Construction Boom, Product Innovation, and Integrated Solutions Driving Growth

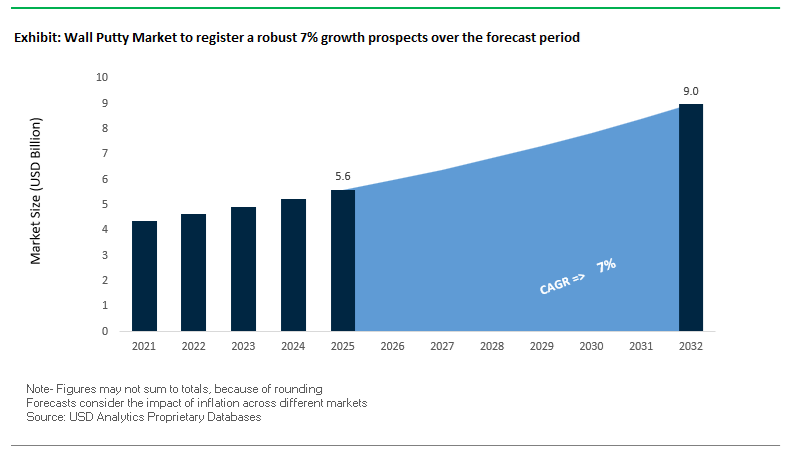

The global Wall Putty Market is expanding steadily, supported by rising demand from residential construction, urban infrastructure development, and renovation activities. The market was valued at $5.6 billion in 2025 and is projected to reach $9 billion by 2032, growing at a CAGR of 7% during 2025–2032. Growth is particularly strong in emerging economies, where rapid urbanization and housing demand are driving consumption of cement-based and acrylic wall putties.

A key structural driver is the increasing emphasis on surface preparation quality in modern construction practices. Wall putty plays a critical role in ensuring smooth finishes, paint adhesion, durability, and crack resistance, making it indispensable in both residential and commercial projects. The shift toward premium paints and decorative coatings is further elevating demand for high-performance putties that provide uniform whiteness and enhanced surface leveling.

Another major trend is the growing adoption of ready-to-use and multifunctional formulations, which reduce application time and labor costs. Contractors are increasingly favoring products that offer faster drying, reduced sanding requirements, and compatibility with multiple substrates, particularly in large-scale projects where efficiency is critical.

Sustainability and performance enhancement are also shaping the market. Manufacturers are focusing on low-VOC formulations, moisture-resistant technologies, and long-lasting finishes, especially for regions with extreme weather conditions such as high humidity or coastal exposure. Additionally, the integration of thermal and energy-efficient properties into wall preparation materials is emerging as a niche but high-potential segment.

Market Analysis: Capacity Expansion in India, 2-in-1 Product Innovation, and Coastal-Grade Formulations Reshaping Competitive Landscape

The wall putty market is undergoing significant transformation, driven by capacity expansion, product innovation, and strategic consolidation, particularly in high-growth regions like India. The February 2026 amalgamation of Kansai Nerolac Paints with Nerofix marks a key consolidation move, strengthening the company’s position in construction chemicals and adhesive-linked putty systems, while improving manufacturing and distribution efficiency.

Capacity expansion is a major growth lever. J.K. Cement’s February 2026 commissioning of a fully automated plant in Gujarat adds 400,000 tons of annual capacity, specifically targeting the western India market. This follows its September 2025 expansion, which increased total white cement and putty capacity to 3.05 MTPA, reinforcing its leadership in the value-added segment.

Product innovation is increasingly focused on efficiency and performance. Asian Paints’ Neo-Finish series (January 2026) introduces self-leveling, ultra-smooth putties designed to reduce sanding time, addressing a key contractor pain point. Similarly, Birla Opus’ One Pro Putty+Primer (August 2025) offers a 2-in-1 formulation, eliminating the need for a separate primer coat and providing extended durability warranties, making it highly suitable for fast-track projects.

Strategic acquisitions are strengthening market positioning. The April 2025 acquisition of Wonder WallCare by Aditya Birla Group provides immediate access to a 600,000 MT production facility in Rajasthan, significantly enhancing its manufacturing footprint and competitiveness in the Indian market.

Regional product specialization is also emerging. Nippon Paint’s “Coastal Guard” putty (November 2025) targets high-humidity and coastal environments, incorporating moisture-barrier technology to prevent efflorescence, a common issue in such regions.

Innovation is extending into functional construction materials. AkzoNobel’s solar-absorbing wall technology (October 2025) integrates specialized base-layer formulations that enhance thermal efficiency, indicating a convergence between wall preparation materials and energy-efficient building systems.

