Tobacco Packaging Market Size, Overview, and Growth Outlook (2025–2034)

Tobacco Packaging Market Set to Reach $32.7 Billion by 2034 Amid Regulatory Shifts and Brand Innovation

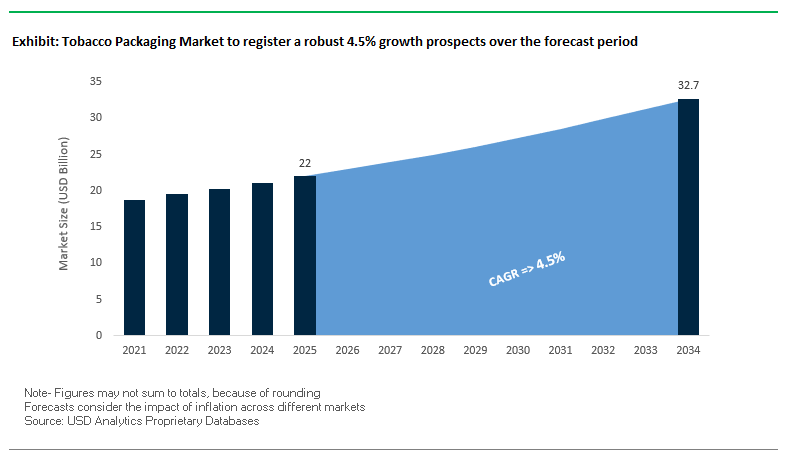

The global tobacco packaging market is projected to grow from $22 billion in 2025 to $32.7 billion by 2034, at a CAGR of 4.5%. This market is at the intersection of regulatory compliance, technological innovation, and consumer behavior shifts, offering unique challenges and opportunities for packaging manufacturers and brand owners.

Key Insights for industry professionals and buyers:

- Regulatory compliance is reshaping design strategies, with plain packaging mandates requiring prominent health warnings and removal of brand logos and colors.

- Innovation in heated tobacco units (HTUs) and next-generation products is driving demand for differentiated packaging solutions outside traditional cigarette regulations.

- Advanced printing and finishing techniques such as embossing, varnishes, and tactile textures are being leveraged to maintain a premium feel and brand identity.

- Anti-counterfeiting and secure packaging solutions are increasingly critical, incorporating QR codes, holograms, and track-and-trace technologies.

- Sustainability focus is rising, with developments in recyclable materials and mono-material packaging that reduce environmental impact.

The market presents substantial opportunities for material science innovation, security-enhanced packaging, and sustainable solutions, making it highly relevant for tobacco brand owners, packaging designers, and compliance-focused stakeholders.

Market Analysis: Strategic Innovations and Material Advancements Are Driving the Tobacco Packaging Market

The tobacco packaging industry is rapidly evolving, with technological innovation and sustainability initiatives taking center stage. In August 2025, Mondi launched a new flexible packaging grade, Borcycle™ M, enhancing performance in tobacco applications. Concurrently, Borealis partnered with IMCD for the Americas, showcasing the potential of advanced material science applications across industries, including tobacco packaging.

Sustainability-led developments continue to transform packaging approaches. In June 2025, Mondi introduced recyclable mono-material bags for dry pet food, signaling a broader trend toward circular packaging that can influence tobacco packaging designs. Similarly, April 2025 saw Mondi develop a recyclable pre-made paper bag for chemical powders with Evonik, replacing plastic-coated layers and reducing carbon footprint. Innovative product features like LINDAL Group's FlipStraw dual spray actuator launched in April 2025 also emphasize functionality improvements with reduced material waste.

Consolidation and strategic partnerships are shaping the competitive landscape. In January 2025, International Paper and DS Smith combined to enhance global capabilities in sustainable packaging, extending potential benefits to tobacco packaging. Academic insights from October 2024 highlighted the use of 25% sugarcane bagasse fiber in biodegradable films, improving mechanical properties and water vapor resistance—a promising innovation for sustainable tobacco packs.

