Tris Nonylphenyl Phosphite Market Overview 2025–2034: $676.9 Million to $1,143.6 Million at 6% CAGR Reshaped by SVHC Regulation, Food-Contact Substitutions, and Circular Polymer Stabilization

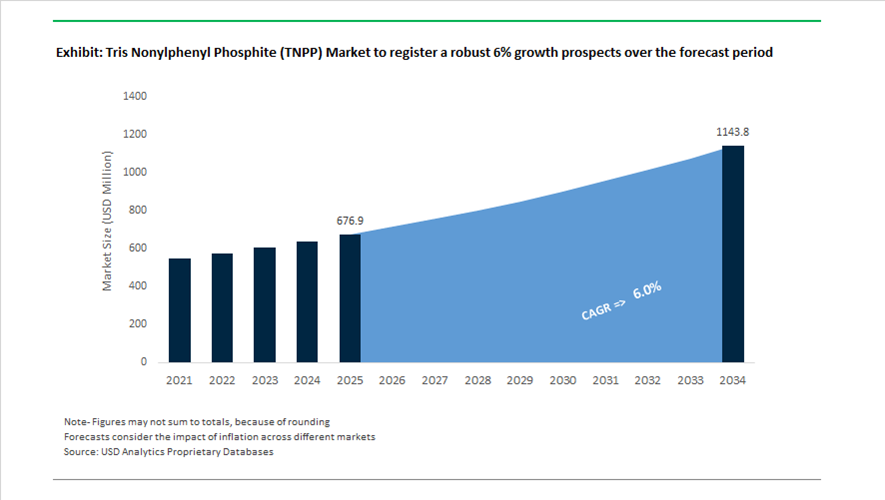

The global Tris Nonylphenyl Phosphite (TNPP) market is valued at $676.9 million in 2025 and is projected to reach $1,143.6 million by 2034, expanding at a CAGR of 6%. TNPP is widely used as a secondary antioxidant and phosphite stabilizer in polyolefins, PVC, elastomers, engineering plastics, adhesives, and food-contact packaging. Market dynamics have shifted sharply due to regulatory scrutiny under EU REACH, rising demand for nonylphenol-free alternatives, and increasing requirements for stabilizers that preserve polymer integrity in recycled materials. The value chain is transitioning from conventional TNPP formulations toward next-generation phosphite antioxidants with low nonylphenol residue, food-contact approval, and circular-economy compatibility.

Regulatory inflection occurred between 2024 and 2025. In August 2024, French authorities formally proposed TNPP for identification as a Substance of Very High Concern (SVHC) under REACH, triggering a public consultation that concluded in October 2024. On January 21, 2025, the European Chemicals Agency added tris(4-nonylphenyl, branched and linear) phosphite to the REACH Candidate List due to endocrine-disrupting properties linked to its degradation into 4-nonylphenol. As of July 2025, EU suppliers of articles containing TNPP above 0.1% concentration are required to provide safety disclosures to downstream recipients and consumers. This mandatory disclosure framework accelerated substitution efforts in food packaging, consumer goods, and branded polyolefin applications. Manufacturers serving European converters are increasingly reformulating additive packages to meet compliance thresholds while preserving melt-flow stability and oxidation resistance.

Substitution technologies gained commercial traction during 2025 and 2026. In September 2025, Dover Chemical launched DoverCycle™, a platform designed for recycled polyolefins using advanced phosphite stabilizers that maintain polymer molecular weight across multiple processing cycles. In October 2025 at the K exhibition, SI Group showcased WESTON™ 705, a nonylphenol-free liquid phosphite antioxidant positioned as a regulatory-compliant alternative to TNPP, with food-contact approvals spanning more than 50 jurisdictions. In February 2026, the European Commission authorized Doverphos® LGP-12 for EU food-contact polyolefin applications following a positive EFSA safety opinion published in April 2024. This authorization establishes LGP-12 as a leading replacement for TNPP in European food packaging and high-purity polymer systems. Portfolio realignment accompanied these product launches. In June 2025, Dover Chemical reported progress toward low-nonylphenol residue formulations in its sustainability report, earning EcoVadis Bronze recognition. In October 2025, SI Group completed a $1.7 billion debt reduction initiative to free capital for R&D investment in nonylphenol-free and PFAS-free additive technologies. In November 2025, SONGWON announced a greenfield One Pack Systems facility in Saudi Arabia to supply customized phosphite blends for Middle Eastern petrochemical converters.

