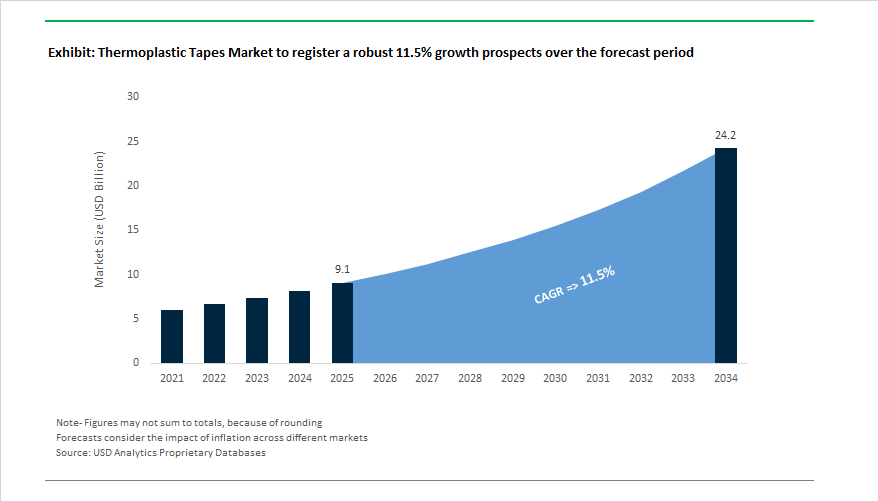

The Global Thermoplastic Tapes Market is projected to expand from USD 9.1 billion in 2025 to USD 24.2 billion by 2034, advancing at a CAGR of 11.5%, as continuous-fiber-reinforced thermoplastic (CFRTP) tapes move decisively from qualification-heavy aerospace programs into rate-driven, multi-industry structural manufacturing. The market’s acceleration is not volume-led; it is being shaped by OEM decisions to redesign load paths, assembly logic, and production takt times around weldable, reprocessable, and automation-compatible composite architectures.

Across aerospace and advanced air mobility, manufacturers are increasingly specifying carbon-fiber-reinforced PEEK, PAEK, PPS, and PEKK tapes capable of tensile strengths exceeding 2,500 MPa, enabling thinner laminates without compromising damage tolerance or fatigue life. Airbus, Boeing suppliers, and Tier-1 aerostructure manufacturers are scaling Automated Fiber Placement (AFP) and Automated Tape Laying (ATL) lines where thermoplastic tapes support layup speeds approaching 1,000–1,270 mm/s, materially compressing cycle times compared with thermoset prepregs. This shift directly addresses one of aerospace’s longest-standing constraints: the inability to reconcile structural composites with rate production.

Automotive and industrial buyers are driving a second, structurally different demand vector. OEMs and Tier-1s are adopting glass- and carbon-fiber-reinforced polypropylene (CF/PP, GF/PP) and PA-based tapes to enable welded, clip-free assemblies in seat structures, battery enclosures, underbody shields, and pressure vessels. The ability to consolidate parts via induction, resistance, or ultrasonic welding—rather than adhesive bonding or mechanical fastening—is increasingly viewed as a manufacturing advantage, reducing bill-of-material complexity and improving recyclability at end of life. Several automotive-focused tape suppliers now position thermoplastic UD tapes explicitly as “metal-replacement systems” rather than composite reinforcements.

Market Analysis: Recent Developments Shaping Thermoplastic Tape Adoption

Thermoplastic tape adoption accelerated on three fronts—aerospace demonstrators, automotive CF/PP scale-up, and traceable sustainability. In March 2024, Hexcel and Arkema unveiled a high-performance thermoplastic composite structure demonstrator, validating co-developed CF/PEKK/PEEK tape pathways for aeronautical structures and underscoring the readiness of high-rate thermoplastic manufacturing. By September 2024, Toray Advanced Composites launched Toray Cetex® PESU for UAM and aircraft interiors, targeting a sweet spot of flame resistance, cost efficiency, and formability. In November 2024, Toray further expanded capacity in continuous fiber reinforced thermoplastics—de-risking supply for industrial, automotive, and interiors. In parallel (Q4 2024/Q1 2025), Mitsui Chemicals broadened TAFNEX™ CF/PP automotive use (e.g., cross-car beams, oil pans), highlighting short cycles and 3D integration that fit mass-production tact times.