Trends and Opportunities in the Tobacco Packaging Market

Global Implementation of Standardized (Plain) Packaging Regulations

The tobacco packaging market is undergoing a paradigm shift with the widespread adoption of plain packaging laws, fundamentally altering the industry’s design and branding strategies. As of 2024, at least 25 countries and territories—including Saudi Arabia, Israel, and Turkey—have fully adopted standardized packaging, compared to only nine in 2018. This acceleration reflects the influence of the WHO Framework Convention on Tobacco Control (FCTC), which encourages governments to use packaging as a regulatory tool.

Plain packaging mandates the use of Pantone 448C (often referred to as the “world’s ugliest color”), large graphic health warnings covering up to 90% of pack surfaces, and uniform typography for brand names. This eliminates tobacco packaging’s role as a marketing differentiator and repositions it as a compliance-driven platform. Market studies show that plain packaging has a direct impact on consumer behavior, making smokers more price-sensitive and encouraging a shift from premium to budget categories. For manufacturers, this regulatory pressure increases the need to compete on pricing strategies, product innovation, and alternative nicotine offerings rather than packaging aesthetics.

Integration of Covert and Overt Anti-Counterfeiting Technologies

As branding diminishes, security and authenticity features are becoming central to tobacco packaging innovation. The European Union’s Tobacco Products Directive requires unique identifiers and traceability for every pack, driving investment in covert and overt authentication technologies. Companies are deploying invisible inks, micro-text, and smartphone-enabled verification systems to combat counterfeiting and illicit trade, which remains a significant global challenge.

Multi-layered protection strategies now extend beyond basic holograms to include semi-covert inks visible only under UV light, color-shifting inks activated by touch, and fiber-embedded substrates detectable only with specialized equipment. Countries such as Latvia are mandating covert features, creating a robust regulatory framework for product security. The emphasis on counterfeit deterrence not only protects brand equity but also safeguards government tax revenues. For industry leaders, the integration of authentication technologies into standardized packaging is becoming both a regulatory requirement and a strategic differentiator.

Development of Sustainable and Recyclable Barrier Papers

The industry faces growing pressure to replace non-recyclable aluminum foils and multilayer plastics used in inner liners, which are significant contaminants in recycling streams. This presents a strong opportunity for sustainable barrier papers engineered to meet moisture retention and freshness requirements while being compatible with conventional paper recycling systems.

Mondi’s FunctionalBarrier Paper Ultimate, launched with a €16 million investment, delivers oxygen and water vapor transmission rates (OTR) below 0.5, enabling it to match foil performance while being recyclable. Similarly, Nissha Metallizing Solutions has introduced metallized papers that balance barrier integrity with sustainability, offering a film- and foil-free alternative aligned with circular economy objectives. The ability to combine premium protection with recyclability makes this opportunity highly attractive to manufacturers seeking to meet consumer and regulatory sustainability demands without compromising product integrity.

Packaging as a Platform for Reduced-Risk Product (RRP) Communication

While cigarette packaging is increasingly restricted, reduced-risk products (RRPs) such as heated tobacco, nicotine pouches, and vaping devices present a new frontier for packaging innovation. With traditional advertising heavily regulated, packaging becomes a critical communication channel to educate consumers about usage, differentiate product categories, and highlight relative risk profiles.

Companies like SWM International are developing biosourced wrapping papers for nicotine pouches, which not only reduce environmental impact but also offer a premium tactile and visual experience. For heated tobacco devices, specialized packaging must address device protection, modular storage, and safety labeling. This creates opportunities to design packaging that serves both functional and informational roles, particularly as RRPs grow in acceptance among regulators and consumers. By leveraging packaging as a compliance-driven yet experience-enhancing medium, tobacco companies can position RRPs as distinct from traditional cigarettes while maintaining a premium market presence.

