Regulatory Shift, Sustainable Solvents, and Industrial Demand Driving Stable Growth

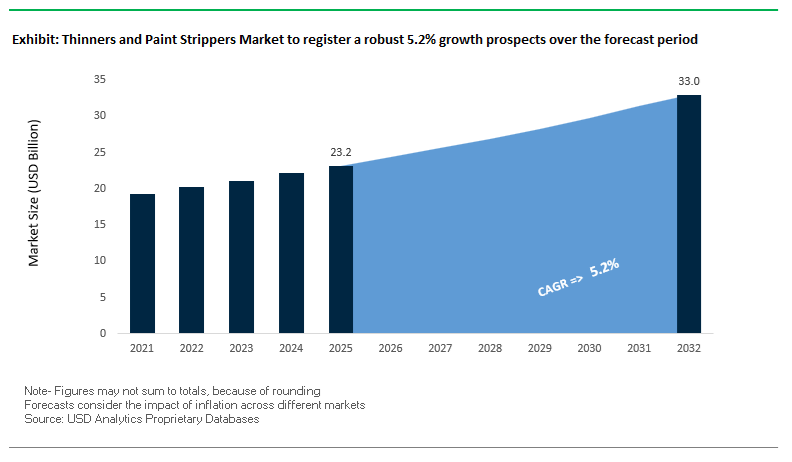

The global Thinners and Paint Strippers Market is undergoing steady expansion, supported by sustained demand from automotive refinish, construction, industrial maintenance, and manufacturing sectors. The market was valued at $23.2 billion in 2025 and is projected to reach $33.1 billion by 2032, growing at a CAGR of 5.2% during 2025–2032. Growth is being shaped by a dual dynamic: continued reliance on high-performance solvent systems alongside a structural transition toward low-VOC, bio-based, and environmentally compliant formulations.

A key structural driver is the increasing demand for efficient surface preparation and coating removal solutions, particularly in infrastructure renovation, automotive refinishing, and industrial maintenance. Thinners play a critical role in optimizing viscosity, flow, and drying characteristics of coatings, while paint strippers are essential for substrate restoration and recoating cycles. The expansion of global construction and refurbishment activity, especially in aging urban infrastructure, is sustaining demand for these products.

However, the market is undergoing a significant transformation due to tightening environmental and occupational safety regulations, particularly restrictions on hazardous solvents such as methylene chloride. This has accelerated the development of water-based, pH-neutral, and bio-derived stripping solutions, as well as VOC-exempt thinners that maintain performance while reducing environmental impact. Manufacturers are increasingly focusing on green chemistry innovations, solvent recovery systems, and circular economy models to align with regulatory requirements and sustainability goals.

Another emerging trend is the integration of digital tools and process optimization technologies, enabling users to select the most appropriate solvent systems based on application conditions, regulatory constraints, and performance requirements. This is improving operational efficiency while reducing misuse and environmental risks.

Market Analysis: Bio-Based Strippers, Fast-Drying Thinner Systems, and Circular Solvent Models Reshaping Competitive Landscape

The thinners and paint strippers market is being reshaped by regulatory-driven innovation, strategic portfolio restructuring, and sustainability-focused product development, reflecting the industry’s transition toward safer and more efficient solutions. The March 2026 proposed merger between AkzoNobel and Axalta represents a major consolidation move, combining extensive portfolios in industrial thinners and solvent recovery systems, and strengthening global capabilities in high-performance solvent technologies.

Product innovation is increasingly focused on performance optimization and energy efficiency. PPG’s March 2026 launch of DELTRON fast-drying clearcoat and specialized thinners introduces formulations designed to optimize flow and leveling at lower curing temperatures, enabling body shops to reduce energy consumption while maintaining finish quality.

Regulatory pressures are accelerating the adoption of safer stripping technologies. Dumond Chemicals’ January 2026 expansion of SmartStrip™, a bio-based, pH-neutral paint remover, reflects the industry’s response to restrictions on hazardous solvents, particularly in architectural restoration projects. Similarly, Henkel’s February 2025 R&D expansion focuses on developing water-based stripping technologies that eliminate toxic aromatic solvents while maintaining industrial-grade performance.

