High-Performance Finishes, Aesthetic Innovation, and Sustainability Driving Steady Growth

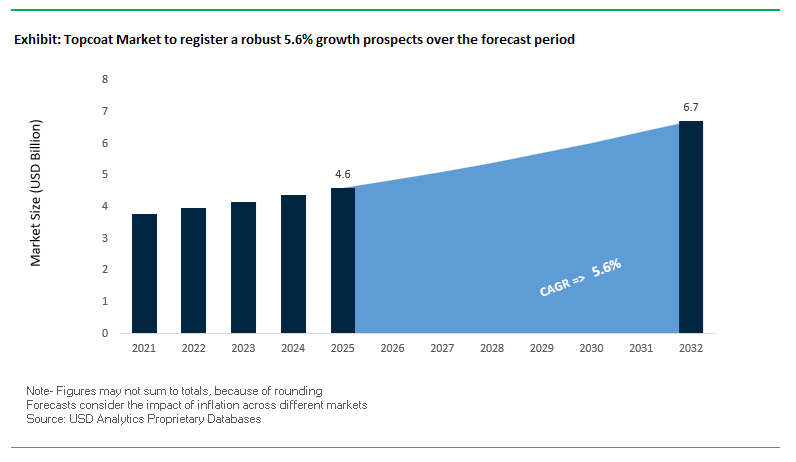

The global Topcoat Market is expanding steadily, supported by rising demand for protective and decorative finishing layers across automotive, construction, wood, and industrial applications. The market was valued at $4.6 billion in 2025 and is projected to reach $6.7 billion by 2032, growing at a CAGR of 5.6% during 2025–2032. This growth is driven by the increasing importance of topcoats as the final performance layer, delivering UV resistance, chemical protection, gloss retention, and aesthetic appeal.

A key structural driver is the growing demand for high-performance topcoats in automotive and industrial sectors, where coatings must withstand harsh environmental conditions while maintaining visual quality. In automotive applications, topcoats are evolving to support electric and autonomous vehicles, requiring enhanced durability, color stability, and compatibility with advanced sensors. Similarly, in construction and wood coatings, topcoats are essential for weather resistance, scratch protection, and long-term surface integrity.

Another major trend is the shift toward eco-friendly and waterborne topcoat systems, driven by stringent environmental regulations and sustainability goals. Manufacturers are increasingly adopting low-VOC, high-solids, and water-based formulations that reduce emissions while maintaining performance. This transition is particularly evident in automotive OEM and refinish segments, where regulatory compliance is a critical factor.

Aesthetic innovation is also playing a central role in market growth. The development of multi-dimensional colors, interference pigments, and texture-enhancing finishes is enabling topcoats to deliver unique visual effects, enhancing product differentiation. Additionally, advancements in application efficiency and automation technologies are improving productivity and reducing operational costs in coating processes.

Market Analysis: High-Solids Automotive Systems, Wood Finish Innovation, and Strategic Consolidation Reshaping Competitive Landscape

The topcoat market is being reshaped by product innovation, strategic mergers, and sustainability-driven manufacturing expansion, reflecting the growing importance of both performance and design. The March 2026 merger between AkzoNobel and Axalta represents a significant consolidation move, combining their strengths in industrial, automotive, and decorative topcoats, and enabling enhanced R&D capabilities for next-generation coating technologies.

Design-driven innovation is particularly prominent in wood and interior applications. AkzoNobel’s “Rhythm of Blues” collection (March 2026) introduces specialized topcoat shades designed for cabinetry and flooring, emphasizing durability and aesthetic depth. This reflects the increasing role of topcoats in premium interior design and customization trends.

In the automotive sector, Axalta’s “Solar Boost” 2026 Color of the Year highlights the integration of advanced pigment technologies into topcoats, creating dynamic color effects that change with light exposure. Similarly, BASF’s “Driving the Proxy” collection introduces multidimensional finishes such as Tesseract Blue, which utilize interference pigments to enhance visual depth.