Regulatory Compression, Performance Retention, and Reformulation Pathways in the Tris Nonylphenyl Phosphite (TNPP) Market

Regulatory Substitution Pressure in Food-Contact and Consumer Polyolefins

The TNPP market in 2025 is being decisively shaped by regulatory compression rather than demand-side innovation. Across food-contact packaging, toys, and consumer polyolefins, TNPP is no longer viewed as a “manageable risk” additive but as a regulatory liability due to its degradation into nonylphenol. The reinforcement of TNPP’s classification as a Substance of Very High Concern under EU REACH has materially altered stabilizer selection economics. Once the nonylphenol content exceeds the 0.1% threshold, resin producers face authorization obligations, customer disclosure requirements, and downstream brand rejection, effectively removing TNPP from sensitive applications regardless of its technical performance.

This regulatory pressure is global rather than regional. Japan’s finalized Positive List System for Food-Contact Materials, effective June 2025, has introduced zero-tolerance ambiguity for additives with unclear migration profiles. When combined with China’s 10 ppb migration cap for nonylphenol and increasingly strict EFSA alignment, polyolefin producers supplying multinational packaging brands are being forced to adopt stabilizers that clear all major jurisdictions simultaneously. As a result, TNPP substitution is occurring not through incremental reformulation but through portfolio-level redesign, with liquid tertiary phosphites that are explicitly nonylphenol-free becoming the default choice for PE and PP film grades targeting food, medical, and childcare markets.

Residual but Strategic Use in Engineering Plastics and Synthetic Rubber

Despite regulatory retreat in consumer-facing applications, TNPP retains technical relevance in industrial polymers where performance demands outweigh regulatory exposure. In engineering plastics, synthetic rubber, and high-stress extrusion environments, TNPP’s liquid form continues to offer processing advantages that solid phosphite antioxidants struggle to replicate. Its ability to disperse uniformly at low loadings allows processors to fine-tune oxidative stability in continuous compounding lines without modifying screw design, residence time, or feed strategy.

Industrial processing data presented across 2024 and 2025 consistently shows that TNPP can suppress gel formation by an order of magnitude under high-temperature shear conditions, particularly in Cr-type HDPE, HIPS, and SBR. This matters commercially because gel defects directly translate into scrap rates, surface defects, and customer rejections in automotive and appliance-grade polymers. In synthetic rubber, TNPP’s stabilizing action during polymerization and finishing improves Mooney viscosity consistency, supporting downstream calendering and molding operations.

Another critical but often overlooked factor is TNPP’s role in maintaining Melt Flow Rate stability during polyolefin recycling. Automotive OEMs accelerating circular-economy adoption are increasingly relying on stabilized regrind to meet recycled content mandates. TNPP’s effectiveness in limiting molecular weight degradation across multiple heat histories has made it a preferred stabilizer in closed-loop automotive interior and under-hood applications where food-contact exposure is irrelevant but long-term thermal stability is non-negotiable.

Opportunity: Scaling Nonylphenol-Free Drop-In Liquid Phosphites

The most commercially attractive growth pathway linked to TNPP is not its continued use, but its functional replacement. Resin producers are explicitly seeking drop-in liquid phosphites that replicate TNPP’s handling, solubility, and processing behavior while eliminating regulatory risk. This requirement favors liquid, high-phosphorus-content stabilizers that can be dosed precisely in existing equipment without reformulating the entire antioxidant package.

Nonylphenol-free liquid phosphites are gaining traction because they allow formulators to reduce total stabilizer loading while improving melt-flow retention and color stability. Higher phosphorus efficiency translates into lower phenolic antioxidant demand, which in turn improves long-term thermal aging and reduces yellowing. From a cost perspective, these alternatives are increasingly competitive as suppliers scale capacity and standardize global approvals, allowing polymer producers to simplify SKUs across regions rather than maintaining separate compliant and non-compliant grades.

