Market Overview: Global Ti-6Al-4V Titanium Alloy Market Value, Growth Outlook & Strategic Insights

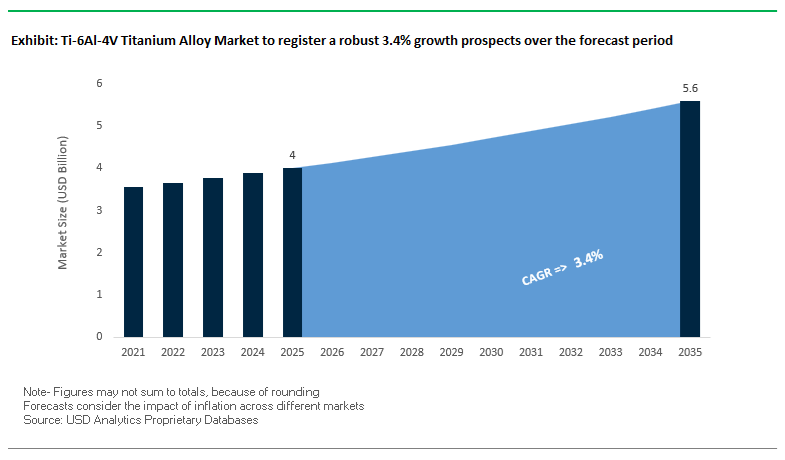

The Global Ti-6Al-4V Titanium Alloy Market is projected to reach USD 4 billion in 2025, expanding to USD 5.6 billion by 2035, reflecting a steady CAGR of 3.4% (2025–2035). The market’s long-term momentum is anchored in its critical role across aerospace engines, airframes, biomedical implants, defense systems, and high-precision industrial components. Manufacturers and vendors continue to prioritize Ti-6Al-4V due to its exceptional strength-to-weight ratio (UTS ~1170 MPa), fatigue strength (≥510 MPa), thermal stability up to 350°C, and biocompatibility, which collectively support its dominance as the world’s most widely used titanium alloy.

The alloy’s adoption is expanding as OEMs seek lightweight materials to improve aircraft fuel efficiency, extend component life cycles, and reduce maintenance downtime. Emerging manufacturing technologies—particularly near-net-shape forging and additive manufacturing (AM)—are addressing machining cost challenges by minimizing waste and enhancing production efficiency. Demand for Ti-6Al-4V ELI (Grade 23) is rising sharply as orthopedic implant manufacturers shift toward materials with tighter interstitial control and fracture toughness compliance. Vendors increasingly emphasize material traceability, NADCAP-certified processes, and AMS-qualified grades to retain competitiveness in a supply chain dominated by stringent aerospace and medical regulations.

Key Market Insights

- Aerospace Dominance: Ti-6Al-4V constitutes 15–25% of total weight in modern commercial jet engines, underpinning durable fan blades, compressor disks, and casings.

- Manufacturing Cost Pressure: Machining the alloy can be 3–5× more expensive than aluminum or stainless steel, accelerating demand for AM powder and engineered extrusions.

- Biomedical Growth: Grade 23 (ELI) adoption accelerates due to ultra-low interstitial content (O ≤0.13%), crucial for orthopedic implants requiring high ductility and fatigue resistance.

- Material Properties Lead Market Preference: High specific strength offers up to 40% advantage over aerospace steel alternatives.

- Supply Chain Shifts: Increasing domestic aerospace titanium output in China (+43% growth from 2021–2024) is reshaping global demand and procurement strategies.

Market Analysis: Expansion Strategies, Supply Chain Movements & Regulatory Shifts Transforming Ti-6Al-4V Alloy Demand

The Ti-6Al-4V Titanium Alloy Market is undergoing structural changes driven by aerospace backlog recovery, geopolitical supply chain realignments, and technological advances in powder metallurgy. In Q1 2025, ATI secured a USD 1-billion multi-year contract with Airbus, reinforcing titanium’s strategic role in next-generation fuel-efficient aircraft. This deal underscores rising OEM commitment to locking long-term alloy supply due to volatile global sponge production capacity. Parallelly, VSMPO-AVISMA’s 2025 announcement to expand titanium sponge output by 3,000 metric tons annually signals an industry-wide effort to stabilize raw material availability amid tightening aerospace demand cycles.