Performance-driven innovation is also evident in commercial and industrial coatings. Axalta’s Standox Standofleet HS Pro (October 2025) and Spies Hecker’s Permafleet HS Race Topcoat 690 focus on high-solids formulations and rapid application cycles, enabling faster throughput without compromising durability or gloss. PPG’s VELOCITY® refinish system further enhances efficiency by integrating automated paint mixing technologies for color accuracy and reduced repair times.

Sustainability initiatives are shaping production strategies. PPG’s March 2025 expansion of its waterborne automotive coatings facility in Thailand supports the growing demand for eco-friendly topcoat systems in Southeast Asia’s automotive manufacturing hub.

In the wood and flooring segment, AkzoNobel’s ArmorLux innovations (July 2025) introduce robust and waterborne topcoats designed for flooring and exterior wood applications, emphasizing durability and reduced rework for OEMs.

Strategic realignment is also strengthening market positioning. Kansai Nerolac’s February 2026 merger with Nerofix consolidates its topcoat and adhesive portfolio, enhancing its presence in industrial and decorative coatings. Meanwhile, Hempel’s “Accelerate to Win” strategy (January 2026) focuses on expanding marine and energy topcoats, leveraging durability to reduce emissions and extend asset lifecycles.

Market Trend: FAA and DoD 2026 Enforcement Accelerates Elimination of Hexavalent Chromium in Aerospace Topcoats

The aerospace topcoat industry is undergoing a structural transition as the Federal Aviation Administration and the U.S. Department of Defense enforce the phase-out of hexavalent chromium across coating systems aligned with MIL-PRF-85582 and MIL-PRF-85285 specifications. Historically, Cr6+ compounds have been critical for corrosion inhibition, particularly in high-strength aluminum alloys such as AA7075-T6. However, the 2026 regulatory milestone mandates that chromate-free topcoats achieve equivalent or superior performance without the associated toxicity risks. To meet compliance, next-generation formulations must demonstrate corrosion resistance exceeding 3,000 hours in neutral salt spray testing, a benchmark previously dominated by chromated systems. Additionally, these coatings are required to maintain structural integrity under extreme thermal cycling, including flexibility at temperatures as low as -54°C, ensuring resistance to cracking during high-altitude operations. This transition is driving rapid innovation in alternative corrosion inhibition mechanisms, including rare-earth inhibitors and advanced polymer chemistries. As regulatory and environmental pressures intensify, chromate-free topcoats are becoming the new standard for aerospace applications, redefining performance expectations across the industry.

Market Trend: EU REACH 2026 PFAS Restrictions Reshape Functional Topcoat Formulations and Surface Engineering

The European Union’s regulatory framework under REACH is imposing stringent restrictions on the use of per- and polyfluoroalkyl substances in topcoat formulations, significantly impacting applications that rely on oleophobic and weather-resistant properties. The 2026 updates establish strict concentration thresholds, limiting individual PFAS compounds to 25 parts per billion and total PFAS content to 50 parts per million. These limits effectively eliminate traditional fluoropolymer-based additives and coatings, including those derived from C6 and C8 chemistries. As a result, manufacturers are accelerating the development of alternative surface technologies that can replicate low surface energy characteristics without environmental persistence. Silicone-polyurethane hybrid systems are emerging as a leading solution, capable of achieving surface free energy values below 22 mN/m, thereby maintaining easy-clean and anti-fouling performance in applications such as public transport, architectural metal, and industrial equipment. This regulatory shift is also influencing global supply chains, as manufacturers align product portfolios with PFAS-free requirements to maintain access to European markets. The transition toward non-fluorinated topcoats is therefore becoming a key driver of innovation and differentiation in the coatings industry.

Market Opportunity: Self-Healing Clear Topcoats Introduce Autonomous Surface Repair in Automotive Applications

Self-healing topcoat technologies are emerging as a transformative innovation in the automotive sector, moving beyond traditional scratch resistance toward autonomous surface repair capabilities. These coatings utilize dynamic covalent bonding mechanisms, including reversible Diels-Alder reactions, to repair micro-scale damage when exposed to thermal stimuli such as sunlight or engine heat. In 2026, advanced self-healing clearcoats are demonstrating gloss retention levels of approximately 95% after a decade of simulated environmental exposure, significantly outperforming conventional polyurethane systems. The ability to repair scratches up to 20 microns in depth within minutes at elevated temperatures, or within hours under ambient solar conditions, provides a substantial advantage in maintaining vehicle aesthetics and reducing maintenance costs. Additionally, the incorporation of reversible cross-linking networks enhances fracture toughness by up to 40%, improving resistance to mechanical damage from road debris and environmental stress. As automotive manufacturers increasingly prioritize durability, lifecycle cost reduction, and premium surface finishes, self-healing topcoats are positioned as a high-value innovation within the coatings market.