Capacity expansion between 2024 and 2025 has been directly aligned with this transition, particularly in Asia-Pacific where automotive plastics, appliance housings, and consumer electronics casings are growing rapidly. The strategic implication is that TNPP is effectively acting as a reference benchmark rather than a growth product, with innovation and capital flowing toward stabilizers engineered to outperform it under tightening regulatory frameworks.

Opportunity: Advanced Synergistic Stabilizer Blends for Recycled and Bio-Based Polymers

A second, more specialized opportunity lies in stabilizer systems designed for recycled and bio-based polymers, where oxidative instability is structurally higher than in virgin resins. Mechanical recycling introduces chain scission, hydroperoxide formation, and contaminant residues that overwhelm traditional antioxidant packages. This has created demand for advanced secondary antioxidants that deliver hydrolytic stability, high-temperature endurance, and compatibility with diverse feedstocks.

In this context, TNPP-free diphosphites and synergistic blends are being positioned as re-stabilization technologies rather than simple antioxidants. These systems are designed to protect polymers during their second and third life cycles, preserving mechanical properties and aesthetics while enabling compliance with recycled content mandates. For circular economy applications, stabilizer performance directly determines whether recycled polymers can access high-value markets such as automotive interiors, durable consumer goods, and construction products.

A niche but economically attractive extension of this trend exists in closed-loop industrial adhesives, coatings, and gasket materials. In these systems, stabilizers are encapsulated or immobilized within polymer matrices, minimizing migration and environmental exposure. This allows formulators to leverage phosphite chemistry for heat resistance and processing stability while aligning with increasingly strict environmental discharge and sustainability reporting requirements.

Tris Nonylphenyl Phosphite Market Share and Segmentation Insights

Product Type Market Share: High-Purity TNPP Leads with Regulatory-Compliant Polymer Stabilization

High-purity TNPP accounts for 48.60% of the tris nonylphenyl phosphite market in 2025, driven by increasing regulatory scrutiny on nonylphenol content and migration in polymer applications. This segment benefits from reduced free nonylphenol levels while maintaining high antioxidant and heat stabilizer performance in polyolefins, PVC, and engineering plastics. Conventional TNPP and solid phosphite stabilizers continue to serve cost-sensitive and niche processing applications. A key market driver is regulatory compliance, where high-purity TNPP is increasingly specified for food contact materials, automotive plastics, and consumer goods, with manufacturers investing in advanced purification technologies to meet global environmental and safety standards.

End-Use Industry Market Share: Packaging Segment Dominates with Polyolefin Processing and Food Contact Compliance

Packaging holds a 42.80% share of the tris nonylphenyl phosphite market in 2025, supported by extensive use in stabilizing polyolefins during film extrusion, blow molding, and injection molding processes. TNPP plays a critical role as an antioxidant stabilizer, preventing thermal degradation and maintaining polymer performance throughout the product lifecycle. Automotive, consumer goods, petrochemicals, and construction industries contribute additional demand across engineering plastic applications. A key trend is the growing emphasis on food packaging compliance, where converters and brand owners prioritize low nonylphenol TNPP grades with certified food contact approval, ensuring regulatory alignment while maintaining processing efficiency and product durability.

Tris Nonylphenyl Phosphite Market Competitive Landscape

The Tris Nonylphenyl Phosphite market in 2026 is defined by HiPure low-residual formulations, nonylphenol-free alternatives, and formula-ready liquid phosphite blends that enhance hydrolytic stability, low-color performance, and regulatory compliance across polyolefins, food-contact packaging, and medical-grade plastics.