Sustainability initiatives are also reshaping product portfolios. W.M. Barr & Co’s 2025–2026 “green solvent” initiative aims to reformulate thinner products using VOC-exempt solvents, while AkzoNobel’s January 2025 partnership for eco-friendly stripping solutions targets low-odor, low-emission products for indoor infrastructure projects.

Strategic divestments are enabling companies to focus on high-value segments. PPG’s August 2025 divestiture of its North American decorative business allows it to concentrate on industrial and aerospace solvent systems, while BASF’s October 2025 sale of its coatings and surface treatment business transfers a significant portion of its automotive thinner portfolio to a new entity backed by Carlyle and QIA.

Digitalization is improving product selection and compliance. PPG’s December 2024 launch of a digital stripper selection platform provides users with application-specific guidance and safety resources, helping navigate evolving regulatory requirements.

Circular economy models are gaining traction. Recochem’s November 2024 expansion of solvent recovery services enables industrial users to recycle and reuse thinners, reducing waste and lowering operational costs while supporting sustainability goals.

Market Trend: EPA TSCA 2026 Enforcement Eliminates Methylene Chloride and Tightens NMP Exposure Controls

The thinners and paint strippers industry is undergoing a fundamental regulatory shift following the full enforcement of the U.S. Environmental Protection Agency’s TSCA Section 6 rule banning methylene chloride for most consumer and industrial applications. This measure directly targets acute toxicity risks, including fatal inhalation exposure historically associated with enclosed-space stripping operations. As of early 2026, commercial refinishing and industrial coating removal operations must either fully transition away from dichloromethane-based formulations or face immediate compliance violations. In parallel, N-Methylpyrrolidone is subject to stringent Workplace Chemical Protection Program requirements, mandating exposure limits of 0.1 ppm over an eight-hour time-weighted average. This is forcing the adoption of advanced ventilation systems, continuous exposure monitoring, and enhanced personal protective equipment protocols. The regulatory environment is therefore shifting the industry away from high-volatility, high-toxicity solvents toward safer, lower-emission alternatives. This transition is also influencing procurement decisions in aerospace, automotive, and industrial maintenance sectors, where compliance with occupational safety standards is now a primary determinant of product selection.

Market Trend: China GB/T 41652-2025 Redefines Thinner Formulations with Strict VOC and BTEX Limits

China’s nationwide enforcement of GB/T 41652-2025 is significantly restructuring the formulation landscape for industrial thinners. The regulation imposes a maximum VOC content of 420 g/L for general-purpose thinners, effectively phasing out traditional solvent systems dominated by high-aromatic hydrocarbon blends. Additionally, the standard introduces strict limits on benzene, toluene, ethylbenzene, and xylene, capping their combined concentration at 10% by weight. These restrictions are driving a transition toward oxygenated solvents and water-miscible systems that offer lower toxicity and improved environmental performance. The impact is particularly pronounced in industrial clusters such as the Pearl River Delta, where legacy supply chains have been heavily reliant on BTEX-rich formulations. Manufacturers are now re-engineering solvent blends to maintain solvency power, evaporation rates, and compatibility with coatings while meeting regulatory thresholds. As China continues to align industrial policy with its dual carbon objectives, low-VOC and low-toxicity thinners are becoming the new baseline standard, influencing both domestic production and export-oriented formulations.

Market Opportunity: Bio-Based Paint Strippers Gain Market Share as Safe and Sustainable Alternatives to Legacy Solvents

The regulatory phase-out of methylene chloride is creating a substantial opportunity for bio-based paint strippers derived from renewable feedstocks such as corn, soy, and citrus. These formulations, typically based on esters and terpenes such as dimethyl adipate and ethyl lactate, are achieving performance levels comparable to traditional chemical strippers without the associated health hazards. In 2026, high-performance bio-based systems are capable of removing multi-layer polyurethane coatings within 60 to 90 minutes, matching the efficiency of legacy products while significantly reducing toxicity. From a sustainability perspective, formulations containing 70% or more bio-based content, as measured under ASTM D6866, enable compliance with federal procurement initiatives that prioritize low-embodied carbon materials. Additionally, the lower vapor pressure of these solvents reduces evaporative losses by up to 50% compared to conventional acetone-based systems, improving material utilization and reducing emissions. As industries increasingly prioritize worker safety and environmental compliance, bio-based paint strippers are emerging as a key growth segment in the global coatings removal market.