Additive manufacturing is playing an increasingly central role in shaping the market. Prices for AM-grade Ti-6Al-4V powder, historically a major adoption barrier, began softening in 2025, with industry averages moving to USD 120–220/kg. Technology advancements improved powder production yields and consistency, fostering broader application in aerospace brackets, hydraulic system components, and patient-specific implants. The June 2025 expansion by Plymouth Tube in near-net-shape extrusion capabilities exemplifies how suppliers are minimizing machining costs associated with titanium’s low thermal conductivity and work-hardening tendency. This capability is particularly valuable as OEMs push for material efficiency to support sustainability and cost-reduction programs.

On the geopolitical front, China’s domestic titanium aerospace production surged between 2021–2024, growing 43% across key provinces and consuming 58% of aerospace-grade titanium internally. This shift is exerting pressure on global availability for Western aerospace programs, prompting U.S., EU, and Japanese manufacturers to diversify sources and invest in regional titanium processing capacity. Meanwhile, medical titanium standards are tightening: ISO’s update to ISO 5832-11 in 2024 triggered stricter requirements for alloy purity and performance, indirectly raising specification thresholds for Ti-6Al-4V ELI (Grade 23). This regulatory evolution supports stronger quality assurance but increases certification and testing costs for implant manufacturers.

Momentum in the commercial aviation sector significantly influences market direction. Howmet Aerospace reported 17% growth in commercial engine sales in Q3 2024, driven by strong demand for titanium structural castings and rotating engine components that rely heavily on Ti-6Al-4V feedstock. Additionally, Titanium Industries’ participation at Aero India in February 2025 highlights growing opportunities in India’s defense and aerospace manufacturing ecosystem, where the alloy is increasingly used for airframe ribs, landing gear parts, and engine casings. The combination of rising aerospace production rates, expanding medical implant demand, and new manufacturing technologies positions Ti-6Al-4V for sustained long-term growth.

Market Trend 1: Aerospace Qualification of Additively Manufactured Ti-6Al-4V for Lightweight Structural Applications

A major technological transformation in the Ti-6Al-4V (Grade 5) Titanium Alloy Market is the accelerated qualification of additively manufactured (AM) Ti-6Al-4V components for certified aerospace structures. Powder Bed Fusion (PBF) and Directed Energy AM pathways are enabling complex geometries and topology-optimized structures previously impossible with forging or machining, unlocking 30–60% weight reductions in brackets, supports, housings, and lattice-filled components—translating directly into fuel savings and emissions reduction.

Mechanical performance breakthroughs have also validated AM Ti-6Al-4V for demanding flight-critical applications. After Hot Isostatic Pressing (HIP) post-processing, AM components achieve high-cycle fatigue (HCF) life approaching or surpassing 550 MPa at 10⁷ cycles, matching or exceeding wrought and mill-annealed benchmarks. HIP effectively neutralizes internal porosity and lack-of-fusion defects, the primary drivers of fatigue failures in AM parts, enabling consistent and certifiable mechanical behavior.

Thermal treatments further enhance mechanical strength, with AM Ti-6Al-4V routinely achieving Ultimate Tensile Strength (UTS) >950 MPa, fully satisfying industry standards for wrought Grade 5. These developments collectively support the growing movement toward AM-first qualification for aerospace hardware, reducing lead times, minimizing material waste, and enabling unprecedented design freedom.

Market Trend 2: Disruption of Titanium Supply Economics Through Metallothermic and Electrochemical Reduction Routes

A second transformational trend is the global shift toward low-cost titanium production, aimed at replacing the energy-intensive and capital-heavy Kroll process. The Kroll route consumes ≈50 kWh/kg of titanium and requires multistep processing including carbochlorination, TiCl₄ purification, sponge production, and subsequent comminution. Emerging metallothermic and electrochemical technologies—including FFC Cambridge and Metalysis—bypass these steps entirely by producing titanium powder or granules directly from TiO₂ ore (rutile).