SI Group Strengthens WESTON™ TNPP Leadership with Recycled Plastics Stabilization Focus

SI Group is reinforcing its leadership in the Tris Nonylphenyl Phosphite market through its WESTON™ TNPP portfolio, recognized for high-flash-point safety (207°C) and superior low-color polymer processing. The company implemented global price adjustments in March 2026 to offset geopolitical logistics volatility while sustaining investment in sustainable additive technologies. WESTON™ TNPP is optimized for synergistic performance with hindered phenolic antioxidants, reducing total additive loading in polyethylene and elastomer stabilization. SI Group is increasingly targeting recycled plastics processing, using TNPP-based stabilizers to mitigate melt-flow degradation in post-consumer polyolefins. Its “Zero-Distance” technical service model ensures localized compliance with FDA food-contact standards across North America. This combination of performance optimization and regulatory alignment strengthens its position in high-volume and specialty polymer markets.

SONGWON Expands Dual-Track TNPP and Nonylphenol-Free Stabilizer Strategy

SONGWON Industrial Co., Ltd. is advancing its position in the Tris Nonylphenyl Phosphite market through scale-driven production and diversified antioxidant portfolios. The company announced a 12–20% global price increase effective April 2026, addressing rising raw material and freight costs while protecting margins in polymer stabilizers. Its dual-track strategy combines cost-effective TNPP solutions with high-performance alternatives such as SONGNOX® 9228 and SONGSORB® 1164, enabling coverage across both commodity and premium non-toxic packaging markets. SONGWON leverages its Global Technology Center to deliver traceability, regulatory documentation, and application-specific formulation support. Post-2025 restructuring has improved capital efficiency and reduced debt exposure, supporting long-term growth investments. Its strong presence in Asia and export-driven markets positions it as a key supplier for global polyolefin converters.

Dover Chemical Leads HiPure TNPP Segment with Ultra-Low Nonylphenol Content

Dover Chemical Corporation is a specialist leader in the Tris Nonylphenyl Phosphite market, particularly in HiPure TNPP grades designed for stringent regulatory environments. Its Doverphos® HiPure 4 and 4HR grades maintain residual nonylphenol content below 0.1%, enabling compliance with evolving European restrictions and food-contact regulations. The company implemented a $0.25/lb price increase to address energy and logistics cost pressures, maintaining operational stability. Doverphos® 4 is widely used in PET and polyurethane applications due to its high molecular weight and strong extraction resistance. Its hydrolysis-resistant “HR” grades prevent defects such as black specks in emulsion polymerization, ensuring superior product quality in synthetic rubber and SBR. Dover’s expertise in liquid phosphite chemistry positions it as a preferred supplier for high-purity, compliance-driven applications.

Adeka Corporation Advances Low-Migration TNPP and High-Transparency Polymer Stabilizers

Adeka Corporation is strengthening its role in the Tris Nonylphenyl Phosphite market through environment-friendly polymer additives and high-purity stabilizer systems. Its TNPP offerings within the ADK STAB portfolio are engineered for excellent initial color hold and transparency, supporting high-visibility consumer plastics and advanced polypropylene applications. Under its 2026 strategic framework, Adeka is focusing on next-generation clarifiers and stabilizers aligned with lightweighting trends in automotive and battery materials. Its R&D advancements, including lithium-sulfur battery prototypes, are driving innovation in low-migration and environmentally compliant additives. Adeka maintains a strong presence in Asia-Pacific, leveraging technical engagement platforms to strengthen relationships with regional polymer producers. This integration of R&D and market proximity enhances its competitiveness in high-performance stabilizer segments.

Galata Chemicals Enhances TNPP Customization for PVC and Elastomer Applications

Galata Chemicals is positioning itself in the Tris Nonylphenyl Phosphite market through customized phosphite stabilizer solutions tailored to specific polymer processing requirements. Its Markphos® TNPP product line delivers improved thermal stability and processability across PVC, polyurethane, polyethylene, and ABS applications. The company offers flexible manufacturing capabilities, supporting both small- and large-scale production with precise control over viscosity and phosphorus content. Complementary products such as EHDP and PDDP enable formulators to fine-tune stabilization performance by adjusting phosphorus levels. Galata’s global manufacturing footprint supports long-term partnerships with PVC and elastomer producers, particularly in North America and Europe. Its phosphite co-stabilizers play a critical role in enhancing weatherability for outdoor plastics, including agricultural films and geomembranes.

