMMA)

-Polyoxymethylene (POM)

-Polyethylene terephthalate (PET)

-Polybutylene terephthalate (PBT)

-Acrylonitrile Butadiene Styrene (ABS)/Styrene Acrylonitrile (SAN)

High-performance Engineering Thermoplastics

-Polyether Ether Ketone (PEEK)

-Liquid Crystal Polymer (LCP)

-Polytetrafluoroethylene (PTFE)

-Polyimide (PI)

Others

By End-User

Packaging

Building and Construction

Automotive and Transportation

Electrical and Electronics

Sports and Leisure

Medical

Others

10 Asia Pacific Thermoplastic Market Analysis and Outlook To 2032

10.1 Introduction to Asia Pacific Thermoplastic Markets in 2024

10.2 Asia Pacific Thermoplastic Market Size Outlook by Country, 2021-2032

10.2.1 China

10.2.2 India

10.2.3 Japan

10.2.4 South Korea

10.2.5 Indonesia

10.2.6 Malaysia

10.2.7 Australia

10.2.8 Rest of Asia Pacific

10.3 Asia Pacific Thermoplastic Market size Outlook by Segments, 2021-2032

By Product

Commodity Thermoplastics

-Polyethylene (PE)

-Polypropylene (PP)

-Polyvinyl chloride (PVC)

-Polystyrene (PS)

Engineering Thermoplastics

-Polyamide (PA)

-Polycarbonates (PC)

-Polymethyl methacrylate (PMMA)

-Polyoxymethylene (POM)

-Polyethylene terephthalate (PET)

-Polybutylene terephthalate (PBT)

-Acrylonitrile Butadiene Styrene (ABS)/Styrene Acrylonitrile (SAN)

High-performance Engineering Thermoplastics

-Polyether Ether Ketone (PEEK)

-Liquid Crystal Polymer (LCP)

-Polytetrafluoroethylene (PTFE)

-Polyimide (PI)

Others

By End-User

Packaging

Building and Construction

Automotive and Transportation

Electrical and Electronics

Sports and Leisure

Medical

Others

11 South America Thermoplastic Market Analysis and Outlook To 2032

11.1 Introduction to South America Thermoplastic Markets in 2024

11.2 South America Thermoplastic Market Size Outlook by Country, 2021-2032

11.2.1 Brazil

11.2.2 Argentina

11.2.3 Rest of South America

11.3 South America Thermoplastic Market size Outlook by Segments, 2021-2032

By Product

Commodity Thermoplastics

-Polyethylene (PE)

-Polypropylene (PP)

-Polyvinyl chloride (PVC)

-Polystyrene (PS)

Engineering Thermoplastics

-Polyamide (PA)

-Polycarbonates (PC)

-Polymethyl methacrylate (PMMA)

-Polyoxymethylene (POM)

-Polyethylene terephthalate (PET)

-Polybutylene terephthalate (PBT)

-Acrylonitrile Butadiene Styrene (ABS)/Styrene Acrylonitrile (SAN)

High-performance Engineering Thermoplastics

-Polyether Ether Ketone (PEEK)

-Liquid Crystal Polymer (LCP)

-Polytetrafluoroethylene (PTFE)

-Polyimide (PI)

Others

By End-User

Packaging

Building and Construction

Automotive and Transportation

Electrical and Electronics

Sports and Leisure

Medical

Others

12 Middle East and Africa Thermoplastic Market Analysis and Outlook To 2032

12.1 Introduction to Middle East and Africa Thermoplastic Markets in 2024

12.2 Middle East and Africa Thermoplastic Market Size Outlook by Country, 2021-2032

12.2.1 Saudi Arabia

12.2.2 UAE

12.2.3 Oman

12.2.4 Rest of Middle East

12.2.5 Egypt

12.2.6 Nigeria

12.2.7 South Africa

12.2.8 Rest of Africa

12.3 Middle East and Africa Thermoplastic Market size Outlook by Segments, 2021-2032

By Product

Commodity Thermoplastics

-Polyethylene (PE)

-Polypropylene (PP)

-Polyvinyl chloride (PVC)

-Polystyrene (PS)

Engineering Thermoplastics

-Polyamide (PA)

-Polycarbonates (PC)

-Polymethyl methacrylate (PMMA)

-Polyoxymethylene (POM)

-Polyethylene terephthalate (PET)

-Polybutylene terephthalate (PBT)

-Acrylonitrile Butadiene Styrene (ABS)/Styrene Acrylonitrile (SAN)

High-performance Engineering Thermoplastics

-Polyether Ether Ketone (PEEK)

-Liquid Crystal Polymer (LCP)

-Polytetrafluoroethylene (PTFE)

-Polyimide (PI)

Others

By End-User

Packaging

Building and Construction

Automotive and Transportation

Electrical and Electronics

Sports and Leisure

Medical

Others

13 Company Profiles

13.1 Company Snapshot

13.2 SWOT Profiles

13.3 Products and Services

13.4 Recent Developments

13.5 Financial Profile

3M Company

Arkema S.A.

Asahi Kasei Corp

BASF SE

Celanese Corp

Chevron Phillips Chemical Company LLC

Covestro AG

Daicel Corp

DuPont de Nemours Inc

Eastman Chemical Company

Evonik Industries AG

INEOS

Lanxess AG

LG Chem Ltd

LyondellBasell Industries Holdings BV

Mitsubishi Engineering-Plastics Corp

Polyplastics Co. Ltd

Royal DSM N.V.

SABIC

Solvay SA

Teijin Ltd

14 Appendix

14.1 Customization Offerings

14.2 Subscription Services

14.3 Related Reports

14.4 Publisher Expertise

By Product

Commodity Thermoplastics

-Polyethylene (PE)

-Polypropylene (PP)

-Polyvinyl chloride (PVC)

-Polystyrene (PS)

Engineering Thermoplastics

-Polyamide (PA)

-Polycarbonates (PC)

-Polymethyl methacrylate (PMMA)

-Polyoxymethylene (POM)

-Polyethylene terephthalate (PET)

-Polybutylene terephthalate (PBT)

-Acrylonitrile Butadiene Styrene (ABS)/Styrene Acrylonitrile (SAN)

High-performance Engineering Thermoplastics

-Polyether Ether Ketone (PEEK)

-Liquid Crystal Polymer (LCP)

-Polytetrafluoroethylene (PTFE)

-Polyimide (PI)

Others

By End-User

Packaging

Building and Construction

Automotive and Transportation

Electrical and Electronics

Sports and Leisure

Medical

Others

Countries Analyzed

North America (US, Canada, Mexico)

Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

South America (Brazil, Argentina, Rest of South America)

Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)