Competitive Landscape: Leading Tobacco Packaging Companies Are Redefining Market Standards with Sustainability and Security

The tobacco packaging market is driven by a handful of key players leveraging material innovation, regulatory compliance, and sustainability initiatives to maintain competitive advantage.

Smurfit Kappa Group PLC: Advancing Paper-Based Tobacco Packaging with Circular Economy Solutions

Smurfit Kappa specializes in folding cartons and display solutions for tobacco, emphasizing sustainability through its Better Planet 2050 plan. The company invests in advanced paper and corrugated technologies, ensuring packaging is both compliant and environmentally responsible. Its strong focus on material innovation and end-use customization makes it a key partner for tobacco manufacturers.

WestRock Company: Combining Vertically Integrated Expertise with Sustainable Paperboard Solutions

WestRock provides paperboard, folding cartons, and packaging solutions tailored to tobacco products. Its Commitment to a Better World strategic plan drives innovation in circular packaging and sustainable materials. With a globally integrated manufacturing network, WestRock ensures high-quality, compliant solutions while minimizing environmental impact.

Amcor plc: Delivering Flexible and Rigid Packaging with Advanced Recyclability for Tobacco Products

Amcor offers films, laminates, and thermoform blister systems designed to protect and preserve tobacco products. In August 2025, the company upgraded its UK recycling facility and expanded AmSky™ PVC-free, aluminum-free solutions, reflecting a commitment to circular economy and sustainability. Its vertically integrated operations enable scalable, high-quality packaging solutions globally.

International Paper Company: Pioneering Sustainable Paper and Paperboard Innovations for Tobacco Packaging

International Paper produces tailored paper and paperboard products for tobacco applications, integrating innovations like PolariSoft® fluff pulp to enhance performance. Its IP Way Ahead plan emphasizes reducing environmental footprint and supporting circular packaging through material research and development.

Mondi Group: Reducing Plastic Footprint While Offering Recycle-Ready Packaging Solutions

Mondi focuses on flexible plastic packaging and barrier films, providing recyclable and sustainable alternatives. In June 2025, it launched recyclable mono-material bags for dry products and developed Hug&Hold, a paper-based plastic alternative. Mondi’s strategy aligns with its 2030 sustainability targets, promoting recyclable, reusable, or compostable solutions across packaging sectors.

Tobacco Packaging Market Share Insights, 2025-2034

Primary Packaging Dominates Market Share by Packaging Type in Tobacco Packaging Industry

Primary packaging accounts for the largest share of the tobacco packaging market at nearly 60%, reflecting the central role it plays in regulatory compliance and product integrity. Cigarette packs, foil-lined wrappers, and moisture-barrier containers are the first line of defense in ensuring freshness, aroma retention, and consumer safety. Global plain packaging laws and graphic health warnings disproportionately target this category, making it the most heavily engineered and regulated format. Packaging manufacturers have been compelled to prioritize material cost-efficiency, tamper-evident features, and high-speed manufacturability, while still meeting stringent health and safety mandates. As governments continue to intensify restrictions on tobacco marketing, primary packaging has become the focal point of regulatory scrutiny, cementing its dominance within the industry.

Cigarettes Retain Majority Share by Product Type in Tobacco Packaging Industry

Cigarettes remain the dominant product type, representing nearly 65% of the global tobacco packaging market, despite volume declines in mature economies. Their dominance is anchored in sheer consumption scale across emerging markets, which continues to drive immense demand for standardized, cost-effective packaging formats. Cigarette packaging is manufactured at a massive scale, with billions of packs produced annually, requiring high-speed printing, embossing, and foil lamination processes. While next-generation products such as e-cigarettes and heated tobacco are growing rapidly, cigarettes still attract the greatest regulatory attention, including large-format health warnings and track-and-trace features under frameworks like the WHO FCTC Protocol. This entrenched regulatory-driven demand ensures that cigarette packaging continues to command the largest share of the industry.