Market Opportunity: Laser Paint Stripping Technology Disrupts Chemical-Based Removal with Precision and Lifecycle Cost Advantages

Laser Paint Stripping is rapidly gaining traction as a chemical-free alternative in high-value sectors such as aerospace and automotive manufacturing. This technology uses controlled laser pulses to ablate coating layers while preserving the integrity of the underlying substrate. Modern automated systems can achieve stripping rates of 3 to 5 square feet per minute, making them viable for large-scale industrial applications. A key advantage lies in precision control, where integrated feedback sensors detect the transition between coating and substrate, ensuring that the process stops immediately to prevent thermal damage. Additionally, these systems incorporate HEPA-grade vacuum units capable of capturing 99.9% of vaporized particulates, eliminating hazardous waste streams associated with chemical stripping. Although the initial capital investment is relatively high, lifecycle cost analyses indicate that laser stripping can reduce total coating removal costs by approximately 60% over a ten-year period by eliminating expenses related to chemical procurement, handling, and disposal. As regulatory and economic pressures converge, laser-based stripping technologies are positioned as a transformative solution within the paint removal industry.

Thinners and Paint Strippers Market Share and Segmentation Insights: Form & Packaging Trends Driving Industrial Demand

Liquid (Cans & Drums) Segment Leads with 65.6% Share Due to High-Volume Industrial Usage

The liquid segment (cans & drums) dominates the thinners and paint strippers market with a substantial 65.6% market share in 2025, driven by its versatility, cost-efficiency, and widespread industrial adoption. Liquid formulations—including acetone, methyl ethyl ketone (MEK), xylene, and methylene chloride alternatives—are extensively used in the industrial coatings, automotive refinishing, and surface preparation market for applications such as equipment cleaning, brush cleaning, and dip stripping processes. These products are available in a wide range of packaging sizes, from quarts to 55-gallon drums, supporting both small-scale and bulk industrial requirements. Their fast-acting chemical performance and lower cost per volume compared to gel, paste, or aerosol formats make them the preferred choice among auto refinishers, painting contractors, and industrial maintenance teams. As industries continue to prioritize efficiency, solvent performance, and operational cost reduction, liquid formulations maintain their leadership in the global paint thinner and stripper market.

Industrial Distributors Capture 36.9% Share as Key B2B Supply Channel

The industrial distributors segment leads the thinners and paint strippers market by sales channel with a 36.9% share in 2025, reflecting strong demand from B2B customers such as auto body shops, fleet maintenance providers, and industrial painting operations. These distributors play a critical role in the chemical distribution and industrial solvents market, supplying products in bulk quantities, including cases and drums, to meet high-volume consumption needs. A key growth driver is their ability to provide regulatory compliance support, including Safety Data Sheets (SDS), proper handling and disposal guidelines, and recommendations for low-VOC and environmentally compliant formulations aligned with EPA, REACH, and regional environmental standards. Additionally, industrial distributors offer technical expertise, product customization, and reliable supply chain logistics, making them indispensable partners for businesses operating in regulated industries. This combination of volume efficiency, compliance assurance, and technical support reinforces their dominance in the global thinners and paint strippers distribution landscape.

Competitive Landscape Analysis of the Thinners and Paint Strippers Market

Sherwin-Williams Expands Contractor-Focused Thinners and Paint Strippers Distribution

The Sherwin-Williams Company remains a leading player in the thinners and paint strippers market, supported by FY2025 consolidated net sales of USD 23.57 billion and low-to-mid single-digit growth guidance for 2026. Its Paint Stores Group benefited from mid-single-digit selling price increases, offsetting DIY volume softness. The integration of Suvinil added USD 164.5 million to Q4 2025 revenue, expanding Latin American distribution for preparatory solvents and paint thinners. Sherwin-Williams also dominates protective and marine coatings, offering industrial-grade thinners for epoxy and polyurethane systems, where margins reached 20.8%. Its 4,800+ stores ensure fast contractor access to compliant low-odor paint strippers and high-solvency thinners.