These alternative reduction pathways promise >30% cost reductions through simpler process flows, lower energy consumption, and avoidance of high-vacuum distillation. DARPA and industry partners have defined aggressive cost-down targets aligned with these technologies, positioning them as the next generation of supply chain-efficient titanium processing.

Additionally, their ability to use readily available rutile (TiO₂) as a direct feedstock eliminates the need for carbochlorination, expanding raw material flexibility and improving upstream sustainability. As titanium demand rises in aerospace, defense, marine, and AM production, these low-cost routes are poised to fundamentally reshape global titanium supply economics.

Emerging Opportunities in Large-Scale Deposition Technologies and Certified Recycling of Aerospace-Grade Ti-6Al-4V

Market Opportunity 1: Engineering High-Strength, Low-Interstitial WA-DED Wire for Rapid Deposition of Large Titanium Structures

A major commercial opportunity lies in developing high-quality wire feedstock optimized for Wire-Arc Directed Energy Deposition (WA-DED)—a process achieving deposition rates of 5–10 kg/hour, which is 10–100× faster than powder-based AM systems. Such high-throughput capability is crucial for large aerospace, defense, and marine components including frames, ribs, skins, and housings.

Mechanical structure consistency is a critical requirement. Post-Weld Heat Treatment (PWHT) allows WA-DED deposits to reach Yield Strength ≥795 MPa and UTS ≥860 MPa, fully meeting Grade 5 specifications. Similarly, ductility, often limited to ≈4.5% elongation in as-deposited material, can be restored to ≈9.5% after heat treatment, approaching the 10% ductility of wrought Ti-6Al-4V.

To enable certification, wire feedstock must maintain interstitial element concentrations (O, N, C) below thresholds that trigger formation of brittle α′ martensite. Oxygen levels must remain <0.20 wt%, necessitating precision melting, refining, and wire drawing techniques. As WA-DED becomes a cornerstone of large-format AM manufacturing, demand for advanced, crack-resistant, low-interstitial Ti-6Al-4V wire will surge.

Market Opportunity 2: Establishing Certified Closed-Loop Recycling Streams for Aerospace Ti-6Al-4V Swarf and Turnings

Another high-impact opportunity is the creation of certified recycling pathways for aerospace-grade Ti-6Al-4V swarf, addressing both sustainability and cost challenges. Aerospace machining commonly exhibits buy-to-fly ratios of 5:1 to 20:1, meaning 80–95% of primary titanium becomes swarf, representing a massive untapped resource.

Advanced consolidation methods like FAST-forge (Field Assisted Sintering Technology) and powder reclamation deliver dramatic sustainability benefits. Recycling swarf into billets or powder reduces energy consumption by ≈59% and cuts Global Warming Potential (GWP) by ≈68% compared to producing virgin gas-atomized powder.

Purity is crucial for re-certification. After rigorous cleaning, remelted ingots achieve hardness values around 332 ± 6 HV and chemical compositions nearly identical to the original aerospace feedstock. FAST-forge can consolidate loose swarf into ≥99.9% theoretical density billets, ensuring structural integrity for forging into certified aerospace components.

These closed-loop systems enable OEMs to reduce raw material costs, shrink carbon footprints, and achieve circularity targets—all while securing a stable supply of aerospace-grade titanium.

Ti 6Al 4V Titanium Alloy Market Share Analysis

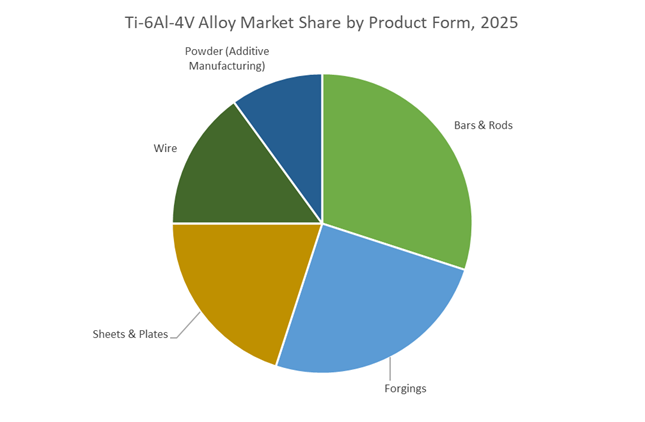

Market Share by Product Form: Bars & Rods Lead Ti-6Al-4V Demand Through Their Central Role in Precision Machining and Forging Workflows