India: Stricter Health Warnings and Sustainable Packaging Initiatives

The India tobacco packaging market is undergoing a major transformation with the Cigarettes and Other Tobacco Products (Packaging and Labelling) Amendment Rules, 2024, which came into effect on June 1, 2025. The updated law mandates that health warnings must cover 85% of the principal display area, comprising 60% pictorial warnings and 25% textual warnings. A new textual warning—“TOBACCO CAUSES PAINFUL DEATH”—is now mandatory, accompanied by a toll-free quitline number. These regulatory changes are designed to deter tobacco consumption, encourage cessation, and prevent uptake among youth.

Alongside health legislation, India is also experiencing growth in sustainable tobacco packaging driven by the e-commerce and retail sectors. Companies are adopting eco-friendly materials with enhanced traceability features such as barcodes and QR codes. This dual push for public health awareness and packaging sustainability is reshaping India’s tobacco packaging industry, pushing manufacturers to adapt to both compliance and consumer expectations.

European Union: Tax Revisions and Secure Packaging to Curb Illicit Trade

In the European Union tobacco packaging market, regulation continues to intensify. On July 16, 2025, the European Commission adopted a proposal to recast the Tobacco Taxation Directive (TTD), expanding taxation to new product categories like e-cigarettes, heated tobacco, and nicotine pouches. This shift will drive new packaging formats, particularly in emerging segments such as next-generation tobacco products. Additionally, the introduction of the Excise Movement and Control System (EMCS) for raw tobacco will enhance traceability and security, pushing companies to adopt advanced anti-counterfeiting measures.

The Packaging and Packaging Waste Regulation (PPWR), effective February 2025, is also driving sustainability by mandating recycled content in all packaging by 2030. Combined with the EU’s public health goal of reducing tobacco usage to below 5% of the population by 2040, packaging innovation is increasingly focused on sustainability, transparency, and compliance. Companies operating in the EU must therefore balance strict regulatory demands with eco-friendly design.

United States: Legal Disputes and Anti-Counterfeiting Packaging Measures

The United States tobacco packaging market remains shaped by ongoing regulatory and legal challenges. The FDA’s final rule on requiring 11 new cigarette health warnings with color graphics is under litigation, with a preliminary injunction in January 2025 delaying enforcement. This legal uncertainty underscores the tobacco industry’s resistance to stricter packaging controls.

Despite this, companies are investing heavily in track-and-trace technologies, such as QR codes, tamper-evident seals, and digital authentication features, to address the growing problem of illicit trade. The American Lung Association’s “State of Tobacco Control 2025” report further emphasizes the industry’s lobbying efforts to delay or dilute regulations on menthol cigarettes and flavored cigars. These dynamics indicate that while the U.S. is slower to enforce graphic warnings compared to other regions, supply chain security and packaging innovation are becoming central to compliance and competitiveness.

China: Limited Warning Regulations and Strong Focus on Branding

The China tobacco packaging market differs significantly from other major regions due to its less restrictive packaging legislation. Current regulations only require text warnings covering 30% of the front and back of packs, leaving significant space for brand imagery and promotional content. This flexibility gives tobacco companies more room to influence consumer perception through packaging design.

However, the State Tobacco Monopoly Administration (STMA) maintains strict control over supply chains, requiring security features and standardized packaging materials to maintain oversight. At the same time, China’s broader policies, such as incentives for remanufacturing and green technology adoption, are encouraging a gradual shift toward sustainable materials in packaging. While public health warnings remain limited compared to global standards, the push for eco-friendly innovation and supply chain transparency is slowly reshaping the landscape.

Japan: Heated Tobacco Products Driving Premium Packaging Demand

The Japan tobacco packaging market is dominated by the rapid adoption of Heated Tobacco Units (HTUs), which are seeing substantial demand from consumers. Global leaders like Japan Tobacco International (JTI) and Philip Morris International (PMI) are introducing high-value, premium packaging designs tailored to HTUs, with advanced materials, sleek aesthetics, and portability.