Sustainability and circularity moved from aspiration to execution in 2025. Hexcel–Fairmat signed a 10-year U.S. recycling agreement (May 2025) to process carbon composite scrap—an important step for aerospace waste valorization. Teijin began rolling out Digital Product Passports (April 2025) aligned with ESPR, improving supply-chain transparency for aramid/carbon reinforcements used in thermoplastic UD tapes; by August 2025, Teijin Aramid achieved ISCC PLUS certification for Twaron®, enabling verifiable mass-balance and circular content claims. At the same time, Hexcel showcased thermoplastic breakthroughs with the HELUES Project at Paris Air Show (June 2025), positioning high-rate thermoplastics for ramping narrowbody and UAM build rates.

Market Trend 1: Qualification of Continuous Fiber Thermoplastic Tapes for Primary Aircraft Structures

The aerospace industry is witnessing a fundamental transformation with the qualification of continuous fiber thermoplastic composites—notably PEEK and PEKK-based tapes—for primary aircraft structures, replacing traditional thermoset composites and metal alloys. Academic and industrial research confirms that these thermoplastic matrices maintain structural performance between −55°C and 120°C, even after prolonged exposure to moisture. Further, they exhibit superior damage tolerance and retention of compressive strength after impact, surpassing epoxy systems in long-term durability and service reliability.

The certification momentum is underpinned by a global shift toward out-of-autoclave (OoA) processing and automated layup technologies, with major aerospace OEMs adopting welding-based assembly methods that achieve up to 90% of base material strength. The leap in manufacturing efficiency eliminates costly mechanical fastening, significantly reducing part count, assembly time, and overall aircraft weight—critical metrics for modern air mobility platforms.

From a policy standpoint, government-backed initiatives in the EU and U.S., aligned with sustainable aviation and fleet modernization goals, are accelerating investment in Automated Tape Laying (ATL) and high-speed thermoplastic processing. These programs aim for 30% or greater cycle time reductions compared to legacy thermoset manufacturing. The qualification of thermoplastic tapes for primary aerospace structures thus marks a pivotal shift toward a lightweight, fuel-efficient, and sustainable aviation ecosystem.

Market Trend 2: Adoption of In-Situ Tape Placement for High-Volume Automotive Structural Components

The automotive sector, particularly the electric vehicle (EV) industry, is rapidly integrating Automated Fiber Placement (AFP) and in-situ tape placement technologies originally developed for aerospace into mass-production structural applications. A groundbreaking simulation by an automotive research group reported that replacing an aluminum battery case (96 kg) with a carbon fiber sheet molding compound (CF-SMC) design could yield a 30% weight reduction—a major advancement for EV energy efficiency and range.

To enable high-volume adoption, new modular AFP systems compatible with standard industrial robots are emerging, reducing Total Cost of Ownership (TCO) by up to 90% for small and medium-sized manufacturers. The democratization of AFP technology is transforming cost structures and making high-speed thermoplastic tape processing viable for components such as battery enclosures, chassis reinforcements, and underbody shields.

In production environments, thermoplastic tape-based automated systems are achieving 40% faster cycle times than manual layup methods, directly addressing the mass production needs of global automakers. As lightweighting becomes a cornerstone of next-generation EV design, the convergence of composite tape innovation, robotic automation, and modular AFP equipment positions thermoplastic tapes as a critical enabler of structural efficiency and manufacturing scalability in the automotive sector.

Market Opportunity 1: Development of Rapidly Processable Tapes for Additive Manufacturing of Large-Scale Tooling

A transformative opportunity lies in the development of rapidly processable thermoplastic tapes tailored for Large-Format Additive Manufacturing (LFAM) or Big Area Additive Manufacturing (BAAM). The innovation directly addresses one of the major cost and time bottlenecks in composite production—the creation of large, high-precision molds and tooling.