PPG Advances Sustainable Solvents and Automated Refinish Mixing Systems

PPG Industries, Inc. is strengthening its position in the paint thinners and strippers market through sustainability-led innovation and aerospace expansion. In 2026, the company launched PPG ENVIROLUXE™ Plus, a sustainable coatings and solvent range with recycled content, backed by third-party environmental impact certification tools. PPG also reached the 3,000th installation of its MOONWALK® automated paint mixing system, reducing refinish paint waste by up to 10% through precision-thinned systems. Its USD 380 million aerospace coatings facility in North Carolina, scheduled for 2027, will produce aircraft-grade strippers using alternatives to traditional toxic solvent chemistry. Four consecutive quarters of 2025 organic growth further highlight momentum in automotive refinish and aerospace solvent demand.

AkzoNobel Shifts Toward VOC-Compliant and Dry Coating Removal Technologies

AkzoNobel N.V. is reshaping its thinners and paint strippers market strategy through portfolio sharpening, sustainability, and industrial coating removal innovation. In 2026, the company completed the divestment of Akzo Nobel India Limited at 25x EBITDA, redirecting capital toward higher-growth decorative and industrial segments in Europe and North America. AkzoNobel maintains leadership in water-based thinners and VOC-compliant paint strippers under its Interpon and International brands, helping industrial clients reduce Scope 3 emissions. Having reached its 2x net debt-to-adjusted EBITDA leverage target ahead of schedule in 2025, the company has flexibility to invest in bio-attributed raw materials. Its IPG Photonics partnership explores laser-assisted coating removal, reducing chemical stripper dependency.

RPM International Builds Momentum in Specialty Strippers and REACH-Compliant Solvents

RPM International Inc. is gaining share in the thinners and paint strippers market through record growth, specialty brands, and operational efficiency. The company reported record fiscal Q3 2026 sales of USD 1.61 billion, up 8.9%, supported by its Performance Coatings Group and MAP margin improvement program. Its Zinsser and Rust-Oleum brands lead hard-to-remove coating applications, including specialty strippers for lead-based paint and industrial mastics. RPM’s European M&A strategy drove 20.1% regional growth in 2025–2026, targeting brands aligned with strict REACH solvent regulations. Strong fixed-cost leverage and SG&A optimization helped maintain record EBIT despite volatility in petroleum-derived solvent costs.

3M Leads Automated Surface Preparation and Low-Odor Paint Stripping Systems

3M Company is a major competitor in the paint strippers and surface preparation market, especially across industrial and manufacturing end users, which represent roughly 30% of global paint stripper demand. Its 2026 portfolio includes 3M™ Floor Stripper and industrial cleaners using automatic dispensing systems to reduce measuring errors and chemical exposure. The company has developed minimal-odor, non-ammoniated stripping formulas that remove burnished finishes while protecting sensitive substrates such as vinyl and specialty composites. 3M is moving toward integrated system-based coating removal solutions, combining Scotch-Brite™ mechanical abrasives with chemical strippers. This dual-action process lowers chemical volume requirements by 15–20%, strengthening its position in safer, efficient paint removal technologies.

United States Transitioning Toward DCM-Free Paint Strippers and Advanced MRO Solutions

The United States is undergoing a structural transformation in the thinners and paint strippers market, driven by stringent environmental regulations and evolving industrial requirements. The enforcement of the EPA’s restrictions on methylene chloride (DCM) is accelerating the shift toward DCM-free and NMP-free paint strippers, forcing manufacturers to adopt safer, compliant alternatives aligned with TSCA Section 6(a) regulations.

Infrastructure investments in aerospace MRO hubs across the Southeast are boosting demand for advanced gel-based paint strippers, particularly for aircraft livery refurbishment. Technological advancements such as hybrid laser-chemical stripping systems are redefining efficiency, combining solvent pre-treatment with robotic laser ablation for precision removal. Product innovation is evident in the development of bio-renewable ester-based thinners, replacing traditional solvents like MEK to meet zero-VOC standards. Additionally, high-performance thinners are gaining traction in emerging applications such as 3D printing resin cleaning, while facility expansions by key players are enhancing production of pH-neutral paint removers for heritage restoration projects.

