Energy-Curable Technologies, Sustainability, and High-Speed Manufacturing Driving Strong Growth

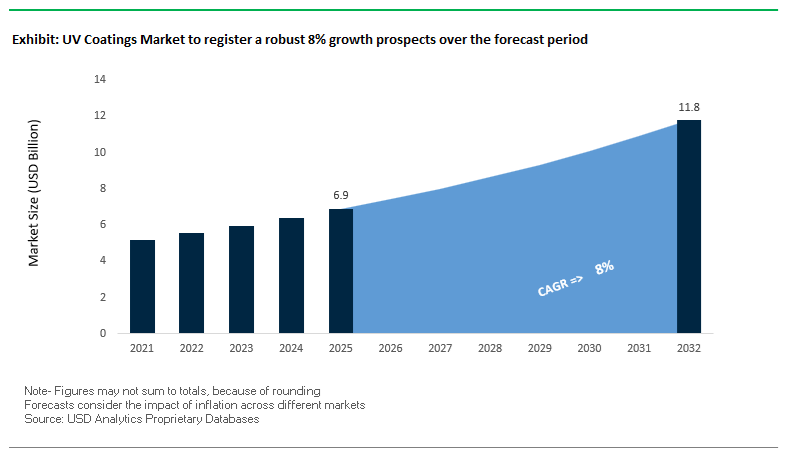

The global UV Coatings Market is witnessing robust expansion, supported by increasing adoption of energy-curable technologies across automotive, packaging, electronics, wood, and industrial applications. The market was valued at $6.9 billion in 2025 and is projected to reach $11.8 billion by 2032, growing at a CAGR of 8% during 2025–2032. This above-average growth rate reflects the strong shift toward UV, LED, and electron beam (EB) curing systems, which offer instant curing, reduced energy consumption, and minimal emissions compared to conventional coating technologies.

A key structural driver is the rising demand for high-throughput manufacturing processes, where UV coatings enable rapid curing speeds, improved productivity, and lower operational costs. These coatings are widely used in automotive refinishing, wood coatings, electronics, and packaging, where performance attributes such as scratch resistance, chemical durability, and high-gloss finishes are critical. Additionally, the increasing use of UV coatings in digital printing and flexible packaging is expanding the market’s application scope.

Sustainability is a central growth catalyst. UV coatings inherently offer low-VOC or solvent-free formulations, aligning with global environmental regulations. The emergence of bio-based UV resins, recyclable coating systems, and mass-balanced production approaches is further strengthening their position as a sustainable alternative to traditional coatings. At the same time, advancements in UV-stable pigments and additives are enhancing long-term durability, particularly in outdoor and automotive applications.

Another important trend is the integration of advanced optical and functional effects, including metallic finishes, interference pigments, and high-depth visual coatings. These innovations are driving demand in premium automotive and consumer applications, where coatings serve both protective and aesthetic roles.

Market Analysis: Bio-Based UV Resins, Fast-Cure Automotive Systems, and Circular Coating Technologies Reshaping Competitive Landscape

The UV coatings market is being transformed by strategic consolidation, sustainability-driven innovation, and advanced curing technologies, reflecting the increasing importance of energy-efficient coating systems. The proposed merger between AkzoNobel and Axalta (2025–2026) represents a major consolidation event, combining their capabilities in UV/LED/EB coating technologies and strengthening R&D across mobility and industrial segments.

Sustainability milestones are driving competitive differentiation. Arkema’s January 2026 achievement of ISCC PLUS certification across over 70% of its coating facilities enables the production of bio-attributed UV resins with at least a 20% reduction in carbon footprint, supporting the transition toward circular and low-carbon coatings.

Automotive innovation remains a key growth engine. Axalta’s “Solar Boost” UV-stable topcoat (January 2026) demonstrates the use of advanced pigment and clearcoat systems designed to maintain gloss and color integrity under intense UV exposure, particularly for electric vehicles. Additionally, Axalta’s R&D 100 Award-winning fast-cure, low-energy system (November 2025) highlights the potential of UV coatings to significantly reduce energy consumption and processing time in collision repair operations.

