Hybrid Vacuum–UV Systems, Premium Finishes, and Electronics Demand Driving Growth

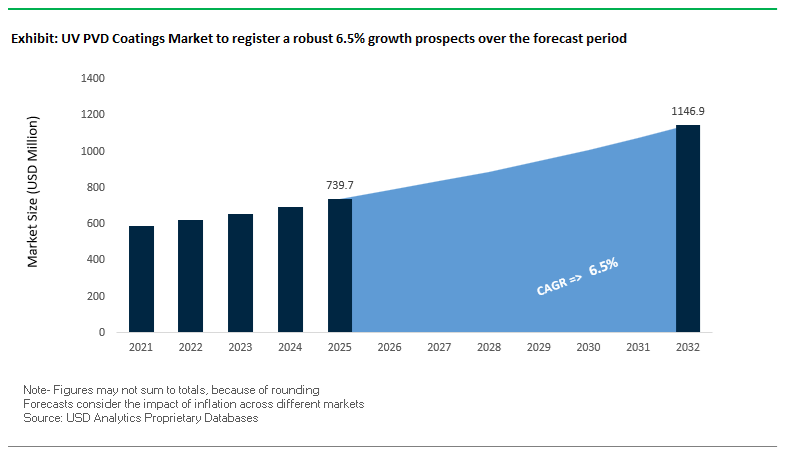

The global UV PVD Coatings Market is expanding steadily, supported by rising adoption of hybrid coating systems that combine physical vapor deposition (PVD) with UV-curable base and topcoats. The market was valued at $739.7 million in 2025 and is projected to reach $1,149.5 million by 2032, growing at a CAGR of 6.5% during 2025–2032. Growth is driven by demand for high-performance decorative and functional coatings across automotive, consumer electronics, luxury goods, and industrial components.

A key structural driver is the increasing use of UV-PVD coating stacks, where UV-curable primers and topcoats are applied before and after the vacuum metallization process. These systems deliver enhanced adhesion, scratch resistance, corrosion protection, and high-gloss metallic finishes, making them essential for applications such as automotive interior trims, smartphone housings, wearables, and premium packaging. The ability to achieve metal-like aesthetics with reduced material usage and lower environmental impact compared to traditional electroplating is further accelerating adoption.

Another major trend is the growing demand for multi-functional coatings, where UV-PVD systems integrate properties such as anti-fingerprint, electromagnetic interference (EMI) shielding, UV resistance, and thermal stability. This is particularly relevant in electric vehicles (EVs) and advanced electronics, where coatings must meet both aesthetic and functional requirements.

Sustainability is also shaping the market. UV-PVD coatings offer low-VOC processing, reduced energy consumption, and compatibility with bio-based resins, aligning with global environmental targets. Additionally, advancements in UV curing technologies and vacuum deposition processes are improving efficiency, enabling faster production cycles and lower operational costs.

Market Analysis: Laser-Based Curing, EV Interior Applications, and Bio-Based PVD Systems Reshaping Competitive Landscape

The UV PVD coatings market is being transformed by technological innovation, strategic consolidation, and expansion into high-growth applications, reflecting the increasing complexity of modern surface engineering. The March 2026 merger between AkzoNobel and Axalta represents a major consolidation, combining expertise in energy-curable coatings and PVD-compatible systems, strengthening R&D capabilities for automotive and electronics applications.

Process innovation is a key differentiator. AkzoNobel’s February 2026 partnership with IPG Photonics introduces laser-based curing technology, which enhances the UV curing stage of PVD processes by reducing energy consumption and enabling faster production cycles compared to conventional UV lamp systems.

Automotive applications, particularly in EVs, are driving innovation. Axalta’s “Solar Boost” UV-PVD compatible topcoat (January 2026) demonstrates advanced pigment and flake technologies designed to maintain color depth and UV stability in high-gloss automotive interiors. Similarly, Mankiewicz’s October 2025 expansion into EV interior coatings focuses on anti-fingerprint and scratch-resistant UV-PVD systems for premium cabin components.

Equipment and system-level advancements are expanding production capabilities. The July 2025 formation of Kolzer International strengthens the global supply of PVD 2.0 systems, which integrate UV-curable coatings into high-speed industrial finishing processes. This reflects the increasing demand for scalable and automated coating solutions.