Using short-fiber-reinforced PAEK-based thermoplastic tapes as feedstock, manufacturers can drastically reduce tooling lead times from months to weeks, leveraging high-output pellet extruders that ensure rapid deposition rates and robust mechanical integrity. These materials maintain thermal stability and low coefficient of thermal expansion (CTE) during subsequent curing processes, ensuring dimensional accuracy and repeatability.

Further, academic research highlights that optimized post-processing and AM-compatible formulations significantly improve tool surface finish and reduce internal stresses, enhancing part release quality and minimizing defects. The integration of AM and thermoplastic tape technologies therefore represents a game-changing avenue for producing low-cost, durable, and thermally stable molds—particularly valuable in aerospace, wind energy, and marine composite manufacturing.

Market Opportunity 2: Engineering of Recyclable and Mono-Material Tape Systems for Consumer Electronics

The next wave of innovation in the thermoplastic tapes industry centers on recyclable and mono-material tape systems tailored for consumer electronics, aligning with global Extended Producer Responsibility (EPR) and circular economy mandates. As global technology brands face mounting pressure to design for recyclability, Continuous Fiber Reinforced Thermoplastics (CFRT) are emerging as a sustainable solution capable of enabling full material recovery and reusability.

CFRT-based thermoplastic tapes offer the dual advantage of mechanical strength and recyclability, making them ideal for lightweight, high-durability enclosures in laptops, tablets, and portable devices. Using unidirectional thermoplastic tape laminates, electronics manufacturers can achieve production volumes exceeding 100,000 units per program via one-shot compression molding and injection overmolding, ensuring cost-effective scalability without sacrificing design flexibility.

By eliminating thermoset and metallic components from assemblies, manufacturers can achieve mono-polymer composite structures that simplify recycling logistics, lower energy consumption, and align with sustainable manufacturing standards. The represents a key growth avenue in the drive toward eco-conscious, high-performance consumer electronics manufacturing.

Thermoplastic Tapes Market Share Insights, 2025-2034

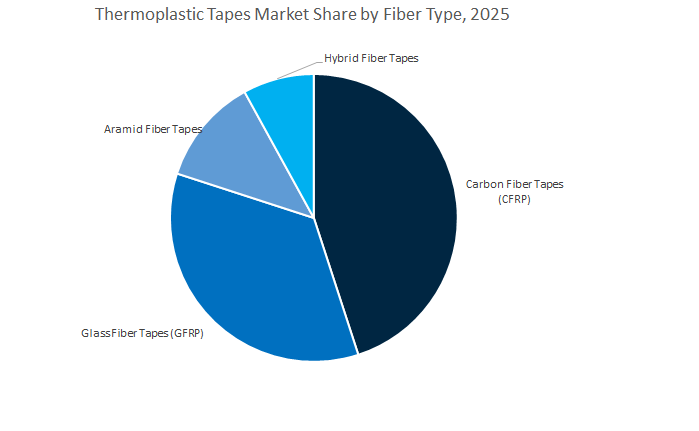

Market Share by Fiber Type

The Carbon Fiber Reinforced Thermoplastic (CFRP) Tapes segment dominates the global thermoplastic tapes market, accounting for approximately 43.8% of the projected 2025 share. This dominance is primarily attributed to carbon fiber’s superior strength-to-weight ratio, stiffness, and fatigue resistance, which make it the preferred material in aerospace, automotive, and high-performance sporting goods applications. As the aerospace industry pushes for lightweight structures to enhance fuel efficiency and reduce emissions, carbon fiber thermoplastic composites are replacing traditional metal components in both structural and semi-structural parts. Moreover, their rapid processing capability and recyclability offer a competitive advantage over thermoset composites, aligning with sustainability goals and production efficiency targets. Glass Fiber Tapes (GFRP) maintain a strong position in the market due to their cost-effectiveness and versatility, offering a balance between mechanical performance and affordability. They are extensively used in wind turbine blades, marine applications, and industrial equipment, where performance-to-cost ratio is key. Aramid Fiber Tapes, known for their exceptional impact and abrasion resistance, find niche applications in defense, protective equipment, and aerospace insulation systems, while Hybrid Fiber Tapes—combining different fiber reinforcements—are gaining traction in advanced manufacturing. These hybrid systems are engineered to provide customized mechanical and thermal properties, appealing to sectors requiring tailored performance, such as automotive crash components and next-generation aircraft structures.