Material and aesthetic innovation is also advancing. BASF’s “Driving the Proxy” collection (October 2025) utilizes interference pigments and liquid-metal effects, which require specialized UV-curable topcoats to achieve high visual depth and durability. AkzoNobel’s particle technology (September 2024) further enhances the application of metallic UV-resistant coatings on complex geometries.

Circular economy solutions are gaining traction in packaging. Sun Chemical’s SunCure EcoPlast (July 2025) introduces a wash-off UV coating system that allows plastic substrates to be recycled efficiently, while Siegwerk’s SICURA Nutriflex series (2024 expansion) ensures compatibility with flexible packaging recycling streams.

Expansion in industrial and wood coatings is also notable. AkzoNobel’s February 2025 launch of a bio-based UV wood coating combines fast curing with reduced fossil-fuel dependency, while its Interpon UV-resistant powder coatings (April 2025) demonstrate long-term gloss retention in outdoor lighting applications.

Market Trend: REACH Annex XIV “Photoinitiator Clean-Up” Forces Shift to Low-Migration, High-Molecular Systems

The UV coatings industry is undergoing a decisive reformulation phase driven by European regulatory pressure on photoinitiators. Following the reclassification of TPO as a Category 1B reprotoxic substance, regulators have expanded scrutiny to additional photoinitiators such as 369 and 379, which are now progressing toward inclusion in the REACH Annex XIV Authorisation List. This regulatory trajectory is compelling manufacturers to transition toward high-molecular-weight and polymeric photoinitiators that exhibit minimal migration into food-contact substrates. Under 2026 compliance requirements, UV coatings used in packaging must meet stringent specific migration limits—typically below 10 ppb for non-evaluated substances and below 50 ppb for approved polymeric systems. This is driving widespread adoption of alternatives such as BAPO-based systems and polymeric thioxanthone derivatives, which provide improved molecular stability and reduced extractability. However, these substitutions introduce formulation challenges related to cure kinetics and photoreactivity, requiring optimization of lamp intensity and spectral output. As regulatory scrutiny intensifies, low-migration chemistry is becoming a foundational requirement in UV coatings for packaging and sensitive applications.

Market Trend: China GB/T 41655-2025 Establishes Ultra-Low VOC and PAA Limits for UV Coatings

China’s enforcement of GB/T 41655-2025 is significantly reshaping the UV coatings landscape by imposing strict limits on volatile organic compounds and migration-related contaminants. The regulation mandates that compliant UV coatings contain less than 2% VOC by weight, effectively requiring the use of 100% solids systems based on reactive diluents. This eliminates the viability of hybrid solvent-containing formulations and accelerates the transition toward fully reactive chemistries. Additionally, the standard introduces a stringent cumulative limit for primary aromatic amines at 0.01 mg/kg of food simulant, aligning Chinese packaging safety standards with European Union requirements. This is forcing a comprehensive reassessment of pigment, resin, and additive selection, particularly in major manufacturing hubs such as the Yangtze River Delta. The combined focus on emission reduction and migration control is driving innovation in raw material purification and formulation design, ensuring compliance without compromising performance. As China continues to elevate its environmental and safety standards, these regulations are setting new global benchmarks for UV coating technologies.

Market Opportunity: LED-UV Coatings Enable Ultra-High-Speed, Energy-Efficient Web Processing

The transition from mercury-vapor lamps to LED-UV curing systems is creating a major opportunity for UV coatings in high-speed web applications. Modern LED systems operating at wavelengths such as 365 nm and 395 nm deliver substantial energy savings, reducing power consumption by 50% to 75% compared to traditional curing technologies. This shift is also aligned with global environmental agreements targeting mercury phase-out, further accelerating adoption. From a performance standpoint, 2026-generation LED-UV coatings are engineered to achieve full cure at energy densities as low as 20 mJ/cm², enabling web speeds exceeding 350 meters per minute without compromising coating integrity. The absence of infrared heat in LED curing systems allows for processing of heat-sensitive substrates such as ultra-thin PET and BOPP films, expanding application possibilities in flexible packaging. Additionally, the elimination of ozone generation and reduced cooling requirements contribute to lower operational complexity and improved workplace safety. As printing and coating lines push toward higher throughput and sustainability targets, LED-UV coatings are becoming a critical enabler of next-generation manufacturing efficiency.