Functional innovation is extending into electronics and advanced applications. Sokan New Materials’ September 2025 launch of multi-functional UV-PVD coatings introduces systems that combine decorative metallic finishes with EMI shielding, targeting 5G devices and wearable electronics.

Sustainability-driven developments are also gaining traction. Musashi Paint Group’s November 2024 expansion into bio-based UV-PVD resins highlights the industry’s shift toward plant-derived materials, supporting carbon-neutrality goals for global electronics manufacturers.

Luxury and high-end applications are driving precision-focused innovation. Berlac Group’s October 2024 acquisition of a specialized PVD coating unit enhances its capabilities in high-end finishes for watchmaking and cosmetic packaging, where surface quality and tactile experience are critical.

Infrastructure investments are supporting long-term innovation. Oerlikon Balzers’ June 2024 opening of an advanced coating technology center in Westbury, NY provides a hub for R&D in hybrid UV-PVD processes, particularly for aerospace and energy applications.

Additionally, cross-technology integration is expanding capabilities. Sherwin-Williams’ Heat-Flex® technology discussions (August 2025) highlight the use of UV-cured primers for substrate stabilization, demonstrating the convergence of thermal barrier and UV-PVD coating technologies.

Market Trend: REACH 2026 Chromium VI Sunset Accelerates Shift from Electroplating to UV/PVD Systems

The UV PVD coatings industry is benefiting from a decisive regulatory shift in Europe as the European Commission tightens restrictions on hexavalent chromium. Following updated REACH authorization guidance in late 2025, 2026 represents the final viable window for many decorative electroplating operations relying on Cr(VI). Regulatory authorities have signaled a near-zero likelihood of granting new authorizations for non-essential decorative uses, effectively forcing a transition toward safer alternatives such as trivalent chromium systems and, increasingly, PVD-based metallization combined with UV topcoats. This transition is not only compliance-driven but also performance-driven. Advanced UV/PVD coating stacks are now demonstrating superior resistance in aggressive chemical environments, including hydrofluoric acid exposure, where traditional chrome plating often fails. The shift is also reducing environmental and occupational health risks associated with electroplating processes, aligning with broader sustainability and safety objectives. As OEMs and Tier-1 suppliers move away from legacy plating technologies, UV PVD systems are emerging as the preferred solution for high-performance decorative and functional coatings.

Market Trend: EPA PFAS Outreach Signals Transition to PFAS-Free Surface Technologies in PVD Coatings

The regulatory landscape in the United States is evolving with the EPA’s PFAS Outreach initiative, which is expanding its scope from environmental monitoring to industrial source control. By 2026, anticipated rulemaking under TSCA and the Safe Drinking Water Act is expected to impose stricter reporting and eventual phase-out requirements for intentionally added PFAS in coating processes. This is particularly relevant for PVD coating systems, where PFAS-based surfactants have historically been used to achieve low surface energy and enhanced flow characteristics in pretreatment and topcoat layers. In response, leading service providers are transitioning to PFAS-free alternatives, notably silicone-polyurethane hybrid systems. These formulations are capable of achieving surface free energy levels below 20 mN/m, delivering comparable oleophobic and easy-clean properties without the environmental persistence associated with fluorinated compounds. This transition is reshaping formulation strategies and supply chains, as manufacturers prioritize compliance with emerging regulations while maintaining performance characteristics required for high-end applications. The move toward PFAS-free coatings is becoming a defining trend in the UV PVD coatings industry.

Market Opportunity: Anti-Fingerprint UV Topcoats Enable Premium Satin Finishes in Automotive Interiors

The automotive industry’s shift toward low-gloss, tactile interior surfaces is creating a strong demand for advanced UV-curable topcoats in PVD applications. Satin and “stealth” finishes are replacing traditional high-gloss chrome, particularly in integrated cockpit designs where glare reduction and user interaction are critical. UV-curable anti-fingerprint coatings are enabling these design trends by combining optical clarity with functional durability. In 2026, these coatings are achieving exceptional color stability, with Delta E values below 0.5 after extended xenon-arc exposure, ensuring long-term aesthetic consistency. They also demonstrate high chemical resistance, maintaining adhesion performance even after prolonged exposure to aggressive substances such as sunscreen and perspiration under elevated temperatures. From a usability perspective, these coatings deliver high hydrophobic and oleophobic performance, allowing fingerprints to be removed بسهولة with minimal effort, significantly reducing maintenance requirements. As automotive interiors become more digital and user-centric, UV-curable anti-fingerprint coatings are emerging as a key enabler of both functional performance and premium design.