China Tris Nonylphenyl Phosphite Market Driven by Cost Leadership and Polymer Scale

China remains the lowest-cost and most structurally integrated producer in the Tris Nonylphenyl Phosphite market, supported by deliberate upstream localization under the 14th Five-Year Plan for the Chemical Industry. By integrating domestic phosphorus trichloride supply chains, Chinese manufacturers reduced the average TNPP synthesis cost to approximately USD 1,650–1,800 per metric ton during the 2025 fiscal year. This cost position continues to underpin China’s competitiveness in supplying liquid phosphite antioxidants to large-volume polyolefin processors, particularly those serving packaging, film, and flexible plastics applications.

On the production side, SI Group has continued scaling output at its Nanjing facility, focusing on Weston 705 and other liquid phosphite alternatives designed to meet food-contact and export-oriented packaging requirements. These expansions directly align with China’s ongoing ethylene and polyethylene capacity additions in Zhejiang and Guangdong scheduled through 2026, where phosphite stabilizers are essential to prevent discoloration and thermal degradation in LLDPE and HDPE films. Additionally, the Ministry of Industry and Information Technology has begun tracking high-purity TNPP precursors under its Specialty Electronic Chemicals initiative, reflecting the chemical’s indirect relevance to semiconductor-grade polymer materials and advanced electronics packaging.

United States Tris Nonylphenyl Phosphite Market Shaped by Regulation and Grade Substitution

In the United States, the TNPP market is increasingly shaped by regulatory scrutiny rather than volume expansion. The U.S. Environmental Protection Agency’s inclusion of nonylphenol and its ethoxylates in the 2025–2026 TSCA Section 6 risk evaluation has accelerated the transition away from traditional TNPP toward nonylphenol-free phosphite systems, particularly in potable water pipes and consumer-facing plastic applications. As a result, Tier-1 resin producers are redesigning stabilization packages to future-proof formulations against potential restrictions.

Supply security remains a strategic priority. SI Group completed a USD 50 million investment program across three North American sites, consolidating its liquid and solid phosphite portfolio to support the shale-driven polyolefin boom. Innovation has also focused on food-contact applications. Weston 705 received expanded FDA clearances in 2025, enabling U.S. film producers to market high-clarity, nonylphenol-free packaging to premium retail and food brands. However, rising compliance and feedstock monitoring costs led to a general price increase of USD 0.05–0.08 per pound on phosphorus-based antioxidants effective Q1 2026, signaling tighter margins across the domestic stabilizer value chain.

South Korea Tris Nonylphenyl Phosphite Market Anchored in Sustainability Leadership

South Korea’s TNPP market is defined less by volume and more by sustainability-driven differentiation. Songwon Industrial has positioned phosphite antioxidants within its Net-Zero 2050 roadmap, emphasizing synergistic systems such as XP2121 that enhance performance in recycled polypropylene. These formulations address a critical pain point for circular plastics by maintaining melt flow stability and color retention across multiple recycling loops.

Operational decarbonization is reinforcing this positioning. Songwon’s transition to zero-emission external steam at its Ulsan plant is projected to reduce annual emissions by nearly 25,900 tCO₂-equivalent by 2027, directly lowering the carbon footprint of its phosphite portfolio. The company’s sustained EcoVadis Platinum rating through 2025 further strengthens its appeal to multinational polymer converters seeking traceable, low-impact stabilizer sourcing for global consumer brands.

Germany Tris Nonylphenyl Phosphite Market Constrained by Regulation but Innovating for Circularity

Germany represents the most regulation-intensive TNPP market globally. The European Chemicals Agency’s expansion of the SVHC Candidate List in late 2024 to cover broader tris(nonylphenyl) phosphite groups has materially constrained the use of conventional TNPP in the EU. This regulatory backdrop has accelerated substitution toward alternative phosphites and multifunctional stabilizer systems that eliminate endocrine-disrupting concerns while preserving polymer performance.

At the same time, German chemical producers are aligning with the 2025 Antwerp Declaration, which seeks to protect Europe’s polymer additive industry from energy price volatility while supporting the transition to greener chemistries. Within the EU Circular Economy Action Plan, German formulators are prioritizing stabilizer-rich additive packages that enable repeated mechanical recycling without polymer chain scission. This approach positions Germany as a technology leader in recycling-ready stabilization, even as legacy TNPP usage steadily declines.