Bars and rods account for the largest share of the Ti-6Al-4V alloy market—approximately 30% in 2025—driven by their indispensable position as primary feedstock for machining and forging across aerospace, medical, industrial, and high-performance engineering applications. Their uniform microstructure and consistent mechanical properties make them the preferred starting material for manufacturing mission-critical components such as high-strength fasteners, landing gear elements, compressor hardware, actuator housings, and precision shafts where dimensional stability and fatigue resistance are essential. In aerospace production workflows, Ti-6Al-4V bars and rods often serve as billets for closed-die forging, directly supporting the fabrication of load-bearing structures and rotating engine components such as discs and blades. This dual role—both as machining stock and as forging input—significantly amplifies the segment’s market relevance. Beyond aerospace, the biocompatibility and corrosion resistance of Ti-6Al-4V drive extensive utilization of bars and rods in orthopedic implants, trauma fixation devices, and custom medical hardware, while industrial sectors rely on them for high-performance fasteners and chemical-resistant components. As global manufacturing increasingly demands high-strength lightweight materials, bars and rods cement their dominance as the most versatile and high-volume product form within the Ti-6Al-4V alloy market.

Market Share by End-Use: Aerospace & Defense Remains the Largest Consumer Due to Performance-Critical Material Requirements

The Aerospace & Defense sector accounts for roughly 55% of the global Ti-6Al-4V alloy market, underscoring the alloy’s central role in modern aircraft, spacecraft, and military platform engineering. Ti-6Al-4V’s exceptional strength-to-weight ratio—providing high tensile strength at only 60% of steel’s density—enables substantial fuel savings and payload optimization, which are critical metrics for both commercial aviation and defense applications. Its ability to retain mechanical integrity at temperatures approaching 350°C makes it indispensable for the compressor sections of jet engines, including discs, blades, rings, and casings subjected to severe thermal cycling and high mechanical loads. In commercial widebody aircraft such as the Boeing 787 and Airbus A350, titanium alloys account for 14–15% of structural weight, with Ti-6Al-4V being the primary grade used for bulkheads, wing attachments, landing gear elements, and high-load airframe structures. Defense applications further elevate demand through requirements for armor systems, missile components, rotary-wing structures, and high-performance propulsion systems where lightweight durability directly enhances mission capability. With ongoing fleet modernization, rising production of fuel-efficient aircraft, and expanding defense procurement, the aerospace and defense segment remains the largest and most strategically important end-use category shaping global Ti-6Al-4V alloy consumption.

Country Analysis: Global Drivers in Ti-6Al-4V Titanium Alloy Development

United States: Aerospace Rebound, AM Powder Expansion, and Defense-Driven Ti-6Al-4V Demand

The United States remains one of the most influential markets for Ti-6Al-4V, driven by powerful growth in commercial aerospace programs, defense priorities, and rapid adoption of metal additive manufacturing (AM). In Q1 2025, ATI Metals secured a five-year, $1+ billion titanium supply contract with Airbus, reinforcing U.S. dominance in global aerospace-grade Ti-6Al-4V supply chains and ensuring long-term demand for forgings, bar, and mill products. This trend is strengthened by Howmet Aerospace, which reported 17% commercial aerospace sales growth in Q3 2024, a milestone reflecting surging demand for engine discs, blades, and rotating structural components made from Ti-6Al-4V and related alloys.

A transformative shift in the U.S. titanium landscape is the scaling of Additive Manufacturing (AM) powder production, where companies such as Tekna and ATI are expanding highly spherical, high-purity Ti-6Al-4V powder output tailored for SLM and EBM platforms. These AM powders reduce lead times, optimize buy-to-fly ratios, and support near-net-shape production of complex airworthy components. From a defense perspective, Ti-6Al-4V accounts for ~42% of titanium usage in aerospace applications in 2025, playing a critical role in stealth aircraft frames, next-generation jet engines, and high-strength landing gear. The U.S. market is expected to maintain its leadership as military modernization and commercial aircraft backlog growth continue to demand large volumes of high-performance titanium alloy.