Market Opportunity: High-Durability UV Topcoats Protect PVD Finishes in Consumer Electronics

The consumer electronics sector is presenting a major growth opportunity for UV PVD coatings, particularly in applications requiring durable metallic finishes on lightweight substrates. Devices such as smartphones, laptops, and wearables increasingly rely on PVD coatings to achieve premium “brushed metal” aesthetics, but these thin metallic layers are inherently susceptible to abrasion and wear. UV-curable topcoats are addressing this challenge by providing a protective barrier that significantly enhances surface durability. In 2026, advanced formulations are achieving steel wool abrasion resistance exceeding 2,000 cycles under standardized load conditions, representing substantial improvement over traditional coating systems. These coatings also support ultra-thin application, maintaining total thickness below 15 microns to meet stringent dimensional and signal transparency requirements for modern electronic devices. Additionally, they provide effective corrosion protection, with coated systems demonstrating extended resistance in salt spray testing without pitting or degradation. As consumer expectations for durability and aesthetics continue to rise, UV-curable topcoats are becoming a critical component in the design and performance of next-generation electronic products.

UV PVD Coatings Market Share and Segmentation Insights: UV Top-Coat Dominance and Automotive Sector Driving Chrome Replacement Technologies

By Coating Layer: UV Top-Coat Leads with 38.6% Share Enabling Durability, Scratch Resistance, and Premium Surface Finishes

UV top-coats accounted for 38.6% of the UV PVD coatings market in 2025, acting as a critical protective barrier for ultra-thin sub-100nm PVD metal layers. These coatings deliver essential performance attributes such as scratch resistance, chemical resistance, and oxidation protection, ensuring long-term durability in high-wear applications like consumer electronics and automotive interiors. Beyond protection, UV top-coats enable advanced haptic and optical properties, including anti-fingerprint functionality, soft-touch finishes, and high-gloss chrome aesthetics. The integration of self-healing monomers and matting agents further enhances surface performance, positioning UV top-coats as indispensable in premium decorative coatings and high-performance PVD coating systems.

By End-User Industry: Automotive Sector Leads with 28.4% Share Driven by Chrome Replacement and Lightweighting Innovations

The automotive sector held a 28.4% share of the UV PVD coatings market in 2025, driven by the industry-wide shift away from hexavalent chromium electroplating. Stringent regulations such as the EU End-of-Life Vehicles Directive and China RoHS are accelerating the adoption of environmentally compliant UV PVD coatings for automotive trim components, including grilles, emblems, and interior bezels. These coatings provide a mirror-like chrome finish without hazardous waste generation. Additionally, UV PVD coatings enable direct application on plastic substrates such as ABS and PC/ABS, reducing component weight by 40–60% compared to traditional metal plating. This supports vehicle lightweighting strategies, particularly in electric vehicles, enhancing energy efficiency and driving demand for advanced decorative coating technologies.

UV PVD Coatings Market Competitive Landscape Driven by UV-Curable Integration and High-Performance Thin-Film Metallization

The UV PVD coatings market is rapidly evolving, driven by the convergence of UV-curable coating systems and physical vapor deposition technologies. Key players are focusing on high-speed processing, REACH-compliant coatings, and advanced surface engineering solutions to meet demand across automotive, electronics, aerospace, and energy applications.

PPG Expands UV-Curable Coating Capabilities to Strengthen End-to-End UV PVD Solutions

PPG Industries, Inc. is reinforcing its leadership in the UV PVD coatings market through investments in radiation-curable coating technologies. In April 2026, the company established a dedicated testing line in Marly, France, aimed at accelerating the development of UV primers and topcoats for PVD metallization processes. Its product portfolio emphasizes UV-curable primers that deliver superior surface leveling, critical for achieving high-brilliance metallic finishes on plastic and metal substrates. Strong demand from data centers and industrial electronics contributed to PPG’s positive financial outlook in early 2026. The company’s vertically integrated approach, combining coating chemistry with application services, enables seamless adoption of UV PVD workflows. This capability positions PPG as a key partner for manufacturers transitioning to high-efficiency, low-emission coating systems.