India Tris Nonylphenyl Phosphite Market Emerging Through Import Substitution and Infrastructure Growth

India’s TNPP market is transitioning from import reliance toward domestic capability building, driven by petrochemical expansion and policy support. At Indian Petrochem 2025, local producers such as Krishna Antioxidants showcased high-purity TNPP grades targeting the rapidly expanding PVC pipe and irrigation segment, where thermal stability and long service life are critical.

Government Production Linked Incentive programs for specialty chemicals are encouraging Indian firms to localize isobutylene and nonylphenol intermediates, stabilizing input costs for TNPP-based antioxidants. Sustainability compliance is also advancing. Songwon Industrial’s Panoli plant achieved substantial reductions in freshwater withdrawal through Zero Liquid Discharge implementation by 2025, setting a benchmark for phosphorus-chemical manufacturing in India. Collectively, these developments position India as a medium-term alternative supply base for phosphite stabilizers serving South Asia and the Middle East.

Comparative Snapshot: Tris Nonylphenyl Phosphite Market by Country

Tris Nonylphenyl Phosphite (TNPP) Market County Level Snapshot

|

Country

|

Core Market Driver

|

Strategic Direction

|

TNPP Outlook

|

|

China

|

Cost leadership, polymer scale

|

Upstream integration

|

Volume dominance

|

|

United States

|

TSCA regulation, food contact

|

TNPP substitution

|

Grade transition

|

|

South Korea

|

Net-zero plastics

|

Recycled polymer focus

|

Premium positioning

|

|

Germany

|

REACH SVHC pressure

|

Circular stabilizers

|

Structural decline

|

|

India

|

Import substitution

|

Domestic intermediates

|

Gradual expansion

|

Tris Nonylphenyl Phosphite (TNPP) Market Report Scope

Tris Nonylphenyl Phosphite (TNPP) Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$676.9 Million

|

|

Market Size (2034)

|

$1143.6 Million

|

|

Market Growth Rate

|

6%

|

|

Segments

|

By Product Type (Conventional TNPP, High-Purity TNPP, Solid Phosphite Stabilizers), By Grade (Industrial Grade, Food Grade), By Application (Antioxidants and Heat Stabilizers, Color Stabilizers, UV Stabilizer Synergists, Viscosity Control Agents), By End-Use Industry (Packaging, Petrochemicals, Automotive, Consumer Goods, Construction)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

SI Group Inc., Songwon Industrial Co. Ltd., Adeka Corporation, Dover Chemical Corporation, BASF SE, Addivant, Galata Chemicals, Valtris Specialty Chemicals, Krishna Antioxidants Private Limited, Everspring Chemical Co. Ltd., Rianlon Corporation, Nanjing Leopard Chemical Co. Ltd., Sandhya Group, Sterling Auxiliaries Private Limited, Huatian Tianteng Chemical

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Tris Nonylphenyl Phosphite Market Segmentation

By Product Type

- Conventional TNPP

- High-Purity TNPP

- Solid Phosphite Stabilizers

By Grade

- Industrial Grade

- Food Grade

By Application

- Antioxidants and Heat Stabilizers

- Color Stabilizers

- UV Stabilizer Synergists

- Viscosity Control Agents

By End-Use Industry

- Packaging

- Petrochemicals

- Automotive

- Consumer Goods

- Construction

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Tris Nonylphenyl Phosphite Market

- SI Group Inc.

- Songwon Industrial Co. Ltd.

- Adeka Corporation

- Dover Chemical Corporation

- BASF SE

- Addivant

- Galata Chemicals

- Valtris Specialty Chemicals

- Krishna Antioxidants Private Limited

- Everspring Chemical Co. Ltd.

- Rianlon Corporation

- Nanjing Leopard Chemical Co. Ltd.

- Sandhya Group

- Sterling Auxiliaries Private Limited

- Huatian Tianteng Chemical

*- List not Exhaustive