Market Opportunity: UV Coatings in EV Battery Manufacturing Deliver High-Speed, Solvent-Free Production

The rapid expansion of electric vehicle production is opening a high-growth application segment for UV-curable coatings, particularly in battery manufacturing processes. UV coatings are increasingly replacing traditional thermal-cure systems in applications such as dielectric insulation for busbars and protective coatings for battery housings. These coatings provide high electrical performance, achieving dielectric breakdown voltages exceeding 5,000 volts at relatively thin film thicknesses, enabling compact and lightweight designs. In battery separator manufacturing, UV-curable ceramic-filled coatings allow for significantly higher production speeds—up to five times faster than conventional solvent-based processes—while reducing the required factory footprint by eliminating large drying ovens. Furthermore, the adoption of UV-curable binders in dry electrode manufacturing is enabling the elimination of N-Methylpyrrolidone, a solvent with significant environmental and health concerns. This transition is reducing the carbon footprint of battery production by approximately 40% and simplifying solvent recovery systems. As the EV industry scales globally, UV coatings are emerging as a key technology for improving manufacturing efficiency, sustainability, and performance in next-generation energy storage systems.

UV Coatings Market Share and Segmentation Insights

Oligomers Lead with 44.5% Share as Core Component in High-Performance UV Coatings

The oligomers segment dominates the UV coatings market with a 44.5% market share in 2025, reflecting its critical role in defining the mechanical and chemical performance of UV-cured coatings. In the UV-curable coatings and radiation-cured materials market, oligomers such as urethane acrylates, epoxy acrylates, and polyester acrylates are essential for controlling key properties including hardness, flexibility, scratch resistance, adhesion, and weatherability. These characteristics are crucial across applications in wood coatings, metal finishes, plastic coatings, and paper & packaging industries. Oligomers also represent the largest volume component—typically 40–60% of total UV coating formulations, making them the backbone of product performance and formulation design. Their versatility allows manufacturers to tailor coatings for high-speed curing, durability, and environmental resistance, reinforcing their leadership position. As demand for high-performance, low-VOC, and energy-efficient coatings grows, oligomers remain central to innovation in the global UV coatings market.

Direct Sales Channel Dominates with 56.2% Share Through OEM Partnerships and Customization

The direct sales segment leads the UV coatings market by sales channel with a 56.2% market share in 2025, driven by strong integration between coating manufacturers and large-scale industrial users. Within the industrial UV coatings and advanced materials market, companies such as flooring manufacturers, automotive component producers, and electronics coaters rely on direct procurement to seamlessly integrate coatings into high-speed production lines and automated curing systems. This approach ensures consistent quality, optimized cure speeds, and compatibility with specific substrates, which is essential for maintaining production efficiency. Additionally, direct collaboration enables the development of proprietary coating formulations tailored to unique performance requirements, including adhesion, gloss levels, and durability under specific operating conditions. The ability to provide technical support, customization, and long-term supply agreements makes direct sales the preferred channel, reinforcing its dominance in the global UV coatings market supply chain.

Competitive Landscape Analysis of the UV Coatings Market

AkzoNobel Expands Water-Borne UV Coatings Leadership Through Axalta Merger

AkzoNobel N.V. holds 21% of the global UV coatings market, maintaining leadership despite a 5% decline in 2025 group sales and a leaner 31,500-employee operating model entering 2026. Its proposed merger with Axalta Coating Systems is set to create a major coatings powerhouse with 173 manufacturing sites and 91 R&D centers. AkzoNobel is also opening a Dubai Aerospace Coatings Hub in Q2 2026 to supply locally blended Aerobase and Aerodur UV-curable aerospace topcoats for Middle Eastern aviation MRO demand. Its core strength lies in water-borne UV coatings, which account for 54.2% of preferred curing methods in eco-sensitive European markets.