Distribution and branding strategies are also evolving. Walplast’s HomeSure campaign (July 2024) positions wall putty within a broader ecosystem of construction chemicals, while Berger Paints continues to scale production from its Sandila hub, targeting high-demand residential corridors in North India.

Market Trend: BIS IS 15477:2025 Enforcement Accelerating Quality Standardization in India Wall Putty Market

The enforcement of BIS IS 15477:2025 is transforming the India wall putty market by mandating stringent quality benchmarks for polymer-modified cementitious wall putty products. Under the Quality Control Order, manufacturers must now meet a minimum tensile adhesion strength of ≥ 0.8 MPa after 28 days of curing, significantly higher than the earlier 0.5 MPa benchmark. This shift is driving demand for high-performance wall putty formulations capable of supporting advanced decorative coatings without delamination, strengthening the positioning of premium-grade construction materials.

The regulation also enforces a strict water absorption limit of ≤ 0.5 ml after 30 minutes based on the Karsten Tube Test, compelling manufacturers to increase the use of redispersible polymer powders (RDP) to enhance water resistance and durability. This has intensified innovation in polymer-modified wall putty and moisture-resistant construction materials.

With the January 1, 2026 compliance deadline, non-ISI marked wall putty is excluded from government tenders and RERA-approved housing projects, leading to rapid consolidation within the organized wall putty market. Tier-1 manufacturers are gaining competitive advantage, while unorganized players face significant barriers, driving formalization and quality-driven competition across the construction chemicals sector.

Market Trend: China GB/T 41657-2025 Standard Boosting Hygrothermal Stability in High-Humidity Regions

China’s GB/T 41657-2025 standard is redefining performance expectations in the Asia Pacific wall putty market, particularly in high-humidity regions impacted by the Southern Monsoon climate. The regulation prioritizes hygrothermal stability over traditional aesthetic metrics such as smoothness, aligning product development with long-term durability in challenging environmental conditions.

The standard requires a wet-state bond strength of ≥ 0.4 MPa after 168 hours of continuous water immersion, addressing common issues such as bubbling and chalking associated with conventional gypsum-based putty. This requirement is accelerating the adoption of moisture-resistant wall putty and cement-based formulations designed for humid climates.

In addition, the mandated Shore D surface hardness of ≥ 55 is pushing manufacturers toward higher-grade white cement and refined mineral fillers. This trend is enhancing the durability of wall putty during high-traffic construction phases and reinforcing the demand for high-strength wall finishing materials across residential and commercial infrastructure projects.

Market Opportunity: Antimicrobial Wall Putty with Nano Silver and Zinc Oxide Enhancing Indoor Hygiene Standards

The growing focus on healthy building materials under WELL v2 and Fitwel standards is creating strong opportunities for antimicrobial wall putty solutions in the global construction materials market. The integration of nano-silver and zinc oxide (ZnO) into wall putty formulations is enabling pathogen reduction rates exceeding 99.9% against bacteria such as S. aureus and E. coli, as validated by ISO 22196 testing protocols.

Unlike conventional antimicrobial coatings applied at the paint layer, these advanced wall putties provide long-lasting protection at the substrate level. They demonstrate zero fungal growth, achieving Rating 0 under ASTM G21 even after 21 days of exposure to high-moisture environments. This makes antimicrobial wall putty particularly valuable in healthcare infrastructure, laboratories, and educational institutions where hygiene compliance is critical.

Additionally, zinc oxide-based wall putty is emerging as a functional indoor air quality solution, acting as a photocatalytic surface capable of reducing formaldehyde concentrations by 15% to 20%. This dual functionality positions antimicrobial wall putty as a premium segment within the green construction materials market.

Market Opportunity: Low-VOC Wall Putty Innovations Supporting Green Building Certification and Sustainability Targets

The tightening of global green building standards such as LEED v4.1 and BREEAM 2025 is driving significant opportunities for low-VOC wall putty products. Advanced formulations are now achieving VOC levels of ≤ 20 g/L, substantially below the traditional 50 g/L threshold, enabling developers to meet stringent requirements for LEED Platinum certification.

Compliance with European indoor air quality standards is also becoming a key differentiator, with wall putty products required to pass the 28-day AgBB chamber test, maintaining total volatile organic compound emissions of ≤ 1.0 mg/m³. This is accelerating the adoption of water-based, solvent-free binders and eco-friendly construction chemicals across residential and commercial projects.