Oerlikon Balzers Advances REACH-Compliant PVD Technologies for EV and Aerospace Applications

Oerlikon Balzers is a technology leader in advanced PVD coatings, offering high-performance platforms such as BALINIT® and BALORA™. In late 2025, the company introduced INSPIRA carbon with S3p technology, enhancing productivity and coating quality for precision automotive and industrial applications. Oerlikon is actively expanding in the electric vehicle sector, securing major contracts with leading manufacturers for Pulsed Plasma Diffusion (PPD), an environmentally friendly alternative to chrome plating. Its 2026 expansion in Mexico strengthens its aerospace capabilities, particularly for high-temperature turbine components. The company’s REACH-compliant oxidation barrier coatings provide sustainable, wear-resistant solutions for demanding environments. This strong focus on innovation and regulatory compliance positions Oerlikon as a dominant force in high-performance surface engineering.

AkzoNobel Accelerates Sustainable UV PVD Coatings with Bio-Based Resins and Clean Energy Transition

AkzoNobel N.V. is driving innovation in UV PVD coatings through sustainable chemistry and energy-efficient curing technologies. The company is expanding its portfolio of UV-curable coatings for wood and plastic substrates, supporting decorative PVD finishes in automotive interiors. Collaborations with automotive OEMs such as NIO highlight its role in developing sensory-driven coatings for next-generation smart vehicles. AkzoNobel also serves the electronics and consumer device sectors, delivering coatings that enable premium metallic aesthetics with reduced environmental impact. Its transition to renewable energy-powered manufacturing sites, particularly in China and Poland, supports corporate Green Growth targets. This integration of sustainability and high-performance coatings strengthens its competitive positioning in environmentally conscious markets.

Hauzer Enables Scalable UV PVD Manufacturing with Turnkey Flexicoat® Systems and Industry 4.0 Integration

IHI Hauzer Techno Coating B.V. specializes in turnkey PVD coating systems that enable seamless integration of UV-curable coating lines with vacuum deposition processes. Its Flexicoat® series offers modular configurations that support high-volume manufacturing with automated quality control aligned to Industry 4.0 standards. The company is expanding into hydrogen fuel cell technology, developing inline PVD systems for bipolar plate production, a key growth segment in 2026. Hauzer’s solutions integrate pre-treatment, coating, and post-processing into a unified workflow, improving operational efficiency and consistency. Its systems are widely used in automotive trim, sanitary hardware, and industrial tooling applications. This strong focus on scalability and automation positions Hauzer as a critical enabler of industrial UV PVD adoption.

Berlac Delivers High-Precision UV Lacquer Systems for Premium PVD Metallic Finishes

Berlac Group is a niche leader in UV-curable lacquer systems designed for high-end PVD applications across automotive, medical, and luxury goods sectors. The company’s coatings are engineered to ensure optimal adhesion between substrates and vacuum-deposited metal layers, delivering superior aesthetic and functional performance. Berlac focuses on complex geometries and high-gloss finishes, offering UV primers that eliminate the need for pre-polishing, reducing processing time and cost. It has expanded into the medical technology sector with antimicrobial PVD-compatible coatings for surgical instruments and diagnostic devices. Its agile R&D capabilities enable customized solutions, including anti-fingerprint and scratch-resistant topcoats. This specialization in premium coatings and customization strengthens Berlac’s position in high-value UV PVD applications.

China Leading “Zero-Chrome” UV PVD Coatings for 3C Electronics and EV Interiors

China has established itself as the global leader in the UV PVD coatings market, driven by its aggressive transition toward zero-chrome surface engineering solutions across consumer electronics and automotive sectors. Government directives aimed at eliminating traditional electroplating are accelerating the adoption of UV basecoat–PVD–UV topcoat systems, particularly in the Pearl River Delta, where large-scale electronics manufacturing is concentrated.