China: Expanding Titanium Alloy Manufacturing and Accelerating Progress Toward Aero-Certified Ti-6Al-4V

China is undergoing massive expansion in its Ti-6Al-4V Titanium Alloy output, leveraging its commanding position as the world’s largest titanium metal producer—approximately 60% of global supply. This provides an unmatched raw-material foundation for large-scale alloy manufacturing. The Chinese aerospace ecosystem is investing heavily in large forging presses, rolling mills, and heat-treatment lines to produce certified Ti-6Al-4V plates, sheets, and forgings for rapidly growing domestic commercial aircraft programs such as COMAC C919 and military airframes. These investments aim to close the long-standing certification gap with Western aerospace suppliers.

China’s research institutions are also making rapid progress in Additive Manufacturing of Ti-6Al-4V, addressing a key barrier: anisotropic mechanical properties caused by layer-wise AM microstructures. Studies published in 2025 focus on fatigue enhancement and microstructure homogenization, crucial for enabling future certification in high-stress aerospace components. Beyond aerospace, China maintains significant production capacity of Ti-6Al-4V ELI (Grade 23) for orthopedic implants and dental devices, supported by strong domestic healthcare demand and competitive export pricing. With its blend of scale, industrial policy, and expanding R&D output, China is strengthening its position as both a volume leader and a rising quality competitor in the global Ti-6Al-4V market.

European Union (Germany/France): High-Purity Casting, Aerospace-Certified Fabrication, and Medical AM Solutions

Europe—particularly Germany and France—remains a global center for advanced, high-precision Ti-6Al-4V fabrication, driven by robust aerospace supply chains and leadership in medical implant technologies. Over 46% of German titanium production for aerospace is consumed by EU-certified aircraft programs, underscoring Europe’s specialization in high-purity, high-performance mill products that meet strict AMS, EN, and OEM-specific specifications. The region has seen a 29% rise in laser AM production of Ti-6Al-4V components from 2021–2024, reflecting widespread adoption of near-net-shape manufacturing to lower machining requirements and material waste—critical advantages given titanium’s high cost.

Europe also expanded its high-purity casting capacity by 33% between 2021 and 2024, enabling production of complex, defect-sensitive components such as engine casings, compressor housings, and structural airframe nodes. European medical device manufacturers are equally advanced in applying Ti-6Al-4V ELI (Grade 23) to produce patient-specific orthopedic implants, supported by strong hospital adoption of 3D-printed hip, spine, and knee replacements. With its deep engineering expertise and stringent quality frameworks, the EU remains a cornerstone of global Ti-6Al-4V innovation across aerospace, industrial, and biomedical sectors.

Japan: Global Supplier of High-Purity Titanium Sponge and Specialist in Engine-Grade Ti-6Al-4V Components

Japan plays an essential upstream role in the Ti-6Al-4V Titanium Alloy Market as a premier supplier of high-purity titanium sponge, the critical feedstock required for aerospace-grade alloy production. Companies such as Toho Titanium Co., Ltd. and OSAKA Titanium Technologies Co., Ltd. deliver some of the world’s most consistent, certified sponge used by global mills to melt Ti-6Al-4V products meeting AMS, JIS, and ASTM standards. Japan’s stringent quality control and decades of sponge production experience make it a vital partner for international aerospace and medical titanium supply chains.

Japan also manufactures high-specification Ti-6Al-4V mill products and precision components for both civil and defense aerospace applications. These include engine compressor parts, airframe reinforcements, and hot-section components requiring exceptional creep strength and fatigue resistance. With strong compliance to global aerospace standards and a reputation for materials excellence, Japan continues to anchor the high-purity end of the global titanium value chain.