Germany Leading Green Solvent Technologies and Circular Economy Integration

Germany is at the forefront of sustainable solvent solutions in the thinners market, emphasizing circular economy practices and eco-friendly formulations. Regulatory compliance with the EU’s Ecodesign standards is driving the adoption of digital product passports, ensuring transparency in solvent sourcing and carbon footprint tracking.

Technological advancements include the integration of closed-loop solvent recycling systems, significantly reducing raw thinner consumption in industrial paint processes. Product innovation is focused on bio-based and biodegradable paint strippers, such as dimethoxymethane (DMM)-based solutions that offer high performance without environmental hazards. Strategic investments by BASF and Wacker Chemie are expanding the production of bio-based ethyl acetate, a key component in eco-labeled coatings.

Germany also dominates in specialized applications, including paint stripping solutions for wind turbine blades, where precision and material integrity are critical. Innovations such as color-changing smart indicators in paint strippers are improving operational efficiency by signaling complete paint removal. These developments position Germany as a leader in green solvent technologies and sustainable coating removal solutions.

China’s Shift Toward High-Purity Solvents and Regulatory Harmonization

China is transitioning from bulk solvent production to a high-value focus on electronic-grade thinners and advanced paint stripping solutions, driven by stricter environmental standards and technological upgrades. Regulatory reforms, including updates to GB standards, are aligning the market with global safety and environmental benchmarks.

Industrial expansion is evident with significant investments in high-capacity solvent production facilities, supporting demand across coatings and electronics sectors. Technological advancements include the scale-up of ultra-high purity photoresist strippers, critical for semiconductor manufacturing at advanced nodes.

Regulatory policies are also pushing the adoption of low-VOC and water-based paint strippers, particularly in furniture manufacturing and indoor applications. Infrastructure developments, such as automated stripping lines for high-speed rail maintenance, are enhancing efficiency while minimizing material damage. These shifts are positioning China as a major player in high-purity solvent manufacturing and eco-compliant paint removal technologies.

India’s Growth Driven by Automotive Refinish Demand and Infrastructure Expansion

India is experiencing strong growth in the thinners and paint strippers market, fueled by rising automotive refinish demand and rapid infrastructure modernization. Large-scale investments by domestic and international players are expanding production capacity for specialty thinners and coating auxiliaries, particularly in industrial hubs like Maharashtra and Gujarat.

Technological advancements include the development of climate-adaptive thinners, designed to optimize evaporation rates in high-humidity environments, improving coating performance. Infrastructure projects such as the Amrit Bharat railway upgrades are driving demand for advanced stripping technologies to remove legacy coatings efficiently.

The increasing adoption of polyurethane thinners in premium interior applications is reflecting rising consumer demand for high-quality finishes. Expansion of aerospace manufacturing in India is also boosting demand for gel-based paint strippers in aircraft maintenance. Regulatory measures under the Quality Control Order (QCO) are ensuring safer usage through stricter labeling requirements, strengthening the market for compliant and high-performance solvent solutions.

Japan’s Precision Solvent Technologies for Electronics and Urban Applications

Japan is leading innovation in high-precision thinners and paint strippers, focusing on advanced applications in electronics, urban infrastructure, and specialized industries. Breakthrough developments include nanoscale surface-preparation thinners, which significantly enhance coating adhesion in flexible electronic devices such as OLED displays.

Product innovation is centered on low-odor and odor-neutralizing paint strippers, designed for use in occupied environments like elderly care facilities, supporting the country’s aging population. Regulatory updates are encouraging the adoption of high-boiling point solvents, improving safety and reducing emissions in small-scale industrial operations.

Infrastructure investments include specialized production facilities for electronic-grade solvents, catering to the global semiconductor and LCD industries. Japan also excels in niche applications such as precision immersion paint stripping for electronics recycling, ensuring material recovery without damage. Emerging innovations like UV-responsive paint removers are enabling highly targeted stripping processes, reinforcing Japan’s leadership in precision solvent technologies.