PPG Advances Low-Carbon UV Coatings for EV Batteries and Electronics

PPG Industries, Inc. controls 19% of the UV coatings market, with strong positioning in automotive refinish and electronics, which together represent 35% of total UV demand. In April 2026, PPG launched a high-speed, low-carbon radiation-curable testing line at its Marly, France R&D center, simulating IR, LED-UV, excimer, and electron beam curing to reduce customer trial-and-error by 40%. With 43% of 2025 sales from sustainably advantaged products, PPG is pushing 100% solids UV/EB-curable formulations to eliminate VOC emissions. Its UV-curable dielectric coatings support EV battery thermal management through superior insulation and rapid-cycle production.

Sherwin-Williams Strengthens UV Wood and Furniture Coatings Distribution

The Sherwin-Williams Company is expanding in the UV coatings market, supported by Q1 2026 consolidated net sales of USD 5.67 billion, up 6.8%. Its Performance Coatings Group benefited from double-digit growth in UV-curable wood and furniture finishes, a segment expected to dominate UV resin volume in 2026 due to demand for scratch-resistant, fast-curing coatings. The company is leveraging its 2025 acquisition of BASF’s Decorative Paints business to cross-sell UV-curable industrial primers and topcoats across EMEA and Latin America. With more than 4,800 stores, Sherwin-Williams provides just-in-time UV-curable chemistry to contractors and regional industrial plants.

Arkema Leads UV Resin Integration With Bio-Attributed Acrylates

Arkema S.A., through Sartomer and Coating Solutions, is strengthening its role in the UV coatings market by targeting full Specialty Materials status by late 2026. The company is launching ultra-low VOC UV-curable resins to meet tightening EU and U.S. chemical regulations. By early 2026, 70% of Arkema’s coating facilities were ISCC+ certified, enabling mass production of bio-attributed UV acrylates for graphic arts and 3D printing. Arkema is also advancing UV-curable materials for data centers and electronics protection, improving cooling efficiency and structural durability. Its vertical integration through Sartomer gives it control over epoxy acrylates, which hold 36.5% of the UV resin market.

BASF Develops High-Margin UV Coatings for Automotive and e-Mobility Applications

BASF SE is focusing its UV coatings market strategy on automotive color innovation, additive manufacturing, and e-mobility applications. Its “Driving the Proxy” Automotive Color Trends collection uses multi-color UV-curable pigments and liquid-metal surface effects incorporating renewable raw materials. BASF has scaled Tesseract Blue in EMEA and Phygital Magnetar in Asia-Pacific, using advanced two-coat UV technology to merge physical and digital visual depth. Following portfolio high-grading, BASF reported €1.5 billion EBITDA in its coatings division. In 2026, the company is expanding plastic additives capacity to ensure UV-curable exterior automotive coatings retain gloss and structural integrity for more than 15 years.

China’s Rapid Scale-Up in UV Coatings for 5G Infrastructure and EV Applications

China continues to dominate the UV coatings market, leveraging its massive industrial base and aggressive push toward green manufacturing and carbon neutrality goals. A major infrastructure milestone is the establishment of the world’s largest UV-LED optical fiber coating hub, supporting large-scale 5G deployment with high-performance protective coatings. This has significantly increased demand for UV-curable coatings in telecommunications and smart infrastructure.

Technological advancements include the development of graphene-oxide reinforced UV coatings, enhancing EMI shielding capabilities for EV battery enclosures and high-performance electronics. Government initiatives are accelerating the transition to LED-curable coating systems, reducing reliance on mercury-based technologies and aligning with low-emission targets. Strategic investments in photoinitiator production are strengthening China’s vertical supply chain, while regulatory updates mandating low-migration UV coatings for food packaging are driving adoption in the packaging sector. Additionally, nanotechnology-integrated UV stabilizers are gaining traction in automotive applications, particularly for polycarbonate sunroofs exposed to intense UV radiation, positioning China as a global leader in advanced UV coating solutions.