Market Opportunity: High-Solids Polyurethane Topcoats Enhance Durability and Energy Output in Offshore Wind Applications

The expansion of offshore wind energy is creating strong demand for high-performance topcoats capable of protecting turbine blades under extreme environmental conditions. Leading edge protection coatings based on high-solids polyurethane systems are emerging as a critical solution for addressing erosion caused by high-velocity rain impact and prolonged UV exposure. Modern formulations with solids content ranging from 65% to 80% enable high-build applications of up to 500 microns in a single layer while maintaining VOC levels below 250 g/L. This combination of thickness and compliance is essential for delivering long-term protection in harsh offshore environments. Performance testing indicates that these coatings can withstand over 120 minutes of high-speed rain erosion at impact velocities of 140 m/s, translating to a projected service life exceeding 15 years in demanding conditions such as the North Sea. By extending maintenance intervals and reducing downtime, these coatings contribute to improved operational efficiency and increased annual energy production. In large-scale offshore installations, this can result in a 2% to 3% increase in energy output over the turbine’s lifecycle, representing significant economic value for operators.

Topcoat Market Share and Segmentation Insights

Metal Substrates Dominate with 47.4% Share Due to High-Volume Industrial and Automotive Applications

The metal substrate segment leads the global topcoat market with a 47.4% market share in 2025, driven by its extensive use across automotive OEM, industrial equipment, building cladding, and appliance manufacturing sectors. In the protective coatings and finishing systems market, topcoats applied on metal surfaces serve as the final barrier against UV radiation, moisture, chemicals, and abrasion, ensuring long-term durability and corrosion resistance. This makes them a critical component in multi-layer coating systems, particularly in automotive refinishing, coil coating, and heavy machinery applications. Additionally, topcoats play a vital role in aesthetic enhancement, delivering final color, gloss, texture, and metallic finishes that define product appearance and brand differentiation. The dominance of metal substrates is further supported by high production volumes and stringent performance requirements, reinforcing its leading position in the global architectural and industrial topcoat coatings market.

Direct Sales Channel Leads with 51.9% Share Through OEM Partnerships and Bulk Procurement

The direct sales segment dominates the topcoat market by sales channel with a 51.9% share in 2025, reflecting strong demand from large-scale manufacturers in automotive, aerospace, and appliance industries. Within the industrial coatings and OEM coatings market, direct procurement enables companies to maintain strict control over color matching, batch consistency, and proprietary coating formulations, which are essential for brand integrity and product quality. Major OEMs prefer direct relationships with coating suppliers to ensure customized topcoat solutions tailored to specific substrates and performance requirements. Additionally, the segment benefits from high-volume consumption patterns, where manufacturers secure multi-million liter annual supply contracts, gaining advantages such as cost efficiency, priority supply, and long-term pricing stability. This procurement model reduces dependency on intermediaries and enhances supply chain reliability, reinforcing the dominance of direct sales in the global topcoat coatings distribution landscape.

Competitive Landscape Analysis of the Topcoat Market

AkzoNobel Strengthens Low-VOC Topcoat Leadership Through Industrial Excellence

AkzoNobel N.V. is reinforcing its position in the topcoat market with a projected full-year 2026 adjusted EBITDA of €1.47 billion, supported by its aggressive industrial excellence program. The company’s adjusted EBITDA margin expanded to 14.5% in Q1 2026 from 13.7% in 2025, driven by stronger gross margins in Performance Coatings. AkzoNobel is also moving toward the final stages of a proposed merger with Axalta, which could create the world’s largest topcoat manufacturer. Its partnership with IPG Photonics enabled laser-curing powder topcoats, reducing energy intensity by 30%. With strong low-VOC waterborne topcoats under Sikkens and Interplan, the company is expanding aggressively in Asia-Pacific.