Sustainability trends are further reinforced by the increasing use of post-industrial recycled materials in wall putty manufacturing. Products incorporating ≥ 15% recycled glass or marble dust are gaining preference in commercial tenders, particularly in office developments seeking sustainability premiums. This shift is aligning the wall putty market with circular economy principles while enhancing the appeal of green building materials among environmentally conscious developers and investors.

Wall Putty Market Share and Segmentation Insights

Cement-Based Wall Putty Leads with 44.8% Share Due to Cost Efficiency and Strong Adhesion

The cement-based wall putty segment dominates the global wall putty market with a 44.8% market share in 2025, driven by its cost-effectiveness, widespread availability, and superior performance in construction applications. In the construction chemicals and wall finishing materials market, cement-based putty is extensively used for interior and exterior wall leveling, particularly across high-growth regions such as Asia-Pacific, the Middle East, and Latin America, where cement-based construction remains the standard. Its excellent adhesion to concrete, brick, and plaster surfaces ensures a strong and durable base for paint application, significantly improving paint finish quality and longevity. Additionally, its water-resistant properties help prevent moisture penetration, efflorescence, and paint peeling, making it highly suitable for both residential and commercial buildings. As demand increases for durable, economical, and high-performance wall preparation solutions, cement-based putty continues to lead the global wall putty and surface preparation market.

Wholesale Channels Dominate with 47.6% Share Driven by Bulk Procurement and Regional Reach

The wholesale channel segment leads the wall putty market by distribution channel with a 47.6% market share in 2025, reflecting strong demand from construction contractors, builders, and large-scale infrastructure projects. Within the building materials distribution and construction supply chain market, wholesalers serve as key intermediaries, enabling bulk procurement of wall putty in 20–40 kg bags and pallet quantities, often at discounted pricing. This is particularly important for large painting contractors and real estate developers, who require consistent supply for ongoing projects. Additionally, wholesale networks play a crucial role in regional distribution, supplying hardware stores and smaller retailers across urban and rural markets, ensuring product availability for decentralized construction activities. Their ability to provide logistics support, inventory management, and wide geographic coverage makes them indispensable in the global wall putty market ecosystem, reinforcing their leadership as the preferred distribution channel.

Competitive Landscape Analysis of the Wall Putty Market

Birla White Strengthens Market Leadership with High-Performance Wall Putty Innovation

Birla White (Grasim Industries – Aditya Birla Group) dominates the wall putty market as the world’s largest producer of white cement, ensuring strong vertical integration and cost efficiency. Its Birla White WallCare HP line, scaled in 2026, features advanced water-resistant polymers delivering bonding strength above 1.2 N/mm², surpassing industry standards. The company’s extensive network of over 20,000 dealers and its “Expert Connect” initiative provide on-site training to more than 100,000 painters annually, reinforcing brand loyalty. With 65% of production powered by renewable energy, Birla White aligns with sustainability goals, making it a preferred choice for green building projects and high-durability wall finishing applications.

JK Cement Expands Premium Wall Putty Portfolio with Advanced Polymer Technology

JK Cement Ltd. is strengthening its position in the wall putty market through strategic diversification and innovation. Following its expansion into paints and adhesives with JK Maxx Paints, the company has created a strong cross-selling ecosystem for its JK WallMaxX series. The launch of JK WallMaxX Advanced in 2026 introduced a premium putty with a whiteness index exceeding 95, reducing primer usage by 15%. Its new manufacturing facility, commissioned in 2026 with a capacity of 50,000 MT annually, targets growing urban demand. JK Cement’s focus on luxury interiors and silky smooth finishes positions it strongly in high-end decorative coating applications.

Asian Paints Disrupts Ready-Mix Segment with Digital Supply Chain and VOC-Free Solutions

Asian Paints Ltd. is emerging as a disruptor in the wall putty market, particularly in the ready-mix paste segment where it holds a 12% share in urban renovation projects. Its Trugrip ready-to-use wall putty caters to convenience-driven consumers, while its unified warranty system across waterproofing, putty, and topcoat enhances customer retention. The company leverages AI-driven demand forecasting to maintain 98% product availability across 70,000+ retail outlets. In 2026, Asian Paints introduced a VOC-free, anti-fungal wall putty, targeting healthcare and educational infrastructure where indoor air quality standards are critical.