United States Driving Aerospace-Grade UV Coatings and PFAS-Free Innovation

The United States remains a key innovator in the UV curable coatings industry, with a strong focus on aerospace precision, sustainability, and regulatory compliance. The enforcement of PFAS restrictions and Clean Air Act updates is accelerating the transition toward fluorine-free and environmentally compliant UV coatings, particularly in electronics and medical device manufacturing.

Technological advancements such as hybrid laser-UV curing systems are transforming aerospace MRO processes, enabling rapid and efficient surface sealing for composite structures. Investments by major players are expanding production of UV coatings for intelligent labeling, especially in pharmaceutical cold-chain logistics. Product innovations include self-healing UV polyurethane topcoats, capable of repairing micro-scratches autonomously, enhancing durability in high-performance applications.

Defense applications are also driving growth, with the deployment of multi-spectral camouflage UV coatings in next-generation military aircraft. Expansion of manufacturing facilities for UV-based strippers and primers is further strengthening the market. These developments position the U.S. as a leader in high-performance and sustainable UV coating technologies.

Germany Leading Circular Economy UV Coatings and Hydrogen-Ready Solutions

Germany is at the forefront of the sustainable UV coatings market, focusing on circular economy integration and advanced industrial applications. Regulatory compliance with EU Ecodesign standards is driving the adoption of digital product passports, ensuring traceability and recyclability of UV coating materials.

Innovations include the development of water-vapor-resistant UV coatings for hydrogen-powered turbines, addressing challenges associated with high-moisture combustion environments. Technological advancements such as digital twin-enabled coating processes are improving precision and efficiency in industrial applications.

Infrastructure projects like the Munich Green Rail initiative are promoting the use of fully recyclable UV coatings, supporting long-term sustainability goals. Investments in bio-based polyurethane dispersions are expanding applications in automotive interiors and industrial coatings. Germany also leads in erosion-resistant UV coatings for wind turbine blades, ensuring durability under extreme environmental conditions, reinforcing its leadership in eco-friendly and high-performance UV coatings.

India’s Growth Fueled by Telecom Expansion and Rail Modernization Projects

India is emerging as a high-growth market in the UV coatings sector, supported by rapid infrastructure development and government initiatives promoting domestic manufacturing. The BharatNet project is driving demand for UV coatings in fiber optic networks, particularly those designed to withstand tropical climate conditions.

Government incentives under the PLI Scheme 2.0 are encouraging local production of UV coating equipment, reducing import dependency and strengthening the domestic supply chain. Industrial expansion, including large-scale capacity additions in UV-stable architectural coatings, is supporting the growing construction sector.

Technological advancements include the development of quick-cure UV-LED coatings for railway applications, enabling faster maintenance cycles for high-speed trains like the Vande Bharat fleet. Product innovation is also evident in antimicrobial UV coatings for healthcare infrastructure, improving hygiene standards in public facilities. Regulatory updates mandating performance benchmarks are ensuring quality and durability, positioning India as a key market for cost-effective and scalable UV coating solutions.

Japan’s Nano-Precision UV Coatings for Electronics and Medical Applications

Japan continues to lead the UV coatings market through advancements in nano-scale surface engineering and high-precision applications. Innovations such as ultra-thin hydrophobic UV coatings are enhancing performance in wearable electronics, ensuring optical clarity while maintaining sensor sensitivity.

Technological advancements include the adoption of electron-beam curing systems, significantly reducing energy consumption in coating processes. Investments in advanced photoresist technologies are supporting the development of next-generation semiconductor manufacturing.

Product innovations such as photocatalytic self-cleaning UV coatings are contributing to environmental sustainability by reducing pollutant accumulation on building surfaces. Regulatory updates under Japanese standards are ensuring durability and performance under extreme conditions. Japan also dominates in specialized applications such as anti-fogging UV coatings for medical devices, reinforcing its leadership in precision-driven UV coating technologies.