Market Share by End-Use Industry

The Aerospace and Defense segment leads the thermoplastic tapes industry, capturing an estimated 31.9% of the market share in 2025. This leadership is driven by the aerospace sector’s escalating demand for lightweight, high-performance composites that improve aircraft fuel efficiency, reduce assembly time, and support automated manufacturing processes. Thermoplastic tapes are increasingly replacing thermoset materials in aircraft fuselage panels, brackets, seat frames, and access doors, thanks to their superior impact resistance, weldability, and reprocessability. The Automotive and Transportation sector represents one of the fastest-growing markets, fueled by the shift toward electric vehicles (EVs), sustainable mobility, and lightweighting initiatives. OEMs are integrating thermoplastic tapes into battery casings, underbody shields, and structural reinforcements, capitalizing on their ability to reduce weight while maintaining safety and performance standards. Wind Energy continues to be a significant end-use area, leveraging thermoplastic tapes in turbine blade fabrication and structural stiffeners, where durability, fatigue resistance, and processing efficiency are vital. Sporting Goods applications remain strong, particularly in high-end bicycles, rackets, and skis where performance optimization and material aesthetics are crucial differentiators. Additionally, Oil & Gas and Electrical & Electronics industries utilize thermoplastic tapes for pipe reinforcement, insulation layers, and thermal management systems, while the Medical & Healthcare sector adopts these materials in prosthetics and imaging equipment requiring lightweight, biocompatible, and precise structural solutions.

A concentrated set of leaders competes on matrix breadth (PEEK/PAEK/PPS/PESU/PI), automated placement compatibility (AFP/ATL/ISC), fusion-weldable architectures, and traceable sustainability (ISCC PLUS, DPP, recycling MOUs). Differentiation increasingly hinges on qualified aerospace programs, press-forming/overmolding readiness, and digital manufacturing toolkits for hybrid structures.

Toray TAC’s Cetex® portfolio (PI, PEEK, PPS UD tapes and RTLs) is entrenched on major aircraft programs and aims at UAM. Rapid press-forming and overmolding enable minutes-level cycles for high-volume parts.With Cetex® PESU (September 2024), Toray addresses lightweight, flame-resistant, cost-efficient cabin/UAM structures. Capacity expansion (November 2024) strengthens supply assurance across industrial/automotive/interiors. Toray’s multi-material analysis tech (January 2022) improves predictive performance for hybrid parts combining UD tapes and injection molding—critical for design-to-rate in serial production.

Hexcel provides carbon fiber thermoplastic tapes optimized for AFP/ATL with in-situ consolidation, reducing post-processing and enabling high-rate aerostructures. The Hexcel–Arkema demonstrator (March 2024) validated primary/secondary aero use cases; the HELUES showcase (June 2025) at Paris Air Show highlighted thermoplastic maturation for ramp scenarios. A CDTI grant (February 2024) for EFIPreg advances next-gen aerospace prepregs at high-rate. Hexcel’s 10-year recycling pact with Fairmat (May 2025) brings a tangible circular outlet for carbon scrap, enhancing program sustainability.

Solvay leads in high-performance polymer chemistry (PEEK/PAEK), delivering chemical/thermal resistance and FST compliance for interiors and mass transit. Solutions address lightweighting with strict FST and durability requirements. A 9T Labs partnership (November 2021) broadened CF/PEEK/CF/PPS options for additive and mass production of structural parts. Solvay’s 2050 carbon-neutral pathway underpins sustainable tapes and processing innovation, appealing to OEMs prioritizing verified environmental progress.