PPG Accelerates AI-Designed Clearcoats and Sustainable Topcoat Innovation

PPG Industries, Inc. is advancing the global topcoat market through innovation in automotive refinish topcoats, aerospace coatings, and sustainably advantaged products. In 2026, PPG launched DELTRON® NXT Premium Glamour Speed Clearcoat, an AI-designed topcoat that cuts refinish cycle times by 15%. The company is also investing USD 380 million in a North Carolina aerospace coatings facility to produce next-generation topcoats with advanced IR-reflecting properties. PPG reported USD 15.9 billion in 2025 net sales, supported by 2% organic growth in Protective and Marine and Automotive OEM topcoats. With sustainably advantaged products representing 43% of 2025 sales, PPG aims to reach 50% by 2027.

Sherwin-Williams Expands Premium Architectural and Refinish Topcoat Reach

The Sherwin-Williams Company remains a dominant force in the topcoat market, reporting a 6.8% rise in Q1 2026 consolidated net sales to USD 5.67 billion. Its Performance Coatings Group grew 6.5%, led by double-digit gains in automotive refinish topcoats. The 2025 acquisition of BASF’s Decorative Paints business in Europe and South America significantly expanded its shelf space for specialized architectural topcoats. Its Emerald® and Duration® series continue to lead the premium residential segment, using self-cleaning photocatalytic technology to decompose organic dirt. With more than 4,800 company-operated stores, Sherwin-Williams offers rapid custom color matching and just-in-time delivery for industrial topcoat applications.

Axalta Advances EV Clearcoat Technology and Emerging Market Refinish Growth

Axalta Coating Systems is strengthening its topcoat market position with record adjusted EBITDA of USD 1,128 million in 2025 and a record 22.0% margin. Entering 2026 under its “A Plan,” the company is focused on top-line momentum in Mobility Coatings. Its 2025 Global Automotive Color Popularity Report showed white, black, and gray dominating at 29%, 23%, and 22%, while blue rose 10% in North America, signaling demand for chromatic individuality. Axalta’s clearcoat expertise is especially relevant for EVs, with lower-bake topcoats designed for heat-sensitive battery components. Through Cromax and Spies Hecker, it is expanding refinish demand capture across Southeast Asia.

Nippon Paint Leads Energy-Efficient Wet-on-Wet Topcoat Systems

Nippon Paint Holdings is expanding in the topcoat market after reporting an 8.3% revenue increase to ¥1,774 billion for FY2025, supported by recovery in automotive coatings across Japan and China. In 2026, the company is shifting toward high value-added topcoats with anti-viral and anti-bacterial properties for public infrastructure. Nippon Paint is also consolidating DuluxGroup operations across the Pacific and Europe, using price pass-through strategies to offset raw material volatility and gain share. Its major competitive advantage lies in wet-on-wet 3C1B coating processes, allowing primer, basecoat, and topcoat application without intermediate baking. This helps OEMs reduce energy costs by up to 20%, strengthening its sustainability-driven topcoat leadership.

United States Leading Aerospace Topcoat Innovation and Defense Coating Advancements

The United States continues to dominate the topcoat market, driven by rapid advancements in aerospace manufacturing, defense modernization, and regulatory-driven sustainability transitions. The commercialization of solar-reflective aerospace topcoats has emerged as a key innovation, enabling aircraft to reduce cabin temperatures and improve energy efficiency during ground operations. This aligns with broader industry efforts to enhance operational sustainability and reduce fuel consumption.

Significant investments, including Boeing’s integration of robotic topcoat application systems, are improving coating efficiency and reducing material waste across commercial aircraft production lines. Regulatory pressures following EPA updates are accelerating the shift toward chrome-free and PFAS-free topcoat formulations, particularly through increased adoption of waterborne polyurethane systems. Product innovation is also evident in the development of self-healing topcoats, which automatically repair surface damage when exposed to heat or UV radiation.