Russia: Historically Significant Sponge Supplier with Heightened Geopolitical Risk

Russia remains a major global supplier of titanium sponge and Ti-6Al-4V mill products, primarily through VSMPO-AVISMA, one of the world’s largest integrated titanium producers. The company has historically supplied substantial Ti-6Al-4V volumes to Western aerospace OEMs, contributing to global engine programs and commercial aircraft platforms. VSMPO-AVISMA’s extensive integration—from sponge to mill products—has traditionally ensured competitive pricing and stable supply.

However, ongoing geopolitical tensions and trade restrictions (2024–2025) have significantly altered the reliability of Russian titanium in Western supply chains. Aerospace manufacturers are accelerating qualification of alternative suppliers across the U.S., Japan, and Europe, decreasing reliance on Russian sponge. Despite possessing major global production capacity, Russia’s future influence is now highly dependent on political developments and the restructuring of international titanium procurement strategies.

Competitive Landscape: Key Producers Shaping the Global Ti-6Al-4V Titanium Alloy Supply Chain

Global competition in the Ti-6Al-4V Titanium Alloy Industry is shaped by vertically integrated producers, aerospace-qualified forging specialists, and AM-focused high-purity powder suppliers. Companies compete based on certification depth, material traceability, advanced melting technology, and long-term contracts with major aircraft OEMs. The market remains moderately consolidated, with a handful of suppliers holding critical aerospace and medical approvals that create high entry barriers.

Allegheny Technologies Incorporated (ATI): Strengthening Aerospace Titanium Leadership

ATI is a major U.S.-based titanium and specialty alloy producer operating an end-to-end value chain from sponge to mill products. Its portfolio includes Ti-6Al-4V sheet, plate, bar, and advanced forgings, making it a preferred supplier for aerospace OEMs requiring strict metallurgical consistency. ATI secured a landmark USD 1-billion Airbus contract in Q1 2025, ensuring stable multi-year demand for Ti-6Al-4V aerospace products. With 66% of its revenue tied to aerospace and defense, ATI maintains deep integration through isothermal forging, heat treatment, and precision casting capabilities.

TIMET (Titanium Metals Corporation): Vertically Integrated Capability Under PCC

TIMET, part of Precision Castparts Corp., is one of the most established global suppliers of Ti-6Al-4V ingots, billets, bars, and plates qualified under AMS standards. As a vertically integrated operation—from sponge processing to final component manufacturing—it supports PCC’s aerospace component production, including landing gear and structural castings. TIMET’s AS9100 and NADCAP certifications ensure compliance for civil and military aviation programs, cementing its position as a trusted supplier for critical safety-grade titanium parts.

VSMPO-AVISMA Corporation: Global Titanium Powerhouse with Expanding Capacity

VSMPO-AVISMA is the world’s largest titanium producer, controlling the complete production cycle from raw ore to finished semi-products. Its Ti-6Al-4V billets and forgings are widely used by global aircraft manufacturers. In 2025, the company announced a 3,000-ton annual expansion in sponge production, aimed at supporting the growing titanium requirements of commercial aircraft programs. Despite geopolitical challenges, VSMPO remains essential to global supply chains, historically providing nearly one-quarter of aerospace titanium worldwide.

Kobe Steel Ltd.: Precision Titanium Supplier for Aerospace Fasteners

Kobe Steel of Japan supplies high-precision Ti-6Al-4V bar and rod products for aerospace fasteners and small engine components. Drawing on decades of metallurgical expertise, the company emphasizes purity, fatigue performance, and consistency needed for safety-critical fastening systems. With proprietary melting and forging technologies, Kobe Steel continues to upgrade fatigue life and microstructural uniformity, targeting applications subjected to high cyclic loading.

Carpenter Technology Corporation: Advanced Ti-6Al-4V ELI and AM Powder Innovator

Carpenter Technology specializes in high-performance titanium alloys, including Ti-6Al-4V ELI (Grade 23) for medical implants and aerospace fasteners. The company is a leader in producing fine spherical Ti-6Al-4V powder for additive manufacturing under the CarTech brand, supporting orthopedic implant customization and lightweight aerospace component designs. Carpenter’s strong focus on traceability and certification ensures alignment with FAA and FDA requirements, making it a preferred supplier for critical, regulated applications.