Sustainability is also shaping the market. The Plastic Resource Circulation Strategy mandates that all plastic packaging must be reusable or recyclable by 2025, while the Plastic Resource Circulation Promotion Law, effective the same year, enforces redesign or reduction of 12 categories of single-use plastics. As a result, Japanese manufacturers are exploring compostable alternatives and innovative materials to align tobacco packaging with national sustainability goals while supporting the premium positioning of HTUs.

Brazil: Longstanding Warning Culture and Waste Reduction Policies

The Brazil tobacco packaging market is deeply influenced by its progressive health-warning framework, being the second country globally to adopt pictorial warnings back in 2001. Since then, Anvisa (the National Sanitary Surveillance Agency) has continuously updated regulations, including 2017 rules linking toxic substances in tobacco to familiar items and illnesses, making warnings more impactful.

Sustainability is equally important, with the National Solid Waste Policy (PNRS) enforcing recycling, reuse, and reduction. The January 2025 ban on solid waste imports further strengthens domestic waste management and emphasizes the need for eco-friendly tobacco packaging materials. This combination of longstanding anti-tobacco measures and strong circular economy policies makes Brazil one of the most progressive markets for tobacco packaging innovation and regulation.

Tobacco Packaging Market Report Scope

Tobacco Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$22 Billion

|

|

Market Size (2034)

|

$32.7 Billion

|

|

Market Growth Rate

|

4.5%

|

|

Segments

|

By Material (Paper and Paperboard, Plastics, Metals, Other Materials), By Packaging Type (Primary Packaging, Secondary Packaging, Bulk/Transit Packaging), By Product Type (Cigarettes, Cigars & Cigarillos, Smokeless Tobacco, Next-Generation Products)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Mondi Group, WestRock Company (now Smurfit Westrock), Amcor plc, Huhtamaki Oyj, Smurfit Kappa Group, ITC Limited, DS Smith plc, International Paper, Ruenfo, Siegwerk Druckfarben AG & Co. KGaA, Sonoco Products Company, AR Packaging, BillerudKorsnäs AB, Stora Enso Oyj, Walki Group

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Tobacco Packaging Market Segmentation

By Material

- Paper and Paperboard

- Plastics

- Metals

- Other Materials

By Packaging Type

- Primary Packaging

- Secondary Packaging

- Bulk/Transit Packaging

By Product Type

- Cigarettes

- Cigars & Cigarillos

- Smokeless Tobacco

- Next-Generation Products

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Tobacco Packaging Market

- Mondi Group

- WestRock Company (now Smurfit Westrock)

- Amcor plc

- Huhtamaki Oyj

- Smurfit Kappa Group

- ITC Limited

- DS Smith plc

- International Paper

- Ruenfo

- Siegwerk Druckfarben AG & Co. KGaA

- Sonoco Products Company

- AR Packaging

- BillerudKorsnäs AB

- Stora Enso Oyj

- Walki Group

* List Not Exhaustive

Methodology

USDAnalytics employs a comprehensive and industry-focused research methodology to analyze the global tobacco packaging market, combining both qualitative and quantitative insights. Our approach integrates primary research through interviews with packaging manufacturers, brand owners, regulatory experts, and supply chain stakeholders, alongside secondary research from corporate reports, regulatory publications, and trade data. USDAnalytics evaluates market dynamics including plain packaging regulations, anti-counterfeiting technologies, sustainable and recyclable materials, and innovations in next-generation tobacco products (HTUs, e-cigarettes, nicotine pouches). The research encompasses regional regulatory frameworks and market drivers across the United States, European Union, China, India, Japan, and Brazil, analyzing their impact on product design, material adoption, and packaging security. We also assess technological advancements such as advanced printing, embossing, barrier papers, and track-and-trace solutions. Market sizing, CAGR projections, and growth opportunities are derived using historical trends, adoption rates, and innovation-led expansion, offering actionable insights for tobacco brand owners, packaging designers, investors, and compliance professionals seeking competitive advantage through innovation, sustainability, and regulatory alignment.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.