Teijin leverages Twaron®/Technora® aramid reinforcements for high impact resistance and strength-to-weight in thermoplastic tapes across automotive, renewable energy, and protection. Digital Product Passports (April 2025) address ESPR-driven traceability, while ISCC PLUS (August 2025) certifies sustainable production routes. Teijin’s ecosystem spans ballistics, submarine power cables, and lightweight mobility (e.g., Brunel Solar Team, August 2025), showcasing performance with circular content and verified claims.

Mitsui Chemicals specializes in TAFNEX™ CF/PP UD tapes, exploiting low density, chemical resistance, and high processability for short cycle times and 3D integration. Q4 2024/Q1 2025 deployments detailed cross-car beams, tailgates, oil pans, proving 35–50% weight reduction and vibration damping. The tapes suit thermoforming and overmolding, aligning with automotive takt and cost targets while easing end-of-life recycling compared with multi-material metal assemblies.

Country Analysis: Global Thermoplastic Tapes Industry Developments

United States – Driving High-Performance Thermoplastic Tape Innovation in Aerospace and Defense

The United States continues to dominate the global thermoplastic tapes industry through cutting-edge innovation and large-scale adoption in aerospace, defense, and renewable energy sectors. Key players such as Toray Advanced Composites and Hexcel Corporation are investing heavily in high-performance thermoplastic composite materials, emphasizing carbon fiber-reinforced PEEK (Polyether Ether Ketone) and PEKK tapes for structural and interior aircraft components. In October 2024, Toray expanded its continuous fiber reinforced thermoplastic (CFRTP) product portfolio to support next-generation aerospace applications, while its long-term supply agreement (LTA) with Airborne Aerospace B.V. (July 2025) underscores growing demand for space-grade thermoplastic UD tapes in satellite and solar array systems.

The U.S. Department of Energy’s 2024 GRIP projects further highlight the strategic significance of thermoplastic tapes in the Composite Core Conductor market, a key component in energy transmission infrastructure. Meanwhile, Hexcel’s collaboration with Spirit AeroSystems focuses on integrating sustainable thermoplastic composite technologies for automated tape laying (ATL) and automated fiber placement (AFP) processes, improving production efficiency and recyclability. The aerospace industry’s strict fire, smoke, and toxicity (FST) standards continue to drive adoption of PEEK-based thermoplastic tapes, cementing the United States’ role as the global epicenter for advanced thermoplastic composites innovation.

China – Expanding Thermoplastic Tape Applications in EVs and Lightweight Manufacturing

China remains one of the fastest-growing markets for thermoplastic tapes, driven by its rapid automotive electrification and industrial innovation. The surge in Electric Vehicle (EV) manufacturing is propelling large-scale adoption of polyamide (PA) and polypropylene (PP) thermoplastic tapes for battery enclosures, structural body components, and interior modules. Supported by strong government mandates on vehicle emissions reduction and the “Made in China 2025” policy framework, domestic manufacturers are increasingly replacing metal parts with glass fiber-reinforced thermoplastic (GFRP) tapes to achieve lightweighting and carbon neutrality goals.

The Commercial Aircraft Corporation of China (COMAC) is emerging as a major catalyst for thermoplastic tape demand through its ongoing aircraft development programs, incorporating high-performance carbon fiber reinforced thermoplastic composites (CFRTP) in next-generation airframes. Additionally, China’s emphasis on localized production has resulted in substantial investment in cost-effective thermoplastic UD tape manufacturing, particularly for the automotive, construction, and renewable energy industries. As R&D accelerates in non-silicone and recyclable thermoplastic tape formulations, China is positioning itself as both a production hub and innovation center for thermoplastic composite materials.