UltraTech Cement Drives High-Build Wall Putty Demand in Infrastructure Projects

UltraTech Cement (Aditya Birla Group) plays a crucial role in the wall putty market with its UltraTech Readiplast and WallCare brands, known for high-build applications allowing up to 3mm thickness in a single coat without cracking. The company reported 7.2% revenue growth in its building products segment in 2026, fueled by demand from smart city infrastructure projects. Its expansion of UltraTech Building Solutions outlets to over 3,500 locations provides a comprehensive retail ecosystem for construction materials. Backed by strong R&D in cement chemistry, UltraTech offers formulations with 20% higher coverage, enhancing efficiency in large-scale construction applications.

Nippon Paint Expands Quick-Dry and Green Wall Putty Solutions in Asia-Pacific

Nippon Paint Holdings is advancing in the wall putty market by transitioning toward a total coating solutions provider across Asia-Pacific. Its Vinilex Wall Putty, part of the “Green Choice” series, emphasizes sustainability and eco-friendly construction practices. The company’s quick-dry acrylic putty, developed in 2026, cures in under 90 minutes, enabling same-day painting cycles even in humid climates. Leveraging its N-Prime digital platform, Nippon Paint provides real-time surface quality analysis for large-scale projects. With strong dominance in Southeast Asia—accounting for 42.3% of global growth volume—the company is well-positioned in rapidly urbanizing construction markets.

India Driving White Cement-Based Wall Putty Demand Through Housing Boom and Premium Finishes

India has emerged as the global growth engine for the wall putty market, particularly in the white cement-based wall putty segment, driven by rapid urbanization and government-backed housing initiatives. Programs such as Pradhan Mantri Awas Yojana (PMAY) 2.0 are accelerating the adoption of high-quality wall finishing materials, significantly boosting demand for smooth-finish and durable putty solutions across urban housing projects.

Technological advancements are reshaping the market with the introduction of smart-flow wall putty formulations, which reduce application time and enhance workability. Strategic investments by major players are expanding production capacity, integrating wall putty into broader decorative coating ecosystems. Key applications include water-resistant exterior wall putty for coastal high-rise developments, addressing challenges such as monsoon moisture and humidity. Expansion of polymer-modified putty plants is supporting the premium residential segment, while regulatory measures like the Quality Control Order (QCO) 2026 are ensuring consistent quality standards. These developments position India as a dominant hub for high-performance and cost-effective wall putty solutions.

China Advancing High-Performance Polymer-Based Wall Putty with Low-VOC Innovations

China is transitioning rapidly in the wall putty industry, shifting from traditional gypsum fillers to advanced acrylic and vinyl-based formulations that align with stringent environmental regulations. The launch of bio-based, low-formaldehyde wall putty is addressing growing demand in sensitive sectors such as healthcare and education.

Technological advancements include the deployment of machine-applied wall putty systems, enabling automated, defect-free finishes for large-scale construction projects. Government initiatives promoting low-VOC materials are accelerating adoption of eco-friendly wall putty solutions, particularly in smart city developments. Strategic investments in high-elasticity putty formulations are enhancing crack resistance in modern infrastructure.

Key applications include the use of UV-resistant exterior wall putty for prefabricated building panels, ensuring long-term durability under varying environmental conditions. Expansion of production facilities targeting DIY markets is further strengthening China’s position as a leader in high-performance and sustainable wall putty technologies.

United States Driving Sustainable Wall Putty Solutions for Green Buildings and Drywall Systems

The United States is witnessing steady growth in the wall putty market, driven by the increasing adoption of green building materials and advanced drywall systems. Regulatory enforcement under the Clean Air Act is accelerating the transition toward HAP-free wall leveling compounds, ensuring compliance with environmental standards.

Technological innovations include the development of lightweight wall putty formulations, reducing transportation costs and carbon footprint while maintaining performance. Strategic investments in automated production systems are improving efficiency and supporting large-scale infrastructure projects.

Key applications include the use of mould-resistant acrylic wall putty in residential construction, particularly in high-humidity regions. The emergence of one-coat wall putty systems is reducing labor requirements and improving project timelines, addressing challenges in construction labor costs. These developments position the U.S. as a key market for sustainable and high-performance wall putty solutions.

Germany Leading Circular Economy Wall Putty Innovations and High-End Construction Applications

Germany is at the forefront of sustainable wall putty technologies, focusing on circular economy integration and advanced building materials. Regulatory frameworks under EU Ecodesign standards are promoting the adoption of digital product passports, ensuring transparency in material composition and recyclability.

Innovations in water-soluble wall putty binders are enabling easy removal and recycling of coatings, supporting sustainable construction practices. Technological advancements include the development of thermal-bridge wall putty, incorporating aerogel particles to enhance insulation performance in renovated buildings.