Technological advancements such as multi-target sputtering integrated with UV-LED curing systems are enabling single-cycle metallic finishing for complex electronic housings, significantly improving production efficiency. Major investments in UV PVD resin and equipment manufacturing are supporting the surge in demand for premium smartphone and display coatings, including anti-reflective and anti-fingerprint finishes for OLED panels. Key applications include metallized UV PVD coatings for EV interiors, delivering lightweight, eco-friendly metallic aesthetics. Regulatory standards enforcing low VOC and heavy metal limits are further pushing industries toward vacuum-based coating technologies, reinforcing China’s leadership in high-volume and sustainable UV PVD coating solutions.

United States Advancing Aerospace-Grade UV PVD Coatings and PFAS-Free Technologies

The United States is a major innovator in the UV PVD coatings industry, focusing on aerospace precision, sustainability, and regulatory compliance. The enforcement of PFAS-free mandates is accelerating the adoption of siloxane-modified UV PVD coatings, delivering high-performance oleophobic properties without environmental risks.

Technological advancements include the integration of HiPIMS (High-Power Impulse Magnetron Sputtering) with UV-curable primers, improving adhesion and performance on aerospace-grade composites. Infrastructure developments in turbine modernization programs are boosting the adoption of UV PVD thermal barrier coatings, enhancing fuel efficiency and component durability.

Strategic investments in UV-curable bonding resins are supporting applications in medical devices and advanced manufacturing. Key applications also include UV PVD coatings for satellite systems, designed to withstand extreme radiation and environmental conditions in low Earth orbit. Expansion of compact UV PVD systems is further enabling on-demand coating services across multiple industries, positioning the U.S. as a leader in high-performance and precision UV PVD coating technologies.

Germany Driving Circular Economy Integration and Smart Surface UV PVD Coatings

Germany is at the forefront of sustainable UV PVD coating technologies, emphasizing circular economy practices and advanced industrial applications. Regulatory frameworks such as the EU Ecodesign standards are promoting the adoption of digital product passports, ensuring traceability and recyclability of coating materials.

Innovations include the development of recyclable UV PVD primer systems, enabling full recovery of base polymers in automotive components. Technological advancements such as radar-transparent UV PVD coatings are supporting the growth of smart mobility solutions, particularly in electric vehicles with advanced driver-assistance systems.

Strategic investments in automated coating centers are accelerating the development of premium metallic finishes for automotive interiors. Infrastructure applications include UV PVD coatings for offshore wind turbine sensors, providing long-term corrosion resistance. Germany also leads in integrating conductive UV PVD coatings in medical devices, enhancing functionality while reducing manufacturing complexity, positioning it as a leader in high-value and sustainable UV PVD coating solutions.

Japan’s Nano-Precision UV PVD Coatings for Optics and Semiconductor Applications

Japan remains a global leader in nano-engineered UV PVD coatings, focusing on high-precision applications in electronics, optics, and healthcare. Innovations such as ultra-thin UV PVD coating stacks are enhancing optical clarity and durability in wearable devices, particularly smart glasses and advanced display technologies.

Technological advancements include the implementation of cluster-tool PVD systems, enabling defect-free coating deposition for next-generation semiconductor manufacturing. Industrial expansion in clean-room facilities is supporting the production of anti-static and antimicrobial coatings for medical and diagnostic equipment.

Strategic investments are driving the development of high-performance primers for luxury packaging and electronics. Regulatory updates are ensuring performance standards for architectural coatings, particularly in terms of solar reflectance and durability. Japan also dominates in anti-fogging UV PVD coatings for medical devices, reinforcing its leadership in precision-driven and high-performance coating technologies.

South Korea Advancing UV PVD Coatings for 6G Electronics and Smart Wearables

South Korea is rapidly advancing in the UV PVD coatings market, leveraging its expertise in semiconductors and next-generation electronics. Technological breakthroughs include the commercialization of conductive UV PVD coatings integrated with carbon nanotubes, enabling advanced functionalities in 6G-enabled devices and wearable sensors.

Product innovation is focused on EMI shielding UV PVD coatings, protecting sensitive electronics in robotics and communication systems. Significant investments are supporting the development of radar-absorbent coatings for defense applications, particularly in advanced fighter aircraft technologies.