Germany – Advancing Automotive Lightweighting and CFRTP Manufacturing

Germany is a leading force in carbon fiber reinforced thermoplastic (CFRTP) tape innovation, with a strong emphasis on automotive, wind energy, and industrial engineering applications. As a global hub for automotive component production, Germany is driving high adoption of polyamide (PA) and PEEK-based thermoplastic tapes for vehicle structures, seat modules, and powertrain components. Evonik Industries AG has expanded its production facilities dedicated to thermoplastic UD tapes, particularly targeting renewable energy systems such as wind turbine blades, where strength-to-weight optimization is critical.

Germany’s R&D ecosystem is deeply aligned with the European Union’s circular economy objectives, focusing on material recyclability and resource efficiency. Ongoing projects across German technical institutes aim to recover and repurpose carbon fiber waste from automotive end-of-life products, reinforcing the sustainability of thermoplastic tapes in the CFRP recycling chain. With its advanced polymer science, robust automotive infrastructure, and commitment to sustainable production, Germany remains a global benchmark for thermoplastic tape manufacturing excellence.

Japan – Leading Global Innovation in Carbon Fiber Thermoplastic Tapes

Japan continues to set the global standard for high-performance carbon fiber thermoplastic (CFRTP) tape innovation through advanced materials science, precision manufacturing, and multi-sector applications. Toray Industries, the country’s largest composite material producer, has expanded thermoplastic UD tape production capacity both domestically and abroad to meet surging international demand. In February 2024, Toray received a national innovation award for its ultra-high-strength carbon fiber developed via nanoscale tailoring technology, the foundation for its next-generation CFRTP tapes used in aerospace and automotive lightweighting.

Further driving industry growth, Mitsui Chemicals is promoting its TAFNEX CFRTP beyond industrial applications to high-end consumer electronics and luxury goods, while Toray’s multi-material structural analysis technology enables precise predictive modeling for hybrid composite assemblies. The developments underscore Japan’s leadership in precision engineering and multifunctional composite design, combining mechanical strength, lightness, and aesthetic versatility. As the demand for high-performance, sustainable thermoplastic tapes grows, Japan’s ongoing focus on material performance optimization and global supply integration reinforces its top-tier position in the global thermoplastic composites industry.

Netherlands & European Union – Sustainability and Automated Manufacturing Leadership

The European thermoplastic tapes market, anchored by operations in the Netherlands, is increasingly characterized by a dual focus on sustainability and automation. Toray Advanced Composites is spearheading a joint End-of-Life Aerospace Recycling Program (June 2025) in collaboration with Daher and TARMAC Aerosave, aimed at developing scalable recycling processes for commercial aircraft thermoplastic composites. The initiatives align with the EU’s broader environmental strategy to reduce composite waste and maximize material circularity.

The EU aerospace industry’s transition toward Automated Fiber Placement (AFP) and Automated Tape Laying (ATL) technologies has intensified demand for PEEK and PEKK-based thermoplastic tapes offering exceptional weight reduction, corrosion resistance, and reprocessability. Europe’s growing focus on automation is fostering precision manufacturing efficiency and minimizing human error in structural composite production.

United Arab Emirates (UAE): Regional Pioneer in Water-Based Thermoplastic Tape Innovation

The United Arab Emirates (UAE) is rapidly emerging as a regional leader in thermoplastic composite innovation, driven by advanced research capabilities and a national commitment to sustainability. The Technology Innovation Institute (TII) has successfully developed the region’s first thermoplastic carbon fiber unidirectional (UD) tape for Automated Fiber Placement (AFP), marking a major technological breakthrough for the MENA aerospace and space sectors. The milestone utilizes a state-of-the-art Thermoplastic Impregnation Line to produce water-based, solvent-free PEEK thermoplastic tapes, representing a regional first in clean manufacturing technology.

The UAE’s innovation is strategically aligned with its goal of developing indigenous composite manufacturing ecosystems to support aerospace, logistics, and advanced air mobility (AAM) applications. The introduction of high-performance, flame-retardant, and recyclable thermoplastic tapes from TII positions the country as a front-runner in sustainable materials engineering within the Middle East. The advancement also sets the foundation for a regional supply chain capable of meeting global aerospace and industrial composite requirements.