Defense applications remain a critical growth driver, with the deployment of multi-spectral camouflage topcoats in next-generation military aircraft programs. Additionally, large-scale infrastructure projects led by the Department of Defense are boosting demand for chemical-resistant topcoats in military vehicle retrofitting. These developments reinforce the U.S.’s leadership in high-performance aerospace and defense coatings.

China’s Expansion in Functional Topcoats for Smart Cities and Industrial Applications

China is rapidly expanding its footprint in the global topcoat market, transitioning from volume-based production to high-performance functional coatings for infrastructure, automotive, and electronics sectors. Government initiatives under the New Material Industry Development Plan (2025–2026) are incentivizing the use of thermotropic topcoats in buildings to improve energy efficiency and reduce solar heat gain.

Industrial expansion is evident with major investments in water-based topcoat production facilities, supporting the growing demand for low-VOC coatings in automotive manufacturing clusters. Technological advancements include the integration of graphene-enhanced topcoats, which provide superior corrosion resistance for critical infrastructure such as power grid substations.

China is also scaling the production of anti-graffiti and easy-clean topcoats for high-speed rail networks, significantly reducing maintenance costs. The country has achieved notable progress in UV-curable industrial coatings, strengthening domestic supply capabilities in consumer electronics manufacturing. Additionally, the use of temperature-sensitive topcoats in EV battery systems is enhancing safety by providing visual indicators of thermal anomalies, reinforcing China’s leadership in smart coating technologies.

Germany Driving Sustainable Topcoat Technologies and Circular Economy Integration

Germany is leading innovation in the sustainable topcoat market, with a strong emphasis on circular economy practices and high-performance industrial coatings. Regulatory frameworks under the EU’s Ecodesign standards are driving the adoption of digital product passports, ensuring traceability and environmental compliance across the coating lifecycle.

Technological advancements include the development of water-vapor-resistant topcoats designed for hydrogen-powered turbines, addressing the unique challenges of high-moisture combustion environments. Product innovation is further enhanced by the introduction of smart indicator topcoats, which change color to signal substrate corrosion, enabling predictive maintenance strategies.

Infrastructure projects such as the Munich Green Rail initiative are accelerating the adoption of recyclable polyurethane topcoats, contributing to sustainable transportation systems. Investments by major chemical companies are expanding the production of bio-based polyurethane dispersions, particularly for automotive interiors. Germany also dominates in specialized applications such as erosion-resistant coatings for wind turbine blades, ensuring durability under extreme environmental conditions.

India’s Rapid Growth in Industrial and Infrastructure Topcoat Applications

India is emerging as a high-growth market in the topcoat industry, driven by urbanization, infrastructure development, and government-led manufacturing initiatives. Large-scale investments by leading companies are expanding production capacity for epoxy and polyurethane topcoats, catering to rising demand across industrial and residential sectors.

Infrastructure modernization projects, including railway upgrades under the Amrit Bharat initiative, are driving the adoption of fluoropolymer topcoats known for their long-term durability and resistance to harsh environmental conditions. Government policies under the PLI Scheme 2.0 are encouraging domestic production of aerospace-grade coatings, strengthening India’s manufacturing ecosystem.

Technological advancements include the development of antimicrobial topcoats for healthcare facilities, improving hygiene standards in public infrastructure. Product innovation is focused on hydrophobic and monsoon-resistant coatings, addressing challenges posed by high humidity and rainfall. Additionally, the growing demand for matte-finish automotive coatings in the premium vehicle segment reflects shifting consumer preferences, further boosting market growth.

Japan’s Leadership in Nano-Functional Topcoats and Precision Coating Technologies

Japan is a global leader in nano-engineered topcoat technologies, focusing on precision applications in electronics, healthcare, and high-end architectural coatings. Innovations such as ultra-thin hydrophobic topcoats for wearable devices are enhancing product performance by maintaining clarity and sensor sensitivity.

Product advancements include photocatalytic self-cleaning coatings, which contribute to environmental sustainability by breaking down pollutants on building surfaces. Japan is also investing in clean-room coating facilities to meet the demand for anti-static coatings in semiconductor manufacturing.