Key applications include the integration of smart-heating UV PVD coatings in automotive interiors, enhancing user experience in electric vehicles. Regulatory updates promoting low-solvent technologies are accelerating the adoption of 100% solids UV-LED PVD coatings, improving sustainability. Infrastructure developments such as advanced materials clusters are strengthening production capabilities, positioning South Korea as a global leader in next-generation UV PVD coating technologies.

Saudi Arabia Driving UV PVD Coatings for Extreme Climate and Infrastructure Projects

Saudi Arabia is emerging as a key market in the UV PVD coatings sector, driven by large-scale infrastructure projects and extreme climate conditions under Vision 2030. The deployment of UV PVD coatings in mega-projects like NEOM highlights the demand for coatings capable of withstanding high temperatures and harsh desert environments.

Product innovation includes dust-repellent nano-coatings, ensuring optimal performance of solar panels and infrastructure in sand-heavy regions. Government mandates requiring high solar reflectance index coatings are addressing urban heat challenges, improving energy efficiency in new developments.

Industrial expansion is strengthening local production of UV-curable PVD primers, supporting the country’s large construction pipeline. Key applications include high-durability coatings for metro systems and desalination plants, ensuring long-term performance under extreme environmental conditions. Regulatory standards ensuring durability and weather resistance are further driving adoption, positioning Saudi Arabia as a major market for climate-resilient UV PVD coating technologies.

UV PVD Coatings Market Report Scope

UV PVD Coatings Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$739.7 Million

|

|

Market Size (2032)

|

$1149.5 Million

|

|

Market Growth Rate

|

6.5%

|

|

Segments

|

By Coating Layer (UV Base-coat, PVD Layer, UV Top-coat, UV Mid-coat), By PVD Deposition Technology (Magnetron Sputtering, Thermal Evaporation, Cathodic Arc Deposition, Electron Beam PVD), By Substrate Type (Plastics and Polymers, Composites, Glass and Ceramics, Metals), By Finish and Aesthetics (High-Chrome, Brushed and Satin Finishes, Matte and Soft-touch Finishes, Colored), By End-User Industry (Automotive, Consumer Electronics, Cosmetics and Personal Care Packaging, Consumer Goods and Appliances, Building and Hardware, Aerospace and Defense), By Sales Channel (Direct Sales, Contract Coating Service Providers, Specialized System Integrators)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Oerlikon Balzers, Fujikura Kasei Co., Ltd., AkzoNobel N.V., PPG Industries, Inc., The Sherwin-Williams Company, Sartomer, Kolzer SRL, Mankiewicz Gebr. and Co., Berlac Group, Red Spot Paint and Varnish Company, Inc., Sokan New Materials, Verosol, HCVAC, Kenosistec s.r.l., Huicheng Vacuum Technology Co., Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

UV PVD Coatings Market Segmentation

By Coating Layer

- UV Base-coat

- PVD Layer

- UV Top-coat

- UV Mid-coat

By PVD Deposition Technology

- Magnetron Sputtering

- Thermal Evaporation

- Cathodic Arc Deposition

- Electron Beam PVD

By Substrate Type

- Plastics and Polymers

- Composites

- Glass and Ceramics

- Metals

By Finish and Aesthetics

- High-Chrome

- Brushed and Satin Finishes

- Matte and Soft-touch Finishes

- Colored

By End-User Industry

- Automotive

- Consumer Electronics

- Cosmetics and Personal Care Packaging

- Consumer Goods and Appliances

- Building and Hardware

- Aerospace and Defense

By Sales Channel

- Direct Sales

- Contract Coating Service Providers

- Specialized System Integrators

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in UV PVD Coatings Industry

- Oerlikon Balzers

- Fujikura Kasei Co., Ltd.

- AkzoNobel N.V.

- PPG Industries, Inc.

- The Sherwin-Williams Company

- Sartomer

- Kolzer SRL

- Mankiewicz Gebr. & Co.

- Berlac Group

- Red Spot Paint & Varnish Company, Inc.

- Sokan New Materials

- Verosol

- HCVAC

- Kenosistec s.r.l.

- Huicheng Vacuum Technology Co., Ltd.

*- List not Exhaustive