Industrial expansion is supporting the production of high-performance gypsum-polyurethane hybrid putty, offering superior acoustic and structural benefits. Key applications include precision-grade putty for luxury retail spaces, where seamless finishes are essential. Government initiatives promoting breathable mineral putty for public infrastructure are further driving adoption, positioning Germany as a leader in eco-friendly and high-performance wall putty solutions.

Saudi Arabia Driving High-Temperature Resistant Wall Putty for Mega Infrastructure Projects

Saudi Arabia is emerging as a significant market in the wall putty sector, driven by large-scale infrastructure developments under Vision 2030. The need for coatings that withstand extreme environmental conditions is fueling demand for high-temperature resistant wall putty solutions.

Technological advancements include the development of UV-stable and sand-abrasion resistant putty, designed to maintain performance under intense desert conditions. Government mandates requiring high solar reflectance index materials are improving energy efficiency in urban developments.

Key applications include salt-spray resistant wall putty for coastal projects and durable exterior finishes for mega-projects like NEOM. Expansion of local manufacturing facilities is strengthening supply chains, ensuring availability of high-performance materials. Regulatory standards ensuring long-term durability are further driving adoption, positioning Saudi Arabia as a key market for climate-resilient wall putty technologies.

Brazil Expanding Sustainable Wall Putty Solutions for Urban Renewal and Drywall Applications

Brazil is emerging as a strong player in the wall putty market, leveraging its abundant gypsum resources and focus on sustainable construction practices. Expansion of production facilities is supporting the growing demand for ready-to-use vinyl wall putty, particularly in urban housing projects.

Technological advancements include the development of agro-waste-based wall putty, reducing carbon footprint while maintaining performance. Government initiatives promoting sustainable materials are accelerating adoption of eco-friendly solutions in infrastructure projects.

Key applications include flexible acrylic wall putty for high-rise buildings, designed to withstand structural movement without cracking. Product innovations such as anti-humidity interior putty are addressing challenges in tropical climates, improving indoor air quality and durability. These developments position Brazil as a key market for sustainable and cost-effective wall putty solutions in Latin America.

Wall Putty Market Report Scope

Wall Putty Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$5.6 Billion

|

|

Market Size (2032)

|

$9 Billion

|

|

Market Growth Rate

|

7%

|

|

Segments

|

By Type (Cement-Based Wall Putty, Acrylic-Based Wall Putty, Gypsum-Based Wall Putty, Polymer-Modified Wall Putty, Lime-Based Wall Putty), By Form (Powdered Form, Ready-to-Use Paste), By Application (Interior Walls, Exterior Walls), By End-User Industry (Residential, Commercial, Industrial, Institutional), By Distribution Channel (Direct Sales, Retail Sales, Online, Wholesale Channels), By Pack Size (Small Packs, Medium Packs, Large)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Asian Paints Ltd., UltraTech Cement Limited, J.K. Cement Limited, Berger Paints India Limited, Kansai Nerolac Paints Limited, Nippon Paint Holdings Co., Ltd., AkzoNobel N.V., Saint-Gobain Weber, Mapei S.p.A., Sika AG, Walplast Products Pvt. Ltd., Pidilite Industries Limited, Meichao Group Co., Ltd., SKShu Paint Co., Ltd., Trimurti Plant and Industries Pvt. Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Wall Putty Market Segmentation

By Type

- Cement-Based Wall Putty

- Acrylic-Based Wall Putty

- Gypsum-Based Wall Putty

- Polymer-Modified Wall Putty

- Lime-Based Wall Putty

By Form

- Powdered Form

- Ready-to-Use Paste

By Application

- Interior Walls

- Exterior Walls

By End-User Industry

- Residential

- Commercial

- Industrial

- Institutional

By Distribution Channel

- Direct Sales

- Retail Sales

- Online

- Wholesale Channels

By Pack Size

- Small Packs

- Medium Packs

- Large

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Wall Putty Industry

- Asian Paints Ltd.

- UltraTech Cement Limited

- J.K. Cement Limited

- Berger Paints India Limited

- Kansai Nerolac Paints Limited

- Nippon Paint Holdings Co., Ltd.

- AkzoNobel N.V.

- Saint-Gobain Weber

- Mapei S.p.A.

- Sika AG

- Walplast Products Pvt. Ltd.

- Pidilite Industries Limited

- Meichao Group Co., Ltd.

- SKShu Paint Co., Ltd.

- Trimurti Plant & Industries Pvt. Ltd.

*- List not Exhaustive