Technological progress in electron-beam curing systems is significantly reducing energy consumption in coating processes, supporting sustainability goals. Regulatory updates under Japanese Industrial Standards are enforcing strict performance benchmarks, particularly for heat-reflective coatings that combat urban heat island effects. Japan also dominates in specialized applications such as anti-fogging topcoats for medical devices, reinforcing its leadership in high-precision coating technologies.

Saudi Arabia’s Growth in Heat-Resistant and Climate-Adaptive Topcoats

Saudi Arabia is emerging as a key market in the topcoat sector, driven by large-scale infrastructure projects and extreme climate conditions. The deployment of polysiloxane-based topcoats in mega-projects like NEOM highlights the demand for coatings capable of withstanding high temperatures and harsh desert environments.

Government initiatives under Vision 2030 are promoting the adoption of high solar reflectance index (SRI) coatings, aimed at reducing energy consumption and mitigating urban heat effects. Product innovation is focused on sand-abrasion resistant coatings, protecting critical infrastructure such as solar panels and industrial equipment.

Industrial expansion by major coating manufacturers is strengthening local supply chains, particularly for fluorocarbon topcoats used in residential and commercial construction. Regulatory standards requiring long-term durability are further driving the adoption of high-performance coatings. Additionally, the use of temperature-indicating topcoats in industrial pipelines is enhancing safety by providing real-time visual alerts, positioning Saudi Arabia as a key growth region for climate-resilient coating technologies.

Topcoat Market Report Scope

Topcoat Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$4.6 Billion

|

|

Market Size (2032)

|

$6.7 Billion

|

|

Market Growth Rate

|

5.6%

|

|

Segments

|

By Resin Type (Polyurethane, Acrylic, Epoxy, Polyester, Alkyd, Fluoropolymers, Vinyl and Chlorinated Rubber), By Technology (Solvent-Borne, Water-Borne, Powder Coatings, Radiation-Cured), By Substrate (Metal, Plastics and Composites, Wood and Engineered Wood, Concrete and Masonry, Glass), By Functionality (Clearcoats, Basecoats, High-Gloss Finish, Matte, Specialty Finishes), By Application Type (OEM, Refinish, Maintenance and Repair), By End-User Industry (Automotive and Transportation, Building and Construction, Industrial Manufacturing, Consumer Goods, Energy and Infrastructure), By Sales Channel (Direct Sales, Industrial Distributors, Specialty Trade Retail)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

PPG Industries, Inc., The Sherwin-Williams Company, Akzo Nobel N.V., Axalta Coating Systems Ltd., BASF SE, Nippon Paint Holdings Co., Ltd., Kansai Paint Co., Ltd., Jotun Group, Hempel A/S, RPM International Inc., Mankiewicz Gebr. and Co., Asian Paints Limited, KCC Corporation, Beckers Group, Cromology SAS

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Topcoat Market Segmentation

By Resin Type

- Polyurethane

- Acrylic

- Epoxy

- Polyester

- Alkyd

- Fluoropolymers

- Vinyl and Chlorinated Rubber

By Technology

- Solvent-Borne

- Water-Borne

- Powder Coatings

- Radiation-Cured

By Substrate

- Metal

- Plastics and Composites

- Wood and Engineered Wood

- Concrete and Masonry

- Glass

By Functionality

- Clearcoats

- Basecoats

- High-Gloss Finish

- Matte

- Specialty Finishes

By Application Type

- OEM

- Refinish

- Maintenance and Repair

By End-User Industry

- Automotive and Transportation

- Building and Construction

- Industrial Manufacturing

- Consumer Goods

- Energy and Infrastructure

By Sales Channel

- Direct Sales

- Industrial Distributors

- Specialty Trade Retail

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Topcoat Industry

- PPG Industries, Inc.

- The Sherwin-Williams Company

- Akzo Nobel N.V.

- Axalta Coating Systems Ltd.

- BASF SE

- Nippon Paint Holdings Co., Ltd.

- Kansai Paint Co., Ltd.

- Jotun Group

- Hempel A/S

- RPM International Inc.

- Mankiewicz Gebr. & Co.

- Asian Paints Limited

- KCC Corporation

- Beckers Group

- Cromology SAS

*- List not Exhaustive