Ti-6Al-4V Titanium Alloy Market Report Scope

Ti-6Al-4V Titanium Alloy Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$4 Billion

|

|

Market Size (2035)

|

$5.6 Billion

|

|

Market Growth Rate

|

3.4%

|

|

Segments

|

By Grade (Grade 5, ELI Grade 23, Castings), By Product Form (Bars & Rods, Forgings, Sheets & Plates, Wire, Powder), By Manufacturing Process (Conventional Manufacturing, Additive Manufacturing), By End-Use Application (Aerospace & Defense, Medical & Healthcare, Industrial Processing, Automotive, Oil & Gas)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Precision Castparts/TIMET, Allegheny Technologies, VSMPO-AVISMA, Howmet Aerospace, Baoji Titanium Industry, Toho Titanium, Osaka Titanium Technologies, Kobe Steel, Carpenter Technology, Aubert & Duval, GfE Elektrometallurgie, Tekna Holding, Nippon Steel, Western Superconducting Technologies, Heraeus Group

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Ti-6Al-4V Titanium Alloy Market Segmentation

By Grade

- Ti-6Al-4V Grade 5

- Ti-6Al-4V ELI (Grade 23)

- Ti-6Al-4V Castings

By Product Form

- Bars & Rods

- Forgings

- Sheets & Plates

- Wire

- Powder (Additive Manufacturing)

By Manufacturing Process

- Conventional Manufacturing

- Additive Manufacturing

By End-Use Industry

- Aerospace & Defense

- Medical & Healthcare

- Industrial Processing

- Automotive

- Oil & Gas

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Ti-6Al-4V Titanium Alloy Market

- Precision Castparts / TIMET

- Allegheny Technologies (ATI)

- VSMPO-AVISMA

- Howmet Aerospace

- Baoji Titanium Industry (BAOTAI)

- Toho Titanium

- Osaka Titanium Technologies

- Kobe Steel

- Carpenter Technology

- Aubert & Duval

- GfE Elektrometallurgie

- Tekna Holding

- Nippon Steel

- Western Superconducting Technologies

- Heraeus Group.

*- List not Exhaustive

Research Coverage

The latest Ti-6Al-4V Titanium Alloy Market study from USDAnalytics provides a comprehensive, data-backed outlook on this critical aerospace and biomedical alloy through 2034. Drawing on global production, trade and application datasets, this report investigates long-term demand shifts across aircraft engines, airframes, implants, defense platforms, automotive and industrial systems, while benchmarking mechanical performance, cost structures and qualification pathways. It delivers in-depth analysis reviews of emerging manufacturing routes such as additive manufacturing, near-net-shape forging, Wire-Arc DED and next-generation reduction technologies that may disrupt traditional Kroll-based supply economics. The study highlights how OEM backlogs, evolving ISO/AMS standards, and regional rebalancing of sponge and mill-product capacity are reshaping procurement strategies, including the growing importance of Grade 23 (ELI) in high-fatigue medical applications. Technology breakthroughs in AM powders, HIP post-processing, closed-loop recycling and low-interstitial wire feedstock are critically assessed alongside competitive moves by leading mills, forgers and powder producers. With detailed forecasts, value chain risk mapping, pricing commentary and policy impact assessment, this report is an essential resource for aerospace primes, medical device manufacturers, titanium producers, investors and regulators seeking to understand where the Ti-6Al-4V titanium alloy market is heading and how to position within it.

Scope Highlights

- Segmentation:

By Grade: Ti-6Al-4V Grade 5; Ti-6Al-4V ELI (Grade 23); Ti-6Al-4V Castings

By Product Form: Bars & Rods; Forgings; Sheets & Plates; Wire; Powder (Additive Manufacturing)

By Manufacturing Process: Conventional Manufacturing; Additive Manufacturing

By End-Use Industry: Aerospace & Defense; Medical & Healthcare; Industrial Processing; Automotive; Oil & Gas

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

- Timeframe: Historic data from 2021 to 2025 and forecast data from 2026 to 2034.

- Companies: Analysis / profiles of 15+ companies across the global Ti-6Al-4V titanium alloy value chain.