South Korea Advancing UV Coatings for 6G Electronics and Smart Wearables

South Korea is emerging as a major innovator in the UV coatings market, leveraging its leadership in semiconductors and advanced electronics. Technological breakthroughs include the development of conductive UV coatings integrated with carbon nanotubes, enabling advanced functionalities in 6G communication devices and wearable sensors.

Product innovation is focused on EMI shielding UV coatings, protecting sensitive electronics in robotics and next-generation communication systems. Significant investments are supporting the development of radar-absorbent coatings for defense applications, particularly in advanced fighter aircraft technologies.

Industrial expansion includes specialized clean-room facilities dedicated to producing anti-static UV coatings for semiconductor fabrication environments. The integration of UV coatings into automotive interiors is enhancing user experience through smart heating and interactive features. Regulatory updates promoting low-solvent technologies are accelerating the adoption of 100% solids UV-LED coatings, positioning South Korea as a global leader in next-generation smart coating technologies.

UV Coatings Market Report Scope

UV Coatings Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$6.9 Billion

|

|

Market Size (2032)

|

$11.8 Billion

|

|

Market Growth Rate

|

8%

|

|

Segments

|

By Resin Type (Epoxy Acrylates, Urethane Acrylates, Polyester Acrylates, Polyether Acrylates, Silicone Acrylates, Acrylic Acrylates), By Technology (Water-borne UV Coatings, Solvent-borne UV Coatings, 100% Solids, UV-LED Curable Coatings, Powder UV Coatings), By Composition (Oligomers, Monomers, Photoinitiators, Additives, Pigments and Colorants), By Substrate (Wood, Plastic, Paper and Paperboard, Metal, Glass and Ceramics, Composites), By Application (Overprint Varnishes, Display Coatings, Conformal Coatings, Wood Finishes, Plastic Component Coatings, Automotive Refinishes and Parts), By End-User Industry (Industrial Coatings, Electronics, Graphic Arts and Printing, Packaging, Automotive and Transportation, Building and Construction, Medical Devices), By Sales Channel (Direct Sales, Specialized Chemical Distributors, Aftermarket and Retail Channels)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

AkzoNobel N.V., PPG Industries, Inc., BASF SE, The Sherwin-Williams Company, Axalta Coating Systems, Nippon Paint Holdings Co., Ltd., Kansai Paint Co., Ltd., Sokan New Materials, Hempel A/S, DIC Corporation, RPM International Inc., Fujifilm Holdings Corporation, Dymax Corporation, Siegwerk Druckfarben AG and Co. KGaA, Beckers Group

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

UV Coatings Market Segmentation

By Resin Type

- Epoxy Acrylates

- Urethane Acrylates

- Polyester Acrylates

- Polyether Acrylates

- Silicone Acrylates

- Acrylic Acrylates

By Technology

- Water-borne UV Coatings

- Solvent-borne UV Coatings

- 100% Solids

- UV-LED Curable Coatings

- Powder UV Coatings

By Composition

- Oligomers

- Monomers

- Photoinitiators

- Additives

- Pigments and Colorants

By Substrate

- Wood

- Plastic

- Paper and Paperboard

- Metal

- Glass and Ceramics

- Composites

By Application

- Overprint Varnishes

- Display Coatings

- Conformal Coatings

- Wood Finishes

- Plastic Component Coatings

- Automotive Refinishes and Parts

By End-User Industry

- Industrial Coatings

- Electronics

- Graphic Arts and Printing

- Packaging

- Automotive and Transportation

- Building and Construction

- Medical Devices

By Sales Channel

- Direct Sales

- Specialized Chemical Distributors

- Aftermarket and Retail Channels

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in UV Coatings Industry

- AkzoNobel N.V.

- PPG Industries, Inc.

- BASF SE

- The Sherwin-Williams Company

- Axalta Coating Systems

- Nippon Paint Holdings Co., Ltd.

- Kansai Paint Co., Ltd.

- Sokan New Materials

- Hempel A/S

- DIC Corporation

- RPM International Inc.

- Fujifilm Holdings Corporation

- Dymax Corporation

- Siegwerk Druckfarben AG & Co. KGaA

- Beckers Group

*- List not Exhaustive