Brazil’s Expansion in Bio-Based Thinners and Sustainable Chemical Solutions

Brazil is emerging as a key market in the bio-based thinners and paint strippers segment, leveraging its strong agricultural base and ethanol production capabilities. The country is focusing on renewable solvent technologies, particularly ethyl lactate-based strippers derived from sugarcane biomass, offering environmentally friendly alternatives to traditional solvents.

Infrastructure investments, including capacity expansions by major manufacturers, are supporting increased production of high-performance thinners for industrial applications. Government initiatives under programs like Agro-Tech are promoting the use of bio-renewable solvents in agricultural machinery maintenance, reducing environmental impact.

Key applications include the use of durable thinners in offshore oil platform maintenance, where resistance to harsh marine environments is critical. Regulatory frameworks are also evolving, with stricter safety standards limiting hazardous chemical content in consumer-grade products. These developments position Brazil as a leader in sustainable solvent innovation and bio-based paint stripping solutions in Latin America.

Thinners and Paint Strippers Market Report Scope

Thinners and Paint Strippers Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$23.2 Billion

|

|

Market Size (2032)

|

$33.1 Billion

|

|

Market Growth Rate

|

5.2%

|

|

Segments

|

By Product Type (Paint Thinners, Paint Strippers), By Form and Packaging (Liquid, Gel and Paste, Aerosol Spray, Immersion, Packaging Type), By Application (Surface Preparation, Furniture Refinishing and Restoration, Building Renovation and Remodeling, Vehicle Maintenance and Refinishing, Industrial Equipment Repair, Marine Surface Prep, Graffiti Removal), By End-User Industry (Building and Construction, Automotive and Transportation, Industrial Manufacturing, Marine, Consumer Goods and Furniture), By Sales Channel (Direct Sales, Industrial Distributors, Retail and DIY Stores, E-commerce and Online Specialized Platforms), By Grade (Industrial Grade, Technical Grade, Consumer)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

3M Company, The Sherwin-Williams Company, PPG Industries, Inc., Akzo Nobel N.V., BASF SE, Henkel AG and Co. KGaA, RPM International Inc., Axalta Coating Systems Ltd., W.M. Barr and Company, Inc., Savogran Company, Recochem Inc., Sunnyside Corporation, Franmar Chemical, Inc., Dumond Chemicals, Inc., G.J. Nikolas and Co., Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Thinners and Paint Strippers Market Segmentation

By Product Type

- Paint Thinners

- Acetone

- Turpentine

- Mineral Spirits

- Toluene and Xylene

- Methyl Ethyl Ketone

- Specialized

- Paint Strippers

- Solvent-Based

- Caustic-Based

- Acidic-Based

- Bio-Based

By Form and Packaging

- Liquid

- Gel and Paste

- Aerosol Spray

- Immersion

- Packaging Type

By Application

- Surface Preparation

- Furniture Refinishing and Restoration

- Building Renovation and Remodeling

- Vehicle Maintenance and Refinishing

- Industrial Equipment Repair

- Marine Surface Prep

- Graffiti Removal

By End-User Industry

- Building and Construction

- Automotive and Transportation

- Industrial Manufacturing

- Marine

- Consumer Goods and Furniture

By Sales Channel

- Direct Sales

- Industrial Distributors

- Retail and DIY Stores

- E-commerce and Online Specialized Platforms

By Grade

- Industrial Grade

- Technical Grade

- Consumer

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Thinners and Paint Strippers Industry

- 3M Company

- The Sherwin-Williams Company

- PPG Industries, Inc.

- Akzo Nobel N.V.

- BASF SE

- Henkel AG & Co. KGaA

- RPM International Inc.

- Axalta Coating Systems Ltd.

- W.M. Barr & Company, Inc.

- Savogran Company

- Recochem Inc.

- Sunnyside Corporation

- Franmar Chemical, Inc.

- Dumont Chemicals, Inc.

- G.J. Nikolas & Co., Inc.

*- List not Exhaustive