Thermoplastic Tapes Market Report Scope

Thermoplastic Tapes Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$9.1 Billion

|

|

Market Size (2034)

|

$24.2 Billion

|

|

Market Growth Rate

|

11.5%

|

|

Segments

|

By Fiber Type (Carbon Fiber, Glass Fiber, Aramid Fiber, Hybrid Fiber), By Resin Type (PEEK, PEKK, Polyamide, Polypropylene, PPS, PET), By Manufacturing Process (Unidirectional, Woven Fabric, Laminates, Bulk Molding), By End-User (Aerospace, Automotive, Oil & Gas, Wind Energy, Sporting Goods, Medical, Electrical

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Toray Industries, Inc., Solvay SA, Hexcel Corporation, Celanese Corporation, Victrex plc, Teijin Limited, SABIC, Arkema SA, Avient Corporation, Evonik Industries AG, SGL Carbon, Mitsubishi Chemical Corporation, Gurit Holding AG, Covestro AG, Dixie Chemical Company

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

By Fiber Type

- Carbon Fiber

- Glass Fiber

- Aramid Fiber

- Hybrid Fiber

By Resin Type

- PEEK

- PEKK

- Polyamide

- Polypropylene

- PPS

- PET

By Manufacturing Process

- Unidirectional

- Woven Fabric

- Laminates

- Bulk Molding

By End-Use Industry

- Aerospace

- Automotive

- Oil & Gas

- Wind Energy

- Sporting Goods

- Medical

- Electrical

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Thermoplastic Tapes Market-

- Toray Industries, Inc.

- Solvay SA

- Hexcel Corporation

- Celanese Corporation

- Victrex plc

- Teijin Limited

- SABIC

- Arkema SA

- Avient Corporation

- Evonik Industries AG

- SGL Carbon

- Mitsubishi Chemical Corporation

- Gurit Holding AG

- Covestro AG

- Dixie Chemical Company

*- List not Exhaustive

Research Coverage

Prepared by USDAnalytics, this report investigates the fast-scaling Thermoplastic Tapes ecosystem across aerospace, advanced air mobility, automotive, industrial, oil & gas, wind energy, sporting goods, medical, and electrical applications—translating the shift to high-rate, weldable CFRTP architectures into actionable strategy for engineering, procurement, and operations teams. It curates breakthroughs in in-situ consolidated AFP/ATL, fusion-welded UD laminates, and high-temperature matrices (PEEK/PAEK/PPS/PI) while our analysis reviews manufacturability (layup speeds, OoA consolidation, press-forming/overmolding), durability (fatigue/impact/FST), and circularity (recyclability, DPP/ISCC mass-balance). The study highlights where thermoplastic tapes displace thermosets and metals on cost-per-part, takt-time, and lifecycle metrics, mapping supplier capacity moves, qualification progress, and sustainability credentials. Built for decision makers, this report is an essential resource for benchmarking materials and processes, de-risking scale-up, and aligning product roadmaps with certification, ESG, and total-cost targets, etc……

Scope Highlights

Segmentation:

- By Fiber Type: Carbon Fiber; Glass Fiber; Aramid Fiber; Hybrid Fiber

- By Resin Type: PEEK; PEKK; Polyamide; Polypropylene; PPS; PET

- By Manufacturing Process: Unidirectional; Woven Fabric; Laminates; Bulk Molding

- By End-Use Industry: Aerospace; Automotive; Oil & Gas; Wind Energy; Sporting Goods; Medical; Electrical

- By Region: North America (United States, Canada, Mexico); Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe); Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC); South & Central America (Brazil, Argentina, Rest of SCA); Middle East & Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

Time Horizon: Historic data 2021–2024 and forecast data 2025–2034.

Companies Covered: Analysis/profiles of 15+ companies, including Toray Industries, Solvay, Hexcel, Celanese, Victrex, Teijin, SABIC, Arkema, Avient, Evonik, SGL Carbon, Mitsubishi Chemical, Gurit, Covestro, and Dixie Chemical.

Deliverables

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.